- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Barbeque Grill Market Size Growth & Forecast Report | CAGR of 6.9%

Global Barbeque Grill Market Size, Share & Analysis By Product Type (Charcoal, Gas, Electric), By Application (Household, Commercial), Outdoor Cooking Trends, Seasonal Demand & Forecast 2025–2034

Report Overview

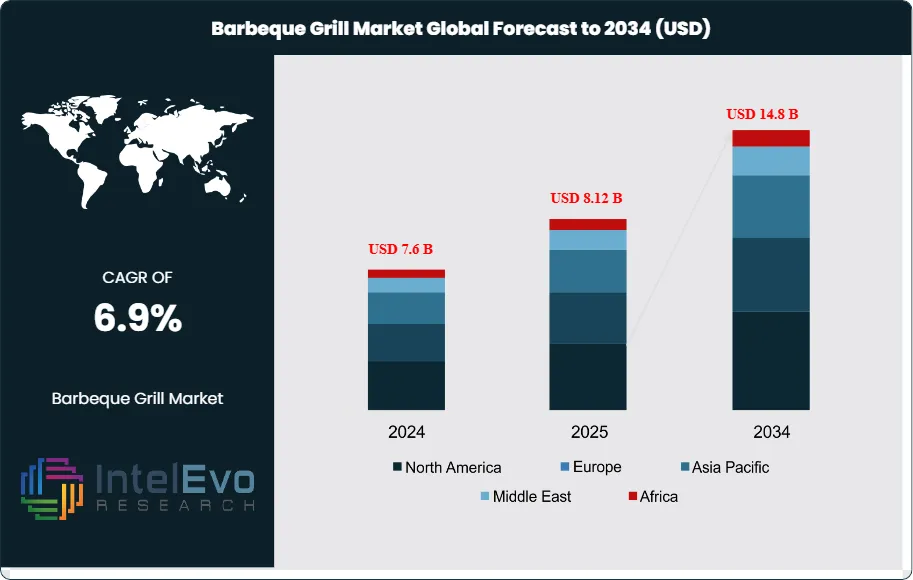

The Barbeque Grill Market is valued at approximately USD 7.6 billion in 2024 and is projected to reach nearly USD 14.8 billion by 2034, expanding at a CAGR of around 6.9% during 2025–2034. The market is gaining momentum as outdoor cooking becomes an essential lifestyle trend, backed by rising urban outdoor spaces, smart grilling technologies, and surging demand for premium gas and electric grills. Growing consumer preference for weekend leisure cooking, smart-connected grilling, and sustainable fuel alternatives is reshaping the industry’s future. With social media driving recipe trends and backyard cooking culture, the next decade is expected to see strong product innovation and higher spending on high-performance grills.

Get More Information about this report -

Request Free Sample Report

After a decade of steady uptake driven by outdoor leisure and at-home entertaining, the category has broadened from seasonal, weekend use to year-round cooking. Ownership penetration remains high in mature markets—80% of U.S. households own a grill or smoker—while participation is deepening beyond dinner into brunch (12%) and breakfast (7%). Product mix continues to evolve: gas remains the largest segment at 43% share and charcoal at 33%, yet both slipped modestly year over year (–1.3 and –0.9 percentage points, respectively) as electric models gained 1.5 points, reflecting urbanization, convenience, and electrification trends. Full-size formats dominate purchase decisions—86% of gas and 62% of electric units purchased—underscoring a preference for multi-zone cooking and entertaining.

Demand-side momentum is reinforced by lifestyle and flavor cues—cited as top drivers by 57% and 40% of consumers—alongside Gen Z and millennial intent to grill more this summer (50% and 25%). Menu diversification is expanding beyond staples such as chicken (83%) and hot dogs (82%) to plant-based experimentation among 28% of millennials, with sauces (68%), marinades (57%), and dry rubs (55%) elevating the experience. On the supply side, innovation is accelerating: connected “smart” grills with Wi-Fi, app-based monitoring, and digital temperature control are improving outcomes for less experienced users; pellet and electric platforms address ease-of-use and emissions; and material advances are extending durability while reducing maintenance. Sustainability is an emerging differentiator as manufacturers pilot eco-friendly materials and lower-emission heat sources; in parallel, natural-gas primary usage among U.S. owners stands near 9%, signaling a niche for plumbed, patio-centric installations.

Key risks include volatile input costs (steel, electronics), retail channel normalization post-pandemic, weather variability, and meat price inflation—10% of consumers expect to grill less on cost grounds. Regulatory scrutiny on outdoor emissions in dense urban areas may also accelerate the shift toward electric and pellet systems. Regionally, North America remains the largest profit pool given high ownership and replacement cycles; Western Europe is steady with premiumization in gas and pellet; and Asia Pacific and Latin America are the fastest-growing investment frontiers as Western cooking habits diffuse and outdoor living spaces proliferate. Investors should watch electrification, smart-feature attach rates, and premium full-size formats as leading indicators of value creation over the next cycle.

