- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Automotive Lightweight Composite Market Size, Share | CAGR 10.5%

Global Automotive Lightweight Composite Market Size, Share, Growth Analysis By Material Type (CFRP, GFRP, NFRP, Aramid Fiber Reinforced Polymer, Hybrid Composites, Metal Matrix Composites), By Matrix Type (Thermoset & Thermoplastic Composites), By Manufacturing Process (RTM, SMC, Compression Molding, Injection Molding, 3D Printing), By Application, By Vehicle Type, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

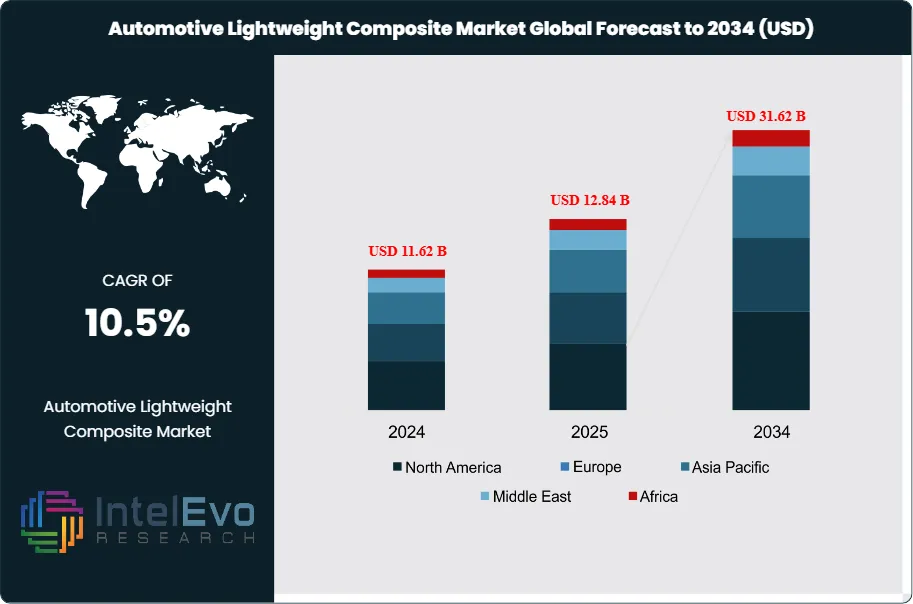

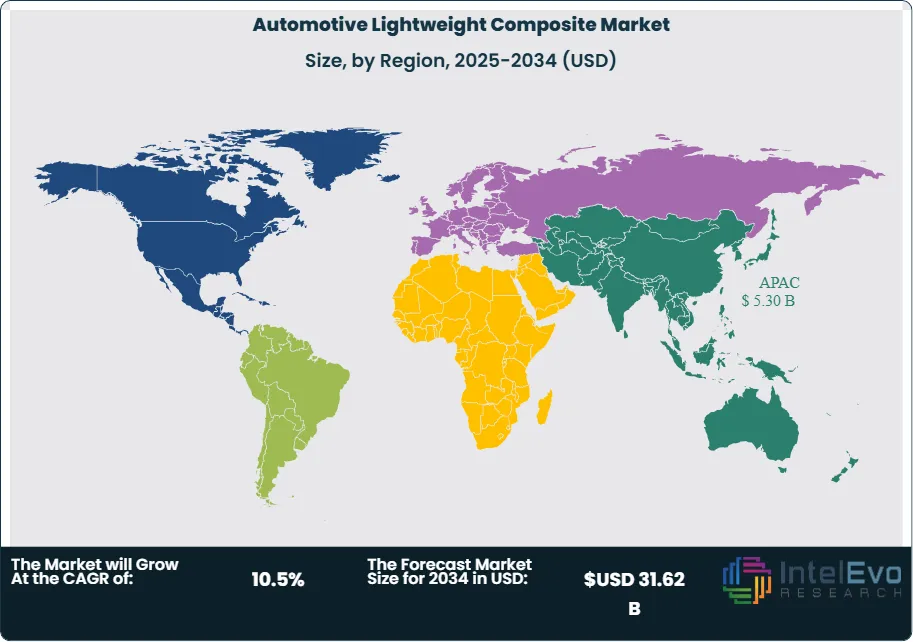

| USD 12.84 Billion | USD 31.62 Billion | 10.5% | Asia Pacific, 41.3% |

The Automotive Lightweight Composite Market was valued at approximately USD 11.62 Billion in 2024 and reached USD 12.84 Billion in 2025. The market is projected to grow to USD 31.62 Billion by 2034, expanding at a CAGR of 10.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 18.78 Billion over the analysis period, driven by mandatory CO2 emission targets, accelerating battery electric vehicle production, and structural substitution of steel and aluminum with advanced fiber-reinforced composites across body, chassis, and battery system applications.

Get More Information about this report -

Request Free Sample ReportAutomotive lightweight composites encompass a diverse class of advanced materials — including carbon fiber reinforced polymers (CFRP), glass fiber reinforced polymers (GFRP), natural fiber reinforced composites (NFRP), aramid fiber systems, and hybrid composite architectures — that deliver structural performance equivalent to or exceeding conventional metals at 30–60% lower mass. The physics of lightweighting generates compounding benefits in battery electric vehicles: every 100 kg of mass reduction extends EV range by 8–12 km under WLTP test cycles, reduces battery sizing requirements by approximately 5–8 kWh, and lowers total vehicle lifecycle carbon footprint by an estimated 3.2–4.8 tonnes CO2 equivalent across a 250,000 km service life. These metrics translate directly into composite material specification decisions at OEM vehicle programs, where mass budget management is a first-order engineering and commercial priority.

Regulatory pressure is the structural demand catalyst for automotive lightweight composites. The EU's CO2 fleet emission regulation (Regulation EU 2019/631) mandates average fleet CO2 emissions of 93.6 g/km for passenger cars from 2025, tightening to 49.5 g/km by 2030 — a 47% reduction that is physically unachievable in battery electric and plug-in hybrid vehicles without systematic mass reduction through lightweighting. The US Corporate Average Fuel Economy (CAFE) standards, finalized by NHTSA in 2024, require average fleet fuel