- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Artificial Lift System Market Size, Share & Growth Analysis | CAGR 5.8%

Global Artificial Lift System Market Size, Share & Industry Analysis By Lift Type (Electric Submersible Pumps, Rod Lift, Gas Lift, Progressing Cavity Pumps and Hydraulic Lift Systems), By Application (Onshore Oilfields, Offshore Production Platforms), By Component (Pump Assemblies and Core Lift Hardware, Monitoring Control & Automation Systems, Surface Equipment Drives & Power Systems, Services), By Reservoir Type (Conventional Reservoirs, Unconventional Reservoirs) Industry Regional Outlook, Competitive Landscape, Key Players, Market Dynamics, Technology Trends & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

| USD 13.71 Billion, 2025 | USD 22.82 Billion, 2034 | 5.8%, 2026–2034 | North America, 40.93%, 2025 |

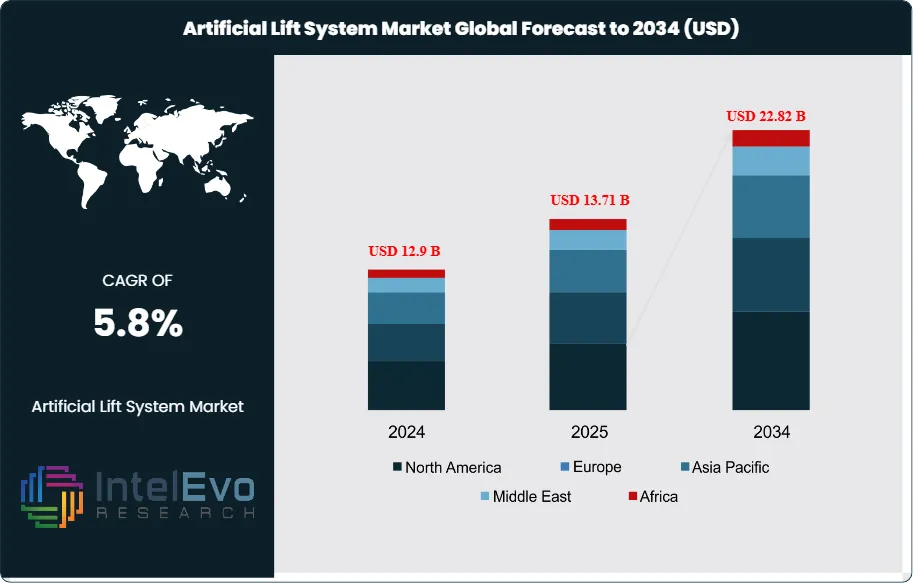

The Artificial Lift System Market was valued at approximately USD 12.9 Billion in 2024 and increased to USD 13.71 Billion in 2025. The market is projected to reach nearly USD 22.82 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 5.8% during the forecast period from 2026 to 2034. The CAGR is mathematically consistent over the nine-year period at about 5.82%. The Artificial Lift System Market is expanding because declining reservoir pressure, aging wells, and rising demand for production improvement are pushing operators to install lift systems earlier and keep them running longer across mature assets. Fortune Business Insights places the market at USD 13.71 Billion in 2025 and USD 22.82 Billion by 2034, with North America holding 40.93% share in 2025. Grand View also shows that electric submersible pumps accounted for 43.8% share in 2023, confirming that high-rate lift systems remain the core revenue engine of the market.

Get More Information about this report -

Request Free Sample ReportThe Artificial Lift System Market is being shaped by a broad shift in upstream spending from pure drilling expansion toward production support in existing wells. The IEA says lower oil prices and demand expectations are set to result in a 6% fall in upstream oil investment in 2025, yet mature wells still need lift systems to sustain commercial output. That keeps artificial lift demand relatively resilient even when broader oilfield activity softens. Mature onshore fields remain the largest demand base, but offshore and unconventional assets are also increasing lift-system intensity as operators pursue better recovery and lower unit production costs. Fortune identifies onshore as the leading application in 2025, while Mordor indicates that onshore installations represented 65.40% of market size in 2025 and conventional reservoirs retained 59.30% revenue share.

