- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Battery Passport Technology Market Size, Share | CAGR 32.1%

Global Battery Passport Technology Market Size, Share, Analysis By Technology (Blockchain-Backed Ledgers, Cloud-Based Databases, IoT & AI-Integrated Lifecycle Platforms), By Identifier Type (Encrypted QR Codes, RFID Tags, NFC Chips), By Data Type (Carbon Footprint Metrics, ESG Material Sourcing, Recycled Content Disclosures, State-of-Health Analytics) Industry Region & Key Players-Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

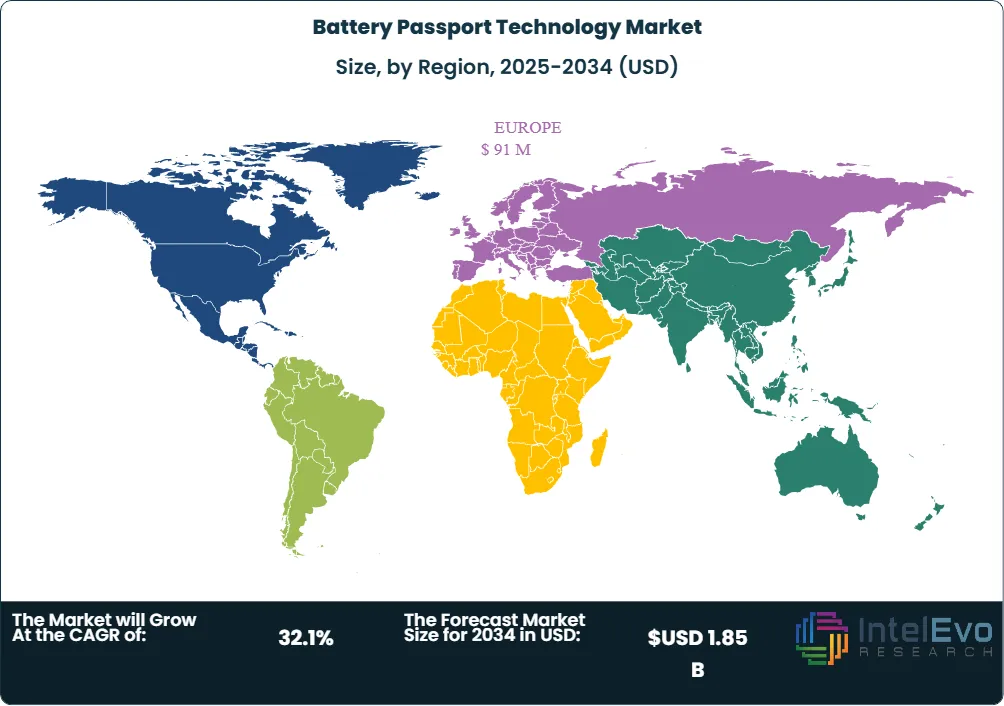

| USD 0.15 Billion | USD 1.85 Billion | 32.1% | Europe, 60.4% |

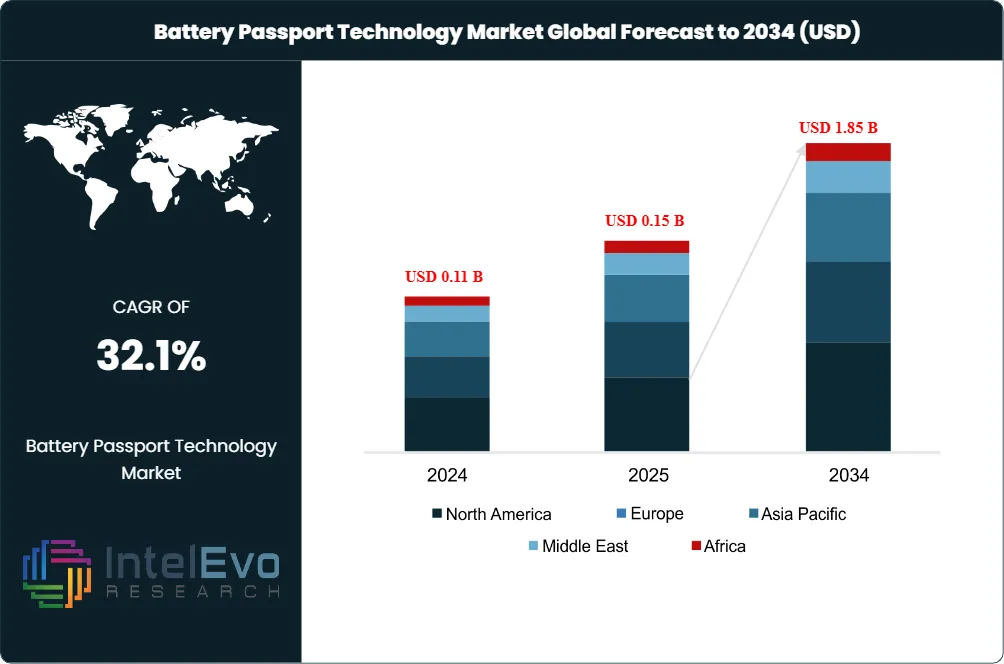

The Battery Passport Technology Market was valued at USD 0.11 Billion in 2024 and USD 0.15 Billion in 2025. The market is projected to reach USD 1.85 Billion by 2034, expanding at a CAGR of 32.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 1.70 Billion over the analysis period. Demand is anchored in EU Regulation 2023/1542, which mandates a digital battery passport for all electric vehicle batteries, light-means-of-transport (LMT) batteries, and industrial batteries above 2 kWh placed on the EU market from 18 February 2027.

Get More Information about this report -

Request Free Sample ReportThe battery passport technology market is shifting from compliance-driven to value-driven adoption. In 2025, Tier-1 suppliers and OEMs in Europe and North America are strengthening IT and data infrastructures ahead of regulatory enforcement, with pilots running across the Catena-X automotive data space and CEN/CENELEC interoperability frameworks. By 2030, passports will function as a market-access requirement for EU sales, mirroring CE marking. The U.S. National Institute of Standards and Technology (NIST) initiated technical evaluations of battery traceability frameworks in 2024, signaling regulatory convergence between Brussels and Washington.

