- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oil & Gas Inspection Drone Market Size & Forecast 2034 | CAGR 13.1%

Global Autonomous Inspection Drone for Oil and Gas Market Size, Share, Growth & Industry Analysis By Drone Type (Multi-Rotor, Fixed-Wing, Hybrid VTOL Drones), By Application (Fixed Asset Integrity Inspection, Pipeline Leak Detection & Monitoring, Offshore Structural Inspection, Environmental & Emissions Monitoring), By Operation (Upstream, Midstream, Downstream), By End-User (NOCs, IOCs, Independent Operators, Third-Party Inspection Firms) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

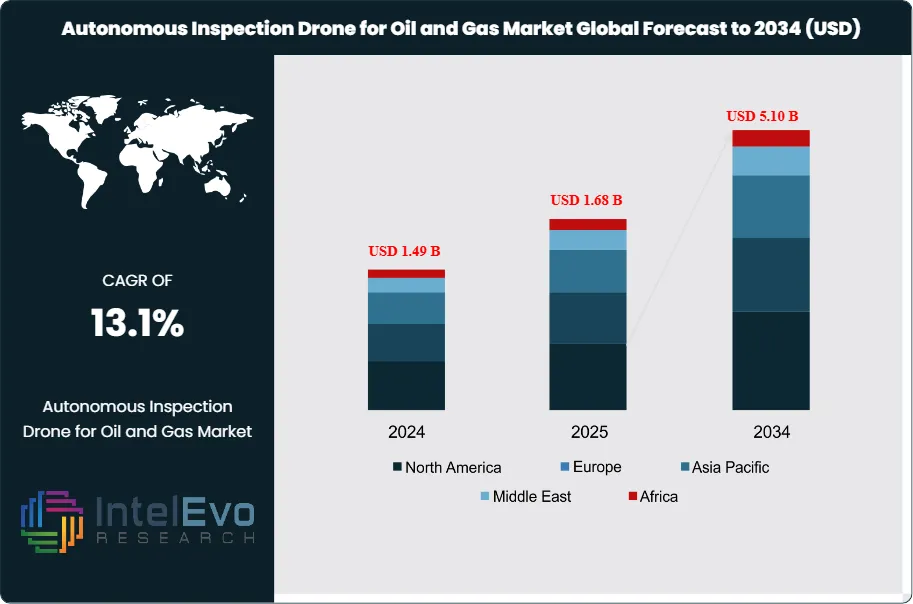

| USD 1.68 Billion | USD 5.10 Billion | 13.1% | North America, 36.9% |

The Autonomous Inspection Drone for Oil and Gas Market was valued at approximately USD 1.49 Billion in 2024 and reached USD 1.68 Billion in 2025. The market is projected to grow to USD 5.10 Billion by 2034, expanding at a CAGR of 13.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 3.42 Billion over the analysis period, driven by mounting pressure on operators to reduce inspection-related fatalities, cut OPEX associated with traditional rope-access and scaffolding methods, and comply with tightening emissions and integrity regulations enforced by the BSEE, PHMSA, and analogous bodies in Europe and the Middle East.

Get More Information about this report -

Request Free Sample ReportThe Autonomous Inspection Drone for Oil and Gas market sits at the intersection of unmanned aerial vehicle technology, AI-driven computer vision, and industrial asset management. These platforms execute repeatable inspection missions across flare stacks, storage tanks, processing columns, pipelines, offshore jacket structures, and subsea risers, capturing high-resolution visual, thermal, and LiDAR data without placing human inspectors in hazardous environments. The transition from piloted drone surveys requiring line-of-sight operators to fully autonomous drone-in-a-box systems operating under beyond visual line of sight rules represents the central technology shift defining the current market cycle. The U.S. FAA's BVLOS rulemaking framework, finalized in 2024, has materially reduced the regulatory barrier for continuous autonomous patrol of pipeline corridors, tank farms, and refinery perimeters in the United States, accelerating commercial deployments.

Demand within the Autonomous Inspection Drone for Oil and Gas market is concentrated in upstream and midstream operations, which together represent 72.4% of 2025 revenues. Offshore assets present particularly strong growth prospects: the International Association of Oil and Gas Producers estimates that confined space and at-height inspection activities account for 38% of all O&G occupational injuries globally, creating a compelling safety and liability case for autonomous drone substitution. The cost differential is equally compelling; a single rope-access inspection campaign on a typical North Sea jacket platform averages USD 850,000, while an equivalent autonomous drone survey costs USD 120,000–180,000 including data analytics processing, representing a 75–85% cost reduction per inspection cycle.

