- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Autonomous Shipping Market Size, Share & Forecast | CAGR 10.6%

Global Autonomous Shipping Market Size, Share, Analysis By Autonomy Level (Partially Autonomous, Remotely Controlled with Crew, Unmanned Remote, Fully Autonomous Degree 4), By Vessel Type (Commercial Cargo, Container Ships, Bulk Carriers, Defense & Naval, Passenger Ferries), By Component (Sensors, LiDAR, Radar, Navigation Software, Cybersecurity), By End-User (Fleet Operators, Navies, Port Authorities) Region & Key Players-Segment Overview, Dynamics, Trends & Forecast 2026-2035

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 6.85 Billion | USD 16.95 Billion | 10.6% | Asia Pacific, 38.4% |

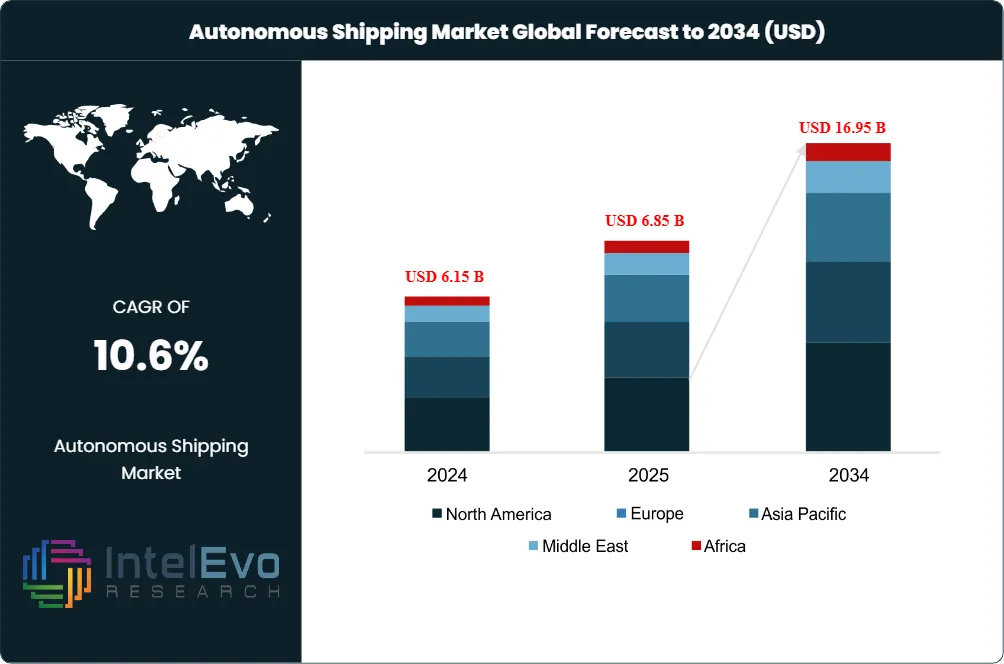

The Autonomous Shipping Market was valued at USD 6.15 Billion in 2024 and USD 6.85 Billion in 2025. The market is projected to reach USD 16.95 Billion by 2034, expanding at a CAGR of 10.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 10.10 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportThe autonomous shipping market spans Maritime Autonomous Surface Ships (MASS) hardware (sensors, radar, LiDAR, GNSS receivers, propulsion control), software (collision avoidance, route optimization, AI navigation), shore-based remote operations centers, and full-stack autonomous vessels across commercial and defense use cases. Adoption pressure stems from rising crew costs, IMO emissions regulations, geopolitical demand for unmanned naval surveillance, and rapid AI and sensor fusion improvements. The IMO Maritime Safety Committee MSC 109 in December 2024 agreed to a revised Road Map for the MASS Code, with finalization and adoption of the non-mandatory Code targeted for May 2026 at MSC 111. A three-year Experience-Building Phase between 2026 and 2028 will inform the mandatory MASS Code, targeted for adoption by July 2030 and entry into force on January 1, 2032 under amendments to the Safety of Life at Sea (SOLAS) Convention.

