- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Pharmaceutical Pricing and Market Size, Share | CAGR 6.2%

Global Automated Greenhouse System Market Size, Share, Analysis By Component (Hardware, Software, Services), By Technology (IoT-Based Monitoring & Control Systems, Artificial Intelligence & Machine Learning, Robotics & Automation, Computer Vision & Imaging Systems, Precision Irrigation & Fertigation Technologies, Cloud-Based Greenhouse Management Systems, Digital Twin & Predictive Analytics), By Application (Climate Control, Irrigation, Crop Monitoring, Pest Detection, Energy Management), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

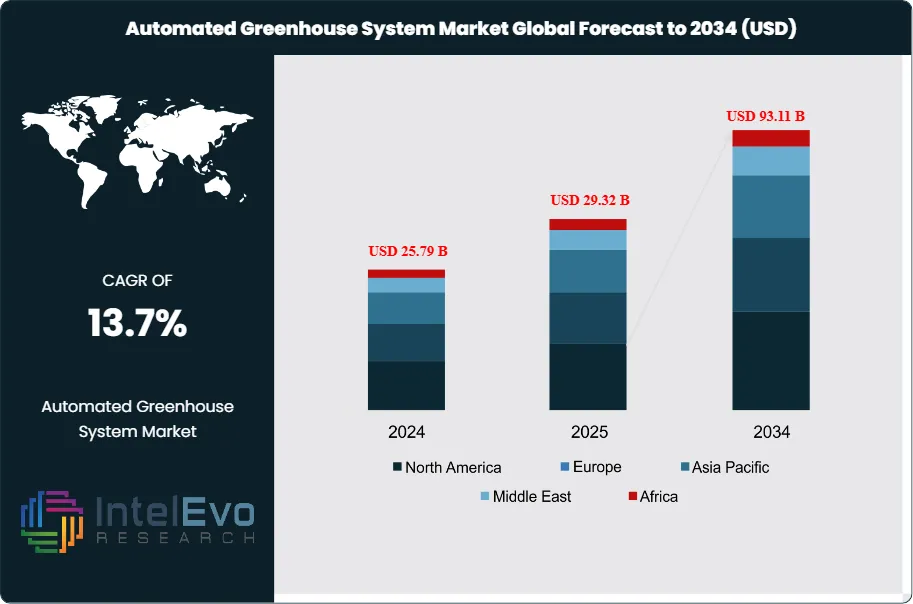

| USD 29.32 Billion | USD 93.11 Billion | 13.7% | Europe, 30.0% |

The Automated Greenhouse System Market was valued at approximately USD 25.79 Billion in 2024 and reached USD 29.32 Billion in 2025. The market is projected to grow to USD 93.11 Billion by 2034, expanding at a CAGR of 13.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 63.79 Billion over the analysis period. The Automated Greenhouse System Market covers hardware, software, and services for controlled-environment agriculture including climate control computers, irrigation and fertigation automation, LED horticultural lighting, CO2 enrichment systems, IoT sensor networks, AI-driven autonomous growing platforms, and integrated turnkey greenhouse construction solutions.

Get More Information about this report -

Request Free Sample ReportDemand growth is anchored in three structural shifts. First, global food security pressure from the UN Food and Agriculture Organization (FAO) projection of 9.7 billion population by 2050 requires 70% higher food production with constrained arable land. Second, labor shortages drive automation adoption across high-wage markets, with Dutch growers achieving up to 20% yield increases through Priva automation and Great Lakes Greenhouses in Canada reporting 19.6% cucumber yield improvement plus 17% energy efficiency gain through Koidra AI integration. Third, climate change and water scarcity accelerate controlled-environment agriculture investment, with the UAE, Saudi Arabia, and Qatar committing substantial capital to indoor cultivation under food security national strategies.

Regulatory and funding tailwinds reinforce the growth trajectory. The Netherlands SDE++ program earmarked EUR 11.5 billion (USD 12.65 billion) in 2024 for daylight greenhouses, air-water heat pumps, and photovoltaic-thermal systems. A Dutch CO2 levy started at EUR 9.50 per metric ton in 2025 and rises to EUR 17.70 per metric ton by 2030. In October 2025 Priva and Gardin announced strategic integration of real-time plant intelligence into Priva One greenhouse climate and automation systems. In March 2025 Autogrow launched Growlink Cloud Pro expanding cloud-based greenhouse automation with AI-driven optimization. In January 2025 Priva and Blue Radix extended their AI-driven autonomous climate and irrigation control collaboration, reducing manual tuning workload by up to 80% while improving yields by 7% and decreasing energy use by 15% in commercial pilots.

