- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Basketball Equipment Market Size, Growth Forecast | CAGR of 6.7%

Global Basketball Equipment Market Size, Share & Analysis By Equipment (Basketball Hoop, Basketball Shoes, Basketball Apparel, Basketball Goal, Other Equipments), By Distribution Channel (Specialty and Sports Shops, Department and Discount Stores), Sports Participation Trends, Brand Competition & Forecast 2025–2034

Report Overview

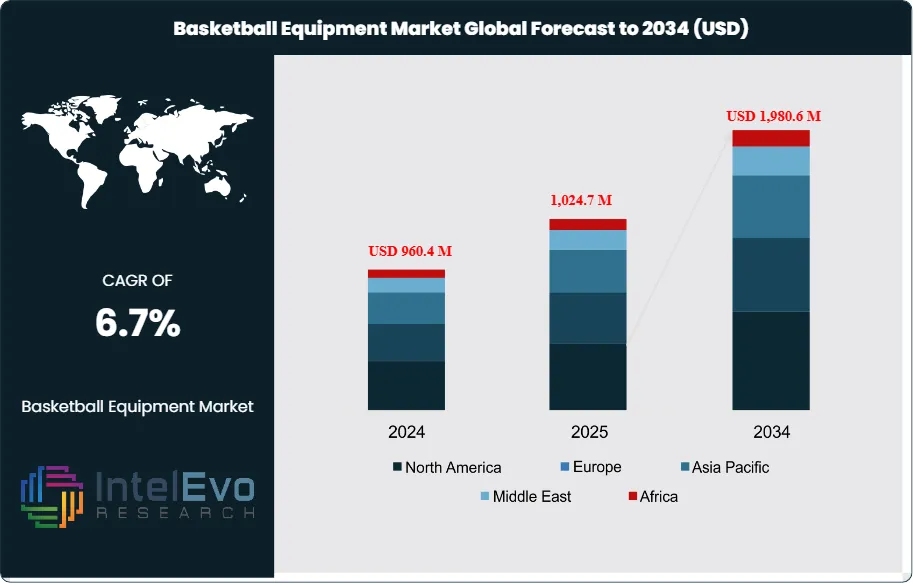

The Basketball Equipment Market is valued at around USD 960.4 million in 2024 and is projected to reach nearly USD 1,980.6 million by 2034, expanding at a CAGR of approximately 6.7% during 2025–2034. Growing global participation, rising sponsorship investment, and the surge of data-driven training technologies are reshaping demand across apparel, footwear, balls, and goal systems. Digital engagement through livestreaming, esports tie-ins, and athlete-led social media campaigns is pushing basketball deeper into youth culture. With outdoor courts, community programs, and women’s leagues gaining momentum worldwide, the next decade is expected to unlock strong multi-segment revenue growth.

Get More Information about this report -

Request Free Sample ReportMarket expansion reflects a steady post-pandemic normalization in team sports participation and a structural shift toward performance and safety upgrades. From 2018 to 2024 the category expanded at an estimated ~3% CAGR, accelerating in 2022–2024 as school and community programs returned to full schedules and retailers cleared supply bottlenecks. Core products—basketballs, hoops/backboards, apparel, footwear accessories, and protective gear—anchor demand; balls and goal systems together account for roughly one-half of revenue, while protective gear and apparel contribute an additional ~30%, supported by rising emphasis on injury prevention and training efficiency.

Demand-side drivers include increasing youth and recreational participation, the global visibility of elite leagues, and the rapid adoption of 3x3 formats ahead of the 2028 Olympic cycle. On the supply side, premiumization and direct-to-consumer (DTC) models are lifting average selling prices, with higher-end composite balls and breakaway rims outgrowing entry tiers. E-commerce now represents about 45–50% of sell-through in mature markets, enabling customization and faster refresh cycles. Key challenges persist: rubber and composite input inflation since 2021, freight volatility, and exposure to counterfeit goods online. Regulatory and sustainability pressures—from chemicals compliance to recycled-content mandates—are reshaping materials choices and supplier qualification, raising barriers to entry but also encouraging brand differentiation.

Technology is reshaping adoption. Connected “smart” balls with embedded sensors and mobile analytics are expanding from elite to training segments; advanced backboard laminates improve durability for schools and municipalities; and eco-formulations (recycled TPU, bio-based adhesives) are gaining traction, with leading brands targeting double-digit recycled content by the end of the decade. AI-enabled sizing, personalization, and inventory planning are trimming returns and improving service levels.