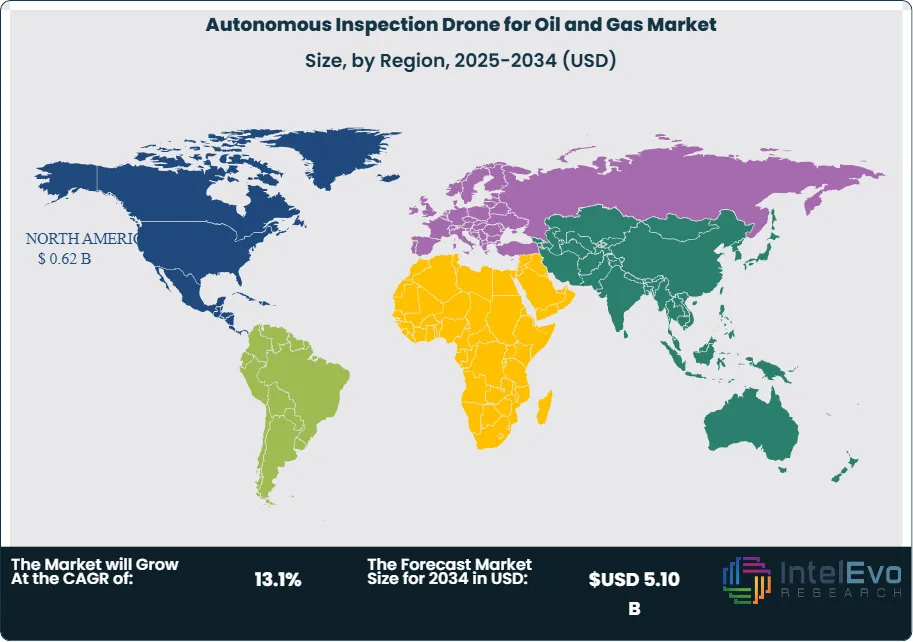

North America holds the largest regional share at 36.9% of 2025 revenues, driven by Permian Basin tank battery inspections and Gulf of Mexico offshore asset monitoring. The Middle East and Africa region is the fastest-growing market through 2034, as NOC digital transformation programs in Saudi Arabia and the UAE incorporate autonomous drone inspection as a standard asset integrity tool. Technology consolidation is accelerating, with drone hardware manufacturers forming data analytics partnerships and oilfield service majors acquiring specialist inspection drone firms to build integrated OPEX solutions. These structural forces will sustain above-market growth for the Autonomous Inspection Drone for Oil and Gas market through 2034.

, By Application (Fixed Asset Integrity Inspection, Pipeline Leak Detection & Monitoring, Offshore Structural Inspection, Environmental & Emissions Monitoring), By Operation (Upstream, Midstream, Downstream), By End-User (NOCs, IOCs, Independent Operators, Third-Party Inspection Firms) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global Autonomous Inspection Drone for Oil and Gas market was valued at USD 1.68 Billion in 2025 and is forecast to reach USD 5.10 Billion by 2034, registering a CAGR of 13.1% during the forecast period 2025–2034.

- Segment Dominance: By drone type, multi-rotor drones held the largest share at 54.6% of 2025 market revenues, owing to their maneuverability in confined spaces including storage tanks, process columns, and offshore module interiors.

- Segment Dominance: By application, fixed asset integrity inspection — covering flare stacks, storage tanks, and pressure vessels — accounted for 41.8% of 2025 revenues, driven by mandatory API 510, API 653, and API 570 inspection cycles.

- Driver: The total cost advantage of autonomous drone inspection over traditional rope-access and scaffolding methods generates a 75–85% OPEX saving per inspection cycle, accelerating adoption across upstream and midstream operators and contributing an estimated USD 1.1 Billion in incremental market revenue through 2028.

- Restraint: Regulatory fragmentation in BVLOS airspace authorization across markets including the EU, India, and Southeast Asia delays commercial autonomous patrol deployment by 18–24 months per jurisdiction, constraining growth in otherwise high-potential markets.

