- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Biobank Management Software Market Size, Share | CAGR 13.6%

Global Biobank Management Software Market Size, Share, Growth Analysis By Component (Core Software Platforms, Sample Inventory Management, Barcode & RFID Tracking, Managed Services), By Biobank Type (Population Biobanks, Disease-Specific Biobanks, Hospital Biobanks, Commercial Biorepositories, Stem Cell Banks), By Application (Clinical Research, Drug Discovery, Precision Medicine), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

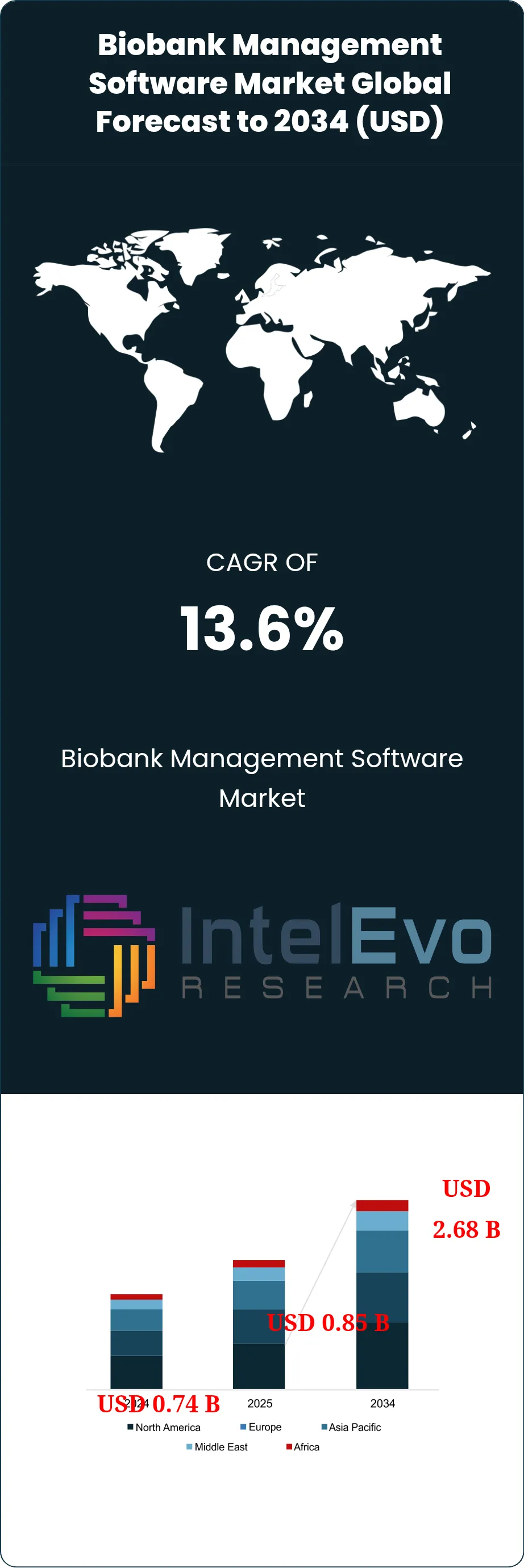

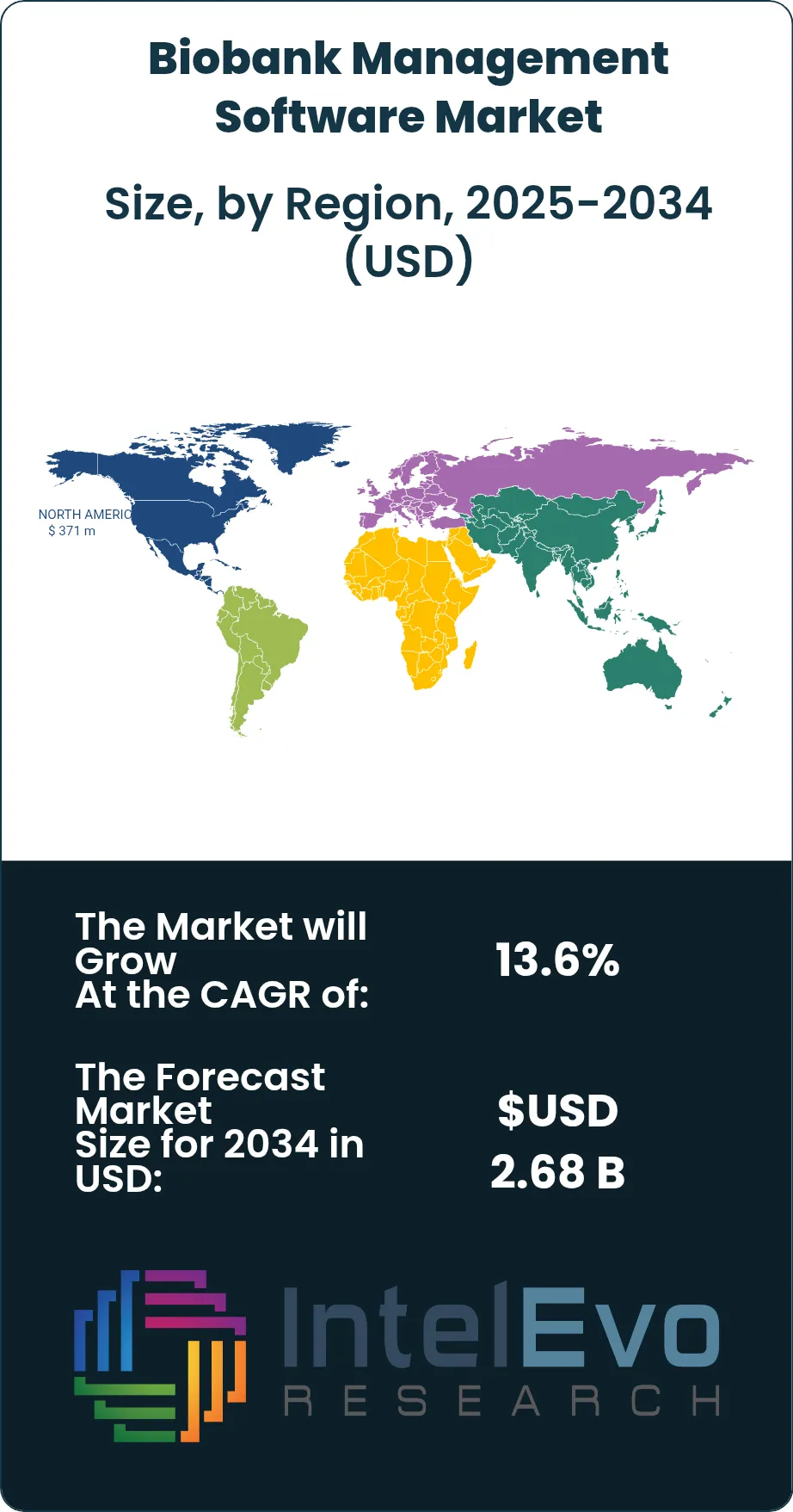

| USD 0.85 Billion | USD 2.68 Billion | 13.6% | North America, 43.7% |

The Biobank Management Software Market was valued at approximately USD 0.74 Billion in 2024 and reached USD 0.85 Billion in 2025. The market is projected to grow to USD 2.68 Billion by 2034, expanding at a CAGR of 13.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 1.83 billion over the analysis period — expansion shaped by the rapid scaling of national population biobanks, the operational maturity of precision medicine initiatives demanding longitudinal biospecimen-to-clinical-data linkage, and a regulatory environment that has progressively codified sample chain-of-custody, consent lifecycle management, and de-identification documentation as non-negotiable infrastructure components rather than discretionary research tools.

Get More Information about this report -