Lithium-ion is forecast to remain the largest battery-type segment through 2034, driven by EV and stationary storage scale where chemistries hold approximately 90 to 95% share. IoT and AI-integrated passport architectures form the fastest-growing technology layer because embedded modules capture impedance spectra, thermal propagation, and micro-cycle stress signatures that feed directly into standardized passport fields. The Battery Pass Consortium's DIN DKE SPEC 99100 standard, published 15 January 2025, defines required data attributes and accelerates vendor procurement decisions across German automotive OEMs.

Europe led the battery passport technology market with approximately 60.4% revenue share in 2025, anchored by Germany's Battery Pass consortium, France's recycling pilots tied to the Global Battery Alliance, and Sweden's value-chain working groups. North America is forecast to record the highest growth rate over 2025-2034, supported by Inflation Reduction Act incentives, Canadian Battery Metals Association of Canada (BMAC) frameworks, and Tesla-associated mine-to-cell pilots. By 2034, vendors integrating blockchain audit trails, cloud-SaaS deployment, and verified Joint Research Centre (JRC) carbon-footprint methodologies are positioned to capture the largest share of the absolute dollar opportunity.

Market Definition & Scope

The battery passport technology market is defined as the global commercial activity covering software platforms, IoT and AI hardware modules, blockchain infrastructure, cloud services, and integration services that produce, store, and exchange digital battery passports. A digital battery passport is a machine-readable record accessible via QR code or unique identifier that documents a battery's identification, chemistry, carbon footprint, recycled content, state-of-health performance, durability, due-diligence sourcing data, and end-of-life routing.