- Opportunity: Continuous autonomous methane leak surveillance across the approximately 2.9 Million miles of U.S. gas pipeline network represents an addressable market of USD 780 Million through 2030, supported by EPA methane reporting mandates and IRA methane waste fee provisions.

- Trend: AI-powered defect detection using computer vision models trained on O&G-specific corrosion, cracking, and coating degradation datasets is the dominant product differentiation trend; leading vendors reported defect detection accuracy rates exceeding 94% in 2025 versus 71% for generic vision models applied to industrial surfaces.

- Regional Analysis: North America led the Autonomous Inspection Drone for Oil and Gas market with a 36.9% share, generating USD 0.62 Billion in 2025 revenues, underpinned by BVLOS regulatory progress and dense Permian Basin and Gulf of Mexico asset concentrations.

Competitive Landscape Overview

The Autonomous Inspection Drone for Oil and Gas market is fragmented, with the top four players — Flyability SA, Percepto Ltd, Aerodyne Group, and BVLOS Technology — collectively holding approximately 34.2% of global revenues in 2025. Competition is primarily technology-driven, focused on autonomy depth, AI defect detection accuracy, and sensor payload versatility. M&A activity intensified between 2024 and 2026, with oilfield service majors and inspection service providers acquiring specialist drone firms to integrate hardware, software, and analytics into subscription-based inspection-as-a-service models. New entrants from the defense drone sector are targeting the O&G market with hardened, all-weather airframes.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Flyability SA | Switzerland | Leader | Elios 3 Confined Space Drone | Europe / Global | Launched Elios 3 Industrial with enhanced LiDAR mapping for refinery inspection (Feb 2025) |

| Percepto Ltd | Israel | Leader | Percepto Arc Autonomous Drone-in-a-Box | North America / MEA | Deployed Arc at 6 Saudi Aramco onshore sites; 3-year managed services contract (May 2025) |

| Aerodyne Group | Malaysia | Leader | Drone-as-a-Service O&G Suite | Asia Pacific / MEA | Acquired Australian drone inspection firm Converge Analytics for USD 28M (Jan 2025) |

| BVLOS Technology Inc. | Canada | Leader | BeyondLine Industrial Inspection UAV | North America | Secured Transport Canada BVLOS blanket exemption for pipeline corridor operations (Aug 2025) |

| SLB (AeroDyne / Robotics Div.) | USA | Challenger | SLB Autonomous Asset Monitor | Global Upstream | Integrated drone inspection data with Delfi Connect subsurface platform (Mar 2025) |

| Apellix Inc. | USA | Challenger | Apellix W1 Spray and Inspect Drone | North America | Partnered with Sherwin-Williams to bundle corrosion coating and drone inspection (Jun 2025) |

| Easy Aerial Inc. | USA | Challenger | SAMS (Scout Autonomous Monitoring) | North America / MEA | Awarded USD 12M U.S. Army Corps contract for pipeline monitoring (Apr 2025) |

| Robotic Skies | USA | Niche Player | Pipeline Patrol Fixed-Wing UAV | North America | Launched AI-powered leak signature detection firmware v3.1 (Sep 2025) |

| Terra Drone Corporation | Japan | Niche Player | Terra Lidar One Inspection Drone | Asia Pacific | Expanded into Middle East via ADNOC offshore inspection contract (Jan 2026) |

| Azur Drones | France | Niche Player | Skeyetech Autonomous Security & Inspection UAV | Europe | Signed perimeter and flare stack inspection deal with TotalEnergies Normandy (Nov 2025) |

By Drone Type

The Autonomous Inspection Drone for Oil and Gas market by Drone Type divides into multi-rotor, fixed-wing, and hybrid VTOL configurations. Multi-rotor drones held the dominant share at 54.6% of 2025 revenues, equivalent to USD 0.92 Billion. Their hovering capability, compact footprint, and ability to navigate confined environments — storage tank interiors, heat exchanger bays, and module spaces on FPSOs — make them the preferred platform for detailed close-up inspection. Advances in collision-tolerant cage-protected designs, pioneered by Flyability's Elios series, have expanded multi-rotor deployment into Class I, Division 1 hazardous areas, eliminating the need for gas purging prior to inspection. Multi-rotor systems carry visual, thermal, and gas detection payloads simultaneously and are increasingly paired with drone-in-a-box stations enabling fully autonomous sorties without operator intervention. Fixed-wing drones captured 28.3% of 2025 revenues, at USD 0.48 Billion, and are deployed for pipeline corridor patrol, perimeter surveillance, and large-area tank farm scanning where endurance and coverage rate outweigh close-proximity maneuverability. Their operational range of 50–120 kilometers per sortie makes them economically superior for linear pipeline inspection. Hybrid VTOL drones represented 17.1% of 2025 revenues at USD 0.29 Billion, combining fixed-wing range with multi-rotor precision for offshore platform surveys and remote midstream compressor station inspections.