economy of 50.4 MPG by model year 2031, imposing equivalent mass reduction imperatives on North American OEMs. China's Phase IV vehicle energy efficiency standards and the MIIT's dual-credit NEV mandate are similarly compelling Chinese automakers to adopt lightweight composite solutions across NEV body structures. OICA production data indicates global vehicle production of 92.4 million units in 2025, with battery electric and plug-in hybrid variants reaching 28.3% of total production — a composite-favorable mix shift that is accelerating materially.

Asia Pacific leads the global automotive lightweight composite market with a 41.3% share at USD 5.30 Billion in 2025, anchored by China's position as the world's largest automotive production market, Japan's established carbon fiber supply chain, and South Korea's rapid transition to electric mobility platforms. Europe follows at 28.6% at USD 3.67 Billion, with German OEMs driving CFRP adoption in premium and performance segments and EU regulatory requirements compelling lightweighting investment across volume manufacturers. North America accounts for 21.8% at USD 2.80 Billion, with Ford, GM, and Tesla driving glass fiber and thermoplastic composite adoption in structural and battery enclosure applications. Carbon fiber composites are the highest-value segment at 38.4% of global revenue, though glass fiber composites retain dominant volume share at 47.2%, reflecting their cost-performance characteristics in high-volume applications. Thermoplastic composite systems — particularly continuous fiber thermoplastic (CFRTP) — are the fastest-growing material category at 16.8% CAGR, driven by their recyclability, high-volume processing compatibility, and suitability for press-forming cycles as short as 60–90 seconds.

Manufacturing process technology is a critical competitive dimension in the automotive lightweight composite market. High-pressure resin transfer molding (HP-RTM), sheet molding compound (SMC) compression molding, and rapid-cure prepreg press curing have collectively reduced composite component cycle times from 20–45 minutes in 2018 to 2–6 minutes in 2025 for structural body panels — approaching the 60–90 second press cycle times of stamped steel that automotive production line economics require. This cycle time convergence is the key enabler of composite adoption beyond premium and performance segments into volume production vehicles exceeding 50,000 units per year, a threshold that opens the composite market's largest addressable segment. AS9100 and IATF 16949 quality management system alignment ensures composite supplier qualifications meet automotive OEM Tier 1 supply chain standards, a requirement that screens out non-automotive-grade composite manufacturers from program award consideration.