Defense demand has accelerated faster than commercial adoption. The U.S. Navy aims to make half of the surface fleet unmanned, with the Modular Attack Surface Craft (MASC) program anchoring procurement. Saronic Technologies (Austin, Texas) closed a USD 392 Million Navy production contract on December 9, 2025 for the 24-foot Corsair unmanned surface vessel costing under USD 1 Million per unit. Anduril Industries announced its Seattle ship canal facility in November 2025 as the U.S. hub for vessel assembly under MASC. The Defense Advanced Research Projects Agency (DARPA) demonstrated the USX-1 Defiant prototype unmanned surface vessel in March 2025. Commercial deployments include Kongsberg Gruppen's Yara Birkeland fully autonomous electric container ship operating in Norway and Avikus (HD Hyundai) demonstrated transoceanic autonomous LNG carrier voyage.

Regulatory frameworks are progressing across multiple bodies. DNV launched its AROS (Autonomous and Remotely Operated Ships) framework in January 2025 as the first dedicated classification framework. Lloyd's Register announced an open-source MASS systems engineering project on March 12, 2026 supporting safe deployment. ABS commentary in February 2026 emphasized the autonomy spectrum from supervised to fully autonomous operations. National frameworks include the U.S. Coast Guard, Norway's Maritime Authority (NMA), Singapore's Maritime and Port Authority (MPA), Korea Register, and ClassNK Japan. Regionally, Asia Pacific held 38.4% revenue share in the autonomous shipping market in 2025, anchored by South Korean, Chinese, and Japanese shipyards. North America captured 27.8% with concentrated U.S. defense spending, while Europe held 24.6% led by Norway's Yara Birkeland and Finland's Wartsila Smart Marine programs.

Market Definition and Scope

The autonomous shipping market is defined as the segment of the maritime technology and shipping industry covering vessels operating with degrees of automation classified by the IMO from Degree One (human-assisted automation) through Degree Four (fully autonomous), plus shore-based remote operations centers, autonomous navigation software, sensor fusion hardware, AI-driven collision avoidance systems, and supporting connectivity infrastructure including 5G and Low Earth Orbit (LEO) satellite links. The market encompasses commercial cargo carriers, container ships, tankers, fishing vessels, ferries, harbor tugs, offshore service vessels, defense unmanned surface vessels (USVs), and unmanned underwater vehicles (UUVs).

This analysis covers hardware (radar, LiDAR, GNSS, cameras, thermal imaging, sonar, propulsion control), software (collision avoidance per IMO COLREGs, route optimization, predictive maintenance, fleet management), and services (remote operations, retrofit integration, classification certification). Vessel categories include cargo ships, tankers, defense vessels, fishing and research vessels, and harbor and inland waterway craft. Excluded from this scope are conventional ships without autonomy capability, traditional shipbuilding revenue not tied to autonomy retrofits, and underwater oil and gas remotely operated vehicles (ROVs) not classified as MASS. The parent global maritime technology and shipbuilding market reached approximately USD 195 Billion in 2025; autonomous shipping represented approximately 3.5% of that parent.

, By Vessel Type (Commercial Cargo, Container Ships, Bulk Carriers, Defense & Naval, Passenger Ferries), By Component (Sensors, LiDAR, Radar, Navigation Software, Cybersecurity), By End-User (Fleet Operators, Navies, Port Authorities) Region & Key Players-Segment Overview, Dynamics, Trends & Forecast 2026-2035")

Key Takeaways

- Market Growth: The autonomous shipping market expanded from USD 6.85 Billion in 2025 toward a projected USD 16.95 Billion by 2034, registering a CAGR of 10.6% during the forecast period.

- Segment Dominance by Autonomy Level: Partially autonomous vessels (Degrees One and Two) held 74.35% market share in 2024, while fully autonomous vessels (Degrees Three and Four) are projected to register the fastest 19.58% CAGR through 2030.

- Segment Dominance by Vessel Type: Cargo vessels led with 41.12% revenue share in 2024 due to global container and bulk shipping volume; defense vessels are projected to grow at 17.80% CAGR, the highest across vessel categories.

- Driver: The U.S. Navy December 9, 2025 USD 392 Million Saronic Corsair production contract validated venture-backed autonomous vessel procurement, with the Navy targeting half the surface fleet unmanned and Saronic moving from prototype to production in under 12 months.

