- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Biobetter Drug Market Size, Share & Forecast | CAGR 8.1%

Global Biobetter Drug Market Size, Share, Growth Analysis By Product Class (Monoclonal Antibodies & Fc-Fusion Proteins, Hormones & Growth Factors, Cytokines & Interferons, Enzymes & Coagulation Factors), By Improvement Strategy (Half-Life Extension, Fc Engineering, Glycoengineering, Pegylation, Device-Led Improvements), By Therapeutic Area, By End User, Industry Trends, Competitive Landscape & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

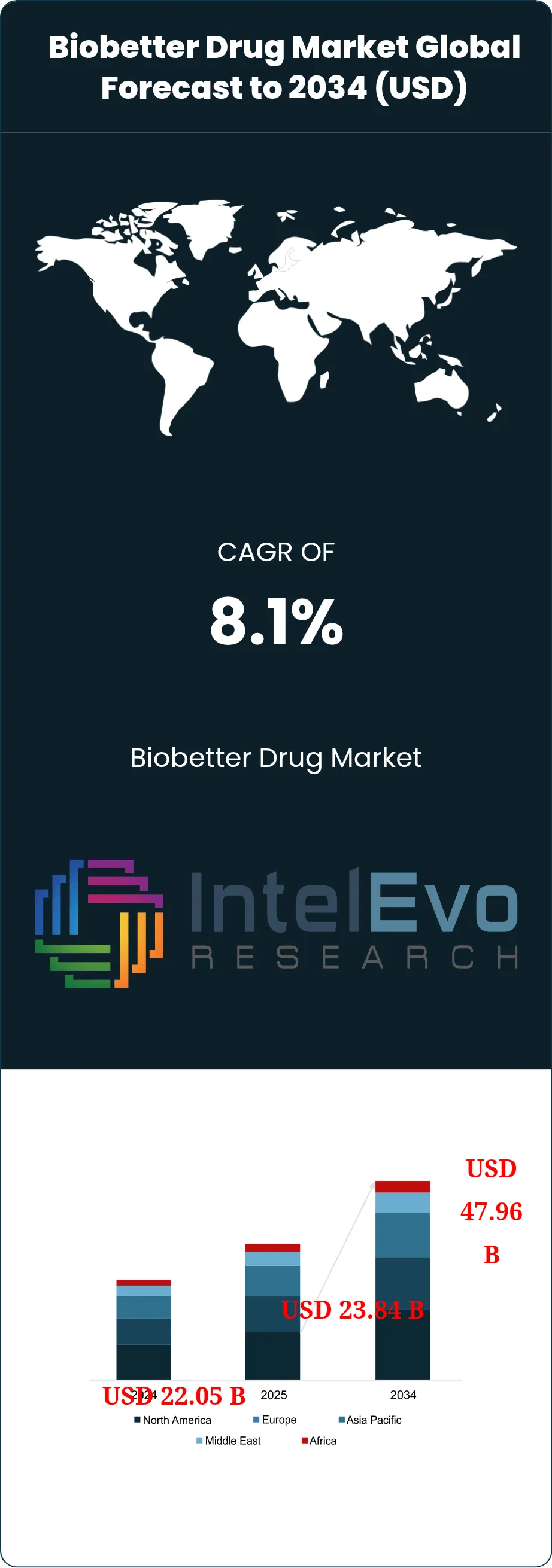

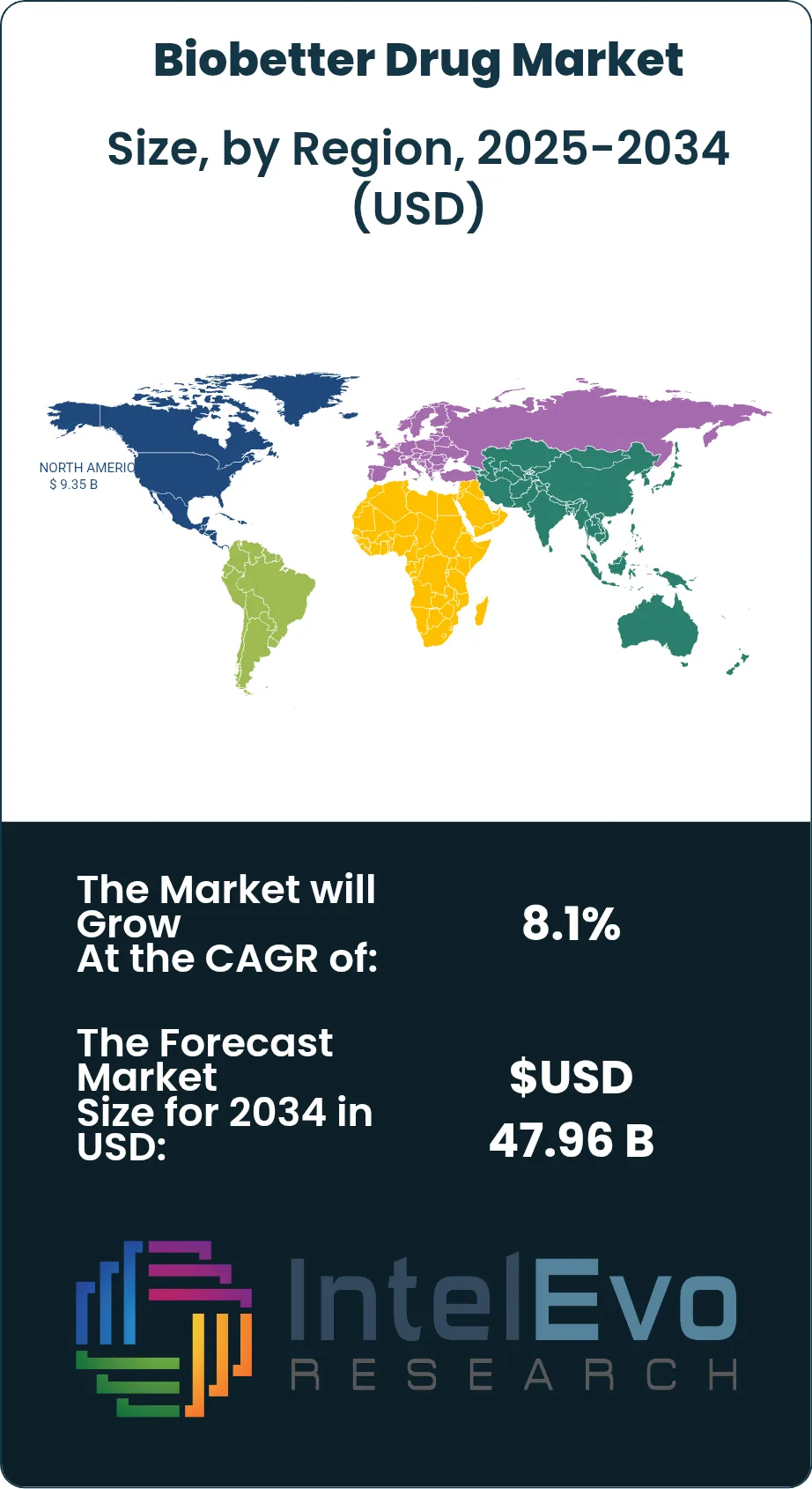

| USD 23.84 Billion | USD 47.96 Billion | 8.1% | North America, 39.2% |

The Biobetter Drug Market was valued at approximately USD 22.05 Billion in 2024 and reached USD 23.84 Billion in 2025. The market is projected to grow to USD 47.96 Billion by 2034, expanding at a CAGR of 8.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 24.12 Billion over the analysis period. The biobetter drug market covers biologics built from validated reference molecules but redesigned to improve half-life, dosing convenience, response durability, safety profile, or site-of-care flexibility. That makes the category distinct from biosimilars, which must stay closely matched to the reference product.