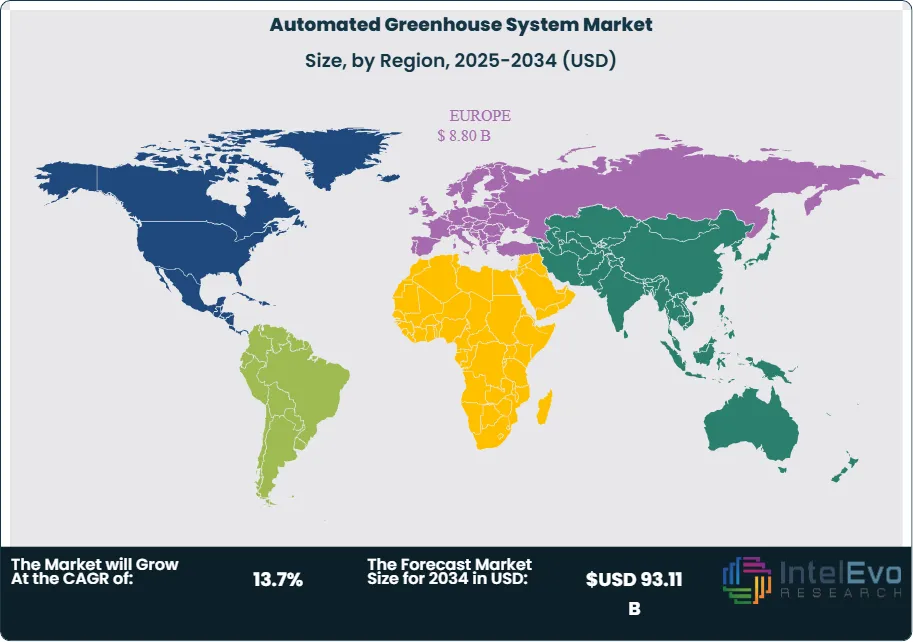

Europe held approximately 30.0% of global Automated Greenhouse System Market revenue in 2025, equivalent to USD 8.80 Billion, with the Netherlands, Spain, France, Italy, and Germany leading adoption. The Netherlands accounts for approximately USD 2.97 billion of regional spending, anchored by Dutch Greenhouse Delta export infrastructure, Westland horticultural cluster, and global vendor headquarters including Priva, Certhon, Hoogendoorn, and Ridder. Asia Pacific held 30.4% share at approximately USD 8.92 Billion, led by China, Japan, and South Korea under government-backed protected cultivation programs. North America captured 18.2% share at approximately USD 5.34 Billion.

Forward visibility through 2034 rests on three catalysts. First, AI-driven autonomous growing platforms including Koidra KoPilot, Blue Radix Crop Controller, and Priva One move the category from remote monitoring toward autonomous crop management, with Koidra achieving consecutive Autonomous Greenhouse Challenge wins at Wageningen University and Research. Second, LED horticultural lighting continues displacing high-pressure sodium (HPS) installations, with dynamic spectrum control enabling 10 to 25% yield gains. Third, hydroponics led the Automated Greenhouse System Market with 59.8% type share in 2025 and is expanding further under organic produce demand and resource efficiency imperatives. These forces together support the 13.7% forecast CAGR in the Automated Greenhouse System Market through 2034.

Market Definition & Scope

The Automated Greenhouse System Market is defined as the commercial space for integrated hardware, software, and services that automate environmental control, resource delivery, and crop management inside greenhouses, polytunnels, vertical farms, and controlled-environment agriculture facilities. The market encompasses climate control systems (temperature, humidity, ventilation, CO2 enrichment), automated irrigation and fertigation, LED horticultural lighting with dynamic spectrum control, IoT sensor networks, cloud-based monitoring platforms, AI-driven autonomous growing software, and associated integration services.

This analysis includes new-build greenhouse automation, retrofits of existing facilities, turnkey high-tech greenhouse construction with integrated automation, commercial horticulture, and research greenhouses. The scope explicitly excludes open-field precision agriculture (GPS-guided tractors, field irrigation pivots without greenhouse context), vertical farm construction without automation modules, standalone LED luminaires sold through consumer channels, and passive polytunnels without active environmental control. The parent greenhouse market reached approximately USD 32.95 Billion in 2025 per Industry Research, with the Automated Greenhouse System Market representing approximately 89% of the parent category through 2025 as automation becomes embedded in virtually all new commercial greenhouse construction.