- Restraint: Fragmented flag-state rules and cybersecurity frameworks delay large-scale international commercial deployment; the IMO non-mandatory MASS Code is scheduled for May 2026 adoption at MSC 111, with mandatory adoption no earlier than January 1, 2032.

- Opportunity: Defense unmanned surface vessel demand drove Saronic Technologies to a USD 9.25 Billion valuation on March 31, 2026 following a USD 1.75 Billion Series E led by Kleiner Perkins, with Sacra estimating Saronic 2025 revenue at USD 400 Million.

- Trend: AI-driven navigation adoption rose by approximately 56% in 2025, while battery-powered autonomous vessels grew 31% supported by short-sea route economics including Norway's Yara Birkeland fully electric container ship.

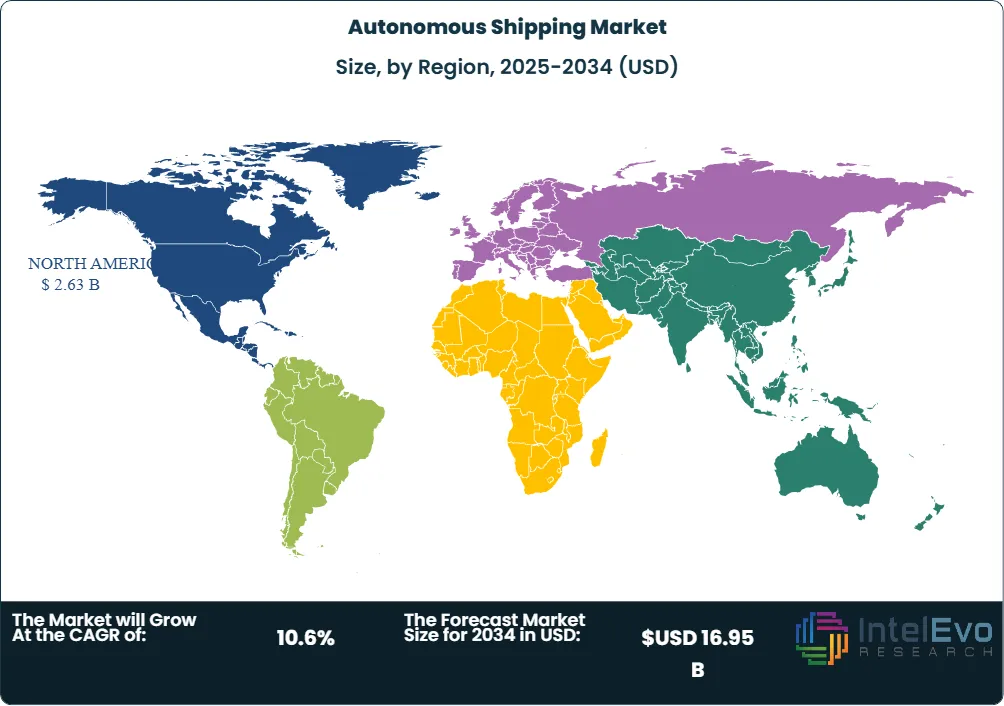

- Regional: Asia Pacific held the largest regional share at 38.4%, equating to approximately USD 2.63 Billion in 2025, with South Korea, China, and Japan combining shipbuilding capacity and government-backed autonomous trials.

Key Insights Summary

- Saronic Technologies disclosed a USD 1.75 Billion Series E round on March 31, 2026 with Kleiner Perkins as lead investor; the financing more than doubled the Austin, Texas autonomous vessel builder's valuation to USD 9.25 Billion from USD 4 Billion in early 2025, with planned ramp to over 20 vessels annually by 2027 across the company's Franklin, Louisiana yard and a proposed Port Alpha site.

- At MSC 109 in December 2024 the IMO Maritime Safety Committee updated the MASS Code Road Map, scheduling non-mandatory adoption at MSC 111 in May 2026, an Experience-Building Phase running 2026 to 2028, mandatory adoption by July 2030, and a SOLAS-aligned entry into force on January 1, 2032.

