- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Baby Powder Market Outlook Size, Share & Growth | CAGR 6.3%

Global Baby Powder Market Size, Share & Analysis By Product (Talc-based, Talc-free), By Distribution Channel (Online, Offline), Safety Regulations, Consumer Preference Shifts & Forecast 2025–2034

Report Overview

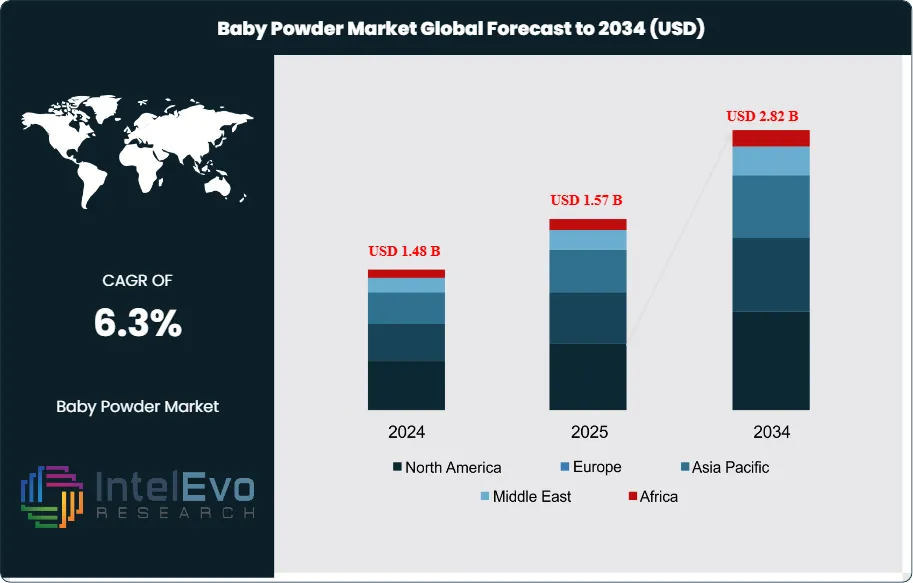

The Baby Powder market was valued at around USD 1.48 Billion in 2024 and is expected to reach nearly USD 2.82 Billion by 2034, growing at a CAGR of approximately 6.3% during 2025–2034. The rising shift toward talc-free, organic, and dermatologist-tested baby powders continues to reshape consumer behavior globally. Growing awareness of infant hygiene, premiumization, and strong demand across Asia-Pacific are further accelerating industry momentum. The market is entering a high-opportunity decade, driven by safety, sustainability, and smart digital marketing.

Get More Information about this report -

Request Free Sample ReportOver the past decade, the market has undergone a steady evolution, shaped by shifting consumer preferences, regulatory oversight, and rising disposable incomes in emerging economies. While baby powder has traditionally been a household staple for infant skincare, recent years have seen a transition toward safer, hypoallergenic, and organic formulations, which are expected to drive future growth.

Demand for baby powder remains firmly rooted in its core function—absorbing moisture and preventing rashes—yet its role is expanding into adult personal care and niche household applications. Rising awareness of infant hygiene, coupled with higher birth rates across Asia-Pacific and Africa, continues to bolster sales. In particular, countries with growing middle-class populations, such as India, Indonesia, and Nigeria, are expected to serve as investment hotspots for multinational players. By contrast, demand in mature markets such as North America and Western Europe is increasingly defined by concerns around product safety and sustainability, spurring greater interest in talc-free and eco-friendly alternatives.

The industry is also being reshaped by technological innovation. Companies are investing in advanced formulations that prioritize natural ingredients such as cornstarch and botanical extracts, aligning with consumer demand for non-toxic, dermatologically tested solutions. Digitalization and e-commerce have further amplified market access, with subscription-based models and targeted marketing campaigns enabling brands to engage more effectively with young parents and caregivers.

However, the sector faces notable challenges. Heightened regulatory scrutiny, particularly regarding talc-based powders, has forced companies to adapt quickly. The high-profile USD 700 million settlement by Johnson & Johnson in 2024 underscores the increasing legal and reputational risks associated with traditional formulations. At the same time, sustainability considerations—ranging from ethical sourcing to recyclable packaging—are emerging as critical differentiators in brand competitiveness.