, By Technology (IoT-Based Monitoring & Control Systems, Artificial Intelligence & Machine Learning, Robotics & Automation, Computer Vision & Imaging Systems, Precision Irrigation & Fertigation Technologies, Cloud-Based Greenhouse Management Systems, Digital Twin & Predictive Analytics), By Application (Climate Control, Irrigation, Crop Monitoring, Pest Detection, Energy Management), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Automated Greenhouse System Market grew from USD 29.32 Billion in 2025 to a projected USD 93.11 Billion in 2034, expanding at a 13.7% CAGR.

- Segment Dominance (By Type): Hydroponics held 59.8% revenue share in 2025 in the smart greenhouse sub-segment, anchored by water efficiency, precise nutrient control, and higher yield per square meter versus traditional cultivation.

- Segment Dominance (By Greenhouse): Hybrid greenhouses dominated with approximately USD 16.57 Billion in 2025 revenue per Fortune Business Insights, combining passive ventilation with active climate control automation.

- Driver: Priva's automation system has helped Dutch growers increase yields by up to 20%, and Great Lakes Greenhouses in Canada achieved 19.6% cucumber yield increase with 17% energy efficiency improvement via Koidra AI.

- Restraint: High upfront capital requirements for high-tech greenhouse construction favor top-quartile operators, accelerating consolidation and excluding mid-tier farms from credit under Dutch bank 'future-proof' lending criteria.

- Opportunity: The Netherlands SDE++ program committed EUR 11.5 billion (USD 12.65 billion) in 2024 for daylight greenhouses, air-water heat pumps, and photovoltaic-thermal systems supporting energy-efficient automation retrofits.

- Trend: Blue Radix Crop Controller reduces operator workload by 80%, increases yields by 7%, and decreases energy use by 15% in commercial pilots integrated with Priva One automation platforms through 2025.

- Regional: Europe held 30.0% revenue share in 2025 at approximately USD 8.80 Billion, with Netherlands at USD 2.97 Billion as the dominant national market.

Key Insights Summary

- Priva and Gardin announced strategic integration of real-time plant intelligence into Priva One greenhouse climate and automation systems in October 2025, enabling actionable crop performance insights across the Priva installed base in 60 countries.

- Autogrow launched Growlink Cloud Pro in March 2025, expanding its cloud-based greenhouse automation platform with remote control, AI-driven optimization, and enhanced data analytics for commercial growers.

- Priva and Blue Radix extended their AI-driven autonomous climate and irrigation control collaboration in January 2025, reducing operator workload by 80% while increasing yields by 7% and decreasing energy use by 15% in commercial pilots.

- Great Lakes Greenhouses in Ontario, Canada, achieved a 19.6% increase in cucumber yield while improving energy efficiency by 17% after implementing Koidra AI autonomous control technology in 2024-2025.

- The Netherlands SDE++ program earmarked EUR 11.5 billion (USD 12.65 billion) in 2024 for daylight greenhouses, air-water heat pumps, and photovoltaic-thermal systems, alongside a CO2 levy rising from EUR 9.50 per ton in 2025 to EUR 17.70 per ton by 2030.

- The United States Agency for International Development (USAID) announced a USD 2 million grant to the UN Food and Agriculture Organization (FAO) to support domestic greenhouse industry expansion in Mongolia through 2025.

- Priva's horticulture automation system has helped Dutch growers achieve yield increases of up to 20% per the GrowDirector industry benchmarking through 2025.

Competitive Landscape Overview

The Automated Greenhouse System Market is moderately fragmented, with the top four companies including Priva, Argus Control Systems, Autogrow, and Certhon collectively holding an estimated 28 to 34% of global revenue in 2025. Competition is structured across three tiers: European horticulture technology leaders including Priva, Hoogendoorn, Ridder, and Certhon anchored in the Netherlands Westland cluster; North American integrated control providers led by Argus and Prospiant (Rough Brothers); and AI-software specialists including Koidra, Blue Radix, Gardin, and 30MHz which partner with hardware vendors rather than competing for full-stack sales.