, By Matrix Type (Thermoset & Thermoplastic Composites), By Manufacturing Process (RTM, SMC, Compression Molding, Injection Molding, 3D Printing), By Application, By Vehicle Type, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global automotive lightweight composite market was valued at USD 12.84 Billion in 2025 and is projected to reach USD 31.62 Billion by 2034, advancing at a CAGR of 10.5% over the 2026–2034 forecast period.

- Segment Dominance: By material type, glass fiber reinforced polymers (GFRP) lead the market at 47.2% of global volume and 34.8% of revenue in 2025, maintaining dominance in body panel, interior structural, and underbody applications where cost-performance optimization at high-volume production rates is the primary specification criterion.

- Segment Dominance: By application, body panels and exterior structures are the largest segment at 31.6% of global automotive lightweight composite revenue in 2025, driven by OEM mass reduction targets for exterior closures, roof panels, hoods, and door skins where composite substitution of steel delivers 40–55% mass savings per component.

- Driver: EU CO2 fleet emission mandates requiring 49.5 g CO2/km average fleet emissions by 2030 — a 47% reduction from the 2025 compliance threshold — are making composite lightweighting a non-discretionary engineering investment for European OEMs, with each gram-per-kilometer of CO2 reduction attributable to mass reduction potentially avoiding EUR 95 per excess g/km fleet-wide penalties under Regulation EU 2019/631.

- Restraint: Carbon fiber composite raw material costs averaging USD 18–32 per kg — 8–14 times the cost of stamped automotive steel at USD 1.80–2.40 per kg — continue to limit CFRP adoption to premium, performance, and structural battery applications where mass reduction value per kilogram saved exceeds the material cost premium.

- Opportunity: EV structural battery enclosures represent an addressable composite market of USD 3.2 Billion by 2030 and USD 6.8 Billion by 2034, as OEMs replace metallic battery housing with carbon fiber and glass fiber composite systems delivering 20–28% mass reduction, improved thermal management, and EMI shielding properties required by ECE R100 and UN GTR 20 battery safety standards.

- Trend: Thermoplastic composite (CFRTP and GFRTP) adoption in high-volume automotive structural applications is accelerating at 16.8% CAGR, driven by 60–90 second press-forming cycle times compatible with OEM body-in-white stamping line productivity, full recyclability addressing EU End-of-Life Vehicles (ELV) Directive revision requirements, and weldability enabling joining with conventional automotive assembly processes.

- Regional Analysis: Asia Pacific leads with a 41.3% market share at USD 5.30 Billion in 2025, driven by China's 30.4 million unit annual vehicle production base, Japan's globally dominant carbon fiber supply chain led by Toray and Teijin, and South Korea's rapid NEV production ramp at Hyundai-Kia creating structural composite specification opportunities.

Competitive Landscape Overview

The automotive lightweight composite market is moderately consolidated, with the top four suppliers — Toray Industries, Hexcel Corporation, Teijin, and SGL Carbon — collectively accounting for approximately 43.6% of global market revenue in 2025. Competition is technology-driven in the carbon fiber and high-performance composite segment, centered on fiber tensile strength (GPa), composite-specific modulus, and manufacturing process cycle time capability. In the glass fiber segment, competition is more price-sensitive, with Owens Corning, Jushi Group, and Chongqing Polycomp International (CPIC) competing primarily on cost per kilogram and localized supply chain positioning. The market has experienced meaningful M&A and capacity expansion activity in 2024–2025 as composite producers invest ahead of projected EV structural composite demand growth. Japanese producers Toray and Teijin retain significant competitive moats through proprietary PAN precursor manufacturing and fiber production IP, while European specialty chemical companies Solvay and Covestro are competing on matrix resin and thermoplastic composite sheet differentiation.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Move (2024–2026) |

