- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Future of Autonomous Air Taxi Market Hit $27.9B by 2034 | CAGR 33.2%

Global Autonomous Air Taxi Market Size, Share, Analysis Report By Vehicle Type (eVTOL Aircraft, Conventional Aircraft), Technology (Automation, Electric Propulsion), Application (Passenger Transport, Cargo Transport), Operation Mode (Piloted, Autonomous), End User (Government, Private), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

Report Overview

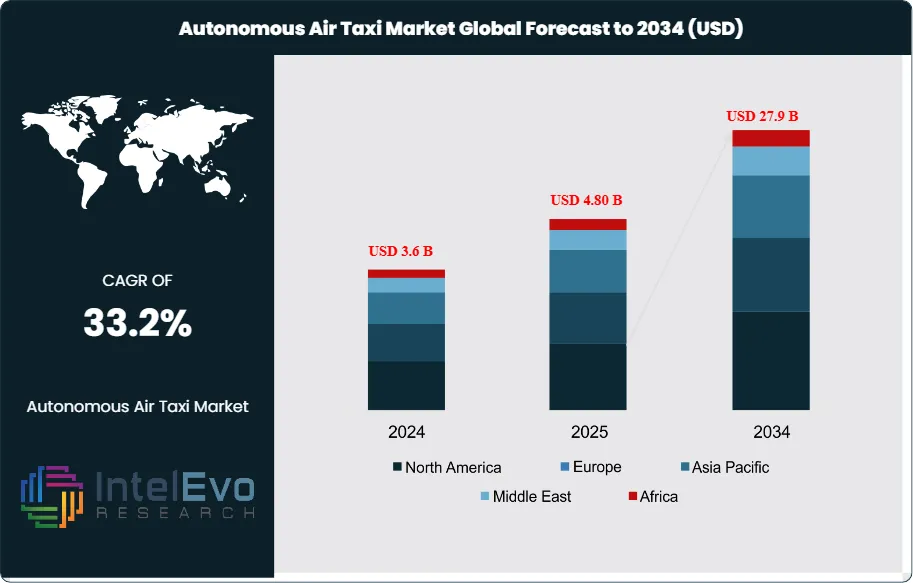

The Global Autonomous Air Taxi Market size is expected to be worth around USD 27.9 Billion by 2034, up from USD 3.6 Billion in 2024, growing at a CAGR of 33.2% during the forecast period from 2024 to 2034. The market outlook reflects rising demand for faster, eco-friendly urban transportation solutions. Autonomous air taxis are set to transform mobility across megacities worldwide.

Get More Information about this report -

Request Free Sample ReportThe global autonomous air taxi market is a segment of urban air mobility (UAM) focusing on developing and deploying electric vertical take-off and landing (eVTOL) aircraft for passenger transport. These air taxis aim to alleviate urban congestion by offering efficient aerial transportation. The market is currently characterized by significant investments from both private and public sectors, advancements in technology, and an increasing focus on sustainability in transportation.

Several factors are driving the growth of the autonomous air taxi market. Key growth dynamics include advancements in aerospace technologies, such as electric propulsion systems, automation, and digital air traffic management. Moreover, increasing urbanization, rising traffic congestion, and the demand for faster transportation solutions are propelling interest in air taxis. Investments from major players like Joby Aviation, Airbus, and EHang are fostering innovation, making air travel more accessible. Additionally, government initiatives supporting urban air mobility infrastructure, including vertiports and charging stations, are critical enablers of market expansion.

North America is expected to lead the autonomous air taxi market, driven by substantial technological advancements and a strong focus on innovation. The United States, in particular, is a hotspot for UAM development, with numerous companies testing and deploying eVTOL aircraft. Europe is also witnessing significant growth, with initiatives aimed at integrating air taxis into existing transportation networks. Meanwhile, the Asia-Pacific region is emerging as a crucial player, fueled by increasing investments and a rising demand for new transportation modalities in densely populated cities like Tokyo and Singapore.