- The U.S. Navy granted Saronic a USD 392 Million production award on December 9, 2025 for the 24-foot Corsair unmanned surface vessel; the platform costs under USD 1 Million per unit, transports 1,000-pound payloads, ranges up to 1,000 nautical miles, and operates under the Echelon command-and-control stack.

- In November 2025 Anduril Industries identified its Seattle ship canal site as the U.S. base for assembling, integrating, and testing Autonomous Surface Vessels under the Navy's Modular Attack Surface Craft (MASC) program, framing the choice around the regional legacy of Kaiser Shipyards.

- Lloyd's Register kicked off an open-source MASS systems engineering framework initiative on March 12, 2026 spanning design, architecture analysis, modeling, simulations, software engineering, ML DevOps, integration, and sustainment activities to support safe rollout of autonomous shipping technologies.

- DNV unveiled its Autonomous and Remotely Operated Ships (AROS) classification family in January 2025 as the maritime sector's first dedicated framework, establishing a basis for demonstrating that auto-remote vessels can match or exceed the safety profile of conventional ships under SOLAS principles.

Competitive Landscape Overview

The autonomous shipping market is moderately consolidated at the established maritime technology tier and increasingly competitive at the venture-backed defense tier. Established leaders, including Kongsberg Gruppen ASA, Wartsila Corporation, ABB Ltd., and Rolls-Royce plc, anchor commercial integration with installed base on existing vessel fleets. Defense-focused challengers, including Saronic Technologies, Anduril Industries, Saildrone, and Blue Water Autonomy, scale rapidly under U.S. Department of Defense procurement reforms. Competition is technology-led rather than price-led, with three competing architectures: integrated maritime OEM solutions (Kongsberg, Wartsila, ABB), fixed-price defense autonomous platforms (Saronic, Anduril), and software-first autonomy retrofits (Sea Machines Robotics, Orca AI, Avikus). The competitive frontier is shifting from sensor and software pilots toward production-scale shipyard operations, exemplified by Saronic's USD 300 Million Franklin Louisiana shipyard expansion. New entrants include Saronic Technologies (Austin, founded 2022), Blue Water Autonomy (Boston, USD 14 Million seed April 2025), Mythos AI (autonomous boat pilot), Bedrock Ocean Exploration, and HavocAI. South Korean Avikus (HD Hyundai), Chinese Bright Laser Technologies, and Japanese national champions extend the regional competitive set.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product / Solution | Geographic Strength | Recent Strategic Move |

| Kongsberg Gruppen ASA | Kongsberg, Norway | Leader | K-Bridge, Maritime Broadband Radio, Yara Birkeland integration | Europe, Asia, Global | Approval in Principle from DNV for shore-based control center role transfer (June 2024) |

| Wartsila Corporation | Helsinki, Finland | Leader | SmartMove Suite, Voyage navigation, autonomous dock-to-dock | Europe, Asia, Global | IntelliTug Singapore deployment with PSA Marine and MPA |

| ABB Ltd. (ABB Marine) | Zurich, Switzerland | Leader | ABB Ability Marine Pilot, Azipod propulsion integration | Europe, North America, Asia | B Zero V autonomous ferry trial expansion in Helsinki harbor |

| Rolls-Royce plc (Marine) | London, United Kingdom | Leader | Intelligent Awareness; Autonomous Naval Vessel concept | Europe, North America | Single-role naval vessel concept with 100-day endurance and 3,500 nm range |

| HD Hyundai Heavy Industries (Avikus) | Ulsan, South Korea | Challenger | Avikus NeuBoat Navi autonomous navigation system | Asia, North America | World-first autonomous transoceanic LNG carrier voyage demonstration |

| Saronic Technologies | Austin, Texas, USA | Challenger | Spyglass, Corsair, Marauder unmanned surface vessels; Echelon software | North America | USD 1.75 Billion Series E funding led by Kleiner Perkins on March 31, 2026 |

| Anduril Industries | Costa Mesa, California, USA | Challenger | Dive-LD; Autonomous Surface Vessels for MASC program | North America | Seattle ship canal facility for U.S. Navy MASC program announced November 2025 |