The competitive environment shifted sharply through 2024-2025 toward AI-driven autonomous growing and partnership ecosystems rather than pure hardware differentiation. Priva announced strategic partnerships with Koidra in 2023, Blue Radix with extended collaboration in January 2025, and Gardin in October 2025, positioning the Priva One platform as the integration anchor for third-party intelligence. Hoogendoorn operates the IIVO platform and Let's Grow cloud data service. Ridder HortiMaX Synopta provides integrated climate and water management. Autogrow Growlink Cloud Pro launched in March 2025 targets small and medium growers. Koidra won the Autonomous Greenhouse Challenge at Wageningen University and Research in consecutive years and received USDA innovation grants. Japanese entrant Denso entered the market through a joint venture with Certhon, illustrating cross-border industrial interest.

Competitive Landscape Matrix

| Company | HQ | Position | Key Platform | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Priva B.V. | De Lier, Netherlands | Leader | Priva Connext; Priva Compass; Priva One platform | Global (60 countries) | Announced strategic integration with Gardin real-time plant intelligence for Priva One platform in October 2025 |

| Argus Control Systems Limited | Surrey, BC, Canada | Leader | Argus TITAN; TITAN Envoy cloud interface | North America, Global | Continued TITAN platform expansion with remote cloud access and mobile device management through 2025 |

| Autogrow Systems Limited | Auckland, New Zealand | Leader (SMB) | Autogrow IntelliClimate; Growlink Cloud Pro | Global | Launched Growlink Cloud Pro in March 2025 expanding cloud-based automation with AI-driven optimization |

| Certhon Build B.V. | Poeldijk, Netherlands | Challenger (Turnkey) | Certhon full turnkey greenhouse; automation integration | Europe, Middle East | Continued Japanese market expansion with Denso joint venture and Middle East turnkey projects 2025 |

| Hoogendoorn Growth Management | Vlaardingen, Netherlands | Challenger | IIVO greenhouse automation platform; Let's Grow data | Europe, Asia Pacific | Continued IIVO platform expansion with integrated crop registration and autonomous growing features 2025 |

| Rough Brothers, Inc. (Prospiant) | Cincinnati, OH, USA | Challenger (US) | Prospiant greenhouse structures and automation integration | North America | Continued indoor agriculture turnkey growth in controlled environment agriculture sector 2025 |

| GrowDirector Ltd. | Tel Aviv, Israel | Niche | GrowDirector 4 PRO climate and fertigation automation | Global (SMB) | Continued expansion of intelligent climate control for commercial and indoor cultivation 2025 |

| Koidra Inc. | Richardson, TX, USA | Niche (AI software) | KoPilot autonomous control; DataPilot | Global (via partners) | Extended Priva partnership with AI autonomous control integration; Autonomous Greenhouse Challenge wins |

| Ridder Group | Harderwijk, Netherlands | Challenger | Ridder Drive Systems; Ridder HortiMaX Synopta | Europe, Asia | Continued HortiMaX Synopta platform expansion with integrated climate and water management 2025 |

| LumiGrow, Inc. | Emeryville, CA, USA | Niche (Lighting) | LumiGrow smartPAR; TopLight LED; wireless control | North America | Continued LED horticulture lighting expansion with smartPAR dynamic light control 2025 |

Segmentation Analysis

The Automated Greenhouse System Market segments across component, technology, application, crop type, and end-user. Procurement leaders building an automated greenhouse procurement checklist should benchmark vendors on climate control precision, integration with existing ERP and farm management systems, LED spectrum control capability, cloud data sovereignty, AI autonomous control roadmap, and total cost of ownership including energy consumption across each segmentation dimension.

By Component

Sensors and control systems led the Automated Greenhouse System Market with approximately 42% revenue share in 2025, equivalent to USD 12.31 Billion, anchored by Priva Connext process computers, Argus TITAN controllers, Hoogendoorn IIVO platforms, and third-party IoT sensor networks covering temperature, humidity, CO2, photosynthetically active radiation (PAR), and soil moisture. HVAC and climate control equipment captured 27% share at approximately USD 7.92 Billion, including heating systems which led the Netherlands commercial greenhouse market at 37.45% share in 2025 per Mordor Intelligence. LED horticultural lighting held 16% share at USD 4.69 Billion, growing faster than the overall market at approximately 15% CAGR through 2034.

Irrigation and fertigation systems captured 11% share at USD 3.23 Billion, including drip irrigation, ebb-and-flow, NFT hydroponic delivery, and integrated fertilizer injection. Material handling and robotics held 4% share at USD 1.17 Billion, reflecting emerging commercial deployment of autonomous mobile robots for harvesting strawberries, cucumbers, and tomatoes. Greenhouse management software captured the remaining share through cloud subscriptions from Priva Connected, Argus TITAN Envoy, Hoogendoorn Let's Grow, and Autogrow Growlink Cloud Pro. Control and automation is projected to deliver the fastest 8.93% CAGR in the Netherlands sub-market through 2031 per Mordor Intelligence.