| Toray Industries | Japan | Leader | Torayca Carbon Fiber Composites | Asia Pacific / North America | Opened USD 1.1B carbon fiber plant in South Carolina, Feb 2025 |

| Hexcel Corporation | USA | Leader | HexPly Automotive CFRP Prepregs | North America / Europe | Launched rapid-cure epoxy prepreg for 2-min press cycle, Apr 2025 |

| Teijin Limited | Japan | Challenger | Sereebo CFRTP Composite | Asia Pacific / Europe | Partnered with BMW Group on next-gen CFRTP body panel supply, Jul 2025 |

| SGL Carbon | Germany | Challenger | SIGRAFIL Carbon Fiber Composites | Europe / North America | Expanded automotive CFRP capacity at Wackersdorf by 3,200 MT, Sep 2025 |

| Owens Corning | USA | Challenger | Advantex Glass Fiber Composites | North America / Europe | Acquired Kuang Yung Glass Fiber for USD 420M to enter APAC auto market, Jan 2025 |

| Solvay SA | Belgium | Niche Player | CYCOM Structural Automotive Epoxy | Europe | Launched bio-based epoxy matrix system meeting IATF 16949, May 2025 |

| Covestro AG | Germany | Niche Player | Maezio CFRTP Thermoplastic Sheet | Europe / Asia Pacific | Signed long-term CFRTP supply agreement with Hyundai Motor, Oct 2025 |

| Mitsubishi Chemical Group | Japan | Niche Player | Pyrofil Carbon Fiber Composites | Asia Pacific | Commenced EV structural battery enclosure composite production, Dec 2025 |

By Material Type

The automotive lightweight composite market by material type is dominated by glass fiber reinforced polymers (GFRP), which account for 47.2% of production volume and 34.8% of revenue at USD 4.47 Billion in 2025. GFRP's market position reflects its cost-performance advantage in high-volume applications: E-glass fiber costs USD 2.40–4.80 per kg versus USD 18–32 per kg for standard modulus carbon fiber, enabling component cost structures compatible with volume segment passenger vehicles. GFRP applications span SMC body panels, GMT structural underbody systems, GFRP door modules, and glass fiber reinforced underbody shields. Continuous glass fiber reinforced thermoplastic (GFRTP) tapes and organosheets are gaining rapid traction in structural applications, processed via rapid-cycle compression molding within 90–120 second cycle times.

Carbon fiber reinforced polymers (CFRP) represent 38.4% of revenue at USD 4.93 Billion in 2025, the highest-value material segment. Standard modulus (240 GPa) and intermediate modulus (290 GPa) PAN-based carbon fiber dominates automotive CFRP, with tensile strengths of 3,500–6,400 MPa enabling structural part designs at 50–65% lower mass than steel equivalents. CFRP adoption is concentrated in BEV battery enclosures, A-pillar and roof bow structural members, hood and trunk lid assemblies in premium vehicles, and racing-derived body structures. Natural fiber reinforced composites (NFRP) — using flax, hemp, kenaf, and jute reinforcement — account for 6.8% at USD 873 Million, growing at 12.4% CAGR in interior trim and non-structural panels where bio-based content supports EU ELV end-of-life recyclability compliance. Aramid fiber composites represent 4.2% at USD 539 Million, primarily in ballistic protection and high-impact energy absorption components. Hybrid composites — combining carbon and glass fibers in optimized layup sequences — account for the remaining 4.6% at USD 591 Million, growing rapidly in applications requiring balanced stiffness, energy absorption, and cost efficiency.

By Matrix Type

Thermoset composites — primarily epoxy, polyester, vinyl ester, and polyurethane matrix systems — lead the automotive lightweight composite market at 61.4% of revenue at USD 7.88 Billion in 2025. Epoxy matrix systems dominate structural CFRP applications due to their high fiber-matrix adhesion, chemical resistance, and mechanical performance at service temperatures up to 130°C. HP-RTM epoxy systems from Hexcel, Huntsman, and Solvay achieve gel times of 60–120 seconds, enabling injection-to-demolding cycles of 2–4 minutes for structural automotive parts. SMC compression molding compounds — typically polyester or vinyl ester matrix reinforced with chopped glass fiber — represent the highest-volume thermoset automotive composite process, producing 45–60 million automotive components annually across North America, Europe, and Asia Pacific.

