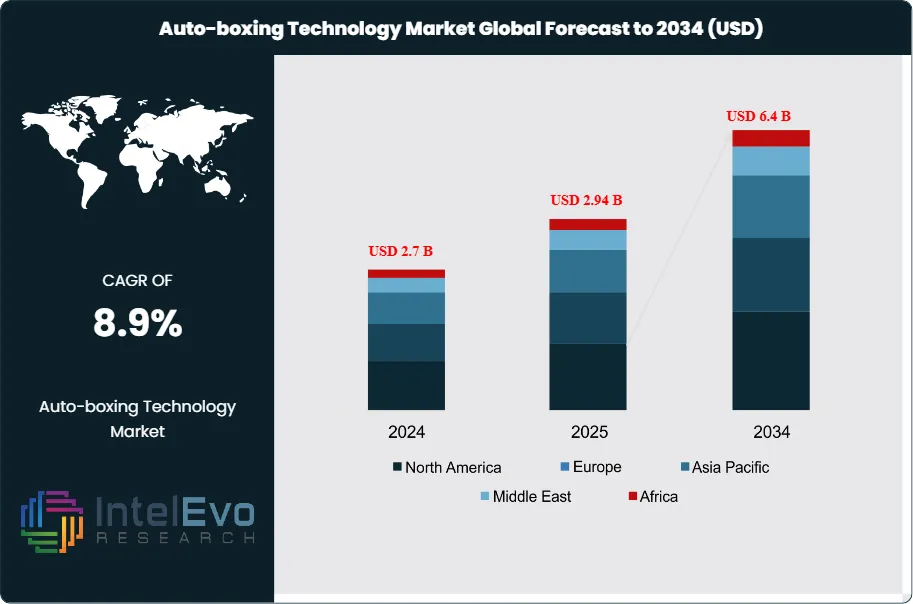

The Auto-boxing Technology Market is projected to grow from USD 2.7 Billion in 2024 to approximately USD 6.4 Billion by 2034, expanding at a CAGR of around 8.9% during 2025–2034. Rising e-commerce order volumes and the shift toward high-speed warehouse automation are significantly driving market adoption. Auto-boxing machines reduce labor dependency, packaging waste, and fulfillment time, making them essential for modern logistics networks. Growing investments in smart warehouses, AI-powered packaging workflows, and last-mile optimization are accelerating widespread deployment across industries. This dynamic market encompasses sophisticated automated packaging systems that revolutionize traditional packaging operations through intelligent dimensioning, adaptive sizing capabilities, and seamless integration with existing supply chain infrastructure.

Auto-boxing technology fundamentally transforms packaging workflows by deploying advanced sensor networks, artificial intelligence, and adjustable mechanical components to automatically measure product dimensions and configure optimal box sizes for each item. These intelligent systems eliminate guesswork in packaging decisions, ensuring precise fit-to-size solutions that protect contents during transit while minimizing material consumption. The technology dramatically accelerates packaging throughput rates, reduces operational dependencies on manual labor, and delivers measurable improvements in overall supply chain efficiency.

Market expansion is primarily driven by the explosive growth of global e-commerce, which has created unprecedented demand for scalable, high-speed packaging solutions capable of handling diverse product portfolios and fluctuating order volumes. The sector's evolution is further accelerated by critical labor market constraints, with manufacturers reporting up to 73% experiencing moderate to severe worker shortages, making automation an essential strategic imperative rather than optional enhancement. Companies implementing auto-boxing solutions report substantial operational benefits, including labor cost reductions of up to 88% and material savings averaging 29%.

Technological innovation continues reshaping market dynamics, with manufacturers integrating machine learning algorithms, IoT-enabled monitoring systems, and predictive maintenance capabilities into next-generation auto-boxing platforms. These advances enable real-time adaptation to varying product specifications without manual intervention, while providing comprehensive operational analytics and performance optimization insights. Sustainability considerations are increasingly influential, as businesses align packaging operations with environmental responsibilities through waste reduction, optimized material utilization, and support for eco-friendly packaging alternatives.

Regional market patterns reveal North America maintaining technological leadership, supported by advanced manufacturing infrastructure and early automation adoption, while Asia-Pacific emerges as the fastest-growing region with projected CAGR rates reaching 10.0% in key markets like China. The convergence of rising labor costs, expanding e-commerce penetration, and strengthening regulatory frameworks supporting automation investments positions auto-boxing technology as a cornerstone solution for modern packaging operations, enabling businesses to achieve operational excellence while maintaining competitive advantage in increasingly demanding market environments.