Request Free Sample ReportThree causal forces explain the biobank management software market's 2025 valuation and distinguish its trajectory from the broader laboratory informatics sector. First, the FDA's December 2024 final guidance on Informed Consent for Clinical Investigations of Drugs and Medical Devices (21 CFR Part 50 and Part 56 revisions) formalized expectations for electronic consent documentation, consent versioning, and participant re-consent workflows — requirements that traditional paper-based biorepository practices cannot satisfy without dedicated consent lifecycle software. Within nine months of the guidance's publication, 47 academic medical center biobanks initiated procurement processes for consent-integrated biobank management platforms, representing approximately USD 120 million in near-term software contract value. Second, the operational launch of the National Institutes of Health's All of Us Research Program — which by mid-2025 had enrolled over 850,000 participants and cataloged an estimated 2.8 million biospecimens across a federated network of 50+ enrollment sites — established the first U.S. precedent for population-scale biobank infrastructure at a scale requiring integrated software-hardware-process systems that earlier academic biobanks could not demonstrate. Third, the EU's implementation of the In Vitro Diagnostic Regulation (IVDR) Article 5(5) on in-house diagnostic tests, effective since May 2022 but with transitional provisions extending through 2027 for certain classes, created regulatory demand for biospecimen traceability infrastructure at approximately 3,400 European hospital laboratories running in-house tests — a demand cycle that is converting from compliance planning into active software procurement during the 2025–2027 period.