| Saildrone, Inc. | Alameda, California, USA | Niche Player | Saildrone Voyager, Surveyor, Explorer USVs | North America, Global | USD 43 Million 2024 revenue with 231% year-over-year growth |

| Sea Machines Robotics | Boston, Massachusetts, USA | Niche Player | SM300 perception and autonomy system; AI-Lookout | North America, Europe | Commercial vessel retrofit deployments across tugs, ferries, and patrol craft |

| BAE Systems plc | London, United Kingdom | Niche Player | Pacific 24 USV; Herne extra-large autonomous underwater vehicle | Europe, North America | Herne XLAUV ready for deployment by mid-2026 per November 2024 announcement |

By Autonomy Level

The autonomous shipping market by autonomy level is led by partially autonomous vessels (IMO Degrees One and Two), which captured 74.35% share in 2024. Degree One covers ships with automated processes and decision support where seafarers remain ready to take control; Degree Two covers remotely controlled ships with seafarers on board. The segment anchors revenue because retrofit economics support adoption across existing global commercial fleets exceeding 100,000 vessels. Fully autonomous vessels (Degrees Three remotely controlled without seafarers and Degree Four fully autonomous) are projected to grow at the fastest CAGR of 19.58% through 2030, supported by the IMO non-mandatory MASS Code finalization at MSC 111 in May 2026 and increasing defense demand. Remotely operated vessels are projected to grow at 5.6% CAGR through 2034 anchored by short-sea routes and harbor operations. Comparison: defense fully autonomous unmanned surface vessel revenue commanded a 4.2x revenue per unit premium over commercial Degree Two retrofits in 2025 driven by mission-specific payload integration and ruggedization requirements.

By Vessel Type

The autonomous shipping market by vessel type is led by cargo vessels at 41.12% share in 2024, anchored by container ships, dry bulk carriers, and project cargo vessels operating across major global trade routes. Tankers represented 18.4% share, with tanker autonomy adoption supported by Maersk Tankers, Mitsui OSK Lines, and Hyundai Merchant Marine fleet retrofit pilots. Defense vessels held 22.7% share in 2024 and are projected to grow at the fastest CAGR of 17.80% through 2030, anchored by the U.S. Navy MASC program, NATO standardization, and rising naval modernization budgets across South Korea, Japan, the United Kingdom, France, Australia, and India.

Ferries and passenger vessels captured 7.4% share, led by Finnish, Norwegian, and Japanese harbor ferry deployments. Fishing vessels held 4.8% share with adoption concentrated on Japanese long-line tuna fleets and Korean autonomous purse seiner trials. Tugs and harbor service vessels represented 3.6% share supported by IntelliTug deployments in Singapore. Research and survey vessels including Saildrone Voyager and Surveyor classes captured 1.6% share, with Saildrone reporting USD 43 Million 2024 revenue with 231% year-over-year growth. Procurement leads at commercial fleet operators should evaluate autonomy retrofit packages against three criteria: classification society approval pathway, IMO COLREGs compliance for collision avoidance, and IACS Unified Requirement E26/E27 cybersecurity baseline.

By Component

The autonomous shipping market by component is led by hardware at 62.78% revenue in 2024, encompassing radar, LiDAR, electro-optical and infrared cameras, GNSS receivers, automatic identification system (AIS) transponders, propulsion control units, and edge computing nodes. Teledyne Technologies, Furuno, Raytheon Anschutz, and Velodyne Lidar anchor the sensor segment. Software is forecast to accelerate at 15.45% CAGR to 2030, with collision avoidance, route optimization, predictive maintenance, and fleet management platforms anchoring growth. Saronic's Echelon command-and-control platform, ABB Ability Marine Pilot, Kongsberg's K-Bridge, and Sea Machines Robotics SM300 occupy core software competitive positions. Services including remote operations, retrofit integration, classification certification, and cybersecurity assurance grew at 14.2% CAGR.

