- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Aramid Fiber Market Size, Share & Forecast | CAGR 7.3%

Global Aramid Fiber Market Size, Share, Growth Analysis By Fiber Type (Para-Aramid Fiber, Meta-Aramid Fiber, Copolymer Aramid Fiber), By Form (Filament Yarn, Staple Fiber, Pulp/Fibrid, Woven & Non-Woven Fabric, Composite Prepreg), By Application (Ballistic Protection, Aerospace Composites, Protective Apparel, Automotive Parts), By End-Use Industry, Market Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

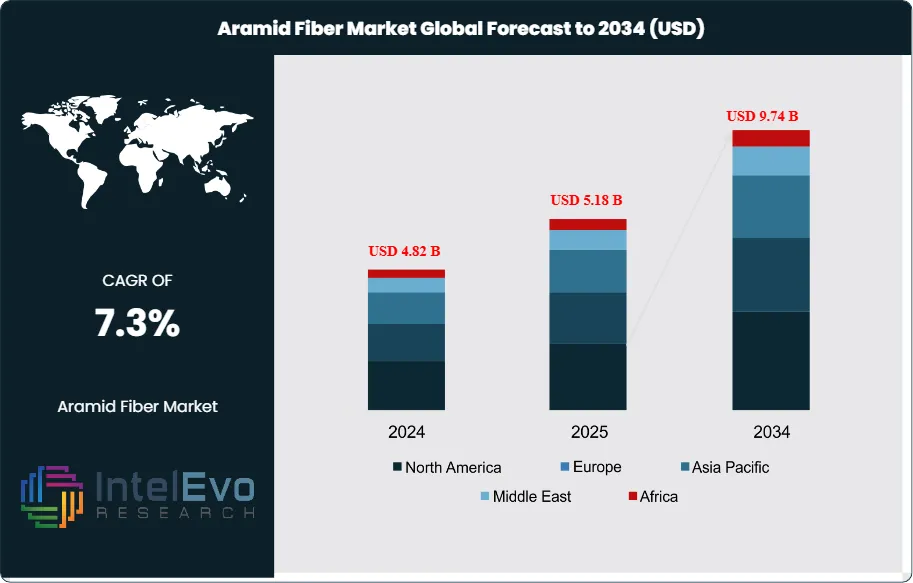

| USD 5.18 Billion | USD 9.74 Billion | 7.3% | Asia Pacific, 38.6% |

The Aramid Fiber Market was valued at approximately USD 4.82 Billion in 2024 and reached USD 5.18 Billion in 2025. The market is projected to grow to USD 9.74 Billion by 2034, expanding at a CAGR of 7.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 4.56 Billion over the analysis period, driven by intensifying demand across defense ballistic protection, automotive light weighting, EV battery safety systems, telecommunications cable reinforcement, and aerospace composite applications where aramid fiber's exceptional tensile strength-to-weight ratio delivers measurable performance advantages over steel, glass, and standard polymer alternatives.

Get More Information about this report -

Request Free Sample ReportAramid fiber is a class of heat-resistant, high-strength synthetic fibers in which the fiber-forming substance is a long-chain synthetic polyamide with at least 85% of amide linkages attached directly to two aromatic rings. The two primary commercial variants, para-aramid and meta-aramid, serve fundamentally different applications: para-aramid fiber (tensile strength 2,800-3,600 MPa, modulus 60-120 GPa) is used in ballistic protection, tire reinforcement, friction products, and structural composites; meta-aramid fiber (continuous service temperature 200-370 degrees Celsius, limiting oxygen index 28-32%) is used in protective apparel, electrical insulation, and high-temperature filtration. The aramid fiber market is defined by high barriers to entry, including polymerization technology complexity, capital-intensive spinning equipment, and strict defense procurement qualification cycles spanning 24-36 months.

The aramid fiber market is shaped by defense spending acceleration, automotive lightweighting mandates, and telecommunications infrastructure expansion. Global defense expenditure exceeded USD 2.4 Trillion in 2024 per the Stockholm International Peace Research Institute (SIPRI), with NATO members collectively committing to 2% of GDP defense spending targets that directly increase procurement volumes for body armor, armored vehicle spall liners, and ballistic helmets containing para-aramid fiber. Automotive demand is driven by EU CO2 emission standards mandating 95 g/km fleet averages and US Corporate Average Fuel Economy (CAFE) standards targeting 62.4 mpg by 2032, creating structural demand for aramid fiber-reinforced composite components that reduce vehicle mass by 30-50% versus steel equivalents. Fiber-to-the-home (FTTH) deployment, targeting 500 million connected households globally by 2030 per the FTTH Council, generates sustained demand for aramid-reinforced optical fiber cable.