Key Takeaways

Market Growth: The global auto-boxing technology market is forecast to grow from USD 2.7 Billion in 2024 to USD 6.4 Billion by 2034, reflecting a healthy CAGR of 8.9%. Growth is primarily driven by the accelerating expansion of the e-commerce sector and the rising demand for automation solutions aimed at reducing labor costs and enhancing operational efficiency.

Component: The Solution segment commands a dominant market position, capturing over 79% market share in 2024, attributed to growing innovation in auto-boxing systems and demand for flexible protective packaging solutions, while Services segment is expected to register the fastest CAGR of 8.3%.

End-Use Industry: The Food segment leads with over 26.5% market share in 2024, driven by increasing packaged food demand and stringent food safety compliance requirements, while Retail & E-commerce segment is projected to achieve the fastest growth at 8.9% CAGR.

Driver: E-commerce sector expansion serves as the primary growth catalyst, with businesses requiring scalable, high-speed packaging solutions to handle diverse product portfolios and fluctuating order volumes, while addressing critical labor shortages with up to 73% of manufacturers experiencing moderate to severe worker shortages.

Restraint: High initial capital investment requirements create significant barriers, particularly for small and medium-sized enterprises, as advanced robotic system implementation, integration costs, and maintenance expenses demand substantial financial commitments that many organizations find challenging to justify.

Opportunity: Integration of artificial intelligence and machine learning technologies presents substantial growth potential, enabling real-time adaptation to varying product specifications, predictive maintenance capabilities, and comprehensive operational analytics that optimize packaging processes without manual intervention.

Trend: Sustainability-driven packaging optimization is emerging as a dominant trend, with auto-boxing systems delivering up to 29% material savings on average and 88% labor cost reductions, aligning packaging operations with environmental responsibilities through waste reduction and eco-friendly material support.

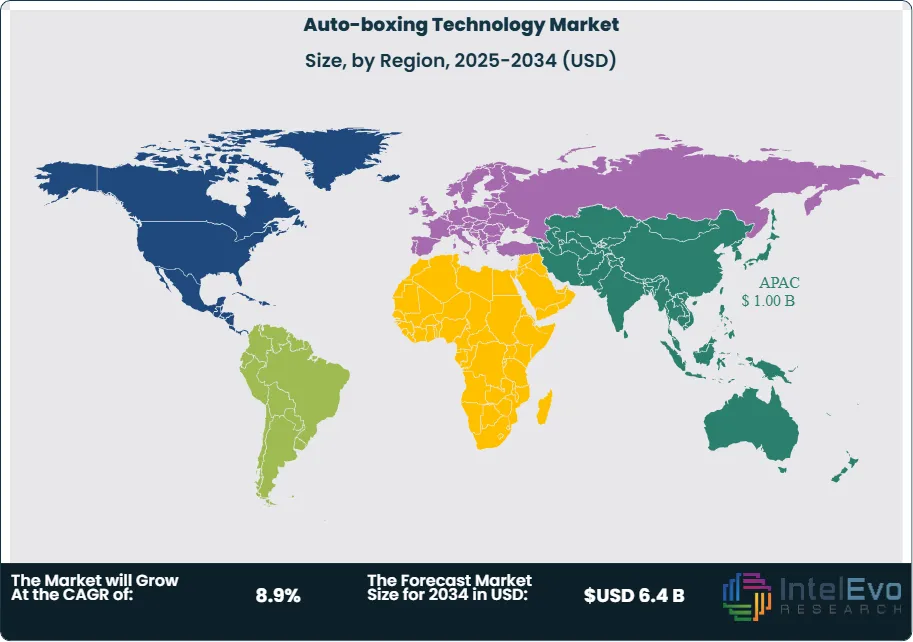

Regional Analysis: Asia Pacific dominates with over 36.8% market share in 2024, led by rapid e-commerce expansion and government automation initiatives, while China projects the fastest growth at 8.2% CAGR supported by manufacturing activities and strong e-commerce infrastructure, compared to North America's technological leadership and Europe's steady industrial adoption.

Component Analysis

The Solution segment establishes its market leadership through commanding over 80% of the global auto-boxing technology market in 2025. This comprehensive segment encompasses both hardware infrastructure and integrated software platforms that constitute the foundational architecture of automated packaging systems. The segment's dominant position reflects the critical importance of sophisticated technological systems capable of delivering precision, adaptability, and operational efficiency across diverse industrial applications.