Technology is changing how the Artificial Lift System Market competes. The market is moving from equipment-only supply toward integrated lift, automation, and digital surveillance. Baker Hughes launched AI-powered functionality within Leucipa Lift Optimizer with Repsol in June 2025. Weatherford expanded long-term contracts for artificial lift equipment and services in Colombia and installed its first rod-lift system in Saudi Arabia’s Jafurah field in 2025. ChampionX introduced ESP production optimization services in February 2025, then became part of SLB in July 2025, giving SLB broader artificial lift, automation, and production chemistry depth. These developments show that digital control, monitoring, and production intelligence are now central to customer value.

Regionally, North America leads because of mature oil fields, shale density, and large installed ESP and rod-lift bases. Europe is gaining from mature-field redevelopment. Asia Pacific remains important through China, India, and Australia. Latin America is strengthening through Colombia, Argentina, and Mexico, while the Middle East is rising through Kuwait, Oman, and Saudi Arabia. Baker Hughes disclosed a multi-year Kuwait Oil Company contract for advanced artificial lift systems in December 2025 and later cited an Oman award covering about 1,400 wells. Risks remain clear. Lower spending can delay installations, and lift systems still carry high maintenance and power requirements. Even so, the Artificial Lift System Market remains structurally supported by mature-field decline and the need to keep existing wells flowing economically.

, By Application (Onshore Oilfields, Offshore Production Platforms), By Component (Pump Assemblies and Core Lift Hardware, Monitoring Control & Automation Systems, Surface Equipment Drives & Power Systems, Services), By Reservoir Type (Conventional Reservoirs, Unconventional Reservoirs) Industry Regional Outlook, Competitive Landscape, Key Players, Market Dynamics, Technology Trends & Forecast 2026–2034")

Key Takeaways

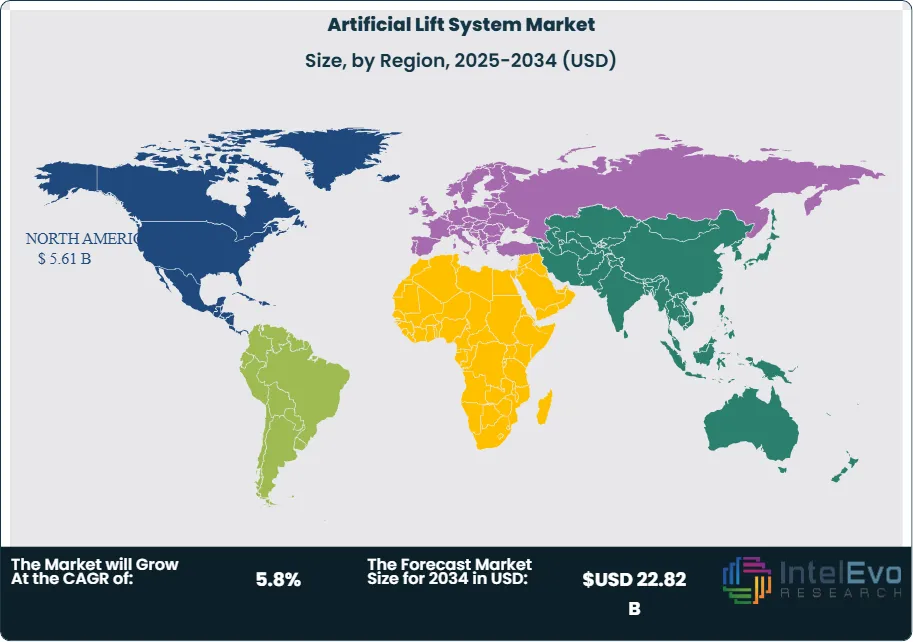

- Market Growth: The Artificial Lift System Market stood at USD 13.71 Billion in 2025 and is projected to reach USD 22.82 Billion by 2034 at a 5.8% CAGR over 2025–2034. North America held the largest regional share at 40.93% in 2025.

- Segment Dominance: Electric submersible pumps remained the top lift type with an estimated 42.0% share in 2025, equal to about USD 5.76 Billion, 2025. Grand View’s market tracking also identifies ESPs as the dominant product family, with 43.8% share in 2023.

- Segment Dominance: Onshore application led with 65.4% share in 2025, equal to about USD 8.97 Billion, 2025. Fortune and Mordor both identify onshore as the leading application in 2025.

- Driver: The main driver is declining reservoir pressure in aging wells. Industry sources identify mature field pressure depletion as a core growth factor, while conventional reservoirs still accounted for 59.3% of 2025 revenue.