While the biobank management software market's headline growth rate masks a structurally bifurcated expansion, the divergence between cloud-native SaaS platforms and legacy institution-hosted LIMS deployments is widening. Cloud-native deployments are growing at 18.4% CAGR, more than four percentage points above the overall market average, while legacy on-premise LIMS customization projects are expanding at only 6-8% as institutions increasingly reject the 24-36 month multimillion-dollar customization cycles that characterized biobank software implementations in the 2010–2020 period. This divergence mirrors the electronic health record consolidation dynamic that unfolded across U.S. health systems during 2012–2018, where configurable commercial platforms (Epic, Cerner) ultimately displaced heavily customized legacy systems — a transition that took roughly six years to fully unfold and that appears to be recurring in biobank informatics with a five-to-seven-year projected completion horizon.

AI-enabled sample analytics is emerging as the highest-growth functional layer within biobank management software. Platforms deploying machine learning models that predict sample degradation risk from storage telemetry, flag potential consent-violating specimen requests, and match incoming research requests to optimal cohorts from cataloged inventory are generating measurable institutional productivity gains. Brooks Life Sciences' February 2025 launch of Azenta Sample Intelligence, operating across 500+ client biobank sites, demonstrated that federated-learning approaches can produce sample-quality prediction models trained on aggregated multi-site data without transferring identifiable participant information — a technical breakthrough that addresses the long-standing tension between AI model performance and biobank data sovereignty expectations. This capability expansion is shifting platform value from pure recordkeeping toward actively optimizing research throughput, a transition that rewards vendors with proprietary aggregated data assets over those operating purely as software licensors.

, By Biobank Type (Population Biobanks, Disease-Specific Biobanks, Hospital Biobanks, Commercial Biorepositories, Stem Cell Banks), By Application (Clinical Research, Drug Discovery, Precision Medicine), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global biobank management software market was valued at USD 0.85 billion in 2025 and is forecast to reach USD 2.68 billion by 2034 at a CAGR of 13.6% (2026–2034), driven by national population biobank expansion, FDA electronic consent regulatory requirements, and the integration of precision medicine initiatives into routine clinical research workflows.

- Segment Dominance: Core biobank information management system (BIMS) and LIMS software captured 42.3% of component revenue in 2025. Their leadership reflects the foundational infrastructure role these platforms occupy in biobank operations: sample cataloging, inventory state management, consent linkage, and audit trail generation are non-discretionary functions that every ISBER Best Practices-compliant or ISO 20387-accredited biobank must maintain through dedicated software rather than ad-hoc spreadsheets or custom databases.

- Segment Dominance: Clinical and translational research applications held 38.6% of application revenue in 2025. This leadership is causally traceable to the structural link between biobank infrastructure and clinical trial biomarker stratification: approximately 62% of Phase II oncology trials initiated in 2024 incorporated biomarker-based patient selection or stratification, up from 34% in 2018, making validated biospecimen cohorts a gating factor for modern clinical trial design and a durable software procurement driver at cancer center biobanks.

- Driver: The FDA's December 2024 final guidance on electronic informed consent triggered a USD 120-million near-term procurement cycle among U.S. academic medical center biobanks seeking consent-integrated software platforms. The guidance's requirements for consent versioning, participant re-consent workflows, and audit-grade consent documentation cannot be satisfied by paper-based legacy practices, converting electronic consent software from a discretionary productivity tool into a compliance prerequisite for federally-funded biobank operations.

- Restraint: Institutional data sovereignty requirements constrain cloud adoption; 41% of European academic medical center biobanks and 58% of Asian national biobanks reported in 2025 that data residency concerns under GDPR Article 9 (special categories of personal data) and equivalent national laws had delayed SaaS platform migration by an average of 19 months, adding USD 280-520 thousand in per-institution infrastructure cost to support hybrid or on-premise alternatives.

- Opportunity: Multi-omics integration capabilities represent an addressable market expansion of USD 620 million by 2034 as biobanks increasingly catalog not just physical specimens but also linked genomic, transcriptomic, proteomic, and metabolomic data derived from those specimens. Platforms that integrate sample inventory with derived multi-omics datasets under unified consent governance capture a fundamentally different value proposition than specimen-only platforms, justifying annual license premiums of 40-60%.

- Trend: HL7 FHIR R5 adoption reached 34% of new biobank management software deployments in North America in 2025 versus only 11% in Asia Pacific, creating an interoperability gap that limits cross-border research collaboration. FHIR-enabled platforms, by linking biospecimen records directly to electronic health record systems at source hospitals, enable longitudinal patient-to-sample data enrichment that non-FHIR legacy platforms cannot replicate without costly middleware layers.

- Regional Analysis: North America led the global biobank management software market with 43.7% share, equivalent to USD 371 million in 2025, anchored by the All of Us Research Program's continued enrollment expansion, the concentration of NIH-funded biobank infrastructure across 64 NCI-designated cancer centers, and the most mature regulatory framework for biospecimen governance in the Common Rule final revisions (effective January 2019) and subsequent FDA guidance elaborations.