By End-User

The autonomous shipping market by end-user is led by commercial operators at 70.50% expenditure share in 2024, including container lines (Maersk, MSC, CMA CGM, Hapag-Lloyd, ONE), dry bulk carriers, tanker operators, and offshore service vessel operators. Government and military customers held 29.5% share but are projected to grow at 15.74% CAGR through 2030, the fastest end-user growth, driven by U.S. Navy procurement reform, the European Defence Fund, AUKUS naval cooperation, and Asia Pacific naval modernization. Port authorities and smart port operators anchor downstream demand for autonomous tug and pilot operations under the Maritime and Port Authority of Singapore (MPA), Port of Rotterdam, Port of Antwerp-Bruges, and Port of Los Angeles initiatives. ROI calculation for autonomous shipping deployment must account for sensor and software CAPEX (USD 350,000 to USD 2.5 Million per vessel for retrofit), classification society approval timelines (12 to 36 months for novel concepts under IMO MSC.1/Circular.1455), cybersecurity certification under IACS UR E26/E27, and crew restructuring costs.

Regional Analysis

The autonomous shipping market by region is led by Asia Pacific at 38.4% revenue share in 2025, equating to approximately USD 2.63 Billion. South Korea anchors regional leadership through HD Hyundai Heavy Industries (Avikus subsidiary, Ulsan), Samsung Heavy Industries, and Hanwha Ocean. The South Korean Ministry of Oceans and Fisheries funds intelligent navigation systems, supporting Avikus NeuBoat Navi commercial deployments and the world-first transoceanic autonomous LNG carrier voyage. China advances under Made in China 2025 with autonomous research vessels, Pearl River and Yangtze inland trials, and naval USV programs by China State Shipbuilding Corporation (CSSC). Japan supports semi-autonomous commercial shipping under Mitsui OSK Lines and Nippon Yusen Kabushiki Kaisha (NYK) MEGURI 2040 initiative, with regulatory caution from the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) limiting fully autonomous deployments. Singapore's MPA hosts IntelliTug and other autonomous harbor pilots.

North America captured 27.8% share in 2025, equivalent to approximately USD 1.90 Billion. The United States dominates through U.S. Navy procurement and venture-backed defense tech, with Saronic Technologies (Austin), Anduril Industries (Costa Mesa with Seattle MASC facility), Saildrone (Alameda), Sea Machines Robotics (Boston), and Blue Water Autonomy. The Defense Innovation Unit, Office of Naval Research, and Defense Advanced Research Projects Agency support program development including the March 2025 USX-1 Defiant prototype. The U.S. Coast Guard regulates domestic autonomous operations under 33 CFR Part 164 and Title 46 USC. Canada hosts Tekna Holding ASA (Sherbrooke) on supporting sensor technology.

Europe held 24.6% share in 2025, valued at approximately USD 1.69 Billion. Norway anchors the region through Kongsberg Gruppen ASA and the Yara Birkeland fully autonomous electric container ship operating between Yara facilities. The Norwegian Maritime Authority (NMA) provides supportive trial regulation. Finland hosts Wartsila Corporation (Helsinki) and the One Sea ecosystem founding partnership. Sweden contributes through Saab AB Autonomous Ocean Core (April 2025) and ABB Marine integration. The United Kingdom anchors classification leadership through Lloyd's Register and BAE Systems plc with the Herne XLAUV. Germany hosts OFFIS automated collision warning research, Switzerland hosts ABB Ltd. headquarters, and the European Maritime Safety Agency (EMSA) coordinates EU-level MASS Code development input.

Middle East and Africa held 5.4% share in 2025, approximately USD 370 Million, projected at the fastest regional CAGR of 14.01% through 2030. Liberal test corridors and smart-port investment in the United Arab Emirates and Saudi Arabia attract foreign autonomous shipping pilots. Israel contributes through Elbit Systems naval USV programs.

Latin America contributed 3.8% share, valued at approximately USD 260 Million in 2025. Brazil and Chile lead regional pilots through PETROBRAS offshore vessel autonomy trials and Chilean Navy USV procurement. Argentine and Mexican naval autonomous trials remain limited.