By Technology

Hydroponics led the Automated Greenhouse System Market with 59.8% revenue share in the smart greenhouse sub-segment in 2025 per IMARC Group, anchored by nutrient film technique (NFT), deep water culture (DWC), and recirculating Dutch bucket systems. Hydroponics adoption is driven by water efficiency (up to 90% less water than soil cultivation), precise nutrient control, higher yield per square meter, and elimination of resource wastage through recirculating nutrient solutions. Aeroponics and aquaponics collectively held approximately 12% share. Non-hydroponic soil-based automated greenhouses captured the remaining share, primarily in legacy cucumber, tomato, and pepper operations transitioning to hybrid setups. Hydroponics in the Netherlands accounted for 48.35% of commercial greenhouse revenue in 2025 per Mordor Intelligence, with hybrid and vertical integration systems projected to grow at 11.9% CAGR through 2031.

By Application

Vegetable production led the Automated Greenhouse System Market with 38% revenue share in 2025, equivalent to approximately USD 11.14 Billion, dominated by tomatoes, cucumbers, peppers, and eggplants which represent approximately 70% of Delphy research center cultivation per Priva case studies. Herbs and leafy greens captured 22% share at USD 6.45 Billion, growing fastest under consumer demand for pesticide-free salads. Flowers and ornamentals held 19% share at USD 5.57 Billion, anchored by Dutch Chrysanthemum, tulip, and rose exports via vendors including Deliflor Chrysanten. Fruits including strawberries and berries captured 13% share, and nursery plants 8%. The herbs and microgreens segment is poised for 8.2% CAGR through 2031 in the Netherlands sub-market.

By End-User

Commercial growers led the Automated Greenhouse System Market at approximately 68% revenue share in 2025, equivalent to USD 19.94 Billion, reflecting the concentration of demand among Fortune 500 agricultural producers, controlled-environment agriculture operators, and multi-site European horticultural exporters. Large-scale operations in the Netherlands, Spain, China, Canada, and the United States drive purchase decisions exceeding USD 2 million per new-build hectare of high-tech glass greenhouse. Research institutions and universities held 12% share, including Wageningen University and Research which hosts the Autonomous Greenhouse Challenge. Small and medium growers held 15% share, served by Autogrow, GrowDirector, and cloud-native platforms. Government and non-profit food security programs captured 5% share, including the USAID-FAO Mongolia program. Automated greenhouse implementation timelines typically range from 4 to 9 months for retrofits and 12 to 24 months for new-build turnkey high-tech facilities.

Regional Analysis

The Automated Greenhouse System Market divides across Europe, Asia Pacific, North America, Latin America, and Middle East & Africa, with Europe leading in technology sophistication and Asia Pacific leading in overall spending volume.

Europe

Europe held 30.0% of global Automated Greenhouse System Market revenue in 2025, equivalent to USD 8.80 Billion. The Netherlands alone contributed approximately USD 2.97 billion, capturing 9% of global greenhouse market share per Industry Research. Spain contributed USD 1.98 billion driven by Almeria's 30,000-hectare greenhouse cluster. Germany, France, Italy, and Belgium anchor secondary European demand. The Netherlands SDE++ program committed EUR 11.5 billion in 2024 for daylight greenhouses, heat pumps, and photovoltaic-thermal systems. The CO2 levy rising from EUR 9.50 per ton in 2025 to EUR 17.70 per ton by 2030 drives energy-efficient automation adoption. European Union Common Agricultural Policy (CAP) 2023-2027 provisions support precision agriculture and digital farming investments. Westland geothermal infrastructure including Warmte Netwerk Westland's 500-megawatt district heat build-out reinforces regional competitive advantage.

Asia Pacific

Asia Pacific held 30.4% share in 2025 at approximately USD 8.92 Billion and is projected to grow fastest at approximately 15% CAGR through 2034 per Fortune Business Insights. China captured 15.0% of the global greenhouse market at USD 4.94 billion in 2025 per Industry Research, driven by Ministry of Agriculture and Rural Affairs protected cultivation programs and government subsidies for high-tech glass and plastic greenhouse construction. Japan's Ministry of Agriculture, Forestry and Fisheries (MAFF) supports Next-Generation Facility Horticulture Promotion, with domestic vendors including Denso, Inaho, and Farmship driving innovation. South Korea's Smart Farm Innovation Valley initiative commits USD 2 billion across four regional valleys. India's National Horticulture Mission subsidizes protected cultivation. Australia's Controlled Environment Horticulture cluster expansion drives baseline regional demand.