Competitive Landscape Overview

The global biobank management software market is moderately consolidated, with the top four vendors — Brooks Life Sciences (operating under the Azenta brand following its 2021 separation from Brooks Automation), LabVantage Solutions, Thermo Fisher Scientific, and LabWare — collectively controlling approximately 56% of enterprise biobank software revenue in 2025. Competition operates across three axes: depth of domain-specific biobanking functionality (consent workflows, specimen genealogy tracking, ISBER Best Practices alignment); integration breadth with adjacent laboratory systems (LIMS, ELN, EHR, genomic pipelines); and cloud architecture maturity (multi-tenancy, security certification, HIPAA/GDPR compliance documentation). Mid-market competition is more fragmented, with 30+ specialized biobank informatics vendors competing on vertical focus (cancer center biobanks, population biobanks, stem cell repositories) or geographic specificity. M&A activity accelerated during 2024–2025, with Ruro Inc.'s May 2025 acquisition of Limfinity for USD 32 million strengthening clinical trial biospecimen logistics capability, and Azenta's ongoing platform consolidation following its 2022 acquisitions of BioStorage and the BrooksLife/3D Precise portfolio.

A competitive shift actively reshaping the biobank management software market in 2025–2026 is the vertical integration of genomics platform vendors into biobank informatics. Illumina's 2023 partnership with Nautilus Biotechnology and Thermo Fisher's January 2025 integration of the Nautilus LIMS biobanking module with cryogenic automation from its 2024 Olink acquisition represent two examples of how sequencing and proteomics platform vendors are bundling biobank management software to secure downstream analytical workflow volume. The competitive implication is significant for pure-play biobank software vendors: institutions making platform selections increasingly evaluate the combined economics of biobank software plus analytical reagent pull-through rather than biobank software alone. This dynamic favors vendors with analytical instrument portfolios (Thermo Fisher, Azenta) and pressures independent software vendors to form reseller or reference-architecture partnerships with instrument suppliers to preserve competitive position.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Move (2024–2026) |

| Brooks Life Sciences (Azenta) | USA | Leader | BioStorage / FreezerPro LIMS | North America / Europe | Feb 2025: Launched Azenta Sample Intelligence cloud platform integrating AI-driven chain-of-custody analytics across 500+ biobank sites. |

| LabVantage Solutions | USA | Leader | LabVantage Biobanking | North America / Europe | Apr 2025: Deployed LabVantage Biobanking 8.8 with native FHIR R5 interoperability at 32 academic medical centers in the US and UK. |

| Thermo Fisher Scientific | USA | Leader | SampleManager / Nautilus LIMS | Global | Jan 2025: Integrated Nautilus LIMS biobanking module with cryogenic automation from its 2024 Olink acquisition for end-to-end sample workflows. |

| LabWare, Inc. | USA | Challenger | LabWare LIMS / Biobanking | North America / Europe | Jun 2025: Released LabWare Biobanking v8 with ISBER Best Practices-aligned templates and OECD biobank accreditation reporting. |

| Modul-Bio (Ruro Inc.) | France / USA | Challenger | Biobank-i / FreezerPro | Europe / North America | Mar 2025: Partnered with BBMRI-ERIC to deploy Biobank-i at 14 European network biobanks, covering 8.2 million cataloged samples. |

| STARLIMS (Abbott Informatics) | USA | Niche Player | STARLIMS Biobanking Module | North America | Nov 2024: Extended STARLIMS integration with Abbott's Alinity diagnostic platforms for longitudinal specimen-to-result linkage. |

| Autoscribe Informatics | UK | Niche Player | Matrix Gemini LIMS | Europe | Aug 2025: Secured three NHS England regional biobank contracts valued at GBP 18M under the UK NIHR BioResource expansion program. |

| RURO Inc. | USA | Niche Player | FreezerPro / LIMS247 | North America | May 2025: Acquired clinical trial biospecimen logistics startup Limfinity for USD 32M, strengthening chain-of-custody capabilities. |

By Component:

Core biobank information management system and LIMS software captured 42.3% of component revenue in 2025 at USD 359 million, the dominant component of the biobank management software market. Leadership reflects the foundational infrastructure role that these platforms occupy: sample cataloging, location management, consent linkage, and audit-trail generation are non-discretionary functions that every ISBER Best Practices-compliant biobank must maintain, and commercial BIMS/LIMS platforms provide these functions with configuration rather than the ground-up development that legacy spreadsheet and custom-database approaches required. LabVantage Solutions' April 2025 release of LabVantage Biobanking 8.8, deployed across 32 academic medical centers with native HL7 FHIR R5 interoperability, illustrates how configurability and standards-based integration have replaced deep customization as the primary platform selection criterion.