Overall, the baby powder market presents a dual narrative of risk and opportunity. Established markets are pushing toward safer, more sustainable solutions, while emerging regions offer robust volume growth. Strategic investments in innovation, transparency, and distribution expansion will be central to unlocking long-term value in this evolving global segment.

, By Distribution Channel (Online, Offline), Safety Regulations, Consumer Preference Shifts & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global baby powder market was valued at USD 1.48 Billion in 2024 and is projected to reach USD 2.82 Billion by 2034, expanding at a CAGR of 6.1% during 2025–2034. Growth is primarily fueled by rising awareness of infant hygiene, premiumization of baby care products, and expanding consumer bases in emerging economies.

- Product Type: Talc-free baby powder accounted for more than 65% of global revenue in 2024, reflecting a clear shift toward cornstarch-based and organic formulations amid growing health and safety concerns over talc.

- Distribution Channel: Offline retail, including supermarkets, pharmacies, and specialty stores, captured over 69% of market share in 2024 due to consumer trust in physical outlets and immediate product availability, though e-commerce is registering faster growth at double-digit rates.

- Driver: Increasing birth rates in developing economies such as India, Indonesia, and Nigeria, combined with rising disposable incomes, are expanding the customer base, with Asia-Pacific alone contributing nearly half of global demand.

- Restraint: Regulatory scrutiny and litigation risks linked to talc-based powders remain a significant market barrier, exemplified by Johnson & Johnson’s USD 700 million settlement in 2024, which continues to shape consumer perceptions and compliance costs.

- Opportunity: Organic and hypoallergenic baby powders represent a high-growth niche, expected to grow at over 8% CAGR through 2033, supported by rising demand from health-conscious parents and the premium baby care segment.

- Trend: Sustainability and ethical sourcing are becoming critical purchase drivers, with brands increasingly adopting recyclable packaging and plant-based formulations to meet evolving consumer and regulatory expectations.

- Regional Analysis: Asia-Pacific dominated the market with a 47% share in 2024, driven by high birth rates and rising middle-class populations, while North America and Europe are witnessing slower but steady growth, shaped by premium product adoption and stricter regulatory oversight.

Product Analysis (Talc-based, Talc-free)

By 2025, talc-free baby powder has established itself as the leading product category, capturing more than two-thirds of global market share. This dominance reflects a decisive consumer shift toward safer, natural, and hypoallergenic formulations, often derived from cornstarch and plant-based ingredients. Heightened awareness of potential health risks linked to talc, combined with regulatory scrutiny and ongoing litigation, has accelerated this transition. Parents, particularly in developed markets, increasingly view talc-free products as the safer choice, aligning with broader trends in clean-label and sustainable personal care.

Talc-based baby powder, which accounted for less than 35% of sales in 2024, continues to lose ground as safety concerns weigh on consumer confidence. Although the segment remains relevant in cost-sensitive markets, where affordability and product availability play a larger role, its long-term prospects are constrained. Manufacturers are responding by reformulating existing lines, introducing hybrid or fortified powders, and emphasizing safety certifications to retain market presence. Nonetheless, the structural shift toward talc-free alternatives is expected to accelerate, especially in North America and Europe.

Distribution Channel Analysis (Online, Offline)

As of 2025, offline retail channels continue to dominate the baby powder market, representing close to 70% of global revenue. Supermarkets, hypermarkets, and pharmacies remain the preferred purchasing venues, particularly for parents who prioritize immediate product access, in-person quality assurance, and promotional deals. The presence of established retail networks in both urban and semi-urban regions reinforces this segment’s strength, while in-store marketing campaigns and bundled baby-care packages further drive offline sales.

However, online distribution is emerging as the fastest-growing channel, projected to expand at a CAGR above 9% through 2033. E-commerce platforms and direct-to-consumer (DTC) models are reshaping purchase behaviors, driven by rising internet penetration, smartphone usage, and the convenience of doorstep delivery. Increasingly, parents are leveraging online platforms for product comparisons, subscription-based supply, and access to niche organic and hypoallergenic brands not widely available offline. This digital momentum is expected to gradually erode offline share, particularly in Asia-Pacific and North America.