Regional dynamics in the aramid fiber market reflect both defense procurement patterns and industrial manufacturing concentration. Asia Pacific leads with 38.6% share at USD 2.00 Billion in 2025, driven by Chinese aramid capacity expansion, Japanese technology leadership from Teijin and Toray, and Korean scale-up by Hyosung and Kolon. North America holds 28.8% share at USD 1.49 Billion, anchored by DuPont Kevlar production and US Department of Defense procurement volumes. Supply chain concentration remains a strategic concern: three companies (DuPont, Teijin, Hyosung) control approximately 62% of global para-aramid production capacity, creating supply security sensitivities for defense and critical infrastructure end-users.

Technology development in the aramid fiber market is focused on ultra-high-modulus para-aramid grades, recycled-content aramid formulations, and hybrid aramid-carbon fiber composites. Ultra-high-modulus para-aramid fibers achieving 180-220 GPa modulus, a 50% improvement over standard grades, are entering commercial qualification for next-generation body armor systems where reduced areal density directly reduces soldier load burden. Recycled aramid fiber, recovered from end-of-life body armor, industrial gaskets, and production waste through dissolution and re-spinning processes, achieved commercial production milestones in 2025 with Teijin's Twaron ECO range offering 30% recycled content certified under the Global Recycled Standard (GRS).

, By Form (Filament Yarn, Staple Fiber, Pulp/Fibrid, Woven & Non-Woven Fabric, Composite Prepreg), By Application (Ballistic Protection, Aerospace Composites, Protective Apparel, Automotive Parts), By End-Use Industry, Market Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The aramid fiber market was valued at USD 5.18 Billion in 2025 and is projected to reach USD 9.74 Billion by 2034, expanding at a CAGR of 7.3% across the 2026-2034 forecast period.

- Segment Dominance: Para-aramid fiber leads the By Fiber Type segment with 68.2% market share in 2025, valued at USD 3.53 Billion, reflecting dominant demand from ballistic protection, tire reinforcement, and composite applications where tensile strength exceeding 2,800 MPa is a non-negotiable specification.

- Segment Dominance: Defense and security leads the By End-Use Industry segment with 26.5% share in 2025, representing USD 1.37 Billion in revenue, supported by record global defense spending exceeding USD 2.4 Trillion annually and accelerating body armor modernization programs across NATO, AUKUS, and Indo-Pacific defense alliances.

- Driver: Rising global defense budgets, with NATO members committing to a combined USD 380 Billion increase in defense spending between 2024 and 2028, are the primary demand driver, directly increasing procurement volumes for para-aramid ballistic protection systems by an estimated 8-12% annually.

- Restraint: High production cost of para-aramid fiber, averaging USD 28-42 per kilogram versus USD 2-4 per kilogram for E-glass fiber, limits adoption in cost-sensitive industrial applications and constrains market penetration in price-competitive emerging economy segments by an estimated 15-20%.

- Opportunity: EV battery safety and thermal protection applications represent a USD 1.4 Billion incremental opportunity by 2034, with aramid fiber thermal barriers, battery cell separators, and pack-level protection systems specified by 8 of the top 10 global EV manufacturers.

- Trend: Recycled and circular-economy aramid fiber products are the defining sustainability trend, with Teijin's Twaron ECO and DuPont's Kevlar recycling program collectively targeting 15% recycled content across aramid fiber output by 2028, up from under 3% in 2023.

- Regional Analysis: Asia Pacific leads all regions with a 38.6% share in 2025, representing USD 2.00 Billion in revenue, driven by Chinese para-aramid capacity expansion, Japanese technology leadership from Teijin and Toray, and Korean production scaling by Hyosung.