The COVID-19 pandemic had a notable impact on the autonomous air taxi market, initially causing delays in testing and regulatory approvals. However, the crisis also accelerated interest in alternative transportation modes due to concerns over public health and safety. The push for efficient and less crowded travel options has renewed focus on air mobility solutions, as stakeholders recognize the potential of air taxis to provide safer, faster, and more efficient transportation post-pandemic. The resilience demonstrated by companies during this challenging period has further solidified the market's long-term prospects.

, Technology (Automation, Electric Propulsion), Application (Passenger Transport, Cargo Transport), Operation Mode (Piloted, Autonomous), End User (Government, Private), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Key Takeaways

- Market Growth: The global autonomous air taxi market is projected to reach USD 27.9 Billion by 2034, growing at a robust CAGR of 33.2%, indicating strong market expansion driven by technological advancements and increasing urbanization.

- Vehicle Type Analysis: eVTOL aircraft dominate the vehicle type segment, accounting for a significant share due to their efficiency and ability to operate in urban environments. Their design caters to both passenger and cargo transport, making them versatile for various applications.

- Technology Analysis: The automation segment is crucial for enhancing operational efficiency in air taxis. With advancements in digital air traffic management and safety protocols, automation technologies are expected to significantly reduce human error and operational costs.

- Driver: The increasing demand for faster, more efficient transportation solutions in urban areas is a key driver. Factors such as rising traffic congestion and urbanization are pushing stakeholders to invest in air mobility solutions.

- Restraint: High development and operational costs pose significant challenges to market growth. Additionally, stringent regulatory requirements can slow down the pace of innovation and deployment of autonomous air taxis.

- Opportunity: The growing focus on sustainable urban transport provides opportunities for innovation. Developing eco-friendly eVTOL designs can attract investments and encourage the adoption of air mobility solutions, especially in environmentally conscious regions.

- Trend: A notable trend is the rise of partnerships between tech companies and aviation firms to develop air taxi solutions, enhancing research and innovation in the market.

- Regional Analysis: North America is projected to lead the market, followed by Europe and Asia-Pacific, driven by significant investments in UAM technologies and the presence of major industry players, indicating high growth potential in these regions

Vehicle Type:

The vehicle type segment of the autonomous air taxi market is primarily divided into electric vertical take-off and landing (eVTOL) aircraft and conventional aircraft. eVTOLs are gaining traction due to their ability to operate in urban environments without the need for lengthy runways, facilitating easier access to city centers. Their design allows for greater efficiency and reduced noise levels compared to traditional helicopters. As technology advances, eVTOLs are becoming increasingly reliable and cost-effective, appealing to both passenger and cargo services. The growing emphasis on sustainability further bolsters the demand for electric aircraft, making eVTOLs a key player in the future of urban air mobility.

Propulsion Type:

The propulsion type segment of the Global Autonomous Air Taxi Market is divided into Fully Electric, Hybrid, and Hydrogen-based systems. Each represents different technological progress and adoption trends. Fully electric air taxis currently lead in development, thanks to quick advancements in battery technology, lower emissions, and cost efficiency. Their ability to scale and fit with global sustainability goals makes them the favored option for early commercialization.

Hybrid propulsion systems combine electric and conventional fuel sources. They act as a bridge to tackle the issues of limited battery capacity and range. These systems are especially suitable for intercity travel, where longer endurance is needed. On the other hand, hydrogen-based air taxis are a new area of interest. They have the potential for zero-emission flights with longer ranges and quicker refueling times compared to batteries. While still in early development, hydrogen propulsion is attracting attention as investments in hydrogen infrastructure grow. Together, these propulsion types will influence the technological path and market potential of urban air mobility solutions around the world.

Application:

The application segment is primarily categorized into passenger transport and cargo transport. Passenger transport is expected to dominate the market, driven by increasing demand for quick and efficient urban mobility solutions. Air taxis can significantly reduce travel time compared to traditional ground transport, making them an attractive option for commuters. On the other hand, the cargo transport application is emerging, driven by the need for rapid delivery services in urban areas. Companies are exploring air taxis for delivering goods, which can provide a competitive edge in logistics. As the market matures, both applications will likely see substantial growth, driven by advancements in technology and infrastructure.

