- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Autonomous Mobile Robot Market Size, Share & Forecast | CAGR 15.1%

Global Autonomous Mobile Robot Market Size, Share & Industry Analysis By Component (Hardware, Software, Services), By Robots Type (Goods-to-Person Picking, Self-Driving Forklifts, Autonomous Inventory, Autonomous Tugger, Unmanned Ground Vehicles, Delivery and Transport, Inspection and Surveillance, Cleaning and Disinfection, Collaborative Mobile, Automated Guided Carts), By End-Use, Industry Region, Market Dynamics, Competitive Landscape, Growth Opportunities, Strategic Insights, Emerging Trends and Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

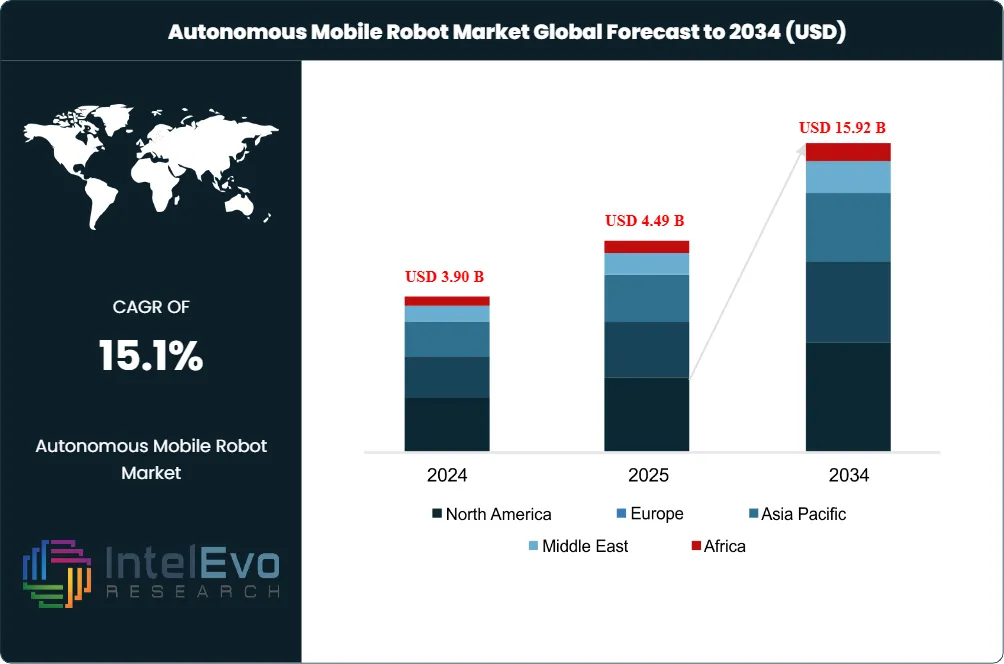

| USD 4.49 Billion | USD 15.92 Billion | 15.1% | Asia Pacific, 37.1% |

The Autonomous Mobile Robot Market was valued at USD 3.90 Billion in 2024 and USD 4.49 Billion in 2025. The market is projected to reach USD 15.92 Billion by 2034, expanding at a CAGR of 15.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 11.43 Billion over the analysis period. Autonomous mobile robots (AMRs) are self-navigating machines that use LiDAR, cameras, AI-powered SLAM algorithms, and fleet orchestration software to perform material handling, order picking, inventory transport, and inspection tasks across warehouses, factories, hospitals, and retail environments without fixed infrastructure such as magnetic strips or rails.

Get More Information about this report -

Request Free Sample ReportAmazon deployed its one-millionth warehouse robot in July 2025 at a fulfillment center in Japan, cementing its position as the world's largest manufacturer and operator of mobile robotics across more than 300 global facilities. Alongside the milestone, Amazon launched DeepFleet, a generative AI foundation model built on AWS SageMaker that coordinates fleet routing and reduces robot travel time by 10%, which at the company's scale translates into projected automation savings of USD 12.6 Billion from 2025 through 2027. The deployment validates the commercial viability of AMR fleets numbering in the hundreds of thousands within single enterprise networks, a scale that was theoretical five years ago.