Thermoplastic composites represent 38.6% of revenue at USD 4.96 Billion in 2025 and are growing at 16.8% CAGR — the fastest sub-segment in the market. Carbon fiber reinforced thermoplastics (CFRTP) and glass fiber reinforced thermoplastics (GFRTP) using PA6, PA66, PP, PPS, PEEK, and LCP matrix polymers offer processing advantages over thermosets: press-forming cycle times of 60–90 seconds versus 2–6 minutes for RTM, full thermoplastic weldability enabling ultrasonic and induction joining, and material recyclability addressing EU ELV Directive 2000/53/EC requirements mandating 85% recyclability by weight for end-of-life vehicles. Covestro's Maezio CFRTP, Teijin's Sereebo CFRTP, and Toray's TenCate thermoplastic composites are leading programs targeting high-volume structural automotive applications above 50,000 units per year.

By Manufacturing Process

Sheet molding compound (SMC) compression molding is the dominant manufacturing process in the automotive lightweight composite market by volume, accounting for 28.4% of total production volume in 2025. SMC's market position reflects 40+ years of automotive production integration, established Tier 1 supplier tooling infrastructure, and cycle times of 60–120 seconds compatible with high-volume body panel production at rates of 200,000–600,000 units per year. Major automotive SMC applications include exterior body panels (hoods, deck lids, fenders, and door skins), structural underbody shielding, and HVAC housings. High-pressure resin transfer molding (HP-RTM) represents 21.6% of process share in 2025, producing structural CFRP components in 2–4 minute cycles for premium and performance vehicle applications requiring near-net-shape complex geometry and design-optimized fiber orientations.

Prepreg autoclave and press curing accounts for 16.8% of process revenue, concentrated in premium OEM structural applications and motorsport where part performance requirements justify the higher capital cost of autoclave processing. Compression molding of thermoplastic organosheets and unidirectional tape layups represents 14.2% of process share, the fastest-growing process segment at 18.3% CAGR as thermoplastic composite adoption accelerates. Injection molding of short and long fiber reinforced thermoplastics accounts for 10.6%, serving high-volume interior structural components. Pultrusion, filament winding, and additive manufacturing collectively represent the remaining 8.4%, with composite 3D printing growing at 22.1% CAGR in prototype and low-volume specialty component applications.

By Application

Body panels and exterior structures represent the largest application segment in the automotive lightweight composite market at 31.6% of revenue at USD 4.06 Billion in 2025. This segment encompasses composite hood assemblies, trunk lids, roof panels, door outer skins, fenders, and tailgates — applications where composite substitution of steel delivers 40–55% mass savings per component with equivalent dent resistance and Class A surface quality achievable through Class A SMC formulations and in-mold coating technologies. BMW's carbon fiber roof bow in the i-series and the 7 Series, Ford's SMC composite hood on the F-150 and Explorer, and General Motors' composite deck lids on Corvette and Cadillac platforms are established volume applications setting industry benchmarks.

Battery enclosures for battery electric vehicles represent 18.4% of the automotive lightweight composite market at USD 2.36 Billion in 2025, growing at 21.3% CAGR — the fastest application growth rate. Composite battery enclosures replace aluminum and steel battery housing structures with CFRP or GFRP systems delivering 20–28% mass reduction, inherent electrical insulation, improved EMI shielding performance, and design freedom to optimize thermal management duct integration. Chassis and frame structures account for 16.2% at USD 2.08 Billion; interior components 14.8% at USD 1.90 Billion; powertrain and engine components 10.6% at USD 1.36 Billion; and underbody and floor systems the remaining 8.4% at USD 1.08 Billion.