By Application

Fixed asset integrity inspection accounted for the largest share at 41.8% of 2025 revenues, generating USD 0.70 Billion. This application covers mandatory inspection cycles for atmospheric storage tanks under API 653, pressure vessels under API 510, and piping systems under API 570, all of which require documented visual and measurement data at defined intervals. Autonomous drone platforms equipped with LiDAR and high-resolution cameras reduce the inspection duration for a standard 10-meter-diameter storage tank from 3–4 days of scaffolding preparation and rope-access work to 4–6 hours of autonomous flight and AI-processed reporting. Pipeline leak detection and monitoring represented 29.4% of 2025 revenues, at USD 0.49 Billion, driven by PHMSA Mega Rule requirements for gas transmission operators and the expanding adoption of hyperspectral and methane-sensing payloads capable of detecting leaks as small as 10 parts per million at flight altitudes up to 30 meters. Offshore structural inspection — covering jacket legs, risers, caissons, and FPSO hull sections — captured 18.6% share at USD 0.31 Billion in 2025, a rapidly growing application as North Sea and Gulf of Mexico operators seek cost-effective alternatives to remotely operated vehicles for above-waterline inspections. Environmental and emissions monitoring represented the remaining 10.2% at USD 0.17 Billion.

By Operation

The Autonomous Inspection Drone for Oil and Gas market segments into upstream, midstream, and downstream verticals. Upstream held the largest share at 44.8% in 2025, generating USD 0.75 Billion, driven by wellhead equipment inspections, FPSO deck surveys, and offshore jacket monitoring. Production facilities with multiple wellheads and processing trains benefit significantly from autonomous drone patrol, where a single drone-in-a-box unit can cover up to 25 wellheads per day compared to 6–8 via manual inspection. Midstream captured 27.6% at USD 0.46 Billion in 2025, primarily through pipeline corridor patrol, compressor station inspections, and gas processing plant monitoring. Regulatory pressure from PHMSA's integrity management requirements makes midstream the segment with the highest compliance-driven procurement velocity. Downstream operations — refineries, petrochemical complexes, and LNG terminals — represented 27.6% of 2025 revenues at USD 0.46 Billion, where turnaround maintenance optimization is the primary use case; operators report that pre-turnaround drone surveys reduce scaffold planning time by 40% and identify 15–20% more defects than prior manual visual inspection records.

By End-User

National Oil Companies held the largest share at 37.4% of 2025 revenues, equivalent to USD 0.63 Billion, led by Saudi Aramco, ADNOC, QatarEnergy, and Petrobras — all of which have active drone inspection procurement programs. Integrated oil companies accounted for 30.2% at USD 0.51 Billion, with Shell's asset inspection digitalization program and TotalEnergies' drone-in-a-box deployments across European refineries serving as sector benchmarks. Independent operators represented 21.8% at USD 0.37 Billion, increasingly adopting drone-as-a-service subscription models to avoid capital expenditure on hardware. Third-party inspection service companies — including Bureau Veritas, SGS, and Applus+ — held 10.6% at USD 0.18 Billion, embedding autonomous drone capability into their service offerings to differentiate from manual inspection competitors.

Regional Analysis

North America

Led the Autonomous Inspection Drone for Oil and Gas market in 2025 with a 36.9% share, generating USD 0.62 Billion in revenues. The United States accounts for the bulk of this figure, with Permian Basin operators deploying multi-rotor drone-in-a-box systems for continuous tank battery monitoring and wellhead integrity surveillance. The FAA's BVLOS regulatory framework, which issued operational authorizations to 14 O&G-focused drone operators in 2024–2025, directly catalyzed commercial deployment of autonomous pipeline patrol. Texas, Oklahoma, and New Mexico collectively represent the highest density of active drone inspection programs in the world. Canada contributes meaningfully through drone-based pipeline inspection in Alberta's heavy oil corridors and offshore East Coast asset monitoring. The Gulf of Mexico offshore sector is driving adoption of multi-sensor autonomous drones for platform structural inspection, with operators reporting 60–70% reductions in manned inspection helicopter deployments since 2023. U.S. government procurement of autonomous inspection drones for federal pipeline and energy infrastructure monitoring added approximately USD 45 Million in incremental demand in 2025.