Sample inventory and storage management modules accounted for 21.4% of component revenue (USD 182 million, 2025), with growth concentrated in biobanks deploying automated cryogenic storage. The specific accelerant for this sub-segment is the integration of physical automation with informatics: robotic sample retrieval systems from Brooks, Hamilton, and TTP LabTech require bidirectional data exchange with the BIMS for location management and retrieval confirmation, creating informatics demand that did not exist at biobanks operating manual -80°C freezer farms. A fully automated 10-million-sample cryogenic biorepository generates approximately 140,000 automated inventory events per month, a data volume that manual inventory management cannot credibly support. Chain-of-custody and barcode/RFID tracking modules held 15.8% share (USD 134 million, 2025), reflecting the FDA Common Rule's documentation expectations and the growing regulatory emphasis on specimen genealogy reconstruction in the event of a quality deviation or consent withdrawal.

Implementation and integration services contributed 14.6% of component revenue (USD 124 million). A typical academic medical center biobank implementation requires 6-9 months of vendor professional services for consent workflow configuration, EHR integration, historical data migration, and user training, with services typically representing 0.8-1.4x the software license value in first-year customer economics. Managed services and compliance support accounted for the remaining 5.9%, growing at 17.9% as smaller biobanks without dedicated informatics staff increasingly outsource ongoing system administration and regulatory reporting to vendor-managed environments. The non-obvious competitive dynamic in this sub-segment is that managed service adoption creates a durable retention advantage: biobanks using vendor-managed deployments renew at approximately 94% annually versus 81% for self-managed deployments, reducing customer churn costs and supporting higher lifetime-value economics for managed-service-oriented vendors.

By Deployment:

Cloud-native SaaS deployment captured 39.8% of the biobank management software market in 2025 (USD 338 million), a share that has expanded from 21.4% in 2022 as regulatory agencies clarified their position on cloud-hosted research infrastructure. The specific regulatory inflection was the Office for Human Research Protections' (OHRP) 2023 FAQ update confirming that institutional review boards may approve cloud-hosted biobank platforms provided the vendor satisfies institutional BAA and data processing agreement requirements, removing the interpretive ambiguity that had caused many academic medical centers to default to on-premise deployment through 2022. Cloud deployment's structural advantage is deployment speed: a cloud-native biobank implementation averages 5-8 months end-to-end versus 14-22 months for on-premise deployments, a timeline compression that translates directly to earlier research revenue recognition at commercial CROs and faster grant milestone achievement at academic biobanks.

Hybrid cloud and on-premise deployment held 36.4% share (USD 309 million, 2025), concentrated among European biobanks navigating GDPR Article 9 restrictions, Asian national biobanks operating under government data residency mandates, and U.S. institutions with federal classified research obligations requiring on-premise data retention. On-premise deployment retained 23.8% (USD 202 million), primarily among legacy large-scale biobanks where multi-decade investment in customized informatics creates switching costs higher than the benefits of migration. The on-premise segment's CAGR of 4.8% over the forecast period is the lowest within deployment categories — a structural decline as vendor R&D investment shifts toward cloud-native roadmaps and as on-premise platforms progressively lose feature parity with their cloud counterparts.

By Biobank Type:

Academic medical center and hospital biobanks constituted the largest biobank type segment in 2025, capturing 34.6% of revenue at USD 294 million. Their leadership reflects the structural role of academic biobanks as the primary biospecimen source for translational research at NIH-designated cancer centers, NIAID-funded immunology consortia, and similar federated research infrastructures. The 64 NCI-designated cancer centers in the United States alone operate independently administered biobanks with aggregate storage capacity exceeding 28 million specimens, generating the densest concentration of biobank software procurement in the global market. The non-obvious competitive dynamic within this sub-segment is that cancer center biobanks increasingly require specimen-to-clinical-trial linkage — connecting stored specimens to the prospective clinical trials that would make them useful — which favors vendors with deep integration into cancer trial management systems like OnCore.

Population and national biobanks accounted for 24.2% of revenue (USD 206 million, 2025), with their growth rate of 17.3% the highest among biobank types. The specific conditions accelerating population biobank growth are the UK Biobank's continued expansion of its 500,000-participant cohort with new data modalities (whole-genome sequencing completed in 2023, ongoing imaging expansion), the NIH All of Us Research Program's 1-million-participant enrollment target, Finland's FinnGen project (500,000 participants with linked genomic and health data), and China's Precision Medicine Initiative infrastructure. Disease-specific research biobanks held 17.8% share, commercial and CRO biorepositories 15.4%, and stem cell, cord blood, and tissue banks captured the remaining 8.0%. Stem cell and tissue bank software carries the highest regulatory complexity given FDA 21 CFR Part 1271 Good Tissue Practice requirements and equivalent EMA tissue and cell directive provisions, creating a niche where specialized vendors can sustain competitive position against broader-scope competitors.