This analysis includes solutions deployed across automotive, industrial energy storage, light-means-of-transport, and consumer-electronics battery applications. Excluded are general-purpose enterprise resource planning (ERP) software, generic battery management systems (BMS) without passport-data export, and non-battery digital product passport implementations (textiles, electronics chassis). Adjacent markets including battery analytics platforms, supply-chain traceability for non-battery commodities, and pure carbon-accounting software without battery-specific data fields are tracked separately. The market sits within the broader digital product passport (DPP) parent market, with batteries representing the first regulated DPP category under EU Regulation 2023/1542.

, By Identifier Type (Encrypted QR Codes, RFID Tags, NFC Chips), By Data Type (Carbon Footprint Metrics, ESG Material Sourcing, Recycled Content Disclosures, State-of-Health Analytics) Industry Region & Key Players-Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The battery passport technology market grew from USD 0.15 Billion in 2025 toward a forecast value of USD 1.85 Billion by 2034 at a 32.1% CAGR.

- Segment Dominance: Cloud-SaaS deployment captured 61% revenue share in 2025, driven by continuous regulatory updates and cross-geography compliance scalability.

- Segment Dominance: The automotive industry held 40 to 45% revenue share in 2025, anchored by EV battery passport mandates affecting CATL, BMW, Volvo, and Stellantis.

- Driver: EU Regulation 2023/1542 enforcement on 18 February 2027 is the primary driver, requiring digital passports for all EV, industrial, and LMT batteries above 2 kWh.

- Restraint: Data standardization across Tier-2 and Tier-3 suppliers remains the principal constraint, with cobalt and lithium upstream visibility limited to fewer than 30% of mines per Global Battery Alliance estimates.

- Opportunity: The carbon-footprint compliance metric represents 29% of passport data demand, opening a USD 0.5 Billion-plus services and verification opportunity by 2034.

- Trend: IoT and AI-integrated passports form the fastest-growing technology, embedding multi-sensor stacks for SOH, SOE, and thermal telemetry into passport infrastructures.

- Regional: Europe led with approximately 60.4% share in 2025 equivalent to roughly USD 91 Million, while North America is forecast as the fastest-growing region during the analysis period.

Key Insights Summary

- EU Regulation 2023/1542 mandates digital battery passports for all EV, LMT, and industrial batteries above 2 kWh placed on the EU market from 18 February 2027, accessed via QR code per Annex XIII.

- DIN DKE SPEC 99100, published by the German Institute for Standardization on 15 January 2025, defines required passport data attributes and is the first national-level technical specification covering Annex XIII requirements.

- The European Commission's Joint Research Centre (JRC) requires site-specific and batch-level data for carbon footprint calculation per the draft delegated act, with carbon offsets explicitly disallowed in reported emissions.

- Circulor reached USD 69.2 Million cumulative funding across three venture rounds and was the first vendor to deploy battery passports at full industrial scale with Volvo Cars in June 2024.

- CATL and BMW Group signed a Memorandum of Understanding on 25 February 2026 to pilot Catena-X-based cross-border passport data exchange, the largest disclosed China-EU passport collaboration to date.

- Material recovery targets under EU Regulation 2023/1542 require 50% lithium, 90% nickel, 90% cobalt, and 90% copper recovery by December 2027, rising to 80% lithium by 2031 per Annex XII.

- EU carbon footprint declaration with third-party verification became required in December 2025, the first hard data-disclosure deadline under the regulation.

Competitive Landscape Overview

The battery passport technology market is fragmented in 2025, with the top four vendors (Circulor, Minespider, Siemens, and Optel Group) controlling an estimated 38 to 45% of global revenue and the long tail of specialist software vendors and consortium-funded projects accounting for the remainder. Circulor holds an early-mover position based on its Volvo Cars production deployment in June 2024 and partnerships with Polestar, Powin, and Acculon Energy. Minespider GmbH anchors blockchain-based identity through the Open Battery Passport platform launched in May 2023 and the BATRAW project funded under Horizon Europe grant 101058359. Siemens AG entered through SiGREEN and Catena-X integration. Optel Group leads North American deployment via the Canadian Battery Metals Association of Canada (BMAC) NMC traceability program.