Operation Mode:

The operation mode segment includes piloted and autonomous air taxis. While piloted air taxis are currently more common, the market is progressively shifting towards fully autonomous operations. Piloted air taxis can serve as a transitional solution, allowing for regulatory compliance and public acceptance as autonomous technology develops. However, the long-term vision focuses on achieving complete autonomy, which promises to enhance operational efficiency and reduce costs. Autonomous operation will also eliminate the need for onboard pilots, allowing air taxi services to operate more frequently and flexibly. This shift is crucial for the overall growth of the autonomous air taxi market.

End User:

The end-user segment comprises government and private sectors. Government use of autonomous air taxis primarily focuses on public transportation initiatives, urban planning, and emergency services. Governments are actively investing in infrastructure to support urban air mobility, recognizing its potential to alleviate traffic congestion and enhance urban connectivity. Conversely, the private sector, including individuals and corporations, is increasingly interested in air taxis for personal and business travel. The demand from both segments is expected to drive market growth, as air taxis become more integrated into existing transportation systems. Strategic partnerships between public entities and private companies are also anticipated to foster innovation and deployment.

Region Analysis:

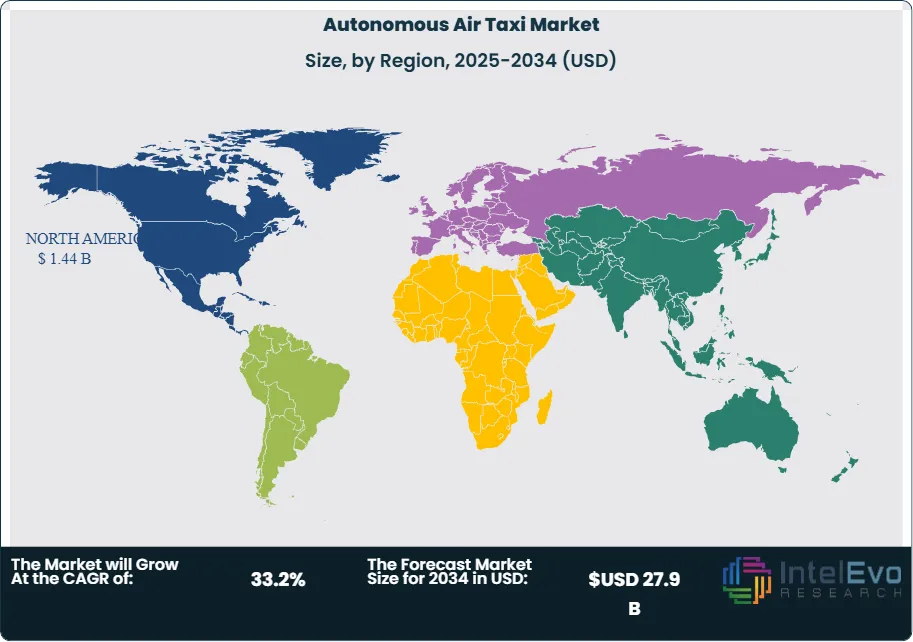

North America Leads with Significant Market Share in the Autonomous Air Taxi Market: North America holds the largest market share in the autonomous air taxi market, accounting for over 40% of the total market value. This dominance is driven by several factors, including substantial investments in urban air mobility technologies, the presence of major players like Uber and Joby Aviation, and a robust regulatory framework. The region's established aerospace infrastructure facilitates testing and deployment, enabling faster integration of air taxis into existing transportation networks. Moreover, urbanization and traffic congestion in major cities like New York and Los Angeles further fuel the demand for efficient aerial transport solutions. North America's commitment to sustainability and innovation also propels advancements in electric vertical take-off and landing (eVTOL) technologies, solidifying its leadership position in the global market.