Get More Information about this report -

Request Free Sample ReportThe biobetter drug market is being shaped by two linked forces. Demand is rising because hospitals, payers, and clinicians want biologics that cut chair time, reduce repeat dosing, and shift care toward outpatient and home settings. Supply is rising because many high-value biologics now face loss-of-exclusivity pressure, making lifecycle redesign more attractive. Oncology and immune-mediated disease together accounted for 62.5% of global revenue in 2025 because those areas show the clearest benefit from reduced administration burden.

Regulation remains central. In the United States, true biobetters usually move through the full 351(a) biologics pathway rather than the abbreviated 351(k) route used for biosimilars. In Europe, centralized review through the EMA favors products that can show clear gains in convenience, adherence, and healthcare-resource use. North America led with 39.2% share in 2025, followed by Europe at 28.4%, because reimbursement depth, biologics penetration, and commercial uptake of improved oncology and immunology agents remain strongest in those regions.

Technology is lowering early-stage waste and expanding the menu of viable upgrades. AI-assisted protein design, automated cell-line selection, digital bioprocess monitoring, hyaluronidase-enabled subcutaneous delivery, and smarter injection systems are making route conversion and half-life extension more commercially attractive. Risk still matters. CMC complexity, cold-chain demands, and payer pushback can delay launches by 18 to 30 months. Even so, the market outlook remains favorable because developers are targeting molecules where a faster, longer-acting, or easier-to-administer version can command premium positioning without starting from a new target.

, By Improvement Strategy (Half-Life Extension, Fc Engineering, Glycoengineering, Pegylation, Device-Led Improvements), By Therapeutic Area, By End User, Industry Trends, Competitive Landscape & Forecast 2026-2034")

Key Takeaways

- Market Growth: The biobetter drug market stood at USD 23.84 Billion in 2025 and is projected to reach USD 47.96 Billion by 2034. That implies an 8.1% CAGR across 2026-2034.

- Segment Dominance: Monoclonal antibodies and Fc-fusion proteins led the biobetter drug market by product class with 46.8% share in 2025, equal to about USD 11.16 Billion.

- Segment Dominance: Oncology was the largest application segment in the biobetter drug market with 34.6% share in 2025, or about USD 8.25 Billion.

- Driver: Rapid-use subcutaneous formats are the main growth driver. This bucket represented 24.9% of 2025 revenue as developers targeted shorter administration times and lower clinic burden.

- Restraint: Development complexity remains the largest brake. A global biobetter program typically requires USD 250 Million to USD 450 Million in direct spending and 18 to 30 extra months of work versus a basic biosimilar plan.

- Opportunity: Off-patent biologics that still depend on infusion-heavy care create the largest white-space opportunity. That pool is expected to support about USD 9.80 Billion of cumulative opportunity during 2025-2030.

- Trend: Hyaluronidase-enabled delivery and other fast-injection systems are reshaping the market. Their combined share is expected to rise from 24.9% in 2025 to above 31.0% by 2034.

- Regional Analysis: North America led the biobetter drug market with 39.2% share and about USD 9.35 Billion in 2025.

Competitive Landscape Overview

The biobetter drug market is moderately consolidated. The top four companies accounted for about 38.6% of global revenue in 2025. Competition is technology-led rather than price-led because value depends on administration speed, dose durability, device design, and clinical separation from the reference biologic. Competitive intensity increased through 2025 and early 2026 as subcutaneous conversion deals, denosumab launches, and immunology rollouts widened the addressable pool.