Competitive evolution is shifting from blockchain-only architectures toward hybrid stacks combining cloud SaaS, decentralized identifiers, and IoT telemetry. Vendor differentiation centers on three axes: depth of upstream supplier integration (mine-to-cell), regulatory readiness against the JRC carbon-footprint methodology, and interoperability with the Catena-X automotive data space. Strategic partnerships are intensifying ahead of the February 2027 mandate: Rockwell Automation joined Circulor in October 2024 for battery, automotive, and tire traceability, while Tata Elxsi partnered with Minespider in January 2025 to extend reach into Indian battery manufacturing. New entrants concentrate in adjacent niches such as decentralized identity (Spherity GmbH) and battery analytics for state-of-health passport data (TWAICE Technologies).

Competitive Landscape Matrix

| Company | HQ | Position | Key Product / Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Circulor Ltd. | UK | Leader | Battery Passport SaaS, blockchain traceability | Europe, North America | Apr 2025 partnership with Powin for utility-scale ESS passports |

| Minespider GmbH | Germany | Leader | Open Battery Passport, blockchain platform | Europe, Asia Pacific | Jan 2025 collaboration with Tata Elxsi on India deployment |

| Siemens AG | Germany | Leader | SiGREEN, Catena-X integration suite | Europe, North America | Feb 2026 expanded Catena-X enabled passport pilots |

| Optel Group | Canada | Leader | Optchain Battery Passport platform | North America, Europe | 2024 led Canadian BMAC NMC traceability framework |

| Circularise BV | Netherlands | Challenger | MassBalancer, DPP for batteries | Europe | Feb 2026 joined BatteryPass-Ready as Supporting Partner |

| AVL List GmbH | Austria | Challenger | AVL Battery Passport solution | Europe | Continued expansion of automotive OEM pilots through 2025 |

| iPoint-systems GmbH | Germany | Challenger | iPoint Battery Passport, DPP suite | Europe | 2025 expanded automotive supplier onboarding modules |

| SAP SE | Germany | Challenger | SAP Sustainability Footprint Mgmt | Europe, North America | 2025 launched DPP integration with Catena-X |

| Spherity GmbH | Germany | Niche Player | Decentralized identity for DPP | Europe | 2025 expanded credentialing partnerships |

| TWAICE Technologies | Germany | Niche Player | Battery analytics for SOH passport data | Europe | 2025 SOH analytics integration with Battery Pass project |

Segmentation Analysis

The battery passport technology market is segmented by technology, battery type, industry, end-user, and business model, each producing distinct competitive and adoption dynamics across the forecast period.

By Technology

The battery passport technology market by technology is split into blockchain, cloud, and IoT and AI-integrated solutions, with cloud-based architectures holding the largest 2025 revenue share at approximately 47% because most pilots run on AWS, Microsoft Azure, or SAP Business Technology Platform infrastructure that supports continuous regulatory updates. Blockchain captures roughly 31% share, anchored by Minespider, Circulor, and Circularise tamper-proof audit trails that satisfy due-diligence reporting under EU Regulation 2023/1542. IoT and AI-integrated passports form the fastest-growing sub-segment with a forecast CAGR exceeding 36%, propelled by embedded multi-sensor stacks that capture charge-rate gradients, impedance spectra, thermal propagation profiles, and micro-cycle stress signatures. AI pipelines convert raw telemetry into standardized passport fields including SOH and SOE projections, degradation coefficients, and carbon-intensity values.

By Battery Type

Lithium-ion batteries account for the largest share of the battery passport technology market across 2025 to 2034, reflecting their 90 to 95% share of global EV and stationary storage volumes. The European Commission projects lithium battery demand will grow more than tenfold by 2030, driving the bulk of passport-enabled transactions. Lead-acid batteries hold a smaller share, primarily addressing industrial backup power and automotive starter applications outside the 2 kWh threshold. Sodium-ion is the fastest-emerging chemistry segment, with CATL, HiNa Battery, and Faradion advancing commercial production through 2025 and 2026; passport vendors are developing chemistry-specific data fields ahead of broader sodium-ion EV deployment expected by 2028.