Asia-Pacific is projected to be the fastest-growing region in the autonomous air taxi market, with a CAGR exceeding 25% through 2034. The rapid urbanization in countries like China and India, coupled with an increasing middle-class population, drives the demand for innovative transport solutions. Governments in the region are prioritizing infrastructure development to accommodate aerial mobility, with initiatives such as the Urban Air Mobility (UAM) pilot programs gaining momentum. Additionally, major cities like Tokyo and Singapore are exploring air taxi services to alleviate severe traffic congestion. Furthermore, investments in smart city projects and advancements in drone technology further enhance growth potential. While Europe is witnessing steady growth due to regulatory advancements and environmental initiatives, regions like Latin America and the Middle East and Africa are gradually exploring opportunities, focusing on enhancing urban connectivity and addressing transportation challenges

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Type:

- Multicopter

- Quadcopter

- Hybrid

- Others

By Vehicle Type:

- eVTOL Aircraft

- Conventional Aircraft

By Range:

- Intracity

- Intercity

By Propulsion Type:

- Fully Electric

- Hybrid

- Hydrogen-based

By Operation Mode:

- Piloted

- Autonomous

By End User:

- Government

- Private

By Application:

- Passenger Transport

- Cargo & Logistics

- Air Ambulance & Emergency Services

- Others

By Region:

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.6 B |

| Forecast Revenue (2034) | USD 27.9 B |

| CAGR (2025-2034) | 33.2% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type: (Multicopter, Quadcopter, Hybrid, Others), By Vehicle Type: (eVTOL Aircraft, Conventional Aircraft), By Range: (Intracity, Intercity), By Propulsion Type: (Fully Electric, Hybrid, Hydrogen-based), By Operation Mode: (Piloted, Autonomous), By End User: (Government, Private), By Application: (Passenger Transport, Cargo & Logistics, Air Ambulance & Emergency Services, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Joby Aviation, Volocopter, EHang, Lilium, Urban Aeronautics, Terrafugia, Bell Textron Inc., Boeing, Airbus, Hyundai, Pipistrel, Kitty Hawk, Sierra Nevada Corporation, Karem Aircraft, Aurora Flight Sciences, Alpha Electro, Wisk Aero, Airspace Experience Technologies (ASX), Ascendance Flight Technologies, Heerema Marine Contractors |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Technology (Automation, Electric Propulsion), Application (Passenger Transport, Cargo Transport), Operation Mode (Piloted, Autonomous), End User (Government, Private), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Technology (Automation, Electric Propulsion), Application (Passenger Transport, Cargo Transport), Operation Mode (Piloted, Autonomous), End User (Government, Private), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Technology (Automation, Electric Propulsion), Application (Passenger Transport, Cargo Transport), Operation Mode (Piloted, Autonomous), End User (Government, Private), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Frequently Asked Questions

How big is the Autonomous Air Taxi Market?

The Autonomous Air Taxi Market will grow from USD 3.6B in 2024 to USD 27.9B by 2034 at 33.2% CAGR, driven by eco-friendly urban mobility demand.

Who are the major players in the Autonomous Air Taxi Market?

Joby Aviation, Volocopter, EHang, Lilium, Urban Aeronautics, Terrafugia, Bell Textron Inc., Boeing, Airbus, Hyundai, Pipistrel, Kitty Hawk, Sierra Nevada Corporation, Karem Aircraft, Aurora Flight Sciences, Alpha Electro, Wisk Aero, Airspace Experience Technologies (ASX), Ascendance Flight Technologies, Heerema Marine Contractors

Which segments covered the Autonomous Air Taxi Market?

By Type: (Multicopter, Quadcopter, Hybrid, Others), By Vehicle Type: (eVTOL Aircraft, Conventional Aircraft), By Range: (Intracity, Intercity), By Propulsion Type: (Fully Electric, Hybrid, Hydrogen-based), By Operation Mode: (Piloted, Autonomous), By End User: (Government, Private), By Application: (Passenger Transport, Cargo & Logistics, Air Ambulance & Emergency Services, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date