North America

North America captured 18.2% share in 2025 at approximately USD 5.34 Billion, with the United States at approximately USD 4.20 billion and Canada and Mexico splitting the remainder. U.S. Department of Agriculture (USDA) Specialty Crop Block Grant Program and Natural Resources Conservation Service (NRCS) Environmental Quality Incentives Program support protected cultivation investment. Canadian greenhouse operators including Leamington Ontario's 2,000+ hectare cluster and Great Lakes Greenhouses deploy Argus Control Systems, Priva, and Koidra AI solutions at scale. Mexico's horticultural exports to the United States drive border-state automated greenhouse construction. Costa Farms in Florida deploys automation modules monitoring external weather to automatically adjust greenhouse environment, closing vents during high winds and activating shade during intense sunlight.

Latin America

Latin America held 4.5% share in 2025 at approximately USD 1.32 Billion, led by Mexico, Brazil, Colombia, and Chile. Mexico's protected horticulture sector spanning approximately 40,000 hectares serves U.S. retail channels, anchored by Sinaloa, Jalisco, and Baja California state production. Brazil's Ministry of Agriculture supports expansion of controlled-environment agriculture under the Plano Nacional de Fertilizantes framework. Chile's Comision Nacional de Riego subsidizes water-efficient irrigation. Colombia's cut flower industry, the world's second-largest cut flower exporter after the Netherlands, drives sustained automated greenhouse procurement from Bogota-region producers. Regional growth is constrained by currency volatility and interest rate pressure, though multinational buyers continue corporate-standard automation deployments.

Middle East & Africa

The Middle East & Africa region held 2.0% share in 2025 at approximately USD 586 Million, growing fastest at approximately 9.30% CAGR through 2034 per Fortune Business Insights. The United Arab Emirates' National Food Security Strategy 2051 targets 50% self-sufficiency, with significant investment in ADQ, Silal, and Pure Harvest Smart Farms facilities. Saudi Arabia's Public Investment Fund (PIF) backs Red Sea Farms, AeroFarms, and Topian (NEOM) under Vision 2030. Qatar's Hassad Food continues expansion following the 2017-2021 blockade resilience program. Israel's precision agriculture leadership including Netafim, GrowDirector, and CropX influences regional automation trends. Egypt's large-scale protected cultivation in the Toshka Valley and Morocco's Souss-Massa region anchor African adoption. Solar-powered climate systems, desalination-based irrigation, and advanced cooling technologies are foundational to the regional automation value proposition.

Country Analysis

The Automated Greenhouse System Market concentrates in four national markets that together contribute approximately 50% of 2025 global revenue: the United States, the Netherlands, China, and Spain.

United States

The United States generated approximately USD 4.20 Billion in Automated Greenhouse System Market revenue in 2025, contributing 12.7% of global share per Industry Research, and is projected to grow at a country CAGR of 14.0% through 2034. The USDA Specialty Crop Block Grant Program, Natural Resources Conservation Service (NRCS) Environmental Quality Incentives Program, and Farm Service Agency programs support protected cultivation. The Controlled Environment Agriculture Consortium at universities including Cornell, University of Arizona, and Purdue drives research. Major U.S. buyers include Costa Farms, Bright Farms, AeroFarms, Gotham Greens, Little Leaf Farms, and Revol Greens. Commercial greenhouse clusters in Leamington-Ontario (cross-border), California's Central Coast, and the Southwestern United States anchor demand. U.S. vendors LumiGrow, Argus (Canadian with U.S. operations), and Prospiant compete alongside European vendors Priva, Hoogendoorn, and Ridder.

Netherlands

The Netherlands contributed approximately USD 2.97 Billion in Automated Greenhouse System Market revenue in 2025, capturing 9% of global greenhouse market share, with a country CAGR of approximately 4.72% for the commercial greenhouse sub-segment through 2031 per Mordor Intelligence. The Dutch horticulture cluster including Westland, Aalsmeer, and Venlo regions operates approximately 9,000 hectares of high-tech glass greenhouses generating EUR 9+ billion in annual exports. Priva B.V., Hoogendoorn Growth Management, Ridder Group, and Certhon Build B.V. are headquartered domestically. The SDE++ program earmarked EUR 11.5 billion in 2024 with a CO2 levy escalating from EUR 9.50 per ton in 2025 to EUR 17.70 per ton by 2030. Blue Radix Crop Controller, Gardin, 30MHz, and Certhon drive AI and autonomous growing innovation. Major Dutch buyers include Deliflor Chrysanten, Royal FloraHolland growers, and Dutch vegetable exporters.