Labor shortages constitute the primary structural demand driver. The European Agency for Safety and Health at Work identifies automation as essential for offsetting shrinking working-age populations across OECD nations. In the United States, warehouse vacancy rates for night and peak-season shifts remain persistently elevated, pushing logistics operators toward AMR solutions that deliver 24/7 throughput without incremental headcount. Locus Robotics surpassed 6 billion robot-assisted picks in October 2025, with throughput reaching 200 to 300 units per second across more than 350 customer sites, demonstrating that AMRs can double or triple piece-handling productivity while reducing workplace injuries by 80%.

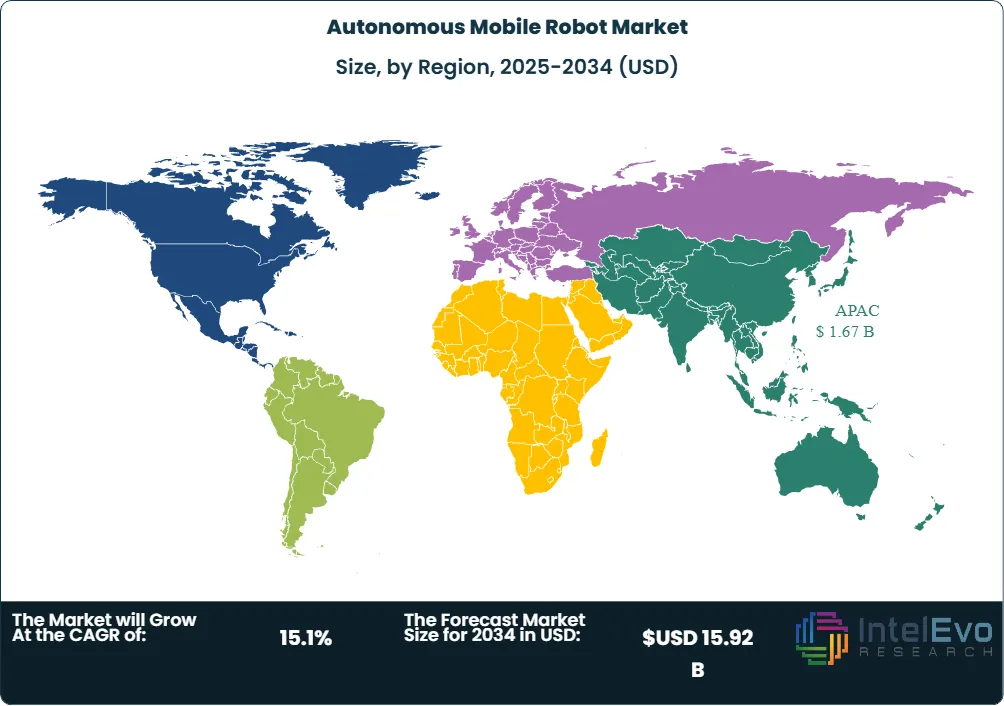

Asia Pacific held the largest regional share at 37.1% in 2025, valued at approximately USD 1.67 Billion, driven by Chinese AMR manufacturers like Geekplus Technology, which reported 31.6% year-over-year revenue growth in fiscal 2025 and achieved net profitability for the first time. Geekplus has delivered over 72,000 robots across more than 40 countries. North America represented 34.2% of the market at USD 1.54 Billion, anchored by Amazon Robotics, Locus Robotics, and the Teradyne subsidiary Mobile Industrial Robots (MiR). Europe accounted for 21.8% at approximately USD 978 million, where ABB, KUKA (part of Midea Group), and OMRON compete intensely on AI-powered Visual SLAM navigation platforms.

Market Definition & Scope

The autonomous mobile robot market is defined as the commercial segment producing and deploying self-navigating robots that use onboard sensors, AI algorithms, and fleet management software to perform material transport, order fulfillment, inspection, and logistics tasks without requiring fixed guidance infrastructure. The market encompasses goods-to-person picking robots, self-driving forklifts, autonomous inventory robots, autonomous tug/cart transport systems, and unmanned ground vehicles deployed in indoor industrial and commercial settings. Hardware components (sensors, controllers, chassis, batteries), software (navigation, fleet orchestration, WMS integration), and services (deployment, maintenance, robotics-as-a-service) are all included.