Solution segment prominence derives from the accelerating demand for intelligent packaging automation that can seamlessly integrate with existing production lines while delivering measurable improvements in throughput and cost optimization. Modern auto-boxing solutions incorporate advanced machine learning algorithms, computer vision systems, and IoT connectivity to enable real-time dimensional analysis and optimal box configuration. These integrated systems deliver tangible benefits including up to 88% reduction in labor costs and 29% savings in material consumption, making them essential investments for competitive operations.

The Services segment demonstrates remarkable growth potential, projected to register the fastest expansion rate at 8.3% CAGR through 2030. This growth trajectory reflects the increasing complexity of auto-boxing implementations and the critical importance of ongoing maintenance, technical support, and system optimization services. As organizations invest in sophisticated automated packaging infrastructure, they require specialized expertise to maximize system performance, minimize downtime, and ensure continuous operational improvements that justify capital investments.

End-use Analysis

The Food industry maintains its leadership position within the auto-boxing technology landscape, capturing over 26% market share in 2025, driven by stringent regulatory compliance requirements and the imperative for contamination-free packaging processes. Food manufacturers increasingly adopt automated boxing solutions to eliminate human contact during packaging operations, ensuring adherence to food safety protocols while maintaining production velocity. The segment benefits from rising consumer preferences for convenient, packaged food products and the industry's need to scale operations efficiently while preserving product integrity throughout distribution networks.

The Beverages sector experiences steady adoption of auto-boxing technology, particularly among high-volume producers requiring consistent packaging quality and rapid processing capabilities. Beverage manufacturers leverage these systems to handle diverse container sizes and shapes while maintaining optimal protection during transportation. The Pharmaceuticals segment demonstrates significant growth potential, with automated boxing solutions addressing critical requirements for sterile packaging environments, precise dosage protection, and comprehensive traceability systems that support regulatory compliance throughout the supply chain.

The Retail & E-commerce segment emerges as the fastest-growing application area, projected to achieve 8.9% CAGR expansion through 2030, reflecting the explosive growth of online commerce and the corresponding demand for scalable, efficient packaging solutions. E-commerce operators require systems capable of processing high order volumes with diverse product specifications while optimizing shipping costs through right-sized packaging. Manufacturing industries increasingly integrate auto-boxing technology to streamline end-of-line operations, reduce packaging labor dependencies, and enhance overall production efficiency in competitive market environments.

Regional Analysis

Asia Pacific solidifies its market leadership position, commanding over 37% of the global auto-boxing technology market in 2025, supported by rapid industrial expansion and aggressive government automation initiatives across major economies. The region's dominance stems from explosive e-commerce growth, particularly in China and India, combined with manufacturing sector evolution toward Industry 4.0 principles. Government programs such as Singapore's Integrated Robotics & Automation Solutions initiative and China's Made in China 2025 strategy actively promote automation adoption, creating favorable conditions for auto-boxing technology proliferation throughout the region.

China specifically demonstrates exceptional growth potential with projected 8.2% CAGR expansion through 2030, driven by robust manufacturing activities, advanced e-commerce infrastructure, and substantial government support for industrial automation. Rising labor costs across Asia Pacific economies further incentivize automation adoption, while local manufacturing capabilities reduce implementation costs and enhance technology accessibility. The region's large consumer population drives demand for efficient packaging solutions across food, beverages, and consumer goods sectors.

North America maintains significant market presence with projected 7.3% CAGR growth, leveraging mature e-commerce infrastructure and high technology adoption rates among established companies. The region's market expansion reflects efforts to address substantial labor cost pressures, with hourly wages exceeding USD 40 in the United States, making automation investments financially attractive. Europe demonstrates steady growth supported by stringent environmental regulations that favor efficient, waste-reducing packaging solutions, while emerging markets in Latin America and the Middle East present long-term growth opportunities driven by increasing industrialization and foreign investment in automation technologies.