Europe

Held 24.3% of the Autonomous Inspection Drone for Oil and Gas market in 2025, at USD 0.41 Billion. The North Sea — spanning UK, Norwegian, and Danish sectors — represents the primary deployment base, with aging infrastructure requiring frequent structural and corrosion inspections on jacket platforms and FPSO units. The UK Civil Aviation Authority and Norway's Civil Aviation Authority have both issued BVLOS permits for offshore platform inspection, enabling fully autonomous sorties from platform-mounted drone-in-a-box stations. The Netherlands, as a major gas distribution hub, is deploying fixed-wing autonomous drones for onshore pipeline patrol under SodM regulatory guidelines. France's refining and petrochemical sector contributes demand through TotalEnergies and Esso's refinery inspection programs. EU drone regulation under the EASA U-Space framework is progressively enabling autonomous O&G operations across member states, with a 2025 update extending SPECIFIC category permits to cover industrial inspection BVLOS operations.

Asia Pacific

Accounted for 21.8% of the Autonomous Inspection Drone for Oil and Gas market in 2025, generating USD 0.37 Billion. Malaysia is the regional leader, with Petronas deploying Aerodyne Group's drone-as-a-service platform across its offshore platform fleet in the South China Sea, covering 143 fixed platforms and 14 FPSOs. Australia's offshore LNG sector — including Gorgon, Ichthys, and Prelude FLNG — is integrating autonomous inspection drones into turnaround planning workflows, supported by CASA's expanded BVLOS trial program. China's CNOOC and Sinopec operate internal drone inspection programs focused on refinery and petrochemical plants, though regulatory restrictions on foreign drone technology constrain the addressable market for international vendors. India's ONGC has initiated drone inspection pilots for onshore oil fields in Gujarat and Rajasthan, supported by DGCA's relaxed drone rules from 2024. Japan's drone inspection market for O&G is maturing, with Inpex and Eneos deploying cage-protected multi-rotor systems for LNG terminal inspection.

Latin America

Held 9.8% of the Autonomous Inspection Drone for Oil and Gas market in 2025, generating USD 0.16 Billion. Brazil dominates the region, with Petrobras operating the world's largest deep-water FPSO fleet and facing persistent asset integrity challenges that drone technology addresses cost-effectively. Petrobras deployed autonomous drone inspection across 18 FPSO vessels in 2025, reducing inspection-related OPEX by an estimated USD 35 Million annually. Colombia's Ecopetrol has initiated fixed-wing pipeline patrol over the Llanos Basin, a region with historically high pipeline third-party interference risk. Argentina's Vaca Muerta shale development is generating upstream well site inspection demand. Infrastructure gaps and import duties on drone hardware in some markets limit growth rates, though drone-as-a-service models are mitigating capital barriers for mid-tier operators.

Middle East and Africa

Contributed 7.2% of the Autonomous Inspection Drone for Oil and Gas market in 2025, at USD 0.12 Billion, and represents the fastest-growing region through 2034. Saudi Arabia is the anchor market, with Saudi Aramco's Digital Transformation Program allocating dedicated budget for autonomous inspection drone deployment across its onshore and offshore asset base. ADNOC's partnership with Percepto for drone-in-a-box deployment across Abu Dhabi's onshore fields established a reference model for NOC autonomous inspection adoption. Qatar's LNG infrastructure, currently undergoing a 64 MTPA capacity expansion, presents significant inspection drone demand for new plant commissioning and ongoing turnaround programs. Africa's developing markets — Nigeria, Angola, and Egypt — are seeing initial drone inspection deployments by IOC operators seeking to reduce exposure of field personnel to security and environmental risks in remote production areas.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Drone Type