, By Application (Household, Commercial), Outdoor Cooking Trends, Seasonal Demand & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global barbeque grill market will expand from USD 7.6 billion in 2024 to USD 14.8 billion by 2034 (6.9% CAGR), adding roughly USD 7.2 billion in new value on the back of outdoor leisure, at-home entertaining, and product replacement cycles.

- Product Type: Gas grills lead with a 57.1% revenue share in 2023, supported by faster heat-up, cleaner operation, and precise temperature control that appeal to frequent users and restaurants seeking throughput.

- Application/End Use: Commercial deployments account for 59.0% of demand (2023), reflecting robust procurement by restaurants, caterers, and venues; higher utilization rates and multi-unit purchases sustain premium feature adoption and aftermarket revenues.

- Driver: Penetration and participation remain high—~80% of U.S. households own a grill/smoker, and ~20% of consumers plan to grill more seasonally, led by Gen Z (50% of intenders) and millennials (25%), reinforcing recurring fuel and accessories consumption.

- Restraint: Cost sensitivity is rising; ~10% of consumers expect to grill less due to meat inflation, while steel and electronic component volatility and unfavorable weather patterns weigh on upgrade cycles and retail sell-through.

- Opportunity: Asia Pacific and Latin America are poised for outperformance as Western cooking formats diffuse—APAC is set to deliver a ~6% CAGR through 2033, capturing an outsized share of incremental value via urban, multi-family, and balcony-safe formats (electric, compact gas).

- Trend: Feature-rich, connected equipment is scaling; smart controls (Wi-Fi/app thermoregulation, probes) and lower-emission platforms (pellet/electric) are gaining mix, while full-size configurations dominate purchases (≈86% of gas and ≈62% of electric), underscoring demand for multi-zone cooking and entertaining.

- Regional Analysis: North America leads with 52.5% share (USD 2.73 billion in 2023) on high ownership and replacement rates; Western Europe maintains premiumization in gas/pellet at mid-single-digit growth, whereas APAC emerges as the key investment hotspot with the fastest CAGR and expanding modern retail channels.

Type Analysis

Gas remains the anchor of the category in 2025, accounting for an estimated 55–58% of global barbeque grill revenue as operators and households prioritize instant ignition, precise temperature control, and lower cleanup. Premiumization is evident in multi-burner, full-size formats with integrated sear zones, rotisseries, and app-enabled thermostats. While unit growth is steady (≈4–5% CAGR through 2030), value growth is amplified by higher average selling prices (ASPs) and accessory attach rates (side burners, griddle plates, connected probes).

Charcoal retains a loyal enthusiast base—roughly 30–33% share—driven by smoke flavor and ritualized usage. Innovation centers on faster ignition systems, airflow optimization, and ceramic/kamado designs that extend into low-and-slow smoking. Growth moderates (≈3–4% CAGR) as urban regulations and convenience bias cap conversion, yet specialty fuel (lump, flavored pellets/wood chunks) supports a resilient aftermarket.

Electric is the fastest riser at 10–12% share in 2025, expanding at 6–8% CAGR on apartment/balcony compliance, emissions scrutiny, and the convergence of indoor/outdoor cooking. Compact plug-in models and high-wattage, digitally controlled plates increasingly replicate gas performance, while hybrid “pellet-electric” architectures blur lines between grilling and smoking for consistent results with minimal oversight.

Application Analysis

Commercial use continues to lead with ~58–60% revenue share in 2025, underpinned by restaurants, caterers, hotels, stadiums, and event venues. High utilization drives demand for heavy-duty, energy-efficient platforms with quick recovery, multi-zone cooking, and NSF-grade materials. Feature adoption—Wi-Fi monitoring, HACCP-ready temperature logging, and automated fuel feed (pellet)—supports throughput, consistency, and labor productivity, sustaining mid-single-digit growth.

Household adoption is broadening beyond weekend cookouts as consumers integrate grilling into weekday meals. Penetration in mature markets remains high (e.g., ~80% of U.S. households own a grill/smoker), while urban dwellers favor portable gas and electric units. Replacement cycles, outdoor-living upgrades (kitchen islands, pergolas), and accessory ecosystems (thermometers, rubs, griddles) lift household spend, with value growth outpacing units on premium features and materials.