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

1.1. MARKET SNAPSHOT

1.2. KEY FINDINGS & INSIGHTS

1.3. ANALYST RECOMMENDATIONS

1.4. FUTURE OUTLOOK

2. RESEARCH METHODOLOGY

2.1. MARKET DEFINITION & SCOPE

2.2. RESEARCH OBJECTIVES: PRIMARY & SECONDARY DATA SOURCES

2.3. DATA COLLECTION SOURCES

2.3.1. COVERAGE OF 100+ PRIMARY RESEARCH/CONSULTATION CALLS WITH INDUSTRY STAKEHOLDERS

FIGURE 17 NORTH AMERICA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 18 NORTH AMERICA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 19 MARKET SHARE BY COUNTRY

FIGURE 20 LATIN AMERICA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 21 LATIN AMERICA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 22 MARKET SHARE BY COUNTRY

FIGURE 23 EASTERN EUROPE AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 24 EASTERN EUROPE AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 25 MARKET SHARE BY COUNTRY

FIGURE 26 WESTERN EUROPE AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 27 WESTERN EUROPE AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 28 MARKET SHARE BY COUNTRY

FIGURE 29 EAST ASIA AND PACIFIC AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 30 EAST ASIA AND PACIFIC AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 31 MARKET SHARE BY COUNTRY

FIGURE 32 SEA AND SOUTH ASIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 33 SEA AND SOUTH ASIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 34 MARKET SHARE BY COUNTRY

FIGURE 35 MIDDLE EAST AND AFRICA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 36 MIDDLE EAST AND AFRICA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 37 NORTH AMERICA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 38 U.S. AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 39 U.S. AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 40 CANADA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 41 CANADA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 42 LATIN AMERICA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 43 MEXICO AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 44 MEXICO AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 45 BRAZIL AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 46 BRAZIL AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 47 ARGENTINA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 48 ARGENTINA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 49 COLUMBIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 50 COLUMBIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 51 REST OF LATIN AMERICA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 52 REST OF LATIN AMERICA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 53 EASTERN EUROPE AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 54 POLAND AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 55 POLAND AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 56 RUSSIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 57 RUSSIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 58 CZECH REPUBLIC AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 59 CZECH REPUBLIC AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 60 ROMANIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 61 ROMANIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 62 REST OF EASTERN EUROPE AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 63 REST OF EASTERN EUROPE AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 64 WESTERN EUROPE AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 65 GERMANY AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 66 GERMANY AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 67 FRANCE AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 68 FRANCE AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 69 UK AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 70 UK AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 71 SPAIN AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 72 SPAIN AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 73 ITALY AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 74 ITALY AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 75 REST OF WESTERN EUROPE AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 76 REST OF WESTERN EUROPE AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 77 EAST ASIA AND PACIFIC AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 78 CHINA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 79 CHINA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 80 JAPAN AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 81 JAPAN AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 82 AUSTRALIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 83 AUSTRALIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 84 CAMBODIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 85 CAMBODIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 86 FIJI AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 87 FIJI AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 88 INDONESIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 89 INDONESIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 90 SOUTH KOREA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 91 SOUTH KOREA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 92 REST OF EAST ASIA AND PACIFIC AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 93 REST OF EAST ASIA AND PACIFIC AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 94 SEA AND SOUTH ASIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 95 BANGLADESH AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 96 BANGLADESH AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 97 NEW ZEALAND AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 98 NEW ZEALAND AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 99 INDIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 100 INDIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 101 SINGAPORE AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 102 SINGAPORE AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 103 THAILAND AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 104 THAILAND AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 105 TAIWAN AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 106 TAIWAN AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 107 MALAYSIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 108 MALAYSIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 109 REST OF SEA AND SOUTH ASIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 110 REST OF SEA AND SOUTH ASIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 111 MIDDLE EAST AND AFRICA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 112 GCC COUNTRIES AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 113 GCC COUNTRIES AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 114 SAUDI ARABIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 115 SAUDI ARABIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 116 UAE AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 117 UAE AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 118 BAHRAIN AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 119 BAHRAIN AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 120 KUWAIT AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 121 KUWAIT AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 122 OMAN AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 123 OMAN AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 124 QATAR AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 125 QATAR AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 126 EGYPT AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 127 EGYPT AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 128 NIGERIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 129 NIGERIA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 130 SOUTH AFRICA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 131 SOUTH AFRICA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 132 ISRAEL AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 133 ISRAEL AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 134 REST OF MEA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 135 REST OF MEA AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 136 U. S. MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 137 U. S. MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 138 CANADA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 139 CANADA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 140 MEXICO MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 141 MEXICO MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 142 CHINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 143 CHINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 144 JAPAN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 145 JAPAN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 146 INDIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 147 INDIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 148 SOUTH KOREA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 149 SOUTH KOREA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 150 SAUDI ARABIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 151 SAUDI ARABIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 152 UAE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 153 UAE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 154 EGYPT MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 155 EGYPT MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 156 NIGERIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 157 NIGERIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 158 SOUTH AFRICA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 159 SOUTH AFRICA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 160 GERMANY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 161 GERMANY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 162 FRANCE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 163 FRANCE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 164 UK MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 165 UK MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 166 SPAIN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 167 SPAIN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 168 ITALY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 169 ITALY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 170 BRAZIL MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 171 BRAZIL MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 172 ARGENTINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 173 ARGENTINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 174 COLUMBIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 175 COLUMBIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 176 GLOBAL AUTO-BOXING TECHNOLOGY CURRENT AND FUTURE MARKET KEY COUNTRY LEVEL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 177 FINANCIAL OVERVIEW:

Key Player Analysis

CMC Packaging Automation: CMC Packaging Automation emerges as a transformative market leader in 2025, establishing itself as a technology innovator through breakthrough solutions including the CMC Super Vertical and CMC Genesys PRIMA systems. The company's strategic differentiation centers on space-efficient automation designed specifically for brownfield environments, with the CMC Super Vertical occupying less than 10 square meters while delivering up to 500 packages per hour capability. CMC's recent inauguration of a 30,000-square-foot Tech Center in Georgia demonstrates its commitment to research and development excellence, positioning the company at the forefront of sustainable packaging innovation and Industry 4.0 integration.

The company's competitive advantage derives from its patented PRIMA-BOX design, which eliminates void filling materials while providing built-in protective corners through innovative corrugated utilization, directly addressing sustainability mandates and operational efficiency requirements. CMC's focus on plug-and-play installation capabilities and seamless integration with warehouse automation systems enables rapid deployment and scalability, making it particularly attractive for organizations seeking to modernize operations without extensive facility modifications. Their strategic partnerships with major material suppliers like Mondi enhance their sustainability positioning while delivering comprehensive packaging ecosystem solutions.

Bell and Howell LLC: Bell and Howell positions itself as a comprehensive automation services and technology organization, leveraging its extensive North American footprint and advanced mechatronics expertise to deliver integrated packaging automation solutions. The company's strategic differentiation lies in its Integrated 360™ technology platform, which provides remote diagnostics, automated dispatch capabilities, and round-the-clock technical support, ensuring minimal downtime and optimal system performance across diverse industrial environments. Bell and Howell's partnership with Packsize International demonstrates its commitment to extending service capabilities and market reach while maintaining its reputation for superior customer support.

The organization's competitive strength emerges from its diversified portfolio spanning mail production, retail automation, and packaging systems, supported by a dedicated team of mechatronic engineers providing comprehensive coverage across all fifty states. Their Remote360 IoT-enabled monitoring platform represents a significant technological advancement, automatically generating service calls based on algorithmic analysis and delivering predictive maintenance capabilities that reduce operational disruptions. Bell and Howell's focus on next-generation service excellence and guaranteed response times positions it as a preferred partner for organizations requiring reliable, scalable automation solutions with comprehensive support infrastructure.

Packsize International Inc.: Packsize International establishes its market leadership through innovative On Demand Packaging® technology, with flagship systems including the X5 and X6 automated solutions capable of producing up to 1,500 custom-sized boxes per hour. The company's strategic positioning centers on right-sized packaging solutions that eliminate void filling requirements while optimizing material utilization and shipping costs, directly addressing e-commerce scalability challenges and sustainability objectives. Packsize's integration of PackNet® Cloud software with existing warehouse management systems enables seamless workflow optimization and comprehensive packaging process control, creating substantial operational efficiencies for high-volume fulfillment operations.

The organization's competitive differentiation derives from its comprehensive technology integration capabilities, combining hardware innovation with sophisticated software platforms that deliver real-time optimization and performance analytics. Packsize's recent launch of the X6 system demonstrates its commitment to meeting European Packaging and Packaging Waste Regulation (PPWR) compliance requirements while providing enhanced flexibility for goods-to-person and shuttle system integration. Their strategic focus on both Box First and Box Last production methodologies, combined with modular design capabilities and subscription-based service models, positions Packsize as a versatile solution provider capable of adapting to diverse operational requirements and future scalability needs.