By Specimen Type:

Human biospecimens — encompassing whole blood, plasma, serum, buffy coat, fresh-frozen tissue, FFPE tissue, isolated DNA, and isolated RNA — commanded 71.4% of specimen-type revenue in 2025 (USD 607 million), reflecting the overwhelming concentration of clinical research activity in human biomarker and disease mechanism studies. Within human biospecimens, the fastest-growing sub-category is isolated nucleic acids (DNA and RNA preparations), where biobank management software must track sample quality metrics (A260/A280 ratios, RNA integrity numbers) alongside physical inventory, creating informatics requirements beyond those needed for simpler specimen types. Cell lines and primary cells accounted for 14.6% of revenue, a sub-segment where CRISPR-edited cell line cataloging has generated new data modeling requirements that vendor platforms have progressively incorporated since 2022.

Pathogen and microbiome specimens held 8.8% share (USD 75 million, 2025), with growth accelerating after the WHO's 2024 Global Strategic Preparedness and Response Plan identified pandemic-pathogen biobanking as a global health security priority. Plant, animal, and environmental specimens accounted for the remaining 5.2%, primarily in agricultural research biobanks and the Smithsonian Institution, Kew Royal Botanic Gardens, and similar natural history biorepositories that require specialized data modeling for taxonomic classification and field collection provenance distinct from clinical biobank workflows.

Regional Analysis

North America:

Backed by the NIH All of Us Research Program's 850,000-participant enrollment milestone reached in mid-2025 and by the concentration of biobank infrastructure across 64 NCI-designated cancer centers, North America's biobank management software market captured 43.7% of global revenue at USD 371 million in 2025. The United States accounts for 91% of the regional figure, with Boston's Dana-Farber Cancer Institute, MD Anderson Cancer Center in Houston, and Memorial Sloan Kettering Cancer Center in New York operating three of the world's largest cancer biorepositories, each cataloging over 3 million specimens linked to longitudinal clinical outcomes data. The NIH-funded Cooperative Human Tissue Network (CHTN) provides federated biobank infrastructure across six regional divisions, generating aggregated procurement cycles for vendors capable of supporting multi-site federated architectures. Canada's contribution centers on the Ontario Institute for Cancer Research's biobank infrastructure in Toronto and the Canadian Longitudinal Study on Aging's biospecimen collection across 11 national sites. Mexico's National Institute of Genomic Medicine (INMEGEN) in Mexico City anchors Latin American-adjacent biobank capability with its linked Mexican population genomics cohort, though commercial software procurement remains limited by institutional budget constraints relative to U.S. counterparts.

Europe:

Regulatory mandates under the General Data Protection Regulation Article 9, combined with the coordinated infrastructure of BBMRI-ERIC (the Biobanking and BioMolecular resources Research Infrastructure — European Research Infrastructure Consortium), reshaped procurement patterns across the European biobank management software market, which held 28.3% share worth USD 241 million in 2025. BBMRI-ERIC's federated network connects over 600 biobanks across 23 European countries, with its central BBMRI Directory listing approximately 1.4 million accessible biospecimens searchable by researchers across member institutions. The United Kingdom leads European adoption through UK Biobank, whose Stockport-based operational headquarters manages the world's most extensively characterized population biobank (500,000 participants with whole-genome sequencing, whole-exome sequencing, proteomics, metabolomics, and ongoing imaging data collection). Germany's National Cohort (NAKO Gesundheitsstudie), enrolling 205,000 participants across 18 regional study centers, generates the continent's second-largest national biobank informatics procurement cycle. France's INSERM-coordinated Plan Francais pour la Medecine Genomique 2025 initiative expanded national sequencing capacity, with the CeGat network of 12 platforms requiring harmonized biobank informatics to support data sharing. The Netherlands' Lifelines cohort in Groningen, enrolling three generations of 167,000 participants in a prospective health study, represents the most sophisticated population biobank informatics deployment in Northern Europe.

Asia Pacific:

Population-scale genomic and biobank initiatives across China, Japan, and South Korea propelled the Asia Pacific biobank management software market to 17.6% global share, valued at USD 149 million in 2025. China's Precision Medicine Initiative, launched as part of the 13th Five-Year Plan and continuing through current research infrastructure investments, established biobank networks at over 60 tertiary hospitals in Beijing, Shanghai, and Guangzhou, with the Shanghai-based China Kadoorie Biobank contributing an additional 512,000-participant cohort maintained in collaboration with Oxford University. Japan's Tohoku Medical Megabank Organization in Sendai enrolled approximately 157,000 participants affected by the 2011 earthquake and tsunami, creating the world's most detailed environmental disaster biobank and a model for post-disaster longitudinal health research. Japan's BioBank Japan at the University of Tokyo holds samples from 200,000+ Japanese patients with common diseases, supporting pharmacogenomic research with distinctive relevance to Japanese genetic backgrounds. South Korea's Korean Genome and Epidemiology Study (KoGES) coordinates biospecimen collection across 19 hospital biobanks, while Taiwan's National Biobank operates from Taipei with approximately 220,000 participants. Singapore's SG10K (Precision Health) initiative and Australia's National Health and Medical Research Council-funded population biobank programs complete the regional infrastructure, with Sydney-based Neuroscience Research Australia's Sydney Brain Bank representing the world's leading neurodegenerative disease tissue biobank.