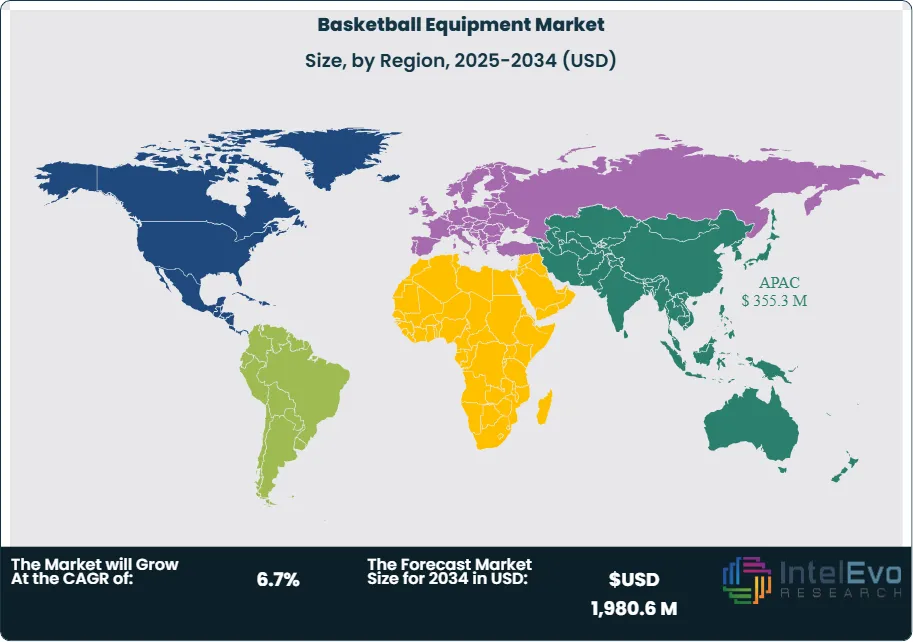

Regionally, North America remains the largest profit pool (≈35–40% of revenue) on strong institutional procurement and a deep retail ecosystem. Asia–Pacific is the fastest-growing opportunity (≈5–6% CAGR), led by China’s city leagues and India’s urban programs, while Europe shows steady replacement-led demand. Emerging hotspots include Southeast Asia, the Middle East’s multi-sport complexes, and Latin America’s school investments. For investors, the most attractive themes are premium goal systems, connected training hardware, women’s basketball and 3x3 equipment lines, and B2B channels serving schools and municipalities.

, By Distribution Channel (Specialty and Sports Shops, Department and Discount Stores), Sports Participation Trends, Brand Competition & Forecast 2025–2034")

Key Takeaways

- Market Growth: The Global Basketball Equipment Market is projected to increase from USD 960.4 million in 2024 to USD 1,980.6 million by 2034 at a 6.7% CAGR, adding approximately USD 1,020 million in incremental value. The expansion is driven by post-pandemic participation recovery, rising school and club procurement, and continued premiumization across footwear, balls, and training systems.

- Equipment (Product Type): Basketball shoes lead with ~36% revenue share in 2024, supported by faster refresh cycles, athlete endorsements, and tiered pricing. Average selling prices in branded shoes rose an estimated 3–4% YoY (2022–2024) as premium models and limited drops expanded mix.

- Distribution Channel: Specialty & sports shops account for ~58% of sell-through, driven by expert fitting, team orders, and bundled services (stringing, customization). Online/DTC is the fastest-growing route (≈8–9% CAGR forecast) and is on pace to approach ~40% share by 2034.

- Driver: Visibility from elite leagues and collegiate programs, combined with expanding school and community programs, is lifting participation and equipment turnover; each 1% increase in average selling price adds ~USD 9.1 million in annual market value off the 2024 base.

- Restraint: Persistent input-cost inflation in rubber/composite materials and freight volatility compress margins; a 10% raw-material increase can reduce gross margin by ~150–200 bps for mid-tier products absent pricing or mix actions.

- Opportunity: Smart/connected training gear (sensorized balls, app-linked shooting analytics) is forecast to grow >15% CAGR from a small base, potentially reaching USD 120–150 million by 2034 as teams and academies formalize data-driven practice.

- Trend: Sustainability is moving from marketing to materials, with recycled TPU covers, bio-based adhesives, and repairable goal systems gaining share; leading brands (e.g., Wilson, Spalding, Nike, Adidas) are scaling SKUs with double-digit recycled content and piloting take-back programs.

- Regional Analysis: North America remains the profit center with ~37% global share on deep retail ecosystems and institutional budgets, while Asia–Pacific is the fastest-growing region (~5–6% CAGR) led by China, India, and Southeast Asia. Europe is stable replacement-led demand (~3–4% CAGR), and emerging hotspots include the Middle East and Latin America where multi-sport complexes and school investments are expanding.