WestRock Company (now Smurfit Westrock): Following its transformative merger with Smurfit Kappa in 2024, WestRock has evolved into Smurfit Westrock, creating the world's largest paper-based packaging solutions provider with over 100,000 employees and 500 converting operations across 40 countries. The company's strategic positioning leverages its unprecedented scale and integrated manufacturing capabilities to deliver comprehensive end-of-line packaging automation solutions, including case formers, sealers, palletizers, and advanced RFID labeling systems. Smurfit Westrock's competitive advantage stems from its unique combination of in-house machinery manufacturing expertise and extensive global infrastructure, enabling customized automation solutions tailored to specific industry requirements.

The organization's market differentiation centers on its ability to provide performance-matched packaging solutions that seamlessly integrate with existing production lines while delivering measurable improvements in efficiency and sustainability. Their comprehensive portfolio spans corrugated packaging, automated machinery, and digital solutions, supported by dedicated technical teams and 24/7 support infrastructure that ensures seamless integration and ongoing operational excellence. Smurfit Westrock's strategic focus on sustainability-driven innovation, combined with its global manufacturing footprint and extensive R&D capabilities, positions it as a comprehensive solutions provider capable of addressing complex automation requirements across diverse industrial sectors while maintaining industry-leading environmental standards.

Market Key Players

Sparck Technologies

Panotec Srl Unipersonale

Ranpak

CMC Packaging Automation

Kolbus Autobox (KOLBUS GmbH & Co. KG)

Bell and Howell LLC

Aopack

Zemat Technology Group

WestRock Company

EMBA Machinery AB

Packsize International Inc.

Pattyn

T-Roc Equipment

Driver

E-commerce Acceleration and Workforce Optimization Solutions

The auto-boxing technology market experiences robust expansion in 2025, fueled by unprecedented e-commerce growth requiring scalable packaging infrastructure capable of processing millions of daily orders across diverse product categories. Modern retailers face the dual challenge of maintaining rapid fulfillment speeds while managing increasingly complex inventory portfolios, driving demand for intelligent packaging systems that automatically adjust to varying product dimensions without manual intervention. Auto-boxing solutions deliver measurable operational improvements, including up to 300% increases in packaging throughput rates and 88% reductions in labor dependencies, making them essential investments for competitive advantage.

Current labor market conditions further accelerate adoption, with 73% of manufacturers reporting moderate to severe worker shortages and average hourly wages exceeding $40 in developed markets, creating compelling economic justification for automation investments. Auto-boxing technology addresses these challenges by eliminating repetitive manual tasks, enabling existing workforce reallocation to higher-value activities, and providing consistent operational capacity regardless of staffing fluctuations.

Restraint

Capital Investment Barriers and Integration Complexity

High upfront capital requirements represent the most significant market constraint in 2025, with comprehensive auto-boxing system implementations requiring investments ranging from $200,000 to $2 million depending on sophistication and capacity requirements. Small and medium-sized enterprises face particular challenges justifying these expenditures despite compelling long-term return on investment projections, especially when competing for limited capital resources against other operational priorities. The financial barrier becomes more pronounced when considering additional costs for facility modifications, staff training, and potential production disruptions during implementation phases.

Integration complexity with existing warehouse management systems and legacy infrastructure creates additional implementation challenges, particularly for established operations with customized workflows and proprietary software environments. Organizations must navigate technical compatibility issues, data synchronization requirements, and potential operational disruptions while ensuring seamless integration with existing supply chain management platforms, further extending implementation timelines and associated costs.

Opportunity

Sustainable Packaging Innovation and Regulatory Compliance

Environmental sustainability initiatives present substantial market opportunities in 2025, as auto-boxing technology directly addresses corporate sustainability goals through waste reduction, material optimization, and carbon footprint minimization. These systems deliver up to 29% material savings by eliminating oversized packaging and reducing void fill requirements, while supporting circular economy principles through enhanced recyclability and reduced transportation emissions. Growing regulatory pressure for sustainable packaging practices, particularly in Europe and North America, creates favorable conditions for auto-boxing adoption as organizations seek compliance-ready solutions that demonstrate measurable environmental impact improvements.

The convergence of sustainability mandates with cost optimization objectives positions auto-boxing technology as a strategic solution addressing multiple organizational priorities simultaneously. Companies leveraging these systems can quantify environmental benefits for sustainability reporting requirements while achieving operational cost reductions, creating compelling value propositions for stakeholder engagement and regulatory compliance demonstration.