This analysis explicitly excludes automated guided vehicles (AGVs) that rely on magnetic tape, wires, or embedded floor markers for navigation. It also excludes unmanned aerial vehicles (UAVs/drones), unmanned marine vehicles, personal service robots (vacuum cleaners, lawn mowers), and fixed-infrastructure automation systems such as conveyor belts and AS/RS (automated storage and retrieval systems). The autonomous mobile robot market constitutes a rapidly growing subset of the broader mobile robotics market, which was valued at approximately USD 20.79 Billion in 2025.

, By Robots Type (Goods-to-Person Picking, Self-Driving Forklifts, Autonomous Inventory, Autonomous Tugger, Unmanned Ground Vehicles, Delivery and Transport, Inspection and Surveillance, Cleaning and Disinfection, Collaborative Mobile, Automated Guided Carts), By End-Use, Industry Region, Market Dynamics, Competitive Landscape, Growth Opportunities, Strategic Insights, Emerging Trends and Forecast 2026-2034")

Key Takeaways

- Market Growth: The autonomous mobile robot market grew from USD 4.49 Billion in 2025 to a projected USD 15.92 Billion by 2034, at a 15.1% CAGR, representing USD 11.43 Billion in absolute dollar opportunity.

- Segment Dominance (By Component): Hardware held the largest component share at 67.4% in 2025 at approximately USD 3.03 Billion, because every AMR deployment requires physical robots, sensors, and chassis as the entry point.

- Segment Dominance (By End-Use): Warehouse and logistics accounted for 32.9% of end-use revenue in 2025 at approximately USD 1.48 Billion, driven by e-commerce fulfillment demand and same-day delivery expectations.

- Driver: Persistent global labor shortages across manufacturing and logistics, combined with Amazon's demonstrated 10% fleet efficiency gain through DeepFleet AI, are compelling enterprises to deploy AMR fleets as structural workforce supplements.

- Restraint: High upfront capital costs for enterprise-scale AMR deployments, averaging USD 25,000 to USD 100,000 per unit depending on payload and capability, limit adoption among small and medium enterprises with fewer than 50 employees.

- Opportunity: The robotics-as-a-service (RaaS) subscription model represents the largest growth accelerator, lowering entry barriers by converting capital expenditure to operating expenditure and enabling facilities to scale robot fleets with seasonal demand.

- Trend: AI-powered fleet orchestration platforms, including Amazon DeepFleet and Locus LocusONE, achieved deployment across hundreds of sites by Q4 2025, enabling multi-robot coordination that reduces travel time, energy consumption, and congestion simultaneously.

- Regional: Asia Pacific led the autonomous mobile robot market with 37.1% share valued at USD 1.67 Billion in 2025, with Geekplus Technology holding the top AMR market position for seven consecutive years according to 2025 industry rankings.

Key Insights Summary

- Amazon surpassed 1 million deployed robots across its global fulfillment network by July 2025, with 75% of the company's deliveries now assisted by a robot in some capacity (Amazon, July 2025).

- Locus Robotics surpassed 6 billion robot-assisted picks in October 2025, achieving the milestone in just 24 weeks, with throughput reaching 200 to 300 units per second and 30 to 40% year-over-year volume growth (Locus Robotics, October 2025).

- Geekplus Technology reported total fiscal 2025 revenue of approximately RMB 3.17 Billion with 31.6% year-over-year growth, achieving net profitability for the first time. The company delivered over 72,000 robots to approximately 950 customers across 40+ countries (Geekplus FY2025 results, March 2026).

- The top five AMR manufacturers, KUKA AG (12.4% share), Geekplus, ABB, Zebra Technologies, and OMRON, held a combined 45.4% market share in 2025 (industry analysis, 2025).

- Global industrial robot installations reached a record 3.9 million units in 2022, with 31% year-over-year growth in automation robot development confirming that pandemic-era demand disruptions were temporary (World Robotics report).

- ABB's AMR Studio software reduces commissioning time by up to 20% and costs by up to 30% compared to conventional fleet deployment systems, enabling non-expert operators to configure and manage multi-robot fleets (ABB, May 2025).