By Industry

The automotive industry dominated battery passport technology demand with 40 to 45% revenue share in 2025, driven by EV battery documentation requirements at General Motors, Ford, Stellantis, BMW, Volkswagen, and Volvo Cars. BMW and CATL's February 2026 MoU on cross-border Catena-X data exchange illustrates how OEM-supplier pairs are operationalizing the regulation ahead of the 2027 deadline. Energy and utility applications represent the second-largest industry segment, driven by stationary battery energy storage systems (SBESS) above 2 kWh that fall under the same regulation. Powin's April 2025 partnership with Circulor extended battery passports into utility-scale energy storage. Off-highway and industrial applications, including forklifts and mining haul trucks, contribute the remaining demand and are expected to grow as ATEX and CE-marking conformity expand.

By End-User

Original equipment manufacturers (OEMs) controlled 41% of battery passport technology demand in 2025 because EU Regulation 2023/1542 places primary compliance responsibility on the entity placing the battery on the market. Tier-1 cell suppliers including CATL, LG Energy Solution, Samsung SDI, SK On, and Panasonic represent the second-largest end-user group as they generate the manufacturing-stage data populating passport fields. Recyclers, including Umicore, Redwood Materials, and Li-Cycle, form the third end-user category and access passport data to improve material recovery routes. Logistics providers and second-life integrators are emerging as the fastest-growing end-user segment, with battery resale values projected to rise 20 to 30% when verifiable SOH passport data accompanies used cells per industry analysis.

By Business Model

Cloud SaaS subscription models led with 61% of 2025 battery passport technology revenue, reflecting buyer preference for ongoing regulatory updates and lower upfront capital. Per-passport licensing models, common at Circulor and Optel, capture per-unit fees as battery volumes scale toward the European Commission's projected 30 million annual EV passports by 2030. Custom integration and consulting services account for approximately 18% of revenue, anchored by initial implementation projects at OEMs requiring Catena-X integration. Pricing benchmarks for SaaS passport subscriptions range from EUR 0.50 to EUR 5.00 per battery depending on data depth and verification level. Implementation timelines for first-year deployment typically run 9 to 14 months across Tier-1 supplier networks.

Regional Analysis

The global battery passport technology market shows distinct regional revenue and growth profiles across Europe, North America, Asia Pacific, Latin America, and Middle East and Africa, with EU regulatory enforcement driving a structurally European-skewed geographic mix in 2025.

Europe

Europe led the battery passport technology market with approximately 60.4% share in 2025, equivalent to roughly USD 91 Million in regional revenue. Germany anchors regional demand through the Battery Pass consortium co-funded by the Federal Ministry for Economic Affairs and Climate Action (BMWK), bringing together AUDI AG, BASF SE, BMW AG, FIWARE Foundation, Fraunhofer IPK, SYSTEMIQ, TWAICE, Umicore, and VDE Renewables. France contributes through recycling pilots tied to the Global Battery Alliance, while Sweden engages via the GBA value-chain working group, and the Netherlands and Belgium participate in the BASE project under Horizon Europe grant 101157200. The DIN DKE SPEC 99100 standard published 15 January 2025 sets the technical baseline for European deployment.

North America

North America held an estimated 21% share of the battery passport technology market in 2025, valued near USD 32 Million. The United States anchors regional demand through Inflation Reduction Act battery-manufacturing incentives and growing corporate ESG reporting requirements at Tesla, GM, and Ford. NIST initiated technical evaluations of battery traceability frameworks in 2024. Canada drives regional momentum through the 2024 OPTEL-Delphi-Norda Stelo program with the Battery Metals Association of Canada (BMAC) producing an auditable ESG and GHG reporting framework for domestic NMC supply chains. The region is forecast as the fastest-growing globally, with U.S. country-level growth tracking near 29.8% CAGR per cross-source synthesis.