Equipment Analysis

The equipment mix in 2025 continues to skew toward footwear, with basketball shoes sustaining leadership at ~36% revenue share. Demand is anchored by faster refresh cycles (6–12 months for active players), signature-athlete launches, and performance gains in cushioning, traction compounds, and upper materials. Average selling prices for branded models have trended 3–4% higher since 2024 as premium and limited-edition lines take greater mix. Hoops (rims/backboards) and full goal systems together remain the second profit pool; standalone hoops account for ~21% of sales on steady replacement in schools and municipal courts, while goal systems (in-ground and portable) hold ~15% driven by home-court upgrades and safety-compliant installations in institutions.

Apparel represents ~18% of equipment value, supported by the crossover of compression baselayers and teamwear into lifestyle channels and by rising women’s and youth participation. “Other equipment”—including basketballs, protective gear, and training aids—accounts for the remaining ~10%; within this, composite-cover balls and sensor-enabled training gear are the fastest growers, with connected products expected to expand >15% CAGR through 2030 from a small base as academies formalize data-driven practice.

Distribution Channel Analysis

Specialty and sports shops remain the primary route to market, representing ~58% of 2025 sell-through. Their edge stems from expert fitting, team-order aggregation, and access to premium allocations, which lift basket sizes and conversion. Many are adding experiential elements—shooting bays, gait and jump assessments—to support upselling into higher-ASP shoes and pro-grade goal systems.

Department and discount stores capture the balance, competing on convenience and price for entry- and mid-tier SKUs. While their per-ticket value is lower, traffic is resilient in suburban formats. Parallel to both channels, brand DTC and marketplace e-commerce are compounding at an estimated 8–10% CAGR (2025–2030), and could approach ~40% of category sales by 2034, pressuring generalists while complementing specialty retailers via click-and-collect and team portals.

End-Use Analysis

Residential demand (backyard systems, portable goals, balls, and entry-to-mid footwear) accounts for roughly 28–30% of 2025 revenue. Upgrades from basic to breakaway-rim systems and the shift to composite balls sustain pricing, while DIY installation kits broaden access in emerging suburbs.

Institutional/Education is the largest end-use at ~32–34%, underpinned by school and collegiate programs with 5–7-year replacement cycles for hoops/backboards and annual refresh for footwear and apparel. Procurement increasingly specifies safety padding, tempered glass backboards, and low-VOC adhesives, nudging ASPs higher. Commercial & Professional facilities—clubs, training centers, and arenas—contribute ~36–38% and drive the premium end of the market, adopting FIBA/NBA-spec systems, connected shot-tracking, and uniform programs; this cohort shows the highest capital intensity and service revenues (installation, maintenance).

Regional Analysis

North America remains the anchor profit pool with ~37% global share in 2025, supported by deep retail ecosystems, robust school/college procurement, and strong participation. Europe delivers steady replacement-led growth (≈3–4% CAGR to 2030), with Spain, France, Germany, and the Balkans as core demand centers; regulations around facility safety and recycled materials are shaping specifications and vendor selection.

Asia Pacific is the fastest-expanding region (≈5–6% CAGR), propelled by urban leagues, school investment, and rising middle-class spending in China, India, and Southeast Asia. Latin America is scaling from a smaller base (≈4–5% CAGR) as public-school sports programs expand in Brazil, Mexico, and the Southern Cone. The Middle East & Africa, though nascent, shows momentum tied to multi-sport complex development in the GCC and municipal recreation upgrades in select African metros, positioning MEA for mid-single-digit growth through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Equipment

- Basketball Hoop

- Basketball Shoes

- Basketball Apparel

- Basketball Goal

- Other Equipments

By Distribution Channel

- Specialty and Sports Shops

- Department and Discount Stores

By Regions

- North America

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 960.4 M |

| Forecast Revenue (2034) | USD 1,980.6 M |

| CAGR (2024-2034) | 6.7% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Equipment (Basketball Hoop, Basketball Shoes, Basketball Apparel, Basketball Goal, Other Equipments), By Distribution Channel (Specialty and Sports Shops, Department and Discount Stores) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Under Armour, Spalding Sports Equipment, McDavid, Adidas, Nivia Sports, JORDAN, Mizuno, Amer Sports, Puma, Rawlings Sporting Goods, |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Distribution Channel (Specialty and Sports Shops, Department and Discount Stores), Sports Participation Trends, Brand Competition & Forecast 2025–2034")

, By Distribution Channel (Specialty and Sports Shops, Department and Discount Stores), Sports Participation Trends, Brand Competition & Forecast 2025–2034")

, By Distribution Channel (Specialty and Sports Shops, Department and Discount Stores), Sports Participation Trends, Brand Competition & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date