- Restraint: The main restraint is softer upstream investment and drilling activity. The IEA expects upstream oil investment to fall 6.0% in 2025, while Weatherford reported lower artificial lift activity affected its first-quarter 2025 segment performance.

- Opportunity: The biggest opportunity lies in digitally managed lift systems and large Middle East field programs. Baker Hughes secured a multi-year Kuwait award in December 2025 and later cited an Oman deployment covering around 1,400 wells.

- Trend: The dominant trend is automation and AI in lift-system control. AI adoption among reservoir engineers rose from 43% in 2024 to 56% in 2025, while Baker Hughes and ChampionX both expanded digital lift surveillance in 2025.

- Regional Analysis: North America led the Artificial Lift System Market with 40.93% share in 2025, equal to about USD 5.61 Billion, 2025. The region benefits from mature oil fields, shale density, and heavy installed lift-system infrastructure.

Competitive Summary

The Artificial Lift System Market is moderately consolidated. The top four companies, SLB, Baker Hughes, Weatherford, and Halliburton, accounted for an estimated 53.0% of 2025 market revenue. Competition is mainly technology-driven and geographic. Leaders win through full lift portfolios, digital control systems, field service reach, and strong positions in mature well basins. Competitive intensity increased in 2025–2026 through SLB’s completion of the ChampionX acquisition, Baker Hughes’ Kuwait award and Repsol AI lift initiative, and Weatherford’s six-year Colombia contracts and first Jafurah rod-lift installation.

Competitive Landscape Matrix

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

|---|---|---|---|---|---|

| SLB | US | Leader | Reda and broader ChampionX lift portfolio | North America, Middle East, Latin America | Completed the acquisition of ChampionX in Jul 2025, adding artificial lift, automation, and production technologies. |

| Baker Hughes | US | Leader | Leucipa Lift Optimizer and ESP systems | Middle East, North America, Latin America | Launched new AI-powered Leucipa Lift Optimizer functionality with Repsol in Jun 2025 and announced a Kuwait artificial lift award in Dec 2025. |

| Weatherford | US | Leader | Rod Lift, Gas Lift, PCP, ESP, ForeSite | Latin America, Middle East, Asia Pacific | Won four 6-year artificial lift contracts with Ecopetrol in Oct 2025 and commissioned its first rod-lift system in Jafurah in Jul 2025. |

| Halliburton | US | Leader | Intelligent completions and lift-related digital solutions | North America, Middle East, Offshore international | Expanded AI-driven artificial lift digital positioning in 2025 and pushed SmartWell-linked completion control systems in offshore awards. |

| NOV | US | Challenger | Extract ESP business and lift-related production systems | North America, Middle East | Reported in Q1 2025 that services and rentals improved due to a full-quarter contribution from its artificial lift business. |

| ChampionX | US | Challenger | Harbison-Fischer rod lift, Norris, Theta, Windrock, ESP optimization | North America, Latin America | Introduced ESP Production Optimization Services in Feb 2025 before being acquired by SLB in Jul 2025. |

| Novomet | UAE / Russia operating base | Niche Player | ImpalaESP systems | Middle East, CIS, Latin America | Announced new ImpalaESP stages for harsh environments in Jun 2025 with solids handling up to 3 g/l. |

| PCM Artificial Lift Solutions | France | Niche Player | PCP systems | Latin America, Middle East | Showcased updated PCP and artificial lift technologies at the 2025 SPE PCP Workshop in Cartagena. |

| Dover Artificial Lift | US | Niche Player | Sucker rod lift and plunger lift systems | North America | Continued operating one of the broadest North American rod-lift portfolios in 2025. |

| Borets | UAE | Niche Player | ESP systems | Middle East, Eurasia | Continued expanding Middle East ESP presence through Sawafi Borets’ regional operating footprint. |

By Lift Type

Electric submersible pumps led the Artificial Lift System Market with an estimated 42.0% share in 2025, equal to about USD 5.76 Billion, 2025. Grand View identifies ESPs as the largest lift technology family, accounting for 43.8% share in 2023, and the structural logic remains intact in 2025 because ESPs handle high flow rates, work across a broad range of well conditions, and remain especially important in offshore, deep wells, and high-volume production settings. Baker Hughes’ 2025 Middle East contract announcements and ChampionX’s 2025 ESP optimization service launch both support the view that ESPs still define the premium end of the market. The segment also benefits from rising use of digital surveillance, variable speed drives, and remote failure prediction tools, which improve run life and reduce intervention frequency. Competitive strength is highest among SLB, Baker Hughes, Weatherford, ChampionX, NOV, and Borets because they combine hardware with field service and control systems. ESPs should remain the largest lift-type segment through 2034, though their share gain will be moderate because rod lift and gas lift remain deeply entrenched in mature onshore fields.