- Multi-Rotor Drone

- Fixed-Wing Drone

- Hybrid VTOL Drone

By Application

- Fixed Asset Integrity Inspection

- Pipeline Leak Detection and Monitoring

- Offshore Structural Inspection

- Environmental and Emissions Monitoring

By Operation

- Upstream

- Midstream

- Downstream

By End-User

- National Oil Companies (NOCs)

- Integrated Oil Companies (IOCs)

- Independent Operators

- Third-Party Inspection Service Companies

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.68 B |

| Forecast Revenue (2034) | USD 5.10 B |

| CAGR (2025-2034) | 13.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Drone Type, (Multi-Rotor Drone, Fixed-Wing Drone, Hybrid VTOL Drone), By Application, (Fixed Asset Integrity Inspection, Pipeline Leak Detection and Monitoring, Offshore Structural Inspection, Environmental and Emissions Monitoring), By Operation, (Upstream, Midstream, Downstream), By End-User, (National Oil Companies (NOCs), Integrated Oil Companies (IOCs), Independent Operators, Third-Party Inspection Service Companies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | FLYABILITY SA, PERCEPTO LTD, AERODYNE GROUP, BVLOS TECHNOLOGY INC., SLB (AUTONOMOUS ASSET MONITORING DIVISION), APELLIX INC., EASY AERIAL INC., ROBOTIC SKIES, TERRA DRONE CORPORATION, AZUR DRONES, SKYDIO INC., DELAIR SAS, INTEL FALCON 8+ (INTEL DRONE GROUP), BOEING INSITU, BAKER HUGHES (AERIAL INSPECTION SERVICES), BUREAU VERITAS (DRONE INSPECTION SERVICES), APPLUS+ VELOSI (DRONE INSPECTION DIVISION), CYBERHAWK INNOVATIONS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Fixed Asset Integrity Inspection, Pipeline Leak Detection & Monitoring, Offshore Structural Inspection, Environmental & Emissions Monitoring), By Operation (Upstream, Midstream, Downstream), By End-User (NOCs, IOCs, Independent Operators, Third-Party Inspection Firms) Industry Trends & Forecast 2026–2034")

, By Application (Fixed Asset Integrity Inspection, Pipeline Leak Detection & Monitoring, Offshore Structural Inspection, Environmental & Emissions Monitoring), By Operation (Upstream, Midstream, Downstream), By End-User (NOCs, IOCs, Independent Operators, Third-Party Inspection Firms) Industry Trends & Forecast 2026–2034")

, By Application (Fixed Asset Integrity Inspection, Pipeline Leak Detection & Monitoring, Offshore Structural Inspection, Environmental & Emissions Monitoring), By Operation (Upstream, Midstream, Downstream), By End-User (NOCs, IOCs, Independent Operators, Third-Party Inspection Firms) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Autonomous Inspection Drone for Oil and Gas Market?

Global Oil & Gas Drone Market to reach USD 5.10B by 2034 with a 13.1% CAGR. Discover how AI-powered UAVs reduce inspection times by 61% and enhance safety in offshore environments.

Who are the major players in the Autonomous Inspection Drone for Oil and Gas Market?

FLYABILITY SA, PERCEPTO LTD, AERODYNE GROUP, BVLOS TECHNOLOGY INC., SLB (AUTONOMOUS ASSET MONITORING DIVISION), APELLIX INC., EASY AERIAL INC., ROBOTIC SKIES, TERRA DRONE CORPORATION, AZUR DRONES, SKYDIO INC., DELAIR SAS, INTEL FALCON 8+ (INTEL DRONE GROUP), BOEING INSITU, BAKER HUGHES (AERIAL INSPECTION SERVICES), BUREAU VERITAS (DRONE INSPECTION SERVICES), APPLUS+ VELOSI (DRONE INSPECTION DIVISION), CYBERHAWK INNOVATIONS, Others

Which segments covered the Autonomous Inspection Drone for Oil and Gas Market?

By Drone Type, (Multi-Rotor Drone, Fixed-Wing Drone, Hybrid VTOL Drone), By Application, (Fixed Asset Integrity Inspection, Pipeline Leak Detection and Monitoring, Offshore Structural Inspection, Environmental and Emissions Monitoring), By Operation, (Upstream, Midstream, Downstream), By End-User, (National Oil Companies (NOCs), Integrated Oil Companies (IOCs), Independent Operators, Third-Party Inspection Service Companies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Autonomous Inspection Drone for Oil and Gas Market

Published Date : 01 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date