Regional Analysis

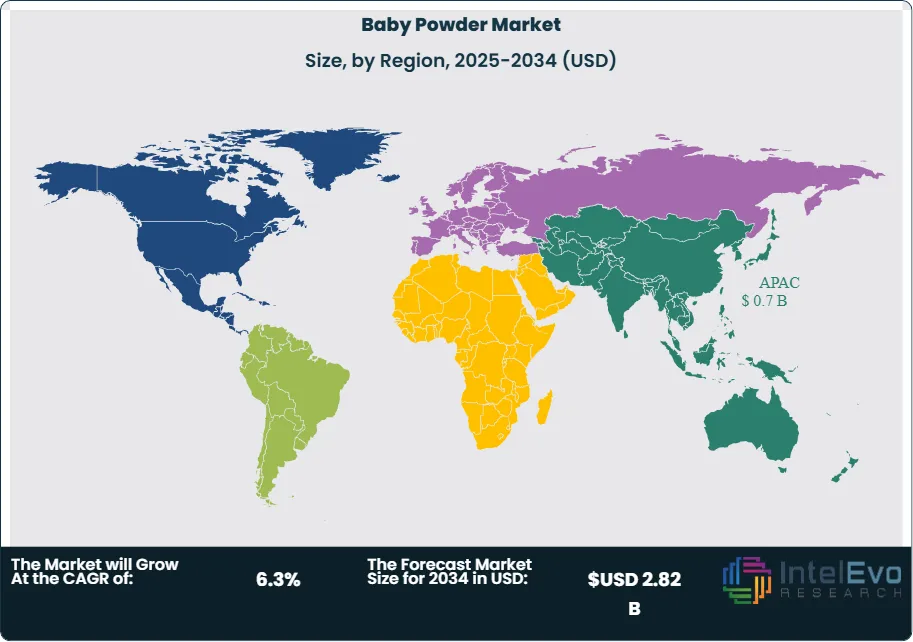

Asia-Pacific continues to be the largest and fastest-growing regional market, commanding nearly half of global revenue in 2025, valued at over USD 0.7 billion. The region’s dominance is underpinned by high birth rates in India, Indonesia, and the Philippines, alongside rising disposable incomes and rapid urbanization. Consumers in Asia-Pacific are also showing a growing preference for organic and talc-free powders, signaling opportunities for premium product penetration.

North America maintains a strong market position, supported by high consumer awareness, stringent safety regulations, and a strong preference for premium, hypoallergenic formulations. Europe follows closely, where the demand for natural and eco-friendly baby powders is intensifying, driven by sustainability-focused consumer behavior and stricter ingredient disclosure norms.

In contrast, Latin America and the Middle East & Africa represent emerging opportunities. Latin America is experiencing growth from an expanding middle class and Western lifestyle adoption, while MEA markets are benefiting from improving healthcare infrastructure, retail expansion, and rising awareness of infant hygiene. These regions, though smaller in current share, are projected to outpace mature markets in growth rates through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product

- Talc-based

- Talc-free

By Distribution Channel

- Online

- Offline

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 1.48 B |

| Forecast Revenue (2034) | USD 2.82 B |

| CAGR (2024-2034) | 6.3% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product (Talc-based, Talc-free), By Distribution Channel (Online, Offline) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Kimberly-Clark, Baby Forest, Prestige Consumer Healthcare, Johnson & Johnson, GLUKi Organics, Pigeon, California Baby, Procter & Gamble, Himalaya Wellness, Church & Dwight, Clorox, Cooney Medical |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Distribution Channel (Online, Offline), Safety Regulations, Consumer Preference Shifts & Forecast 2025–2034")

, By Distribution Channel (Online, Offline), Safety Regulations, Consumer Preference Shifts & Forecast 2025–2034")

, By Distribution Channel (Online, Offline), Safety Regulations, Consumer Preference Shifts & Forecast 2025–2034")

Frequently Asked Questions

How big is the Baby Powder Market?

The Baby Powder Market will reach USD 2.82 Bn by 2034 from USD 1.48 Bn in 2024, driven by rising demand for talc-free, organic, and dermatologist-tested formulations.

Who are the major players in the Baby Powder Market?

Kimberly-Clark, Baby Forest, Prestige Consumer Healthcare, Johnson & Johnson, GLUKi Organics, Pigeon, California Baby, Procter & Gamble, Himalaya Wellness, Church & Dwight, Clorox, Cooney Medical

Which segments covered the Baby Powder Market?

By Product (Talc-based, Talc-free), By Distribution Channel (Online, Offline)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date