Competitive Landscape Overview

The autonomous mobile robot market exhibits a moderately consolidated structure, with the top five players holding a combined 45.4% market share in 2025. KUKA AG (part of China's Midea Group) led with approximately 12.4% share, followed by Geekplus Technology, ABB, Zebra Technologies, and OMRON Corporation. Competition operates on three axes: AI and navigation technology depth, fleet orchestration software maturity, and deployment speed (measured in weeks from contract to operational production). Amazon Robotics, while not a third-party vendor, shapes competitive dynamics because its internal deployments of over 1 million units set performance benchmarks that commercial AMR vendors must match. The market saw consolidation activity in 2025: Zebra Technologies announced it was winding down its Fetch Robotics-based AMR division in December 2025 after the USD 290 million acquisition in 2021 failed to scale. Zebra's exit signals that hardware alone is insufficient; integrated software-plus-service platforms command higher margins and retention. Locus Robotics raised USD 117 million in Series F funding in March 2025, while Teradyne (parent of MiR) posted USD 98 million in Q4 2024 robotics revenue and projected 2025 acceleration.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product/Platform | Geo Strength | Founded | Recent Strategic Move |

| KUKA AG | Germany | Leader | KMR iiwa, AMR fleet | Global | 1898 | New software & AI org in Silicon Valley (2025) |

| Geekplus | China | Leader | Shelf-to-person AMR, Gino 1 humanoid | 40+ countries | 2015 | FY2025 net profitability; 72,000 robots delivered |

| ABB | Switzerland | Leader | Flexley Mover P603/P604 | Global | 1988 | Flexley P603 AI-powered AMR launch (Jun 2025) |

| OMRON | Japan | Leader | LD/HD series AMR | Global | 1933 | AI-powered safety feature integration (2025) |

| Locus Robotics | US | Challenger | Origin, Vector, Array | NA, EMEA, APAC | 2014 | USD 117M Series F (Mar 2025); Locus Array (Apr 2026) |

| MiR (Teradyne) | Denmark | Challenger | MiR250/600/1350 | Global | 2013 | Honeywell partnership (May 2025) |

| GreyOrange | US | Challenger | Ranger series AMR | Americas, APAC | 2011 | AI fulfillment expansion (2025) |

| Boston Dynamics | US | Niche | Stretch, Spot | NA, Europe | 1992 | Warehouse stretch deployment scaling (2025) |

By Component

The autonomous mobile robot market segmented by component was dominated by hardware in 2025, accounting for 67.4% of total revenue at approximately USD 3.03 Billion. Hardware encompasses the physical robot chassis, LiDAR and camera sensor arrays, motor drives, battery packs (lithium-ion and lead-acid), onboard compute modules, and safety systems. The hardware segment commands the largest share because every AMR deployment begins with physical unit procurement. ABB's Flexley Mover P603, launched in June 2025, exemplifies the hardware innovation trajectory: it combines AI-driven Visual SLAM navigation with a 1,500 kg payload capacity in the most compact form factor in its class, using integrated load sensing and omnidirectional mobility. Hardware average selling prices have declined 15 to 20% since 2022 because of Chinese manufacturing scale and falling LiDAR costs; a basic goods-to-person AMR from Geekplus now costs under USD 25,000 per unit.

Software held 20.8% share at approximately USD 934 million in 2025. Fleet orchestration platforms, including Amazon DeepFleet, Locus LocusONE, and ABB AMR Studio, represent the fastest-growing software category. Amazon's DeepFleet uses generative AI trained on warehouse logistics data to coordinate routing across 1 million+ robots, achieving 10% travel efficiency gains. ABB's AMR Studio reduces commissioning time by 20% and costs by 30% through no-code programming interfaces. Software margins exceed hardware margins by 25 to 30 percentage points because of recurring subscription and licensing revenue. The software segment is projected to grow at 18.4% CAGR through 2034, outpacing hardware at 13.2%.

Services comprised 11.8% of the market at approximately USD 530 million in 2025. Services include deployment and integration, ongoing maintenance, fleet management consulting, and robotics-as-a-service (RaaS) subscription models. Locus Robotics pioneered the RaaS model, enabling customers to deploy AMR fleets with zero capital expenditure, paying per-pick or per-robot fees that scale with seasonal demand. DHL Supply Chain, a Locus customer, deployed Locus Array with over 350 LocusBots at a single German site. RaaS adoption is accelerating among mid-market logistics providers and third-party logistics (3PL) companies that require flexible automation without fixed-asset commitments.

