- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Autopilot Deployment Tools Market Size, Share & CAGR 12.4% 2034

Global Autopilot Deployment Tools Market Size, Share, Analysis By Component (Software, Hardware, Services), By Deployment Mode (Cloud, On-Premises, Hybrid), By Application (Automotive, Aerospace, Maritime, Drones & UAVs, Industrial Automation, Others), By End-User (Commercial, Defense, Others) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Artificial Intelligence Integration, Edge Computing Trends & Forecast 2026–2034

Report Overview

The Autopilot Deployment Tools Market was valued at USD 4.0 B in 2024 and is projected to reach approximately USD 4.5 B in 2025. The market is further expected to expand to nearly USD 12.9 B by 2034, registering a compound annual growth rate (CAGR) of about 12.4% during the forecast period from 2026 to 2034. Growth in the market is driven by the increasing adoption of automated device provisioning, cloud-based IT management platforms, and zero-touch deployment solutions across enterprise environments. Autopilot deployment tools enable organizations to streamline device configuration, reduce manual IT workload, and improve operational efficiency in remote and hybrid work models.

Get More Information about this report -

Request Free Sample ReportAdditionally, the rapid expansion of digital transformation initiatives, endpoint management solutions, and enterprise mobility management (EMM) platforms is expected to accelerate demand for autopilot deployment tools, particularly among large enterprises and managed service providers.

The market covers software and orchestration layers that deploy, test, monitor, and update automated control stacks across road vehicles and aircraft. Buyers use these platforms to shorten release cycles, harden safety cases, and maintain traceability across model versions, sensor configurations, and operational design domains.

Demand rises as OEMs and airlines push automation to reduce incident rates, fuel burn, and downtime. Utilization signals support this shift. About 70% of drivers activate an ADAS feature most or all of the time, which expands the installed base that must be calibrated and updated at scale. In aviation, autopilot accounts for roughly 90% of flight time, which increases reliance on repeatable validation, configuration control, and post-deployment monitoring. On the supply side, the vendor set spans automotive middleware specialists, avionics and simulation providers, and hyperscale cloud players. Subscription pricing and usage-based testing in the cloud lift recurring revenue share to an estimated 55% by 2034, up from roughly 35% in 2024, as fleets demand continuous delivery and remote compliance reporting.

Regulation shapes procurement and product design. Automotive programs align with functional safety and cybersecurity requirements, while aviation deployments face stringent certification and software assurance expectations. These constraints raise switching costs and favor vendors that embed audit trails, requirements coverage, and safety evidence automation. Public funding and smart-mobility programs also influence timing, especially where road infrastructure digitization accelerates connected testing and over-the-air rollouts.

Technology change remains the main multiplier. AI-assisted scenario generation, synthetic data, and automated regression testing increase coverage per engineering hour and reduce validation backlogs. At the same time, the market carries material risks. Liability exposure, adversarial attacks, data sovereignty limits, and certification delays can slow deployments and force rework. Regional dynamics remain balanced. North America holds an estimated 35% of 2024 revenue due to early autonomy programs, Europe accounts for about 28% driven by safety-led regulation, and Asia-Pacific approaches 30% on manufacturing scale and rapid pilot activity. Investment hotspots include China, India, the UAE, and Singapore, where fleet digitization and test corridors expand tool adoption.

, By Deployment Mode (Cloud, On-Premises, Hybrid), By Application (Automotive, Aerospace, Maritime, Drones & UAVs, Industrial Automation, Others), By End-User (Commercial, Defense, Others) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Artificial Intelligence Integration, Edge Computing Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: Market revenue rises from 4.5 B USD, 2025 to 14.4 B USD, 2035 at a 12.4% CAGR, 2026–2035. Market size reaches estimated: 4.0 B USD, 2024 and estimated: 12.9 B USD, 2034 to align to 2024-2034.

- Segment Dominance: Software leads by component at 53.9%, 2025, reflecting the highest monetization in orchestration, testing, and lifecycle management layers. Software revenue equals estimated: 2.4 B USD, 2025 based on 4.5 B USD, 2025 total.

- Segment Dominance: Cloud leads by deployment mode at 43.6%, 2025, driven by scalable validation, remote monitoring, and continuous updates. Cloud revenue equals estimated: 2.0 B USD, 2025 based on 4.5 B USD, 2025 total.

- Driver: Commercial operators scale automation to reduce incidents and operating cost, sustaining 59.7%, 2025 end-user share. Commercial spend equals estimated: 2.7 B USD, 2025 based on 4.5 B USD, 2025 total.