Trend

AI-Driven Predictive Packaging and Digital Integration

Artificial intelligence integration emerges as the dominant trend reshaping auto-boxing technology in 2025, with machine learning algorithms enabling predictive packaging optimization, real-time demand forecasting, and dynamic system configuration adjustments. Advanced auto-boxing platforms now incorporate computer vision systems, IoT connectivity, and cloud-based analytics to create comprehensive packaging intelligence ecosystems that continuously optimize performance based on historical data patterns and real-time operational metrics. This technological evolution enables autonomous decision-making capabilities, reducing human oversight requirements while delivering superior packaging precision and material utilization efficiency.

The integration of digital twin technology with auto-boxing systems represents another significant trend, enabling virtual simulation and optimization of packaging workflows before physical implementation. These digital platforms allow organizations to test packaging scenarios, predict system performance, and optimize configurations using advanced modeling capabilities, reducing implementation risks and accelerating deployment timelines across diverse operational environments.

Recent Developments

January 2025 – CMC Packaging Automation: Unveiled the CMC Genesys COMPACT, a plug-and-play auto-boxing system with embedded AI dimensioning and IoT connectivity. This launch enhances CMC’s market leadership by offering rapid deployment of intelligent, space-efficient packaging solutions.

February 2025 – Packsize International Inc.: Partnered with Amazon Fulfillment to pilot right-sized packaging stations powered by PackNet® Cloud analytics across three U.S. distribution centers. This collaboration expands Packsize’s strategic footprint in high-volume e-commerce operations and validates its cloud-based optimization platform.

March 2025 – Bell and Howell LLC: Introduced Remote360 AI, integrating machine learning-driven predictive maintenance into its Integrated 360™ service ecosystem for packaging lines. The upgrade strengthens Bell and Howell’s value proposition in minimizing downtime and improving system reliability for global customers.

April 2025 – Smurfit Westrock: Completed acquisition of BoxTech Solutions, a European automated boxing equipment manufacturer, to augment its end-of-line automation portfolio. This strategic move accelerates Smurfit Westrock’s expansion into continental Europe and broadens its turnkey packaging offerings.

May 2025 – Microsoft Azure: Launched Azure Auto-Boxing Accelerator, a cloud service combining Azure Digital Twins and Azure Machine Learning for real-time packaging process simulation and optimization. The introduction positions Microsoft as a key technology enabler in the auto-boxing ecosystem, driving rapid AI adoption.

December 2024 – Mondi PLC & CMC Packaging Automation: Established a sustainability partnership to co-develop recycled corrugated materials compatible with CMC’s auto-boxing systems. This initiative delivers strategic advantage by aligning both companies with stringent environmental mandates and advancing circular packaging models.

December 2024 – NVIDIA & Packsize International Inc.: Announced integration of NVIDIA TensorRT inference engines into Packsize’s right-sizing software to accelerate box dimension calculations. This collaboration strengthens Packsize’s competitive edge by leveraging GPU-accelerated AI for high-speed packaging optimization.

Frequently Asked Questions

How big is the Auto-boxing Technology Market?

The Auto-boxing Technology Market is expected to grow from USD 2.7 Billion in 2024 to USD 6.4 Billion by 2034, at a CAGR of 8.9%. Rising e-commerce volume, warehouse automation, and demand for efficient, labor-saving packaging systems are driving strong market adoption across logistics and manufacturing sectors.

Who are the major players in the Auto-boxing Technology Market?

Which segments covered the Auto-boxing Technology Market?

By Component (Solution, Services), By End-use (Food, Beverages, Pharmaceuticals, Retail & E-commerce, Manufacturing)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

, By End-use (Food, Beverages, Pharmaceuticals, Retail & E-commerce, Manufacturing) Industry Regions & Key Players – Sports Tech Innovation & Forecast 2025–2034")

, By End-use (Food, Beverages, Pharmaceuticals, Retail & E-commerce, Manufacturing) Industry Regions & Key Players – Sports Tech Innovation & Forecast 2025–2034")

, By End-use (Food, Beverages, Pharmaceuticals, Retail & E-commerce, Manufacturing) Industry Regions & Key Players – Sports Tech Innovation & Forecast 2025–2034")

, By End-use (Food, Beverages, Pharmaceuticals, Retail & E-commerce, Manufacturing) Industry Regions & Key Players – Sports Tech Innovation & Forecast 2025–2034")