Country Analysis

United States

The autonomous shipping market in the United States was valued at approximately USD 1.65 Billion in 2025 and is projected to grow at a CAGR of 13.4% during 2025-2034, the fastest among major country markets. The U.S. Navy's MASC program drives demand, with Saronic Technologies' USD 392 Million December 9, 2025 Corsair production contract and Anduril Industries' Seattle ship canal facility announcement in November 2025 anchoring procurement. Defense Innovation Unit, Office of Naval Research, and DARPA support program development including the March 2025 USX-1 Defiant. The Maritime Administration (MARAD), U.S. Coast Guard, and Department of Defense's Defense Industrial Base Resilience initiatives back domestic shipbuilding capacity. Saronic's potential USD 3.2 Billion Brownsville Port Alpha shipyard project would create up to 10,000 jobs through 2034.

Norway

Norway's autonomous shipping market reached approximately USD 280 Million in 2025 with a country CAGR of 11.8% during 2025-2034. Kongsberg Gruppen ASA (Kongsberg) anchors domestic activity with the Yara Birkeland fully autonomous electric container ship demonstrating commercial operations. Massterly, the Kongsberg-Wilhelmsen joint venture, operates the world's first autonomous shipping management company. The Norwegian Maritime Authority (NMA) regulates trials under supportive frameworks supporting MASS Code development input. DNV (formerly DNV GL) anchors classification leadership with the AROS family launched January 2025. Norway's Trondheimsfjord and Horten test areas host ongoing autonomous trials.

South Korea

South Korea's autonomous shipping market reached approximately USD 740 Million in 2025 with a country CAGR of 11.2% during 2025-2034. HD Hyundai Heavy Industries (Ulsan) and its Avikus subsidiary lead Korean autonomous shipping innovation, with Avikus completing a world-first transoceanic autonomous LNG carrier voyage. Samsung Heavy Industries' MoU with DNV signed October 2023 supports continuing collaboration. The Ministry of Oceans and Fisheries funds smart manufacturing subsidies for autonomous and intelligent navigation. Korea Register (KR) provides classification services aligned with IMO MASS Code development. Hanwha Ocean and POSCO Holdings contribute through marine engineering and steel supply for autonomous vessel construction.

Singapore

Singapore's autonomous shipping market reached approximately USD 145 Million in 2025 with a country CAGR of 12.6% during 2025-2034. The Maritime and Port Authority of Singapore (MPA) anchors innovation through the Maritime Innovation and Technology (MINT) Fund supporting projects including IntelliTug between Wartsila, PSA Marine, Lloyd's Register, and the Technology Centre for Offshore and Marine Singapore (TCOMS). Singapore's port handles approximately 37 million TEU annually, providing scale for autonomous tug and harbor pilot deployments. The MPA's Singapore-Rotterdam Green and Digital Shipping Corridor extends autonomous operations into international transit. The Ministry of Trade and Industry supports SmartPort 2030 initiative with port automation investment.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Autonomy Level