End-Use Analysis

Residential buildings account for roughly 40–45% of unit demand in 2025, with growth supported by home improvement projects and the normalization of year-round grilling. Built-in gas islands and weather-resistant materials (304/430 stainless, porcelain-enameled steel) push ASPs higher, while compact electrics open incremental demand in multi-family settings constrained by open-flame rules.

Commercial buildings—restaurants, QSRs, ghost kitchens, hotels—represent 50–55% of revenue due to higher-spec equipment and frequent replacement driven by uptime requirements. Operators increasingly prioritize total cost of ownership through efficient burners, insulated hoods, and modular components that reduce maintenance downtime.

Industrial/institutional facilities (campuses, hospitals, amusement parks, foodservice commissaries) remain a smaller but expanding niche (≈5–8% share), selecting durable, high-capacity grills that integrate with centralized ventilation and safety systems. Compliance, record-keeping, and consistency are catalysts for electrified and pellet solutions.

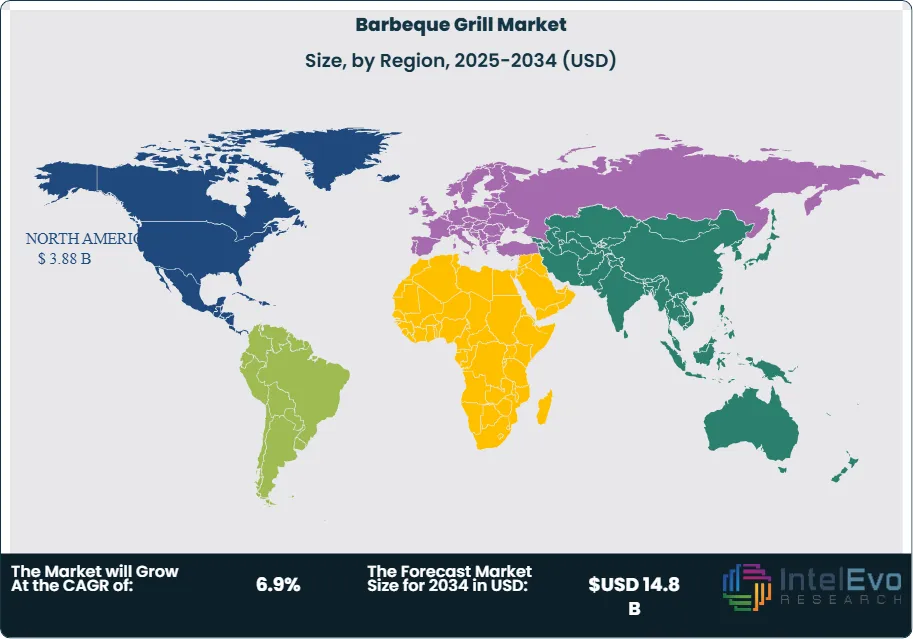

Regional Analysis

North America maintains leadership at ~50–52% of global revenue in 2025, supported by entrenched grilling culture, high disposable income, and robust replacement cycles. Product mix skews toward full-size gas and pellet units, with smart features and premium finishes driving value. Europe holds ~20–22% share, where convenience and regulatory dynamics favor gas and electric; northern markets emphasize durability and energy efficiency, while southern markets benefit from outdoor dining tourism.

Asia Pacific is the fastest-growing region (≈6–7% CAGR through 2030) as Western cooking formats diffuse across China, Southeast Asia, Australia, and Japan. Urbanization and balcony restrictions channel demand toward electric and compact gas platforms, while modern retail and e-commerce expand distribution. Latin America (≈5–6% share) scales from a low base on rising incomes and backyard entertaining, with Brazil and Mexico as demand anchors. The Middle East & Africa (≈4–5% share) sees steady gains tied to hospitality investments and outdoor dining, where heat-resilient materials and efficient burners address climatic conditions.

Get More Information about this report -

Request Free Sample Report

Market Key Segments

By Product Type

- Charcoal

- Gas

- Electric

By Application

- Household

- Commercial

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 7.6 B |

| Forecast Revenue (2034) | USD 14.8 B |

| CAGR (2024-2034) | 6.9% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Charcoal, Gas, Electric), By Application (Household, Commercial) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Traeger Pellet Grills LLC, The Coleman Company, Inc., Char Broil LLC, Royal Gourmet, Landmann, Weber, Dansons, Broilmaster, Kenmore, The Middleby Corporation, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Household, Commercial), Outdoor Cooking Trends, Seasonal Demand & Forecast 2025–2034")

, By Application (Household, Commercial), Outdoor Cooking Trends, Seasonal Demand & Forecast 2025–2034")

, By Application (Household, Commercial), Outdoor Cooking Trends, Seasonal Demand & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date