Competitive Landscape Matrix

| Company Name | Headquarters (Country) | Market Position | Key Product/Solution in this market | Geographic Strength | Recent Strategic Move |

| Roche | Switzerland | Leader | Lunsumio VELO / Tecentriq Hybreza | North America and Europe | Won U.S. approval for Lunsumio VELO in Dec 2025, cutting administration time to about one minute |

| Bristol Myers Squibb | United States | Leader | Opdivo Qvantig | North America and Europe | Secured EC approval in May 2025 for subcutaneous Opdivo across multiple solid tumor indications |

| Celltrion | South Korea | Challenger | AVTOZMA SC | North America and Asia Pacific | Launched AVTOZMA SC in the U.S. in Mar 2026 with both IV and SC formats available |

| Biocon Biologics | India | Challenger | Vevzuo / Evfraxy | Asia Pacific and Europe | Gained EC approval in Jul 2025 for denosumab biosimilars covering bone disease and osteoporosis |

| Samsung Bioepis | South Korea | Challenger | PYZCHIVA | North America and Europe | Started U.S. launch of PYZCHIVA in Feb 2025 through Sandoz commercialization |

| Sandoz | Switzerland | Leader | Jubbonti / Wyost | Europe and North America | Launched denosumab biosimilars in Europe in Jan 2025 and in the U.S. in Jun 2025 |

| Fresenius Kabi | Germany | Niche Player | Otulfi / Tyenne | Europe | Expanded U.S. and EU availability of Otulfi in Mar 2025 and continued Tyenne rollout with IV and SC formats |

| Halozyme Therapeutics | United States | Niche Player | ENHANZE | North America | Signed a global collaboration with Takeda in Jan 2026 for vedolizumab with ENHANZE |

| Alteogen | South Korea | Niche Player | ALT-B4 | Asia Pacific | Licensed ALT-B4 to AstraZeneca in Mar 2025 for multiple oncology subcutaneous formulations |

| Amgen | United States | Challenger | Wezlana / BKEMV | North America | Added 2025 U.S. launches of Wezlana and BKEMV to expand its biosimilar base |

By Product Class

The biobetter drug market by product class is led by monoclonal antibodies and Fc-fusion proteins, which held 46.8% share in 2025, equal to USD 11.16 Billion. This class benefits from the depth of reference biology in oncology, immunology, and hematology and from the fact that antibody backbones are well suited to half-life extension, Fc tuning, glycoengineering, and subcutaneous conversion. Hormones and growth factors ranked second with 24.7% share, or USD 5.89 Billion, supported by long-acting erythropoietins, pegylated colony-stimulating factors, and sustained-action endocrine biologics. Cytokines and interferons represented 15.3%, while enzymes and coagulation factors accounted for 8.9%. Other protein formats made up the remaining 4.3%. Revenue concentration therefore favors molecules where an improved product can translate directly into fewer administrations or broader site-of-care use.

By Improvement Strategy

The biobetter drug market by improvement strategy shows where manufacturers are trying to create measurable clinical and commercial separation from the reference molecule. Half-life extension and Fc engineering led with 31.4% share in 2025, or USD 7.49 Billion, because they can reduce dosing frequency and support stronger persistence. Subcutaneous reformulation with absorption-enhancing systems held 24.9%, or USD 5.94 Billion, and is the fastest-growing bucket because it can convert an infusion-centered franchise into a rapid-injection model with visible health-system savings. Glycoengineering and affinity tuning made up 21.7%, while pegylation and other conjugation approaches accounted for 14.1%. Device-led and formulation-led improvements represented the final 7.9%. The mix shows that market leadership now depends on choosing the one upgrade that payers and clinicians can measure quickly.

By Therapeutic Area

The biobetter drug market by therapeutic area remains anchored in oncology, which generated 34.6% of global revenue in 2025, or USD 8.25 Billion. Cancer care leads because infusion burden is high, treatment lines are numerous, and administration savings are easy for providers to value. Autoimmune and inflammatory disorders followed with 27.9% share, or USD 6.65 Billion, supported by rheumatoid arthritis, inflammatory bowel disease, psoriasis, and related conditions where patients favor self-administration and long-term adherence. Metabolic and endocrine disorders held 14.8%, hematology represented 11.7%, and ophthalmology reached 6.2% as aflibercept-type programs broadened. Other indications accounted for 4.8%. Therapeutic leadership is therefore determined by how clearly a product redesign reduces treatment burden and how quickly that benefit converts into reimbursement support.