Rod lift accounted for an estimated 28.0% share in 2025, equal to about USD 3.84 Billion, 2025. Rod lift remains essential in mature onshore wells because it is field-proven, cost disciplined, and well suited to lower-rate production environments. Weatherford’s first rod-lift commissioning at Saudi Arabia’s Jafurah field in 2025 shows that the technology is also finding room in new unconventional gas applications when operators need rugged and controllable lift systems. Rod lift gains from its large installed base in North America and Latin America, where operators often prefer systems that are easier to maintain, supported by local service networks, and compatible with digital monitoring retrofits. The segment is less exposed to extreme offshore conditions than ESP or gas lift, but it remains commercially strong because mature land wells still dominate installed lift volumes globally. Competitive intensity is strong among Weatherford, ChampionX, Dover Artificial Lift, and smaller regional suppliers. Through 2034, rod lift should hold a large installed-base advantage even if ESP systems continue to lead total revenue.

Gas lift held an estimated 16.0% share in 2025, equal to about USD 2.19 Billion, 2025. Gas lift remains important in offshore wells, deviated wells, and fields where gas handling infrastructure is already present. It benefits from fewer downhole moving parts and strong suitability for harsh operating environments. Weatherford continues to position premium and specialty gas-lift systems as key solutions, which supports the segment’s relevance in offshore and production-restoration use cases. Gas lift demand is especially strong in the Middle East, offshore Latin America, and selected high-pressure wells where operators value reliability and flow assurance over simple equipment cost. The segment faces competition from ESP systems where higher lift rates are needed, but it remains strategically important because it supports long well life and can be integrated into broader completion architectures. Growth through 2034 should remain healthy, particularly where operators seek lower intervention frequency and better handling of challenging flow conditions.

Progressing cavity pumps and hydraulic lift systems together represented an estimated 14.0% share in 2025, equal to about USD 1.92 Billion, 2025. This category serves heavy oil, solids-heavy, and lower-volume wells where conventional ESP or rod-lift approaches may not be the best fit. PCM Artificial Lift Solutions remains a visible specialist in PCP systems, while hydraulic lift stays relevant in selected offshore and difficult-well settings. The segment is more fragmented than ESP and rod lift because specialists, regional players, and niche engineering providers compete heavily. Even so, it plays a valuable role in mature-field redevelopment and production improvement where fluid properties or sand conditions make standard lift systems less effective. Through 2034, the segment should grow steadily rather than rapidly, with its strongest gains in heavy oil and technically difficult wells.

By Application

Onshore remained the dominant application in the Artificial Lift System Market with 65.4% share in 2025, equal to about USD 8.97 Billion, 2025. Fortune identifies onshore as the leading application in 2025, and Mordor gives a more specific estimate of 65.40%. This segment dominates because mature land fields and shale assets account for the largest installed lift base. Onshore wells also allow lower-cost installation, easier maintenance access, faster replacement cycles, and broader use of rod lift, PCP, and smaller ESP systems. North America, Argentina, Colombia, China, India, and large Middle East onshore fields all reinforce this structure. Weatherford’s Colombia contracts and Baker Hughes’ Kuwait deployment both support the continuing strength of onshore lift demand. The segment is more price competitive than offshore, but scale and repeat work keep it dominant in revenue terms. Through 2034, onshore should remain the largest application because mature land wells will continue to require lift-system replacement, digital upgrades, and service support.