By Type

Goods-to-person picking robots held the largest type share in the autonomous mobile robot market at 38.5% in 2025, valued at approximately USD 1.73 Billion. These AMRs transport inventory shelves, totes, or bins directly to human pickers, eliminating worker travel time. Geekplus dominates this category with its shelf-to-person systems, holding the top global position for seven consecutive years. Amazon's Kiva-derived systems and Locus Robotics' Origin and Vector robots also compete in this segment. Self-driving forklifts accounted for 28.2% at USD 1.27 Billion, driven by demand for autonomous pallet transport in manufacturing and distribution. KUKA, Jungheinrich, and Crown Equipment are active competitors. Autonomous inventory robots held 18.9% at USD 849 million, performing cycle counting and stock-level verification using RFID, barcode scanning, and computer vision. Autonomous tug and cart transport systems comprised the remaining 14.4% at USD 647 million.

By End-Use

The warehouse and logistics sector led the autonomous mobile robot market by end-use in 2025 with 32.9% share at approximately USD 1.48 Billion. E-commerce growth, same-day delivery expectations, and chronic labor shortages drive investment. Amazon's 1 million-robot deployment and Locus Robotics' 6 billion-pick milestone validate the scale of warehouse AMR adoption. Manufacturing held 31.4% share at USD 1.41 Billion, where AMRs perform lineside delivery, work-in-progress transport, and material staging. ABB and KUKA dominate this segment through integration with existing factory automation infrastructure. Healthcare accounted for 12.8% at USD 575 million, with AMRs delivering medications, laboratory specimens, linens, and meals across hospital campuses. Aethon's TUG robots are deployed at over 600 hospitals globally. Retail and hospitality held 11.3% at USD 507 million, and other applications including agriculture, defense, and inspection comprised 11.6% at USD 521 million.

Regional Analysis

Asia Pacific

Asia Pacific held the largest share of the autonomous mobile robot market at 37.1% in 2025, valued at approximately USD 1.67 Billion. China is the dominant country market, led by Geekplus Technology (72,000+ robots delivered, RMB 3.17 Billion FY2025 revenue), Quicktron, and Hikrobot. Chinese AMR manufacturers combine software-centric design with aggressive pricing, making their products 30 to 40% less expensive than European and American equivalents. South Korea, Japan, and Singapore lead in robot density per 10,000 employees. The region benefits from government support for smart manufacturing initiatives and the concentration of semiconductor and electronics manufacturing, which accounts for 22.7% of all AMR deployments.

North America

North America represented 34.2% of the autonomous mobile robot market at USD 1.54 Billion in 2025. The United States accounted for USD 815 million of regional demand. Amazon's 1 million-robot network, spanning 300+ facilities, anchors the region. Locus Robotics operates over 350 sites across North America and Europe, serving customers including DHL Supply Chain, GEODIS, Staples Canada, and Carhartt. The Teradyne-Honeywell partnership announced in May 2025 integrates MiR AMRs with Honeywell's WMS software and cybersecurity platforms for logistics automation. Canada's contribution is driven by Ottawa-based Clearpath Robotics (OTTO Motors), specializing in heavy-payload industrial AMRs.

Europe

Europe accounted for 21.8% of the autonomous mobile robot market at approximately USD 978 million in 2025. Germany leads European demand through KUKA, Jungheinrich, and the KION Group. ABB's Flexley Mover P603 and P604 were unveiled at the Automatica trade show in Munich in June 2025. Denmark-based Mobile Industrial Robots (MiR), a Teradyne subsidiary, operates globally from its Odense headquarters. The European Agency for Safety and Health at Work's endorsement of automation for aging-workforce management creates institutional demand. ISO 3691-4 safety compliance requirements shape product design and certification costs for European deployments.

Latin America

Latin America held 4.2% of the autonomous mobile robot market at approximately USD 189 million in 2025. Brazil and Mexico are the primary markets, where automotive and consumer goods manufacturers deploy AMRs for lineside delivery and warehousing. Locus Robotics operates in Mexico through partnerships with GEODIS for e-commerce fulfillment. Middle East and Africa accounted for 2.7% at approximately USD 121 million, where mega-project developments in Saudi Arabia and the UAE generate demand for heavy-duty AMR systems in construction logistics and warehouse automation.