By Vehicle Type

Passenger cars dominate the automotive lightweight composite market by vehicle type, accounting for 52.4% of global revenue at USD 6.73 Billion in 2025. Within passenger cars, premium and luxury vehicles (price segments above USD 50,000) represent 43.8% of passenger car composite revenue at USD 2.95 Billion, driven by the financial margin available to absorb composite material premiums and the brand equity associated with advanced material content. However, the most significant growth vector is volume passenger cars in the USD 25,000–50,000 segment, where EV powertrain requirements are compelling composite adoption in body and battery applications previously addressed by steel.

Battery electric vehicles (BEV) and plug-in hybrid electric vehicles (PHEV) represent 34.6% of total automotive lightweight composite revenue at USD 4.44 Billion in 2025, growing at 17.2% CAGR as global BEV production reaches 26.2 million units annually. EV-specific composite applications — including structural battery enclosures, composite floor systems integrating battery thermal channels, and lightweight body structures optimizing range per unit battery capacity — are generating composite content per vehicle that is 38–54% higher than equivalent ICE vehicle composite content. Commercial vehicles account for 9.2% at USD 1.18 Billion, sports and performance vehicles 3.8% at USD 488 Million, and light commercial vehicles (LCVs) the remaining 4.6% at USD 590 Million in 2025.

Regional Analysis

Asia Pacific

Asia Pacific leads the global automotive lightweight composite market with a 41.3% share at USD 5.30 Billion in 2025, growing at an 11.8% CAGR through 2034. China is by far the largest country market, representing 52.4% of APAC composite revenue at USD 2.78 Billion in 2025. China's MIIT dual-credit policy, Phase IV fuel economy standards, and the government's 2035 New Energy Vehicle development plan — targeting 50% NEV share of new vehicle sales — are collectively driving the most aggressive lightweighting adoption program in the global automotive industry. Chinese NEV manufacturers including BYD, NIO, Li Auto, and SAIC are specifying composite battery enclosures, composite body panels, and GFRP structural floor systems at production scales unprecedented outside premium European brands. Japan represents 24.6% of APAC revenue at USD 1.30 Billion, with Toyota's carbon fiber usage across Lexus and GR platforms, Honda's SMC composite body panel programs, and the country's globally dominant position in carbon fiber feedstock — Toray, Toho Tenax (Teijin), and Mitsubishi Chemical account for approximately 60% of global carbon fiber production capacity. South Korea contributes 12.8% of APAC revenue at USD 679 Million, with Hyundai's Covestro CFRTP agreement and Kia's composite body panel programs driving demand.

Europe

Europe holds 28.6% of global automotive lightweight composite revenue at USD 3.67 Billion in 2025. Germany is the dominant European market at 34.2% of European revenue at USD 1.26 Billion, anchored by BMW's vertically integrated CFRP supply chain (SGL Carbon JV), Volkswagen Group's composite body panel programs across VW, Audi, and Porsche, and Mercedes-Benz's composite structural applications in the EQ electric platform. BMW's i3 and i5 carbon fiber body-in-white architecture remains the industry's most comprehensive CFRP passenger vehicle program, with BMW consuming approximately 3,000 MT of carbon fiber annually from its Moses Lake, Washington and Wackersdorf joint venture facilities. Italy represents 14.8% of European revenue at USD 543 Million, driven by Ferrari's extensive CFRP use and Lamborghini's Forged Composite and prepreg carbon fiber structural programs. France contributes 14.2% at USD 521 Million, with Renault Group and Stellantis driving GFRP composite adoption in volume passenger car body panels. The EU's 2030 CO2 fleet emission target of 49.5 g/km is the most powerful single regulatory driver of composite investment in the European automotive industry.

North America

North America accounts for 21.8% of global automotive lightweight composite revenue at USD 2.80 Billion in 2025. The United States represents 84.6% of North American composite revenue at USD 2.37 Billion, driven by Ford's industry-leading aluminum-composite multi-material strategy in the F-150 Lightning and Mustang Mach-E, General Motors' composite applications across the Corvette C8 carbon fiber architecture and Silverado EV structural floor, and Tesla's expanding composite usage in Model 3, Model Y, and Cybertruck programs. Toray's new South Carolina facility, Ford's supply agreement with SGL Carbon for composite panels, and the US Department of Energy's Vehicle Technologies Office funding of USD 280 Million for lightweight materials manufacturing research in FY2025 are collectively accelerating the North American composite supply chain. CAFE standards for model year 2031 requiring 50.4 MPG fleet average are the primary long-term regulatory demand driver. Canada contributes 9.8% of North American revenue, with Ontario Tier 1 suppliers Magna International and Martinrea investing in composite component manufacturing capabilities to serve both Detroit Three and European OEM transplant programs.