- Remotely Operated Ships

- Partially Autonomous Ships

- Highly Autonomous Ships

- Fully Autonomous Ships

- Others

By Vessel Type

- Cargo Ships

- Container Ships

- Bulk Carriers

- Tankers

- Passenger Ships and Ferries

- Naval and Defense Vessels

- Offshore Support Vessels

- Fishing Vessels

- Research and Survey Vessels

- Others

By Component

- Hardware

- Software

- Others

By End-User

- Commercial Shipping Companies

- Naval and Defense Organizations

- Port Authorities

- Offshore Oil and Gas Companies

- Government Maritime Agencies

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 6.85 B |

| Forecast Revenue (2034) | USD 16.95 B |

| CAGR (2025-2034) | 10.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Autonomy Level, (Remotely Operated Ships, Partially Autonomous Ships, Highly Autonomous Ships, Fully Autonomous Ships, Others), By Vessel Type, (Cargo Ships, Container Ships, Bulk Carriers, Tankers, Passenger Ships and Ferries, Naval and Defense Vessels, Offshore Support Vessels, Fishing Vessels, Research and Survey Vessels, Others), By Component, (Hardware, Software, Others), By End-User, (Commercial Shipping Companies, Naval and Defense Organizations, Port Authorities, Offshore Oil and Gas Companies, Government Maritime Agencies, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | KONGSBERG GRUPPEN ASA, WARTSILA CORPORATION, ABB LTD. (ABB MARINE), ROLLS-ROYCE PLC (MARINE), HD HYUNDAI HEAVY INDUSTRIES (AVIKUS), SARONIC TECHNOLOGIES, ANDURIL INDUSTRIES, SAILDRONE, INC., SEA MACHINES ROBOTICS, INC., BAE SYSTEMS PLC, L3HARRIS TECHNOLOGIES INC., NORTHROP GRUMMAN CORPORATION, SAMSUNG HEAVY INDUSTRIES CO. LTD., MITSUI O.S.K. LINES, MARINE TECHNOLOGIES LLC, ULSTEIN GROUP ASA, HONEYWELL INTERNATIONAL INC., SAAB AB, DNV AS, VALMET OYJ, BLUE WATER AUTONOMY, INC., BUFFALO AUTOMATION, ORCA AI, MASSTERLY (KONGSBERG-WILHELMSEN), TELEDYNE TECHNOLOGIES, SIEMENS AG, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Vessel Type (Commercial Cargo, Container Ships, Bulk Carriers, Defense & Naval, Passenger Ferries), By Component (Sensors, LiDAR, Radar, Navigation Software, Cybersecurity), By End-User (Fleet Operators, Navies, Port Authorities) Region & Key Players-Segment Overview, Dynamics, Trends & Forecast 2026-2035")

, By Vessel Type (Commercial Cargo, Container Ships, Bulk Carriers, Defense & Naval, Passenger Ferries), By Component (Sensors, LiDAR, Radar, Navigation Software, Cybersecurity), By End-User (Fleet Operators, Navies, Port Authorities) Region & Key Players-Segment Overview, Dynamics, Trends & Forecast 2026-2035")

, By Vessel Type (Commercial Cargo, Container Ships, Bulk Carriers, Defense & Naval, Passenger Ferries), By Component (Sensors, LiDAR, Radar, Navigation Software, Cybersecurity), By End-User (Fleet Operators, Navies, Port Authorities) Region & Key Players-Segment Overview, Dynamics, Trends & Forecast 2026-2035")

Frequently Asked Questions

How big is the Autonomous Shipping Market?

The Global Autonomous Shipping Market was valued at USD 6.15 Billion in 2024 and USD 6.85 Billion in 2025, and is projected to reach USD 16.95 Billion by 2034, growing at a CAGR of 10.6% from 2026 to 2034. Market growth is driven by AI-powered navigation, autonomous vessels, smart maritime technologies, and digital fleet management.

Who are the major players in the Autonomous Shipping Market?

KONGSBERG GRUPPEN ASA, WARTSILA CORPORATION, ABB LTD. (ABB MARINE), ROLLS-ROYCE PLC (MARINE), HD HYUNDAI HEAVY INDUSTRIES (AVIKUS), SARONIC TECHNOLOGIES, ANDURIL INDUSTRIES, SAILDRONE, INC., SEA MACHINES ROBOTICS, INC., BAE SYSTEMS PLC, L3HARRIS TECHNOLOGIES INC., NORTHROP GRUMMAN CORPORATION, SAMSUNG HEAVY INDUSTRIES CO. LTD., MITSUI O.S.K. LINES, MARINE TECHNOLOGIES LLC, ULSTEIN GROUP ASA, HONEYWELL INTERNATIONAL INC., SAAB AB, DNV AS, VALMET OYJ, BLUE WATER AUTONOMY, INC., BUFFALO AUTOMATION, ORCA AI, MASSTERLY (KONGSBERG-WILHELMSEN), TELEDYNE TECHNOLOGIES, SIEMENS AG, Others

Which segments covered the Autonomous Shipping Market?

By Autonomy Level, (Remotely Operated Ships, Partially Autonomous Ships, Highly Autonomous Ships, Fully Autonomous Ships, Others), By Vessel Type, (Cargo Ships, Container Ships, Bulk Carriers, Tankers, Passenger Ships and Ferries, Naval and Defense Vessels, Offshore Support Vessels, Fishing Vessels, Research and Survey Vessels, Others), By Component, (Hardware, Software, Others), By End-User, (Commercial Shipping Companies, Naval and Defense Organizations, Port Authorities, Offshore Oil and Gas Companies, Government Maritime Agencies, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date