Offshore held 34.6% share in 2025, equal to about USD 4.74 Billion, 2025. Offshore lift demand is smaller in installed volume, but higher in revenue per system because technical requirements, installation complexity, and intervention costs are much greater. ESPs and gas lift are especially important here. Fortune points to faster offshore growth as operators continue pursuing reserves in deepwater and harsh environments. Offshore lift systems are favored when operators need better reservoir drawdown, longer run life, and lower subsea intervention frequency. This segment benefits from activity in Brazil, the Gulf of Mexico, the North Sea, West Africa, and selected Asia Pacific gas projects. Competitive advantage is concentrated among large providers such as Baker Hughes, SLB, Weatherford, and Halliburton, which can pair lift equipment with offshore completions, digital monitoring, and production support. Offshore should outpace onshore in growth rate through 2034, but not in total revenue because the land-well installed base remains much larger.

By Component

Pump assemblies and core lift hardware accounted for an estimated 41.4% share in 2025, equal to about USD 5.68 Billion, 2025. Mordor identifies pump assemblies as the largest component category in 2025. This makes structural sense because pumps, rod strings, motors, gas-lift valves, and PCP hardware still represent the largest share of system capital cost across most lift installations. The segment gains from both new well installations and replacement cycles in aging fields. Baker Hughes, Weatherford, ChampionX, Novomet, Borets, and Dover all compete meaningfully here. Component demand remains closely tied to field activity, but it is more stable than pure rig-count-linked segments because installed lift systems need replacement and maintenance regardless of short-term drilling swings. Through 2034, pump assemblies should remain the largest component segment, though their share will gradually ease as digital monitoring and control layers capture more value.

Monitoring, control, and automation systems represented an estimated 26.0% share in 2025, equal to about USD 3.56 Billion, 2025. This segment is growing faster because operators want real-time surveillance, better equipment health visibility, and earlier warnings of lift instability, gas interference, or pump failure. ChampionX’s digital control and ESP production optimization services, Baker Hughes’ Leucipa Lift Optimizer, and Weatherford’s ForeSite-linked rod-lift offerings all point to the same commercial shift. This segment is less capital-heavy than pump hardware, but it carries high value because it improves production continuity and lowers workover frequency. It is also central to the AI trend now visible in artificial lift operations. Through 2034, monitoring and automation should gain share faster than any other component category because customers increasingly want lift systems that are observed, controlled, and adjusted remotely rather than only installed and serviced mechanically.

Surface equipment, drives, and power systems held an estimated 20.0% share in 2025, equal to about USD 2.74 Billion, 2025. This segment includes variable speed drives, surface pumping units, control panels, and related power and interface systems. It remains important because energy consumption, reliability, and ease of field adjustment all affect total lift-system economics. Weatherford’s Rotaflex PowerMag system and ChampionX digital lift controls show how surface equipment is becoming more electrically advanced and data-aware. The segment benefits from operators’ focus on equipment uptime and lower field labor demands. Growth should remain solid through 2034, though somewhat below the pace of digital monitoring software and services.

Services represented the remaining estimated 12.6% share in 2025, equal to about USD 1.73 Billion, 2025. Services cover installation, field surveillance, run-life analysis, failure diagnostics, and performance improvement support. The category remains smaller in direct revenue than equipment, but it is commercially important because artificial lift systems require continuous operational attention. Baker Hughes’ and Weatherford’s multi-year service contracts show that customers increasingly buy lift systems as part of a broader production package rather than as one-time equipment purchases. This segment should gain value through 2034 as more customers seek vendor-supported monitoring and field management.

By Reservoir Type

Conventional reservoirs held 59.3% share in 2025, equal to about USD 8.13 Billion, 2025. Mordor identifies conventional reservoirs as the larger revenue base in 2025. This remains logical because large conventional fields still dominate global producing asset inventories, especially in North America, the Middle East, Latin America, and parts of Asia Pacific. Conventional wells also tend to progress steadily into lift-system dependence as reservoir pressure declines. The segment benefits from huge installed field infrastructure, long well-life economics, and broad service availability. SLB, Baker Hughes, Weatherford, Halliburton, and ChampionX all hold strong positions here through full-lifecycle production support. Through 2034, conventional reservoirs will remain the largest reservoir-type segment because the global well inventory is still anchored in conventional production systems.

Unconventional reservoirs accounted for 40.7% share in 2025, equal to about USD 5.58 Billion, 2025. Mordor identifies unconventional formations as the highest-growth reservoir segment, with 8.55% CAGR through its forecast period. This segment is strongest in North America and is growing in selected Middle East gas developments. Unconventional wells increasingly require lift earlier in life because flow declines rapidly and operators are working larger volumes of horizontal wells. Rod lift, ESP, and plunger lift systems all play roles here depending on flow profile and completion design. Weatherford’s Jafurah rod-lift installation and ChampionX’s digital control positioning both support the market’s shift toward higher unconventional lift intensity. Through 2034, unconventional reservoirs should outgrow conventional reservoirs in rate terms, but not in total revenue because the conventional installed base remains larger.