Competitive Landscape Overview

The aramid fiber market exhibits high concentration in 2025, with the top four producers — DuPont, Teijin, Hyosung Advanced Materials, and Toray — collectively controlling approximately 62% of global para-aramid production capacity and 54% of total market revenue. Competition is technology-driven, centered on fiber tensile strength grades, modulus performance, thermal stability specifications, and defense procurement qualification status. Chinese producers, led by Yantai Tayho, Hebei Silicon Valley Chemical, and X-FIPER, are accelerating capacity additions and international certification efforts that are intensifying pricing competition in the mid-tier para-aramid and meta-aramid segments. Three capacity expansion investments exceeding USD 150 Million each were announced in 2024-2025, signaling sustained supply-side capital commitment.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product / Platform | Geo Strength | Recent Strategic Move (2024-2026) |

| DuPont de Nemours | USA | Leader | Kevlar Para-Aramid Fiber | North America / Global | Commissioned USD 500M Kevlar capacity expansion at Richmond, VA facility (Q1 2025), adding 5,000 tonnes/year to meet defense and EV demand. |

| Teijin Limited | Japan | Leader | Twaron / Technora Aramid | Asia Pacific / Global | Launched Twaron ECO range with 30% recycled aramid content certified under GRS (Global Recycled Standard) for industrial applications (Mar 2025). |

| Hyosung Advanced Materials | South Korea | Leader | Alkex Meta-Aramid Fiber | Asia Pacific | Completed KRW 280B (USD 210M) aramid plant expansion in Ulsan (Jun 2025), doubling annual para-aramid production capacity to 10,000 tonnes. |

| Toray Industries | Japan | Leader | Torayca Aramid Composites | Asia Pacific / Europe | Entered strategic supply agreement with Airbus for aramid composite structural components across A350 and A320neo platforms (Sep 2025), valued at EUR 320M. |

| Kolon Industries | South Korea | Challenger | Heracron Para-Aramid | Asia Pacific / North America | Invested USD 150M in Heracron production line expansion in Gumi, South Korea, targeting 3,500 tonnes/year incremental para-aramid capacity (2025). |

| Yantai Tayho Advanced Materials | China | Challenger | Taparan Para-Aramid | Asia Pacific | Achieved ISO 9001 and EN 469 certification for para-aramid fiber used in European firefighter protective apparel (Q4 2024), opening EU export channels. |

| Kermel (Baikowski Group) | France | Niche Player | Kermel Meta-Aramid Fiber | Europe | Secured EUR 45M French Ministry of Armed Forces contract for military-grade meta-aramid protective garments (Jan 2026). |

| SRO Aramid (Kamensk) | Russia | Niche Player | Rusar / Armos Para-Aramid | Russia / CIS | Expanded Rusar production capacity by 1,200 tonnes/year at Kamensk-Shakhtinsky facility to serve Russian defense contracts (2025). |

| Hebei Silicon Valley Chemical | China | Niche Player | Aoshen Meta-Aramid Fiber | Asia Pacific | Completed 3,000 tonnes/year meta-aramid fiber plant in Shijiazhuang, becoming the third-largest meta-aramid producer globally (Mar 2025). |

| X-FIPER New Material | China | Niche Player | X-FIPER Para-Aramid | Asia Pacific | Received Chinese National Defense Science and Technology Award for high-modulus para-aramid fiber achieving 3,600 MPa tensile strength (2025). |

By Fiber Type:

Para-aramid fiber dominates the aramid fiber market with a 68.2% share in 2025, valued at USD 3.53 Billion. Para-aramid's molecular structure, featuring rod-like polymer chains aligned along the fiber axis, delivers tensile strength of 2,800-3,600 MPa and elastic modulus of 60-120 GPa, performance levels that make it the reference material for ballistic protection, tire reinforcement, friction products, and structural composites. DuPont Kevlar and Teijin Twaron collectively represent over 75% of global para-aramid output. Meta-aramid fiber holds 26.8% share at USD 1.39 Billion, valued for its thermal stability (continuous service temperature 200-370 degrees Celsius) and flame resistance (limiting oxygen index 28-32%), making it the material of choice for firefighter protective apparel, military combat uniforms, hot-gas filtration, and electrical insulation applications. Nomex (DuPont) and Conex (Teijin) are the incumbent meta-aramid brands. Copolymer aramid fibers represent 5.0% at USD 259 Million, serving niche applications requiring specific combinations of thermal and mechanical performance not achievable with standard para or meta grades.