China

China contributed approximately USD 4.94 Billion in Automated Greenhouse System Market revenue in 2025, capturing 15.0% of global greenhouse market share, with a country CAGR of approximately 13.4% through 2034. The Ministry of Agriculture and Rural Affairs Five-Year Plan for Agricultural Modernization supports protected cultivation expansion with direct subsidies. Shandong, Liaoning, Hebei, and Yunnan provinces anchor regional production. Chinese domestic vendors including Beijing Kingpeng International Agriculture, Guangdong Kington Industrial, Shandong Sainpoly Greenhouse, and Wanzhuang (Wanzhuang Agri) compete alongside international vendors Priva, Certhon, and Hoogendoorn. The 14th Five-Year Plan allocated funding for smart agriculture demonstration parks. Rural revitalization strategy and food security imperatives drive sustained greenhouse automation investment.

Spain

Spain generated approximately USD 1.98 Billion in Automated Greenhouse System Market revenue in 2025, capturing 6% of global greenhouse market share, with a country CAGR of approximately 13.0% through 2034. Almeria's 30,000-hectare greenhouse cluster (the Mar de Plastico) is the largest concentration of greenhouses globally by area. Andalusia, Murcia, and Canary Islands anchor domestic production, exporting to Germany, France, and the United Kingdom. Spanish domestic vendors including Ulma Agricola, Ritec, Naandanjain, and Novedades Agricolas compete alongside Dutch vendors. The European Agricultural Fund for Rural Development (EAFRD) and Spanish Ministry of Agriculture, Fisheries and Food (MAPA) Next Generation EU recovery fund allocations support automation retrofits. Water scarcity pressure from the southern Spain drought through 2023-2025 drives adoption of precision irrigation and hydroponics.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Component

- Hardware

- Sensors (Temperature, Humidity, CO₂, Light, Soil Moisture, pH)

- Climate Control Systems

- Irrigation & Fertigation Systems

- Ventilation & Cooling Equipment

- Lighting Systems (LED Grow Lights)

- Robotics & Automated Machinery

- Software

- Greenhouse Management Platforms

- Analytics & Monitoring Software

- AI-Based Decision Support Systems

- Services

- Installation & Integration Services

- Consulting Services

- Maintenance & Support Services

By Technology

- IoT-Based Monitoring & Control Systems

- Artificial Intelligence (AI) & Machine Learning

- Robotics & Automation

- Computer Vision & Imaging Systems

- Precision Irrigation & Fertigation Technologies

- Cloud-Based Greenhouse Management Systems

- Digital Twin & Predictive Analytics Solutions

By Application

- Climate Monitoring & Control

- Irrigation & Water Management

- Fertigation & Nutrient Management

- Crop Monitoring & Yield Optimization

- Pest & Disease Detection

- Harvesting & Post-Harvest Automation

- Energy Management & Sustainability Optimization

By End-User

- Commercial Greenhouse Growers

- Horticulture Farms

- Vertical Farming Operators

- Research Institutes & Agricultural Universities

- Nursery & Floriculture Producers

- Agricultural Cooperatives

- Others (Government Agricultural Facilities, Demonstration Farms)