Regional Analysis

North America Artificial Lift System Market

North America held 40.93% share of the Artificial Lift System Market in 2025, equal to about USD 5.61 Billion, 2025. Fortune identifies North America as the leading regional market in 2025. The region dominates because it combines mature oil fields, dense shale activity, the world’s largest installed rod-lift base, and strong penetration of ESP and digital lift-control systems. The United States is the core market, driven by shale, mature conventional wells, and a deep service ecosystem. Canada remains important through heavy oil, mature land wells, and ESP and PCP demand. Mexico contributes through mature production assets and offshore redevelopment. North America also benefits from the strongest concentration of major vendors, including SLB, Baker Hughes, Weatherford, Halliburton, ChampionX heritage operations, NOV, and Dover Artificial Lift. The main headwind is weaker drilling activity during low-price periods, but lift demand remains more resilient than some drilling-linked categories because producing wells still need support. North America should remain the largest regional market through 2034 even as the Middle East and Latin America grow strongly.

Europe Artificial Lift System Market

Europe represented an estimated 18.0% share in 2025, equal to about USD 2.47 Billion, 2025. Europe is smaller than North America in total lift-system volume, but it remains a valuable market because of mature-field redevelopment, strict well-economics discipline, and rising interest in digital field management. Germany, France, the UK, and Norway are the most relevant countries in this report structure. The UK and Norway dominate commercial demand because North Sea fields increasingly need lift support, production improvement, and longer run-life management. Germany and France are smaller in hydrocarbon output, but they remain relevant through engineering, service hubs, and energy transition-linked subsurface activity. Europe benefits from operators’ focus on extracting more value from aging assets rather than simply expanding drilling volume. The region should record healthy growth through 2034 because mature wells continue to shift toward lift dependence and operators increasingly favor digital monitoring to reduce intervention frequency. Competitive advantage lies mainly with Baker Hughes, Weatherford, SLB, Halliburton, and selected specialist suppliers.

Asia Pacific Artificial Lift System Market

Asia Pacific held an estimated 17.5% share in 2025, equal to about USD 2.40 Billion, 2025. The region remains strategically important because many fields are mature or pressure-depleted, while energy security concerns continue to support domestic production. China is the largest country market and continues to require lift systems across large mature onshore fields. India is growing through stronger production support activity and broader field modernization. Japan is smaller in direct upstream scale, but remains part of regional energy technology networks. Australia is strategically relevant because of mature fields, gas developments, and lift requirements in unconventional and offshore-linked operations. Asia Pacific also benefits from growing adoption of automated lift monitoring rather than only hardware replacement. The region is less saturated than North America, which gives vendors room to win new users as operators move toward more data-driven production management. Through 2034, Asia Pacific should remain one of the faster-growing regional markets, supported by pressure-depleted fields and broader digital adoption.

Latin America Artificial Lift System Market

Latin America accounted for an estimated 13.2% share in 2025, equal to about USD 1.81 Billion, 2025. The region is important because many producing fields require lift support to sustain commercial output and because operators increasingly combine equipment, services, and digital controls in one package. Brazil matters through mature offshore and onshore production support. Mexico remains relevant through legacy fields and production-enhancement needs. Argentina is significant because unconventional development continues to increase lift-system intensity in land operations. Weatherford’s 2025 awards in Argentina and Colombia show how artificial lift demand is spreading across the region beyond a few major offshore markets. Latin America’s main challenge is spending volatility, but the region still offers solid long-term opportunity because mature wells and production decline support steady lift demand. Through 2034, Latin America should outgrow some developed regions in percentage terms because digital lift systems are still expanding from a lower installed base.