By End User

The biobetter drug market by end user shows hospital-administered specialty centers still held the largest channel share at 58.6% in 2025, equal to USD 13.97 Billion. These settings remain dominant because many launches begin in oncology infusion centers or tertiary immunology clinics where monitoring, cold-chain handling, and reimbursement workflows are already in place. Specialty clinics represented 24.1%, while specialty pharmacies and home-care channels reached 17.3% and should grow fastest through 2034 as more products support home injection, autoinjector use, and nurse-assisted initiation outside acute care. Products that move safely from hospital chair to clinic room or home treatment generally see better uptake because the benefit is visible to patients, providers, and payers at the same time.

Regional Analysis

North America

The biobetter drug market in North America accounted for 39.2% of global revenue in 2025, equal to about USD 9.35 Billion. The United States represented the vast majority of that demand because biologic spending is high, specialty pharmacy channels are mature, and oncologists and immunologists adopt administration-saving products quickly when reimbursement supports them. Canada adds a smaller but clinically relevant market with strong use of hospital and provincial formularies for biologics. The region also has the deepest base of route-conversion activity in oncology and inflammatory disease, where subcutaneous options reduce chair time and improve site-of-care flexibility.

Europe

The biobetter drug market in Europe held 28.4% share in 2025, or roughly USD 6.77 Billion. Germany, France, the United Kingdom, and Italy are the most important country markets because they combine high biologic use, dense hospital systems, and mature switching frameworks. Europe differs from North America in that healthcare-resource savings are a more visible part of the value case. A product that shortens administration time or lowers nursing burden often gains traction faster than a product that relies only on modest efficacy messaging. That favors biobetters with faster administration, dual-route flexibility, or stronger persistence data.

Asia Pacific

The biobetter drug market in Asia Pacific reached 22.1% of global revenue in 2025, or about USD 5.27 Billion. South Korea, Japan, China, and India form the strategic core of regional activity. South Korea leads on development depth through strong antibody and analytical capabilities. Japan remains attractive because premium biologics still command solid clinical demand. China is becoming more important as manufacturing capacity and trial execution improve, while India combines cost-competitive development with growing domestic use of oncology and endocrinology biologics. Asia Pacific should post the fastest expansion rate among major regions through 2034.

Latin America

The biobetter drug market in Latin America represented 5.8% of global revenue in 2025, or around USD 1.38 Billion. Brazil is the anchor market because it has the largest biologics demand base in the region, established oncology treatment centers, and a public-private mix that can absorb high-value therapies when access terms are clear. Mexico follows through private hospitals and major urban specialty centers, while Argentina provides additional demand in oncology and autoimmune disease despite procurement volatility. The strongest openings are in products that reduce administration cost rather than those priced only on pharmacology claims.

Middle East and Africa

The biobetter drug market in the Middle East and Africa accounted for 4.5% of global revenue in 2025, or about USD 1.07 Billion. The United Arab Emirates, Saudi Arabia, and South Africa are the principal demand centers, while selected Gulf markets act as early adopters for premium oncology and autoimmune biologics. Adoption across the wider region remains constrained by reimbursement fragmentation, cold-chain gaps, and uneven specialist coverage. Even so, products that shorten infusion time or allow less resource-intensive administration are gaining traction because they fit better with capacity-constrained treatment systems.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Class