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 29.32 B |

| Forecast Revenue (2034) | USD 93.11 B |

| CAGR (2025-2034) | 13.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Hardware, Software, Services), By Technology, (IoT-Based Monitoring & Control Systems, Artificial Intelligence (AI) & Machine Learning, Robotics & Automation, Computer Vision & Imaging Systems, Precision Irrigation & Fertigation Technologies, Cloud-Based Greenhouse Management Systems, Digital Twin & Predictive Analytics Solutions), By Application, (Climate Monitoring & Control, Irrigation & Water Management, Fertigation & Nutrient Management, Crop Monitoring & Yield Optimization, Pest & Disease Detection, Harvesting & Post-Harvest Automation, Energy Management & Sustainability Optimization), By End-User, (Commercial Greenhouse Growers, Horticulture Farms, Vertical Farming Operators, Research Institutes & Agricultural Universities, Nursery & Floriculture Producers, Agricultural Cooperatives, Others (Government Agricultural Facilities, Demonstration Farms)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | PRIVA B.V., ARGUS CONTROL SYSTEMS LIMITED, AUTOGROW SYSTEMS LIMITED, CERTHON BUILD B.V., HOOGENDOORN GROWTH MANAGEMENT, ROUGH BROTHERS, INC. (PROSPIANT), GROWDIRECTOR LTD., KOIDRA INC., RIDDER GROUP, LUMIGROW, INC., CLIMATE CONTROL SYSTEMS INC., NEXUS CORPORATION, LOGIQS B.V., SENSAPHONE, HELIOSPECTRA AB, SIGNIFY N.V. (PHILIPS HORTICULTURE LED), NETAFIM LTD., BLUE RADIX B.V., KUBO GREENHOUSE PROJECTS, DALSEM GREENHOUSE TECHNOLOGY, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (IoT-Based Monitoring & Control Systems, Artificial Intelligence & Machine Learning, Robotics & Automation, Computer Vision & Imaging Systems, Precision Irrigation & Fertigation Technologies, Cloud-Based Greenhouse Management Systems, Digital Twin & Predictive Analytics), By Application (Climate Control, Irrigation, Crop Monitoring, Pest Detection, Energy Management), Industry Trends & Forecast 2026-2034")

, By Technology (IoT-Based Monitoring & Control Systems, Artificial Intelligence & Machine Learning, Robotics & Automation, Computer Vision & Imaging Systems, Precision Irrigation & Fertigation Technologies, Cloud-Based Greenhouse Management Systems, Digital Twin & Predictive Analytics), By Application (Climate Control, Irrigation, Crop Monitoring, Pest Detection, Energy Management), Industry Trends & Forecast 2026-2034")

, By Technology (IoT-Based Monitoring & Control Systems, Artificial Intelligence & Machine Learning, Robotics & Automation, Computer Vision & Imaging Systems, Precision Irrigation & Fertigation Technologies, Cloud-Based Greenhouse Management Systems, Digital Twin & Predictive Analytics), By Application (Climate Control, Irrigation, Crop Monitoring, Pest Detection, Energy Management), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Automated Greenhouse System Market?

The Global Pharmaceutical Pricing and Market was valued at USD 1.67 Trillion in 2024 and is projected to reach USD 3.03 Trillion by 2034, growing at a CAGR of 6.2% from 2026 to 2034. Growth is driven by increasing demand for innovative drugs, specialty pharmaceuticals, biologics, biosimilars, precision medicine, rising chronic disease prevalence, expanding healthcare access, evolving reimbursement models, and growing pharmaceutical R&D investments across global healthcare markets.

Who are the major players in the Automated Greenhouse System Market?

PRIVA B.V., ARGUS CONTROL SYSTEMS LIMITED, AUTOGROW SYSTEMS LIMITED, CERTHON BUILD B.V., HOOGENDOORN GROWTH MANAGEMENT, ROUGH BROTHERS, INC. (PROSPIANT), GROWDIRECTOR LTD., KOIDRA INC., RIDDER GROUP, LUMIGROW, INC., CLIMATE CONTROL SYSTEMS INC., NEXUS CORPORATION, LOGIQS B.V., SENSAPHONE, HELIOSPECTRA AB, SIGNIFY N.V. (PHILIPS HORTICULTURE LED), NETAFIM LTD., BLUE RADIX B.V., KUBO GREENHOUSE PROJECTS, DALSEM GREENHOUSE TECHNOLOGY, Others

Which segments covered the Automated Greenhouse System Market?

By Component, (Hardware, Software, Services), By Technology, (IoT-Based Monitoring & Control Systems, Artificial Intelligence (AI) & Machine Learning, Robotics & Automation, Computer Vision & Imaging Systems, Precision Irrigation & Fertigation Technologies, Cloud-Based Greenhouse Management Systems, Digital Twin & Predictive Analytics Solutions), By Application, (Climate Monitoring & Control, Irrigation & Water Management, Fertigation & Nutrient Management, Crop Monitoring & Yield Optimization, Pest & Disease Detection, Harvesting & Post-Harvest Automation, Energy Management & Sustainability Optimization), By End-User, (Commercial Greenhouse Growers, Horticulture Farms, Vertical Farming Operators, Research Institutes & Agricultural Universities, Nursery & Floriculture Producers, Agricultural Cooperatives, Others (Government Agricultural Facilities, Demonstration Farms))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Automated Greenhouse System Market

Published Date : 04 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date