By Form:

Filament yarn represents 35.5% of the aramid fiber market at USD 1.84 Billion in 2025, serving ballistic fabric weaving, rubber reinforcement, and composite roving applications. Continuous filament para-aramid yarn in 1,000-3,000 denier formats is the primary commercial product for body armor fabric, tire cord, and cable reinforcement. Staple fiber holds 24.0% share at USD 1.24 Billion, used predominantly in meta-aramid protective apparel, filtration media, and friction product manufacturing. Pulp and fibrid forms account for 16.5% at USD 855 Million, consumed in gasket manufacturing, brake pad formulation, and specialty paper production where short-fiber reinforcement improves dimensional stability under thermal cycling. Fabric products (woven and non-woven aramid textiles) represent 15.0% at USD 777 Million. Composite prepreg formats hold 9.0% at USD 466 Million, growing at an above-market rate of 10.4% CAGR as aerospace and defense composite applications expand.

By Application:

Ballistic protection and body armor leads all applications with 22.5% market share at USD 1.17 Billion in 2025, reflecting the scale of global military and law enforcement procurement programs. The US Army's Soldier Protection System (SPS) and similar NATO body armor modernization programs specify para-aramid fabric in all soft armor panels. Friction products and gaskets hold 18.0% share at USD 932 Million, with aramid pulp replacing asbestos in brake pads, clutch plates, and industrial gaskets worldwide. Tire and rubber reinforcement accounts for 16.0% at USD 829 Million, where aramid cord reinforces high-performance tire sidewalls, conveyor belts, and V-belts. Optical fiber cable reinforcement represents 12.5% at USD 648 Million, growing at 9.2% CAGR as FTTH deployment accelerates. Aerospace and defense composites hold 10.5% at USD 544 Million. Protective apparel represents 9.0% at USD 466 Million. Automotive structural parts account for 6.5% at USD 337 Million. Electrical insulation holds 5.0% at USD 259 Million.

By End-Use Industry:

Defense and security commands 26.5% of the aramid fiber market at USD 1.37 Billion in 2025, the single largest end-use sector. Automotive and transportation holds 22.0% at USD 1.14 Billion, driven by lightweighting mandates and tire reinforcement demand. Aerospace accounts for 12.5% at USD 647 Million, with aramid honeycomb core structures used in aircraft interior panels, engine nacelles, and helicopter rotor blades. Telecommunications represents 11.0% at USD 570 Million, driven by optical fiber cable aramid strength member demand. Oil and gas holds 8.5% at USD 440 Million, consuming aramid in umbilical cables, riser reinforcement, and high-pressure gaskets. Construction accounts for 8.0% at USD 414 Million, primarily in concrete reinforcement and seismic retrofit applications. Industrial manufacturing represents 11.5% at USD 596 Million.

By Grade:

Standard modulus para-aramid fiber (60-80 GPa) holds 45% of the aramid fiber market, serving high-volume applications including tire reinforcement, friction products, and cable reinforcement. Intermediate modulus (80-115 GPa) holds 28%, used in ballistic protection fabrics and industrial composites. High modulus (115-145 GPa) represents 18%, targeted at aerospace composites and premium body armor systems where reduced areal density is specified. Ultra-high modulus (145-220 GPa), the newest commercial grade, accounts for 9% and is growing at 14% CAGR as defense procurement programs specify maximum strength-to-weight performance for next-generation soldier protection systems.

Regional Analysis

Asia Pacific

Asia Pacific leads the global aramid fiber market with a 38.6% share in 2025, valued at USD 2.00 Billion. China is the dominant country market, accounting for 44% of regional revenue at USD 880 Million, driven by state-supported aramid production capacity expansion under the 14th Five-Year Plan for New Materials Industry and a domestic military modernization program consuming over 4,500 tonnes of para-aramid annually. Yantai Tayho, Hebei Silicon Valley Chemical, and X-FIPER have collectively added over 8,000 tonnes of annual aramid capacity between 2022 and 2025. Japan holds 24% of Asia Pacific revenue at USD 480 Million, anchored by Teijin and Toray's globally leading aramid technology portfolios and a strong aerospace composite supply chain serving Boeing and Airbus programs. South Korea contributes 22% at USD 440 Million, with Hyosung and Kolon operating the fastest-growing para-aramid production complexes globally. India represents 8% at USD 160 Million, with growth driven by defense procurement under the Make in India initiative and telecommunications cable deployment supporting BharatNet broadband infrastructure. Asia Pacific is projected to grow at a CAGR of 8.4% to reach USD 4.14 Billion by 2034.