Latin America

Latin America holds 5.4% of global automotive lightweight composite revenue at USD 693 Million in 2025. Brazil is the dominant market at 58.4% of LATAM revenue at USD 405 Million, driven by the country's position as Latin America's largest vehicle production market — producing 2.4 million vehicles annually — and growing composite adoption among Brazilian Tier 1 suppliers serving Ford, GM, Stellantis, and Volkswagen production in Sao Paulo and Minas Gerais states. Brazil's Rota 2030 mobility program provides industry funding for lightweight materials research, supporting composite supplier capability development at SENAI and FIEMG industrial research centers. Mexico represents 32.6% of LATAM revenue at USD 226 Million, with the country's Tier 1 automotive supplier base — serving US-bound vehicle programs — increasingly specifying composite body components to meet CAFE-driven mass reduction requirements cascaded from North American OEM program offices. Argentina contributes 6.2% at USD 43 Million, with GFRP composite adoption concentrated in commercial vehicle body applications.

Middle East & Africa

The Middle East and Africa region accounts for 2.9% of global automotive lightweight composite revenue at USD 372 Million in 2025. The region's composite automotive market is at an early development stage, with demand primarily driven by vehicle assembly operations rather than composite material production. South Africa leads MEA composite revenue at 42.8% at USD 159 Million, anchored by BMW South Africa's Rosslyn plant — producing BMW 3 Series for global export — which sources composite components from the same European supply chain as German domestic production. The UAE contributes 24.6% of MEA revenue at USD 92 Million, primarily through aftermarket composite body kits for premium and performance vehicles and nascent composite component manufacturing at Khalifa Industrial Zone Abu Dhabi (KIZAD). Saudi Arabia represents 18.4% at USD 68 Million, with Vision 2030 initiatives to establish a domestic automotive manufacturing industry driving interest in composite material supply chain development. Regional market growth through 2034 is contingent on the development of local composite manufacturing capacity to reduce import dependency and associated logistics cost premiums.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Material Type

- Carbon Fiber Reinforced Polymer (CFRP)

- Glass Fiber Reinforced Polymer (GFRP)

- Natural Fiber Reinforced Polymer (NFRP)

- Aramid Fiber Reinforced Polymer

- Hybrid Composites

- Metal Matrix Composites (MMC)

By Matrix Type

- Thermoset Composites

- Thermoplastic Composites (CFRTP / GFRTP)

By Manufacturing Process

- Resin Transfer Molding (RTM)

- Sheet Molding Compound (SMC)

- Prepreg / Autoclave

- Compression Molding

- Injection Molding

- Filament Winding

- Pultrusion

- 3D Printing / Additive Manufacturing

By Application

- Body Panels & Exterior Structures

- Chassis & Frame Structures

- Interior Components

- Powertrain & Engine Components

- Battery Enclosures (EV)

- Underbody & Floor Systems

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Electric Vehicles (BEV / PHEV)

- Sports & Performance Vehicles

- Light Commercial Vehicles (LCVs)