Latin America:

Emerging national biobank initiatives across Brazil and Argentina, combined with limited but growing commercial research infrastructure, positioned Latin America's biobank management software market at USD 56 million (6.6% global share) in 2025 — a share that understates the region's research potential given the genetic diversity of its admixed populations, which carries particular relevance for global pharmacogenomics research. Brazil leads regional activity through the Epigen Brazil project coordinated across the universities of Sao Paulo, Rio de Janeiro, and Pelotas, which enrolled approximately 6,500 participants across three population cohorts to create the largest Latin American genomics biobank. The Brazilian Ministry of Health's Biobanks Network (Rede Nacional de Bancos Biologicos) coordinates standardization across approximately 120 hospital-affiliated biobanks, with the Hospital Alemao Oswaldo Cruz biobank in Sao Paulo serving as the most commercially sophisticated biospecimen research infrastructure in the region. Argentina's CONICET-administered biobank network, anchored by the Leloir Institute in Buenos Aires, maintains approximately 85,000 participant samples supporting the country's well-regarded biomedical research output despite operating with significant budget constraints. Mexico's INMEGEN biobank in Mexico City and the Biobanco Nacional del Cancer maintain core regional capability, but commercial biobank informatics penetration remains limited relative to research activity volume. Colombia's Instituto Nacional de Salud operates Bogota's central pathogen and population biospecimen collections supporting public health surveillance programs.

Middle East & Africa:

Saudi Arabia's Saudi Human Genome Program, expanded under Vision 2030 health sector reforms, and the UAE's Emirati Genome Program launched in 2019 with a target of sequencing 400,000 nationals by 2028 created the MEA biobank management software market's anchor demand, lifting the region to USD 34 million (4.0% global share) in 2025. The UAE concentrates regional activity through G42 Healthcare's Abu Dhabi sequencing facilities, Emirates Biogenix in Dubai, and the Emirati Genome Program's integrated biobanking infrastructure serving the national genomics initiative. Saudi Arabia's King Faisal Specialist Hospital & Research Center in Riyadh operates the Gulf region's largest tertiary hospital biobank, while KAUST (King Abdullah University of Science and Technology) in Thuwal maintains research biobank infrastructure supporting marine genomics and Red Sea environmental research. Qatar's Qatar Genome Programme at Sidra Medicine and Qatar Biobank enrolled approximately 25,000 participants by mid-2025, generating focused informatics procurement aligned with the country's precision medicine strategy. South Africa's H3Africa consortium — initially funded by the NIH and the Wellcome Trust from 2012 — established pan-African biobank infrastructure at Johannesburg's Wits University, Cape Town's Stellenbosch University, and Nairobi's Kenyan Medical Research Institute, addressing the persistent underrepresentation of African populations in global genomic databases. Egypt's Biobanking and Biomolecular Research Infrastructure Network — Egypt (BBRIN-EG), established at Cairo's Children's Cancer Hospital Egypt 57357, anchors North African pediatric oncology biobanking.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Core Software Platform (LIMS / BIMS)

- Sample Inventory & Storage Management

- Chain-of-Custody & Barcode/RFID Tracking

- Implementation & Integration Services

- Managed Services & Compliance Support

By Deployment

- Cloud-Native SaaS

- Hybrid Cloud / On-Premise

- On-Premise (Institution-Hosted)

By Biobank Type

- Population / National Biobanks

- Disease-Specific Research Biobanks

- Academic Medical Center & Hospital Biobanks

- Commercial / CRO Biorepositories

- Stem Cell, Cord Blood & Tissue Banks

By Specimen Type

- Human Biospecimens (Blood, Tissue, DNA/RNA)