Country Analysis

The United States leads the autonomous mobile robot market with an estimated value of USD 815 million in 2025 and a country-level CAGR of 16.3% through 2034. Amazon Robotics, headquartered in North Reading, Massachusetts, deployed its one-millionth robot in July 2025 and launched DeepFleet, which coordinates fleet routing across 300+ fulfillment centers. Locus Robotics, based in Wilmington, Massachusetts, raised USD 117 million in Series F funding in March 2025 and surpassed 6 billion robot-assisted picks by October 2025. The company launched Locus Array in April 2026, a fully autonomous fulfillment system combining mobile robotics, robotic picking arms, and AI-powered perception, with DHL Supply Chain as an early deployment customer. U.S. labor market dynamics, with warehouse worker turnover exceeding 100% annually in some regions, provide a structural tailwind for AMR investment.

China represents the second-largest national market at approximately USD 780 million in 2025, with a projected CAGR of 17.8%. Geekplus Technology (listed on HKEX as stock code 2590.HK) achieved net profitability in fiscal 2025 on revenue of approximately RMB 3.17 Billion, with non-mainland markets contributing over 75% of revenue at 46.6% gross margin. The company has delivered 72,000+ robots to 950 customers including over 80 Fortune Global 500 companies. Quicktron, also based in Wuxi, competes in the shelf-to-person and sorting robot segments. Chinese manufacturers benefit from domestic component supply chains that reduce production costs by 30 to 40% compared to European competitors.

Germany is Europe's largest AMR market, valued at approximately USD 310 million in 2025 with a CAGR of 14.5%. KUKA AG, headquartered in Augsburg and owned by China's Midea Group, held the leading 12.4% global market share in 2025. KUKA established a new software and AI organization in Silicon Valley in 2025, signaling its strategic pivot toward intelligence-driven robotics. Jungheinrich AG and the KION Group (parent of Dematic) are additional German-headquartered competitors. The Automatica trade show in Munich (June 2025) served as the launch venue for multiple AMR platforms, including ABB's Flexley P603.

Japan contributed approximately USD 240 million to the autonomous mobile robot market in 2025 with a CAGR of 13.9%. OMRON Corporation and Daifuku Co., Ltd. are the primary domestic players. Amazon's one-millionth robot was deployed at a Japanese fulfillment center, reflecting the country's high automation adoption rate. Japan ranks among the top three countries globally in robot density per 10,000 manufacturing employees. The country's aging demographic profile, with over 29% of the population aged 65+, creates structural labor replacement demand.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Component

- Hardware

- Sensors

- Cameras and Vision Systems

- LiDAR Systems

- Controllers and Processors

- Actuators and Motors

- Batteries and Power Systems

- Safety Components

- Communication Modules

- Software

- Navigation and Mapping Software

- Fleet Management Software

- Artificial Intelligence and Machine Learning Software

- Analytics and Monitoring Software

- Services

- Consulting Services

- Integration and Deployment Services

- Maintenance and Support Services

- Training Services

By Type

- Goods-to-Person Picking Robots

- Self-Driving Forklifts

- Autonomous Inventory Robots

- Autonomous Tugger Robots

- Unmanned Ground Vehicles (UGVs)

- Delivery and Transport Robots

- Inspection and Surveillance Robots

- Cleaning and Disinfection Robots

- Collaborative Mobile Robots (Co-bots)

- Automated Guided Carts (AGCs)

- Others

By End-Use

- Manufacturing

- Automotive

- Electronics and Semiconductor

- Aerospace and Defense

- Metals and Heavy Machinery

- Food and Beverage Manufacturing

- Pharmaceuticals Manufacturing

- Warehousing and Logistics

- Distribution Centers

- Third-Party Logistics (3PL)