- Restraint: Certification, safety assurance, and cybersecurity requirements increase time-to-deploy and raise compliance cost to estimated: 8.0% of project budget, 2025. Regulatory friction delays rollouts by estimated: 6.0 months, 2025 in tightly governed aviation and automotive programs.

- Opportunity: Automotive remains the largest application at 38.0%, 2025 and expands tool demand across ADAS-to-autonomy deployment pipelines. Automotive revenue equals estimated: 1.7 B USD, 2025 based on 4.5 B USD, 2025 total.

- Trend: Vendors embed AI-driven scenario generation and automated regression to raise test coverage and release velocity, supporting estimated: 55.0% recurring revenue mix, 2034. Toolchains shift toward continuous delivery with estimated: 30.0% faster validation cycles, 2025.

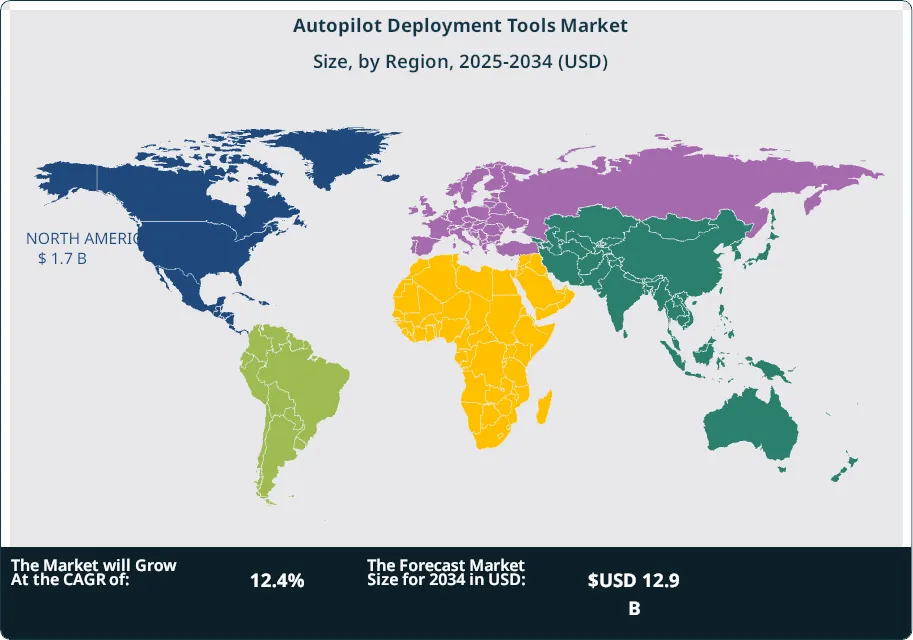

- Regional Analysis: North America leads with 37.8% share valued at 1.7 B USD, 2025, anchored by early autonomy programs and mature cloud infrastructure. North America reaches estimated: 4.9 B USD, 2034 if the 37.8% share holds against 12.9 B USD, 2034 global.

By Component

Software remains the central revenue contributor within the autopilot deployment tools market as of 2025, accounting for approximately 53.9% of total market value. Software platforms manage perception models, control logic, simulation environments, and lifecycle updates required for autonomous systems. Their importance continues to rise as vehicle platforms rely on continuous software validation, over-the-air updates, and real-time monitoring to meet safety and compliance requirements across automotive, aerospace, and industrial domains.

Hardware forms the physical foundation of autopilot systems through sensors, compute modules, actuators, and communication units. LiDAR, radar, high-resolution cameras, and embedded processors enable real-time environment sensing and execution of autonomous commands. Ongoing advances in sensor accuracy and processor efficiency support higher autonomy levels while reducing system latency and energy consumption, particularly in automotive and unmanned aerial platforms.

Services represent a growing support layer that includes system integration, testing, certification support, training, and post-deployment maintenance. As regulatory scrutiny intensifies, enterprises increasingly depend on specialized service providers to ensure compliance and system reliability. Service revenues continue to expand as organizations seek long-term operational assurance rather than one-time deployment support.

By Deployment Mode

Cloud-based deployment leads the market with an estimated 43.6% share in 2025, driven by centralized data processing, remote access, and elastic compute capacity. Cloud environments enable large-scale simulation, fleet-wide software updates, and continuous performance tracking. These capabilities are essential as autonomous systems generate high volumes of sensor data that require frequent analysis and validation.

On-premises deployment maintains relevance among users with strict data governance, national security constraints, or ultra-low latency requirements. Aerospace and defense operators favor local infrastructure to retain full operational control and avoid reliance on external networks. This model supports predictable performance in mission-critical scenarios.

Hybrid deployment continues to gain traction as organizations balance security with flexibility. Sensitive datasets remain on local servers, while computationally intensive analytics and model training move to the cloud. This approach reduces infrastructure risk while supporting phased adoption of automation technologies.