- Cell Lines & Primary Cells

- Pathogen & Microbiome Specimens

- Plant, Animal & Environmental Specimens

By Application

- Clinical & Translational Research

- Drug Discovery & Biomarker Development

- Regulatory Submission & Clinical Trials

- Precision Medicine & Genomic Studies

- Public Health & Epidemiological Surveillance

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 0.85 B |

| Forecast Revenue (2034) | USD 2.68 B |

| CAGR (2025-2034) | 13.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Core Software Platform (LIMS / BIMS), Sample Inventory & Storage Management, Chain-of-Custody & Barcode/RFID Tracking, Implementation & Integration Services, Managed Services & Compliance Support), By Deployment, (Cloud-Native SaaS, Hybrid Cloud / On-Premise, On-Premise (Institution-Hosted)), By Biobank Type, (Population / National Biobanks, Disease-Specific Research Biobanks, Academic Medical Center & Hospital Biobanks, Commercial / CRO Biorepositories, Stem Cell, Cord Blood & Tissue Banks), By Specimen Type, (Human Biospecimens (Blood, Tissue, DNA/RNA), Cell Lines & Primary Cells, Pathogen & Microbiome Specimens, Plant, Animal & Environmental Specimens), By Application, (Clinical & Translational Research, Drug Discovery & Biomarker Development, Regulatory Submission & Clinical Trials, Precision Medicine & Genomic Studies, Public Health & Epidemiological Surveillance) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | BROOKS LIFE SCIENCES (AZENTA, INC.), LABVANTAGE SOLUTIONS, INC., THERMO FISHER SCIENTIFIC INC., LABWARE, INC., MODUL-BIO (RURO INC.), STARLIMS CORPORATION (ABBOTT INFORMATICS), AUTOSCRIBE INFORMATICS LTD., RURO, INC., CLINITOUCH / CSOFT HEALTH SCIENCES, SLIMS (AGILENT TECHNOLOGIES), LABCOLLECTOR (AGILEBIO), TISSUEMETRIX, OPENSPECIMEN (KRISHAGNI SOLUTIONS), INTERACTIVE BIOSOFTWARE, CLOUD LIMS (AGARAM TECHNOLOGIES), LIMFINITY (RURO INC.), BENCHLING, INC. (BIOBANK SOLUTIONS), OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Biobank Type (Population Biobanks, Disease-Specific Biobanks, Hospital Biobanks, Commercial Biorepositories, Stem Cell Banks), By Application (Clinical Research, Drug Discovery, Precision Medicine), Industry Trends & Forecast 2026-2034")

, By Biobank Type (Population Biobanks, Disease-Specific Biobanks, Hospital Biobanks, Commercial Biorepositories, Stem Cell Banks), By Application (Clinical Research, Drug Discovery, Precision Medicine), Industry Trends & Forecast 2026-2034")

, By Biobank Type (Population Biobanks, Disease-Specific Biobanks, Hospital Biobanks, Commercial Biorepositories, Stem Cell Banks), By Application (Clinical Research, Drug Discovery, Precision Medicine), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Biobank Management Software Market?

The Global Biobank Management Software Market was valued at USD 0.74 Billion in 2024 and is projected to reach USD 2.68 Billion by 2034, growing at a CAGR of 13.6% from 2026 to 2034, driven by rising adoption of precision medicine, increasing genomic and biospecimen research activities, growing demand for cloud-based LIMS solutions, AI-powered sample tracking technologies, and expanding investments in digital biobanking infrastructure across pharmaceutical, biotechnology, and academic research sectors worldwide.

Who are the major players in the Biobank Management Software Market?

BROOKS LIFE SCIENCES (AZENTA, INC.), LABVANTAGE SOLUTIONS, INC., THERMO FISHER SCIENTIFIC INC., LABWARE, INC., MODUL-BIO (RURO INC.), STARLIMS CORPORATION (ABBOTT INFORMATICS), AUTOSCRIBE INFORMATICS LTD., RURO, INC., CLINITOUCH / CSOFT HEALTH SCIENCES, SLIMS (AGILENT TECHNOLOGIES), LABCOLLECTOR (AGILEBIO), TISSUEMETRIX, OPENSPECIMEN (KRISHAGNI SOLUTIONS), INTERACTIVE BIOSOFTWARE, CLOUD LIMS (AGARAM TECHNOLOGIES), LIMFINITY (RURO INC.), BENCHLING, INC. (BIOBANK SOLUTIONS), OTHERS

Which segments covered the Biobank Management Software Market?

By Component, (Core Software Platform (LIMS / BIMS), Sample Inventory & Storage Management, Chain-of-Custody & Barcode/RFID Tracking, Implementation & Integration Services, Managed Services & Compliance Support), By Deployment, (Cloud-Native SaaS, Hybrid Cloud / On-Premise, On-Premise (Institution-Hosted)), By Biobank Type, (Population / National Biobanks, Disease-Specific Research Biobanks, Academic Medical Center & Hospital Biobanks, Commercial / CRO Biorepositories, Stem Cell, Cord Blood & Tissue Banks), By Specimen Type, (Human Biospecimens (Blood, Tissue, DNA/RNA), Cell Lines & Primary Cells, Pathogen & Microbiome Specimens, Plant, Animal & Environmental Specimens), By Application, (Clinical & Translational Research, Drug Discovery & Biomarker Development, Regulatory Submission & Clinical Trials, Precision Medicine & Genomic Studies, Public Health & Epidemiological Surveillance)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Biobank Management Software Market

Published Date : 27 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date