North America

North America accounts for 28.8% of the aramid fiber market in 2025, valued at USD 1.49 Billion. The United States represents 88% of regional revenue at USD 1.31 Billion, driven by Department of Defense procurement exceeding USD 2.2 Billion annually for body armor, vehicle protection, and helicopter composite components containing aramid fiber. DuPont's Kevlar manufacturing complex in Richmond, Virginia is the largest single-site para-aramid production facility globally, with the March 2025 capacity expansion adding 5,000 tonnes per year to meet defense and EV battery protection demand. The Department of Commerce's Office of Technology Evaluation has classified para-aramid as a critical material under Defense Production Act Title III, enabling federal investment in domestic capacity expansion. Canada contributes 9% of regional revenue at USD 134 Million, with aramid consumed in aerospace composites and cold-climate protective apparel. Mexico holds 3% at USD 45 Million. North America is forecast to grow at a CAGR of 6.8% to reach USD 2.70 Billion by 2034.

Europe

Europe represents 22.4% of the aramid fiber market in 2025, valued at USD 1.16 Billion. Germany leads European demand with 24% of regional revenue at USD 278 Million, driven by automotive OEM lightweighting programs from BMW, Mercedes-Benz, and Volkswagen specifying aramid composite components. France holds 18% at USD 209 Million, with Kermel serving as the domestic meta-aramid supplier for French and EU defense programs. The United Kingdom contributes 14% at USD 162 Million, with aramid composite demand concentrated in aerospace (Rolls-Royce, BAE Systems) and defense body armor programs. The Netherlands accounts for 12% at USD 139 Million as the location of Teijin's Twaron production facilities in Emmen and Delfzijl, representing the largest para-aramid manufacturing base in Europe. EU defense procurement policy under the European Defence Industrial Development Programme (EDIDP) is mandating supply chain sovereignty for ballistic fiber, directing procurement toward European-sourced aramid and creating guaranteed demand volumes for Teijin's Twaron and Kermel's meta-aramid operations. Europe is forecast to grow at 6.6% CAGR to reach USD 2.06 Billion by 2034.

Latin America

Latin America holds 5.8% of the aramid fiber market in 2025, valued at USD 300 Million. Brazil represents 55% of regional revenue at USD 165 Million, driven by military and police body armor procurement programs under Brazil's National Defense Strategy (Estrategia Nacional de Defesa) and industrial friction product manufacturing for the domestic automotive aftermarket. Mexico accounts for 32% at USD 96 Million, with aramid consumed in automotive components manufactured for USMCA export and telecommunications cable for CFE Telecomunicaciones broadband expansion. Argentina contributes 8% at USD 24 Million. Regional growth is constrained by limited domestic aramid production capacity, requiring near-complete import dependency from North American and Asian suppliers. Latin America is forecast to grow at 6.2% CAGR to reach USD 515 Million by 2034.

Middle East and Africa

Middle East and Africa accounts for 4.4% of the aramid fiber market in 2025, valued at USD 228 Million. Saudi Arabia leads MEA demand with 34% of regional revenue at USD 78 Million, driven by Saudi Arabian National Guard and Royal Saudi Land Forces body armor procurement and aramid-reinforced pipeline protection for Saudi Aramco infrastructure. The UAE contributes 28% at USD 64 Million, with defense procurement from Abu Dhabi-based EDGE Group specifying para-aramid for armored vehicle spall liners and personnel protection. South Africa holds 20% at USD 46 Million, primarily in mining industry friction products and defense applications. The African Development Bank's infrastructure investment program is creating early-stage demand for aramid-reinforced telecommunications cable across Sub-Saharan fiber optic backbone networks. MEA is projected to grow at 7.5% CAGR to reach USD 438 Million by 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Fiber Type

- Para-Aramid Fiber

- Meta-Aramid Fiber

- Copolymer Aramid Fiber

By Form

- Filament Yarn

- Staple Fiber

- Pulp / Fibrid

- Fabric (Woven / Non-Woven)