- Monoclonal Antibodies and Fc-fusion Proteins

- Hormones and Growth Factors

- Cytokines and Interferons

- Enzymes and Coagulation Factors

- Others

By Improvement Strategy

- Half-life Extension and Fc Engineering

- Subcutaneous Reformulation with Absorption Enhancers

- Glycoengineering and Affinity Tuning

- Pegylation and Conjugation

- Device-led and Formulation-led Improvements

By Therapeutic Area

- Oncology

- Autoimmune and Inflammatory Disorders

- Metabolic and Endocrine Disorders

- Hematology

- Ophthalmology

- Others

By End User

- Hospital-administered Specialty Centers

- Specialty Clinics

- Specialty Pharmacies and Home Care

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 23.84 B |

| Forecast Revenue (2034) | USD 47.96 B |

| CAGR (2025-2034) | 8.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Class, (Monoclonal Antibodies and Fc-fusion Proteins, Hormones and Growth Factors, Cytokines and Interferons, Enzymes and Coagulation Factors, Others), By Improvement Strategy, (Half-life Extension and Fc Engineering, Subcutaneous Reformulation with Absorption Enhancers, Glycoengineering and Affinity Tuning, Pegylation and Conjugation, Device-led and Formulation-led Improvements), By Therapeutic Area, (Oncology, Autoimmune and Inflammatory Disorders, Metabolic and Endocrine Disorders, Hematology, Ophthalmology, Others), By End User, (Hospital-administered Specialty Centers, Specialty Clinics, Specialty Pharmacies and Home Care) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ROCHE, BRISTOL MYERS SQUIBB, CELLTRION, BIOCON BIOLOGICS, SAMSUNG BIOEPIS, SANDOZ, FRESENIUS KABI, HALOZYME THERAPEUTICS, ALTEOGEN, AMGEN, COHERUS BIOSCIENCES, DR. REDDY'S LABORATORIES, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Improvement Strategy (Half-Life Extension, Fc Engineering, Glycoengineering, Pegylation, Device-Led Improvements), By Therapeutic Area, By End User, Industry Trends, Competitive Landscape & Forecast 2026-2034")

, By Improvement Strategy (Half-Life Extension, Fc Engineering, Glycoengineering, Pegylation, Device-Led Improvements), By Therapeutic Area, By End User, Industry Trends, Competitive Landscape & Forecast 2026-2034")

, By Improvement Strategy (Half-Life Extension, Fc Engineering, Glycoengineering, Pegylation, Device-Led Improvements), By Therapeutic Area, By End User, Industry Trends, Competitive Landscape & Forecast 2026-2034")

Frequently Asked Questions

How big is the Biobetter Drug Market?

The Global Biobetter Drug Market was valued at USD 22.05 Billion in 2024 and is projected to reach USD 47.96 Billion by 2034, growing at a CAGR of 8.1% from 2026 to 2034, driven by increasing demand for enhanced biologics, longer-lasting therapies, and advancements in protein engineering and drug delivery technologies.

Who are the major players in the Biobetter Drug Market?

ROCHE, BRISTOL MYERS SQUIBB, CELLTRION, BIOCON BIOLOGICS, SAMSUNG BIOEPIS, SANDOZ, FRESENIUS KABI, HALOZYME THERAPEUTICS, ALTEOGEN, AMGEN, COHERUS BIOSCIENCES, DR. REDDY'S LABORATORIES, Others

Which segments covered the Biobetter Drug Market?

By Product Class, (Monoclonal Antibodies and Fc-fusion Proteins, Hormones and Growth Factors, Cytokines and Interferons, Enzymes and Coagulation Factors, Others), By Improvement Strategy, (Half-life Extension and Fc Engineering, Subcutaneous Reformulation with Absorption Enhancers, Glycoengineering and Affinity Tuning, Pegylation and Conjugation, Device-led and Formulation-led Improvements), By Therapeutic Area, (Oncology, Autoimmune and Inflammatory Disorders, Metabolic and Endocrine Disorders, Hematology, Ophthalmology, Others), By End User, (Hospital-administered Specialty Centers, Specialty Clinics, Specialty Pharmacies and Home Care)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date