Asia Pacific

Asia Pacific captured approximately 14% of battery passport technology market revenue in 2025, anchored by export-driven compliance pressure on Chinese battery majors selling into Europe. CATL leads regional adoption through its February 2026 MoU with BMW Group on Catena-X-based cross-border passport pilots. South Korea is advancing through LG Energy Solution and Samsung SDI compliance programs, with country-level CAGR near 17.9%. Japan tracks at 15.8% country CAGR, with Panasonic, GS Yuasa, and Toyota preparing passport architectures for European market access. India is at an earlier adoption stage; Tata Elxsi's January 2025 partnership with Minespider extends battery passport infrastructure into Indian battery manufacturing.

Latin America

Latin America accounted for approximately 2.8% of battery passport technology market revenue in 2025. Brazil leads regional adoption driven by lithium extraction projects in Minas Gerais and growing EV component manufacturing at BYD's Camacari plant. Chile and Argentina contribute through lithium-triangle mining traceability requirements increasingly tied to OEM upstream procurement audits. Regional growth is constrained by limited Tier-1 manufacturing presence and concentration of value-chain activity in raw-material extraction rather than cell or pack production.

Middle East & Africa

Middle East and Africa held approximately 1.8% of battery passport technology market revenue in 2025. The UAE and Saudi Arabia anchor regional demand through Vision 2030 EV manufacturing initiatives, including Lucid Motors' Saudi Arabia plant. The Democratic Republic of Congo, Zambia, and South Africa contribute through cobalt and copper traceability requirements imposed by EU due-diligence rules. Glencore, CMOC, and ERG ReSource platform pilots demonstrated mine-to-cell traceability through Tesla-associated programs in 2023, providing the regional reference architecture for upstream passport-data feeds.

Country Analysis

United States

The United States battery passport technology market reached approximately USD 25 Million in 2025, with country-specific growth tracking near 29.8% CAGR through 2034. Demand is concentrated in Michigan, Ohio, Tennessee, and Nevada battery-manufacturing corridors, with major procurement at Tesla, GM, Ford, and Stellantis Warren plants. The Inflation Reduction Act Section 30D EV tax credit ties eligibility to battery component sourcing thresholds rising to 80% non-foreign-entity-of-concern by 2027, creating a domestic data-traceability mandate parallel to EU Regulation 2023/1542. NIST initiated technical evaluations of battery traceability frameworks in 2024, while the Department of Energy allocated USD 3.5 Billion through the Bipartisan Infrastructure Law to domestic battery cell and component manufacturing, embedding traceability requirements in grant terms.

Germany

Germany's battery passport technology market reached approximately USD 38 Million in 2025, the largest single-country market globally with country CAGR near 26.5% through 2034. Germany leads the Battery Pass consortium under BMWK co-funding, the FIWARE Foundation, and IPCEI Batteries; the BASE project links partners across Spain, Belgium, Lithuania, the Netherlands, and Ireland. DIN DKE SPEC 99100, published 15 January 2025, sets the national technical specification for passport data attributes. Domestic OEMs including BMW, Volkswagen, Mercedes-Benz, and Porsche anchor commercial demand, while battery cell producers Northvolt Drei, Verkor (cross-border), and CATL Thuringia are scaling local data infrastructure.

France

France's battery passport technology market reached approximately USD 13 Million in 2025, with country CAGR near 32.1% through 2034. Stellantis-Renault EV manufacturing and the Verkor gigafactory in Dunkirk anchor commercial demand. Government investments through France 2030 allocate EUR 5.5 Billion to battery-value-chain development including digital traceability components. ACC (Automotive Cells Company), the Stellantis-Mercedes-TotalEnergies joint venture, partnered with Circulor in January 2024 for EV battery materials traceability, providing the largest French commercial deployment to date.