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 12.84 B |

| Forecast Revenue (2034) | USD 31.62 B |

| CAGR (2025-2034) | 10.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Material Type (Carbon Fiber Reinforced Polymer (CFRP), Glass Fiber Reinforced Polymer (GFRP), Natural Fiber Reinforced Polymer (NFRP), Aramid Fiber Reinforced Polymer, Hybrid Composites, Metal Matrix Composites (MMC)), By Matrix Type (Thermoset Composites, Thermoplastic Composites (CFRTP / GFRTP)), By Manufacturing Process (Resin Transfer Molding (RTM), Sheet Molding Compound (SMC), Prepreg / Autoclave, Compression Molding, Injection Molding, Filament Winding, Pultrusion, 3D Printing / Additive Manufacturing), By Application (Body Panels & Exterior Structures, Chassis & Frame Structures, Interior Components, Powertrain & Engine Components, Battery Enclosures (EV), Underbody & Floor Systems), By Vehicle Type (Passenger Cars, Commercial Vehicles, Electric Vehicles (BEV / PHEV), Sports & Performance Vehicles, Light Commercial Vehicles (LCVs)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | TORAY INDUSTRIES, HEXCEL CORPORATION, TEIJIN LIMITED, SGL CARBON SE, OWENS CORNING, SOLVAY SA, COVESTRO AG, MITSUBISHI CHEMICAL GROUP, TOHO TENAX (TEIJIN), HUNTSMAN CORPORATION, CYTEC SOLVAY GROUP, GURIT HOLDING AG, RENEGADE MATERIALS (TEIJIN), JUSHI GROUP CO. LTD., CHONGQING POLYCOMP INTERNATIONAL (CPIC), MAGNA INTERNATIONAL, BENTELER COMPOSITES, PLASAN CARBON COMPOSITES, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Matrix Type (Thermoset & Thermoplastic Composites), By Manufacturing Process (RTM, SMC, Compression Molding, Injection Molding, 3D Printing), By Application, By Vehicle Type, Industry Trends & Forecast 2026-2034")

, By Matrix Type (Thermoset & Thermoplastic Composites), By Manufacturing Process (RTM, SMC, Compression Molding, Injection Molding, 3D Printing), By Application, By Vehicle Type, Industry Trends & Forecast 2026-2034")

, By Matrix Type (Thermoset & Thermoplastic Composites), By Manufacturing Process (RTM, SMC, Compression Molding, Injection Molding, 3D Printing), By Application, By Vehicle Type, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Automotive Lightweight Composite Market?

The Global Automotive Lightweight Composite Market was valued at USD 11.62 Billion in 2024 and is projected to reach USD 31.62 Billion by 2034, growing at a CAGR of 10.5% from 2026 to 2034, driven by rising electric vehicle production, stringent fuel efficiency regulations, and increasing adoption of carbon fiber and advanced lightweight composite materials in automotive manufacturing.

Who are the major players in the Automotive Lightweight Composite Market?

TORAY INDUSTRIES, HEXCEL CORPORATION, TEIJIN LIMITED, SGL CARBON SE, OWENS CORNING, SOLVAY SA, COVESTRO AG, MITSUBISHI CHEMICAL GROUP, TOHO TENAX (TEIJIN), HUNTSMAN CORPORATION, CYTEC SOLVAY GROUP, GURIT HOLDING AG, RENEGADE MATERIALS (TEIJIN), JUSHI GROUP CO. LTD., CHONGQING POLYCOMP INTERNATIONAL (CPIC), MAGNA INTERNATIONAL, BENTELER COMPOSITES, PLASAN CARBON COMPOSITES, OTHERS

Which segments covered the Automotive Lightweight Composite Market?

By Material Type (Carbon Fiber Reinforced Polymer (CFRP), Glass Fiber Reinforced Polymer (GFRP), Natural Fiber Reinforced Polymer (NFRP), Aramid Fiber Reinforced Polymer, Hybrid Composites, Metal Matrix Composites (MMC)), By Matrix Type (Thermoset Composites, Thermoplastic Composites (CFRTP / GFRTP)), By Manufacturing Process (Resin Transfer Molding (RTM), Sheet Molding Compound (SMC), Prepreg / Autoclave, Compression Molding, Injection Molding, Filament Winding, Pultrusion, 3D Printing / Additive Manufacturing), By Application (Body Panels & Exterior Structures, Chassis & Frame Structures, Interior Components, Powertrain & Engine Components, Battery Enclosures (EV), Underbody & Floor Systems), By Vehicle Type (Passenger Cars, Commercial Vehicles, Electric Vehicles (BEV / PHEV), Sports & Performance Vehicles, Light Commercial Vehicles (LCVs))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Automotive Lightweight Composite Market

Published Date : 14 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date