Middle East & Africa Artificial Lift System Market

Middle East & Africa held an estimated 10.4% share in 2025, equal to about USD 1.43 Billion, 2025. The region has one of the strongest long-term growth profiles because giant mature fields, new unconventional gas developments, and rising service integration all support lift demand. Saudi Arabia is a key market, highlighted by Weatherford’s first rod-lift commissioning in Jafurah in 2025. The UAE remains important through mature-field production support and regional service capacity. South Africa is smaller today but remains part of the regional opportunity set in this report structure. The wider region gained further weight when Baker Hughes secured a multi-year Kuwait Oil Company contract and an Oman award covering around 1,400 wells. These developments show that the Middle East is moving toward larger-scale, digitally informed lift deployments. Through 2034, Middle East & Africa should gain share because national operators continue investing in field-life extension, lower decline rates, and stronger production surveillance.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Lift Type

- Electric Submersible Pumps

- Rod Lift

- Gas Lift

- Progressing Cavity Pumps and Hydraulic Lift Systems

By Application

- Onshore

- Offshore

By Component

- Pump Assemblies and Core Lift Hardware

- Monitoring, Control, and Automation Systems

- Surface Equipment, Drives, and Power Systems

- Services

By Reservoir Type

- Conventional Reservoirs

- Unconventional Reservoirs

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 13.71 B |

| Forecast Revenue (2034) | USD 22.82 B |

| CAGR (2025-2034) | 5.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Lift Type (Electric Submersible Pumps, Rod Lift, Gas Lift, Progressing Cavity Pumps and Hydraulic Lift Systems), By Application (Onshore, Offshore), By Component (Pump Assemblies and Core Lift Hardware, Monitoring, Control, and Automation Systems, Surface Equipment, Drives, and Power Systems, Services), By Reservoir Type (Conventional Reservoirs, Unconventional Reservoirs) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB, BAKER HUGHES, WEATHERFORD, HALLIBURTON, NOV, CHAMPIONX, DOVER ARTIFICIAL LIFT, BORETS, NOVOMET, PCM ARTIFICIAL LIFT SOLUTIONS, ACCESSESP, KUDU INDUSTRIES, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Onshore Oilfields, Offshore Production Platforms), By Component (Pump Assemblies and Core Lift Hardware, Monitoring Control & Automation Systems, Surface Equipment Drives & Power Systems, Services), By Reservoir Type (Conventional Reservoirs, Unconventional Reservoirs) Industry Regional Outlook, Competitive Landscape, Key Players, Market Dynamics, Technology Trends & Forecast 2026–2034")

, By Application (Onshore Oilfields, Offshore Production Platforms), By Component (Pump Assemblies and Core Lift Hardware, Monitoring Control & Automation Systems, Surface Equipment Drives & Power Systems, Services), By Reservoir Type (Conventional Reservoirs, Unconventional Reservoirs) Industry Regional Outlook, Competitive Landscape, Key Players, Market Dynamics, Technology Trends & Forecast 2026–2034")

, By Application (Onshore Oilfields, Offshore Production Platforms), By Component (Pump Assemblies and Core Lift Hardware, Monitoring Control & Automation Systems, Surface Equipment Drives & Power Systems, Services), By Reservoir Type (Conventional Reservoirs, Unconventional Reservoirs) Industry Regional Outlook, Competitive Landscape, Key Players, Market Dynamics, Technology Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Artificial Lift System Market?

The Global Artificial Lift System Market was valued at USD 12.9 Billion in 2024 and USD 13.71 Billion in 2025, projected to reach USD 22.82 Billion by 2034, growing at a CAGR of 5.8% from 2026–2034. Market growth is driven by rising demand to sustain production from aging oil wells, increasing deployment in unconventional fields, and adoption of digital monitoring and AI-enabled lift optimization technologies.

Who are the major players in the Artificial Lift System Market?

SLB, BAKER HUGHES, WEATHERFORD, HALLIBURTON, NOV, CHAMPIONX, DOVER ARTIFICIAL LIFT, BORETS, NOVOMET, PCM ARTIFICIAL LIFT SOLUTIONS, ACCESSESP, KUDU INDUSTRIES, Others

Which segments covered the Artificial Lift System Market?

By Lift Type (Electric Submersible Pumps, Rod Lift, Gas Lift, Progressing Cavity Pumps and Hydraulic Lift Systems), By Application (Onshore, Offshore), By Component (Pump Assemblies and Core Lift Hardware, Monitoring, Control, and Automation Systems, Surface Equipment, Drives, and Power Systems, Services), By Reservoir Type (Conventional Reservoirs, Unconventional Reservoirs)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Artificial Lift System Market

Published Date : 13 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date