China

China's battery passport technology market reached approximately USD 8 Million in 2025, growing at country CAGR near 18.1% through 2034. Adoption is driven by export compliance pressure rather than domestic mandate, since Chinese cell exports to the EU must carry passports from February 2027. CATL, BYD, and CALB lead implementation, with CATL's February 2026 MoU with BMW Group establishing the largest disclosed China-EU Catena-X cross-border data exchange. The Ministry of Industry and Information Technology has not yet issued a domestic passport mandate equivalent to EU Regulation 2023/1542.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Technology

- Blockchain-Based Battery Passport Solutions

- Cloud-Based Battery Passport Platforms

- Internet of Things (IoT)-Enabled Tracking Technologies

- Artificial Intelligence (AI) and Analytics Solutions

- Digital Twin Technologies

- QR Code and Barcode-Based Identification Systems

- RFID and NFC-Based Traceability Solutions

- Data Management and Integration Platforms

- Lifecycle Assessment and Carbon Footprint Tracking Solutions

- Others

By Battery Type

- Lithium-Ion Batteries

- Lithium Iron Phosphate (LFP) Batteries

- Nickel Manganese Cobalt (NMC) Batteries

- Nickel Cobalt Aluminum (NCA) Batteries

- Solid-State Batteries

- Lead-Acid Batteries

- Nickel-Metal Hydride (NiMH) Batteries

- Sodium-Ion Batteries

- Flow Batteries

- Others

By Industry

- Automotive and Electric Vehicles (EVs)

- Energy Storage Systems (ESS)

- Consumer Electronics

- Industrial Equipment and Machinery

- Aerospace and Defense

- Marine

- Telecommunications

- Healthcare and Medical Devices

- Renewable Energy

- Mining and Raw Material Processing

- Others

By End-User

- Battery Manufacturers

- Automotive OEMs

- Energy Storage System Providers

- Electronics Manufacturers

- Recycling and Second-Life Operators

- Raw Material Suppliers and Miners

- Logistics and Supply Chain Service Providers

- Government and Regulatory Authorities

- Fleet Operators

- Independent Service Providers

- Others

By Business Model

- Software-as-a-Service (SaaS) Platforms

- Subscription-Based Services

- Licensing Models

- Managed Services

- Transaction-Based Models

- Consulting and Integration Services

- Partnership and Consortium-Based Models

- Pay-Per-Use Models

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 0.15 B |

| Forecast Revenue (2034) | USD 1.85 B |

| CAGR (2025-2034) | 32.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology, (Blockchain-Based Battery Passport Solutions, Cloud-Based Battery Passport Platforms, Internet of Things (IoT)-Enabled Tracking Technologies, Artificial Intelligence (AI) and Analytics Solutions, Digital Twin Technologies, QR Code and Barcode-Based Identification Systems, RFID and NFC-Based Traceability Solutions, Data Management and Integration Platforms, Lifecycle Assessment and Carbon Footprint Tracking Solutions, Others), By Battery Type, (Lithium-Ion Batteries, Lithium Iron Phosphate (LFP) Batteries, Nickel Manganese Cobalt (NMC) Batteries, Nickel Cobalt Aluminum (NCA) Batteries, Solid-State Batteries, Lead-Acid Batteries, Nickel-Metal Hydride (NiMH) Batteries, Sodium-Ion Batteries, Flow Batteries, Others), By Industry, (Automotive and Electric Vehicles (EVs), Energy Storage Systems (ESS), Consumer Electronics, Industrial Equipment and Machinery, Aerospace and Defense, Marine, Telecommunications, Healthcare and Medical Devices, Renewable Energy, Mining and Raw Material Processing, Others), By End-User, (Battery Manufacturers, Automotive OEMs, Energy Storage System Providers, Electronics Manufacturers, Recycling and Second-Life Operators, Raw Material Suppliers and Miners, Logistics and Supply Chain Service Providers, Government and Regulatory Authorities, Fleet Operators, Independent Service Providers, Others), By Business Model, (Software-as-a-Service (SaaS) Platforms, Subscription-Based Services, Licensing Models, Managed Services, Transaction-Based Models, Consulting and Integration Services, Partnership and Consortium-Based Models, Pay-Per-Use Models, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CIRCULOR LTD., MINESPIDER GMBH, SIEMENS AG, OPTEL GROUP, CIRCULARISE BV, AVL LIST GMBH, IPOINT-SYSTEMS GMBH, SAP SE, SPHERITY GMBH, TWAICE TECHNOLOGIES GMBH, FIWARE FOUNDATION E.V., TUV RHEINLAND AG, TUV SUD AG, DEKRA SE, BASF SE, GS1 GERMANY GMBH, ROCKWELL AUTOMATION INC., TATA ELXSI LIMITED, GLOBAL BATTERY ALLIANCE, SYSTEMIQ LTD., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Identifier Type (Encrypted QR Codes, RFID Tags, NFC Chips), By Data Type (Carbon Footprint Metrics, ESG Material Sourcing, Recycled Content Disclosures, State-of-Health Analytics) Industry Region & Key Players-Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Identifier Type (Encrypted QR Codes, RFID Tags, NFC Chips), By Data Type (Carbon Footprint Metrics, ESG Material Sourcing, Recycled Content Disclosures, State-of-Health Analytics) Industry Region & Key Players-Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Identifier Type (Encrypted QR Codes, RFID Tags, NFC Chips), By Data Type (Carbon Footprint Metrics, ESG Material Sourcing, Recycled Content Disclosures, State-of-Health Analytics) Industry Region & Key Players-Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Battery Passport Technology Market?