By Application

Automotive represents the largest application segment with a 38.0% share in 2025, supported by widespread ADAS deployment and increasing autonomy features in passenger and commercial vehicles. Automakers invest heavily in deployment tools to manage frequent software releases, validate safety functions, and support regional compliance.

Aerospace applications rely on autopilot deployment tools to manage flight control systems, navigation accuracy, and redundancy validation. Autopilot systems operate during nearly 90% of flight time, reinforcing demand for dependable deployment and monitoring frameworks.

Maritime, drones and UAVs, and industrial automation collectively show strong expansion. Autonomous vessels improve route efficiency, UAVs support logistics and surveillance, and autonomous robots enhance warehouse and factory operations. These segments increasingly adopt standardized deployment tools to manage diverse operating environments.

By End-User

Commercial users dominate with a 59.7% share in 2025, reflecting adoption across logistics, mobility services, manufacturing, and agriculture. These users prioritize deployment efficiency, uptime, and cost control to support large autonomous fleets.

Defense users adopt autopilot systems for unmanned platforms and tactical vehicles, emphasizing system reliability, encryption, and operational resilience. Deployment tools in this segment focus on controlled environments and mission readiness.

Other users include government agencies and research institutions applying autonomous systems in emergency response and environmental monitoring, where reliability and accountability remain critical.

By Region

North America leads the market with a 37.8% share, valued at approximately USD 1.7 B in 2025. The United States anchors demand through strong automotive, aerospace, and defense investment, supported by mature cloud infrastructure and early autonomy programs.

Europe follows with steady adoption driven by strict safety standards and public mobility programs in Germany, France, and the United Kingdom. Compliance-focused deployment tools remain a key purchasing criterion.

Asia Pacific shows the fastest growth trajectory, supported by automotive manufacturing scale, smart city investments, and public funding in China, Japan, South Korea, and India. Latin America and the Middle East and Africa remain smaller but expanding markets, led by pilot projects, infrastructure modernization, and targeted autonomous transport initiatives.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Software

- Hardware

- Services

By Deployment Mode

- Cloud

- On-Premises

- Hybrid

By Application

- Automotive

- Aerospace

- Maritime

- Drones & UAVs

- Industrial Automation

- Others

By End-User

- Commercial

- Defense

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.5 B |

| Forecast Revenue (2034) | USD 12.9 B |

| CAGR (2025-2034) | 12.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component (Software, Hardware, Services), By Deployment Mode (Cloud, On-Premises, Hybrid), By Application (Automotive, Aerospace, Maritime, Drones & UAVs, Industrial Automation, Others, By End-User, Commercial, Defense, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Bosch Group, Aurora Innovation, Inc., Mobileye, Tesla, Inc., NVIDIA Corporation, Aptiv PLC, Apple Inc., Waymo LLC, General Motors, Uber Technologies, Inc., |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment Mode (Cloud, On-Premises, Hybrid), By Application (Automotive, Aerospace, Maritime, Drones & UAVs, Industrial Automation, Others), By End-User (Commercial, Defense, Others) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Artificial Intelligence Integration, Edge Computing Trends & Forecast 2026–2034")

, By Deployment Mode (Cloud, On-Premises, Hybrid), By Application (Automotive, Aerospace, Maritime, Drones & UAVs, Industrial Automation, Others), By End-User (Commercial, Defense, Others) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Artificial Intelligence Integration, Edge Computing Trends & Forecast 2026–2034")

, By Deployment Mode (Cloud, On-Premises, Hybrid), By Application (Automotive, Aerospace, Maritime, Drones & UAVs, Industrial Automation, Others), By End-User (Commercial, Defense, Others) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Artificial Intelligence Integration, Edge Computing Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Autopilot Deployment Tools Market?

Global Autopilot Deployment Tools Market was valued at USD 4.0 billion in 2024 and is projected to reach USD 12.9 billion by 2034, growing at a CAGR of 12.4%. Explore key trends, drivers, and enterprise IT automation growth.

Who are the major players in the Autopilot Deployment Tools Market?

Bosch Group, Aurora Innovation, Inc., Mobileye, Tesla, Inc., NVIDIA Corporation, Aptiv PLC, Apple Inc., Waymo LLC, General Motors, Uber Technologies, Inc.,

Which segments covered the Autopilot Deployment Tools Market?

By Component (Software, Hardware, Services), By Deployment Mode (Cloud, On-Premises, Hybrid), By Application (Automotive, Aerospace, Maritime, Drones & UAVs, Industrial Automation, Others, By End-User, Commercial, Defense, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Autopilot Deployment Tools Market

Published Date : 10 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date