- E-commerce Fulfillment Centers

- Healthcare

- Hospitals

- Laboratories

- Pharmacies

- Retail and E-commerce

- Hospitality

- Hotels

- Restaurants

- Agriculture

- Defense and Security

- Transportation and Airports

- Energy and Utilities

- Mining

- Education and Research

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.49 B |

| Forecast Revenue (2034) | USD 15.92 B |

| CAGR (2025-2034) | 15.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Hardware, Software, Services), By Type, (Goods-to-Person Picking Robots, Self-Driving Forklifts, Autonomous Inventory Robots, Autonomous Tugger Robots, Unmanned Ground Vehicles (UGVs), Delivery and Transport Robots, Inspection and Surveillance Robots, Cleaning and Disinfection Robots, Collaborative Mobile Robots (Co-bots), Automated Guided Carts (AGCs), Others), By End-Use, (Manufacturing, Warehousing and Logistics, Healthcare, Retail and E-commerce, Hospitality, Agriculture, Defense and Security, Transportation and Airports, Energy and Utilities, Mining, Education and Research, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | KUKA AG, GEEKPLUS TECHNOLOGY CO., LTD., ABB LTD., LOCUS ROBOTICS CORP., OMRON CORPORATION, MOBILE INDUSTRIAL ROBOTS (MIR) / TERADYNE INC., AMAZON ROBOTICS, BOSTON DYNAMICS (HYUNDAI), CLEARPATH ROBOTICS / OTTO MOTORS, GREYORANGE, JUNGHEINRICH AG, KION GROUP AG / DEMATIC, QUICKTRON INTELLIGENT TECHNOLOGY, SEEGRID CORPORATION, VECNA ROBOTICS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Robots Type (Goods-to-Person Picking, Self-Driving Forklifts, Autonomous Inventory, Autonomous Tugger, Unmanned Ground Vehicles, Delivery and Transport, Inspection and Surveillance, Cleaning and Disinfection, Collaborative Mobile, Automated Guided Carts), By End-Use, Industry Region, Market Dynamics, Competitive Landscape, Growth Opportunities, Strategic Insights, Emerging Trends and Forecast 2026-2034")

, By Robots Type (Goods-to-Person Picking, Self-Driving Forklifts, Autonomous Inventory, Autonomous Tugger, Unmanned Ground Vehicles, Delivery and Transport, Inspection and Surveillance, Cleaning and Disinfection, Collaborative Mobile, Automated Guided Carts), By End-Use, Industry Region, Market Dynamics, Competitive Landscape, Growth Opportunities, Strategic Insights, Emerging Trends and Forecast 2026-2034")

, By Robots Type (Goods-to-Person Picking, Self-Driving Forklifts, Autonomous Inventory, Autonomous Tugger, Unmanned Ground Vehicles, Delivery and Transport, Inspection and Surveillance, Cleaning and Disinfection, Collaborative Mobile, Automated Guided Carts), By End-Use, Industry Region, Market Dynamics, Competitive Landscape, Growth Opportunities, Strategic Insights, Emerging Trends and Forecast 2026-2034")

Frequently Asked Questions

How big is the Autonomous Mobile Robot Market?

The Global Autonomous Mobile Robot Market was valued at USD 3.90 Billion in 2024 and USD 4.49 Billion in 2025, and is projected to reach USD 15.92 Billion by 2034, growing at a CAGR of 15.1% from 2026 to 2034. Growth is driven by increasing warehouse automation, rising e-commerce demand, and advancements in AI-powered robotic technologies.

Who are the major players in the Autonomous Mobile Robot Market?

KUKA AG, GEEKPLUS TECHNOLOGY CO., LTD., ABB LTD., LOCUS ROBOTICS CORP., OMRON CORPORATION, MOBILE INDUSTRIAL ROBOTS (MIR) / TERADYNE INC., AMAZON ROBOTICS, BOSTON DYNAMICS (HYUNDAI), CLEARPATH ROBOTICS / OTTO MOTORS, GREYORANGE, JUNGHEINRICH AG, KION GROUP AG / DEMATIC, QUICKTRON INTELLIGENT TECHNOLOGY, SEEGRID CORPORATION, VECNA ROBOTICS, Others

Which segments covered the Autonomous Mobile Robot Market?

By Component, (Hardware, Software, Services), By Type, (Goods-to-Person Picking Robots, Self-Driving Forklifts, Autonomous Inventory Robots, Autonomous Tugger Robots, Unmanned Ground Vehicles (UGVs), Delivery and Transport Robots, Inspection and Surveillance Robots, Cleaning and Disinfection Robots, Collaborative Mobile Robots (Co-bots), Automated Guided Carts (AGCs), Others), By End-Use, (Manufacturing, Warehousing and Logistics, Healthcare, Retail and E-commerce, Hospitality, Agriculture, Defense and Security, Transportation and Airports, Energy and Utilities, Mining, Education and Research, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Autonomous Mobile Robot Market

Published Date : 11 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date