The Global Battery Passport Technology Market was valued at USD 0.11 Billion in 2024 and USD 0.15 Billion in 2025, and is projected to reach USD 1.85 Billion by 2034, growing at a CAGR of 32.1% from 2026 to 2034. Market growth is driven by increasing battery traceability regulations, rising EV adoption, and growing demand for sustainable supply chain transparency.

Who are the major players in the Battery Passport Technology Market?

CIRCULOR LTD., MINESPIDER GMBH, SIEMENS AG, OPTEL GROUP, CIRCULARISE BV, AVL LIST GMBH, IPOINT-SYSTEMS GMBH, SAP SE, SPHERITY GMBH, TWAICE TECHNOLOGIES GMBH, FIWARE FOUNDATION E.V., TUV RHEINLAND AG, TUV SUD AG, DEKRA SE, BASF SE, GS1 GERMANY GMBH, ROCKWELL AUTOMATION INC., TATA ELXSI LIMITED, GLOBAL BATTERY ALLIANCE, SYSTEMIQ LTD., Others

Which segments covered the Battery Passport Technology Market?

By Technology, (Blockchain-Based Battery Passport Solutions, Cloud-Based Battery Passport Platforms, Internet of Things (IoT)-Enabled Tracking Technologies, Artificial Intelligence (AI) and Analytics Solutions, Digital Twin Technologies, QR Code and Barcode-Based Identification Systems, RFID and NFC-Based Traceability Solutions, Data Management and Integration Platforms, Lifecycle Assessment and Carbon Footprint Tracking Solutions, Others), By Battery Type, (Lithium-Ion Batteries, Lithium Iron Phosphate (LFP) Batteries, Nickel Manganese Cobalt (NMC) Batteries, Nickel Cobalt Aluminum (NCA) Batteries, Solid-State Batteries, Lead-Acid Batteries, Nickel-Metal Hydride (NiMH) Batteries, Sodium-Ion Batteries, Flow Batteries, Others), By Industry, (Automotive and Electric Vehicles (EVs), Energy Storage Systems (ESS), Consumer Electronics, Industrial Equipment and Machinery, Aerospace and Defense, Marine, Telecommunications, Healthcare and Medical Devices, Renewable Energy, Mining and Raw Material Processing, Others), By End-User, (Battery Manufacturers, Automotive OEMs, Energy Storage System Providers, Electronics Manufacturers, Recycling and Second-Life Operators, Raw Material Suppliers and Miners, Logistics and Supply Chain Service Providers, Government and Regulatory Authorities, Fleet Operators, Independent Service Providers, Others), By Business Model, (Software-as-a-Service (SaaS) Platforms, Subscription-Based Services, Licensing Models, Managed Services, Transaction-Based Models, Consulting and Integration Services, Partnership and Consortium-Based Models, Pay-Per-Use Models, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Battery Passport Technology Market

Published Date : 16 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date