- Composite Prepreg

By Application

- Ballistic Protection & Body Armor

- Friction Products & Gaskets

- Tires & Rubber Reinforcement

- Optical Fiber Cable Reinforcement

- Aerospace & Defense Composites

- Protective Apparel

- Automotive Structural Parts

- Electrical Insulation

By End-Use Industry

- Defense & Security

- Automotive & Transportation

- Aerospace

- Oil & Gas

- Telecommunications

- Construction

- Industrial Manufacturing

By Grade / Performance

- Standard Modulus

- Intermediate Modulus

- High Modulus

- Ultra-High Modulus

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.18 B |

| Forecast Revenue (2034) | USD 9.74 B |

| CAGR (2025-2034) | 7.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Fiber Type, (Para-Aramid Fiber, Meta-Aramid Fiber, Copolymer Aramid Fiber), By Form, Filament Yarn, Staple Fiber, Pulp / Fibrid, Fabric (Woven / Non-Woven), Composite Prepreg), By Application, (Ballistic Protection & Body Armor, Friction Products & Gaskets, Tires & Rubber Reinforcement, Optical Fiber Cable Reinforcement, Aerospace & Defense Composites, Protective Apparel, Automotive Structural Parts, Electrical Insulation), By End-Use Industry, (Defense & Security, Automotive & Transportation, Aerospace, Oil & Gas, Telecommunications, Construction, Industrial Manufacturing), By Grade / Performance, (Standard Modulus, Intermediate Modulus, High Modulus, Ultra-High Modulus) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | DUPONT DE NEMOURS, TORAY INDUSTRIES, KERMEL (BAIKOWSKI GROUP), X-FIPER NEW MATERIAL, HUVIS CORPORATION, TEIJIN LIMITED, KOLON INDUSTRIES, SRO ARAMID (KAMENSK), JSC KAMENSKVOLOKNO, TAYHO ADVANCED MATERIALS, HYOSUNG ADVANCED MATERIALS, YANTAI TAYHO ADVANCED MATERIALS, HEBEI SILICON VALLEY CHEMICAL, CHINA NATIONAL BLUESTAR, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Form (Filament Yarn, Staple Fiber, Pulp/Fibrid, Woven & Non-Woven Fabric, Composite Prepreg), By Application (Ballistic Protection, Aerospace Composites, Protective Apparel, Automotive Parts), By End-Use Industry, Market Trends & Forecast 2026-2034")

, By Form (Filament Yarn, Staple Fiber, Pulp/Fibrid, Woven & Non-Woven Fabric, Composite Prepreg), By Application (Ballistic Protection, Aerospace Composites, Protective Apparel, Automotive Parts), By End-Use Industry, Market Trends & Forecast 2026-2034")

, By Form (Filament Yarn, Staple Fiber, Pulp/Fibrid, Woven & Non-Woven Fabric, Composite Prepreg), By Application (Ballistic Protection, Aerospace Composites, Protective Apparel, Automotive Parts), By End-Use Industry, Market Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Aramid Fiber Market?

The Global Aramid Fiber Market was valued at USD 4.82 Billion in 2024 and is projected to reach USD 9.74 Billion by 2034, growing at a CAGR of 7.3% from 2026 to 2034, driven by rising demand for lightweight high-strength materials, increasing adoption in aerospace and defense applications, expanding automotive composite usage, and growing need for advanced protective apparel and industrial reinforcement solutions.

Who are the major players in the Aramid Fiber Market?

DUPONT DE NEMOURS, TORAY INDUSTRIES, KERMEL (BAIKOWSKI GROUP), X-FIPER NEW MATERIAL, HUVIS CORPORATION, TEIJIN LIMITED, KOLON INDUSTRIES, SRO ARAMID (KAMENSK), JSC KAMENSKVOLOKNO, TAYHO ADVANCED MATERIALS, HYOSUNG ADVANCED MATERIALS, YANTAI TAYHO ADVANCED MATERIALS, HEBEI SILICON VALLEY CHEMICAL, CHINA NATIONAL BLUESTAR, OTHERS

Which segments covered the Aramid Fiber Market?

By Fiber Type, (Para-Aramid Fiber, Meta-Aramid Fiber, Copolymer Aramid Fiber), By Form, Filament Yarn, Staple Fiber, Pulp / Fibrid, Fabric (Woven / Non-Woven), Composite Prepreg), By Application, (Ballistic Protection & Body Armor, Friction Products & Gaskets, Tires & Rubber Reinforcement, Optical Fiber Cable Reinforcement, Aerospace & Defense Composites, Protective Apparel, Automotive Structural Parts, Electrical Insulation), By End-Use Industry, (Defense & Security, Automotive & Transportation, Aerospace, Oil & Gas, Telecommunications, Construction, Industrial Manufacturing), By Grade / Performance, (Standard Modulus, Intermediate Modulus, High Modulus, Ultra-High Modulus)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date