- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Biofortification Market Size, Share & Forecast | CAGR 9.7%

Global Biofortification Market Size, Share, Growth, Analysis By Crop Type (Cereals, Pulses, Fruits & Vegetables, Oilseeds), By Target Nutrient (Iron, Zinc, Vitamin A, Folate), By Technique (Conventional Breeding, Agronomic, Genetic Engineering, Genome Editing), By Distribution Channel (Direct Sales, Dealers, Cooperatives), By End-User (Farmers, Seed Companies, F&B) Regional Outlook, Key Players – Market Dynamics, Emerging Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 158 Million | USD 365 Million | 9.7% | Asia Pacific, 43.0% |

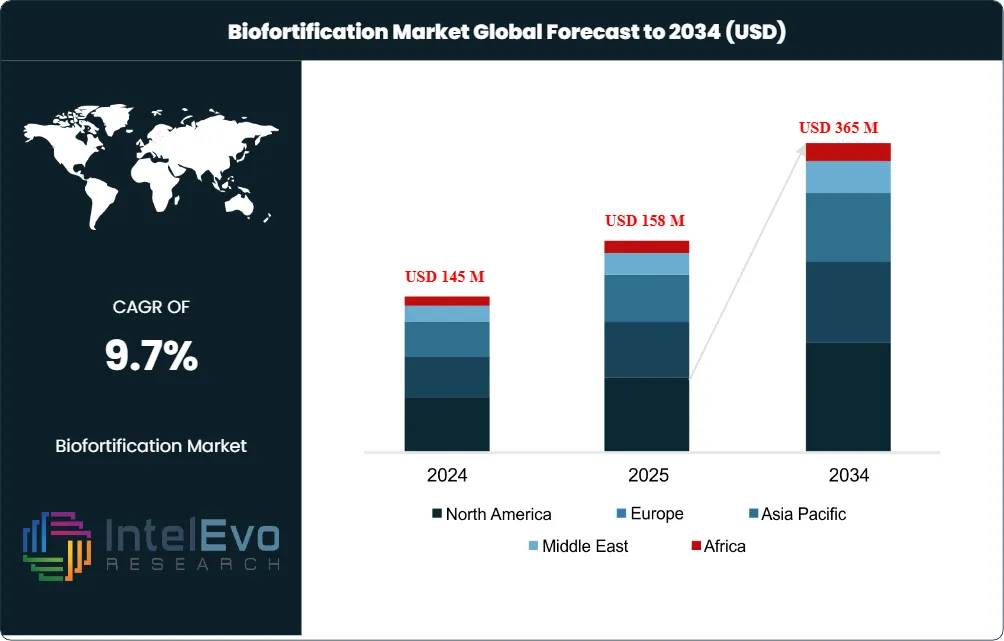

The Biofortification Market was valued at USD 145 Million in 2024 and is estimated to reach USD 158 Million in 2025. The market is projected to attain USD 365 Million by 2034, expanding at a CAGR of 9.7% during the forecast period (2026–2034). This represents an absolute dollar opportunity of USD 207 Million across the analysis window. The market spans nutrient-enhanced staple crop seed production, agronomic biofortification (foliar and soil mineral application), genetic-engineering-based fortification programs, and the broader public-private-partnership infrastructure across HarvestPlus (CGIAR/IFPRI), the Bill & Melinda Gates Foundation, multilateral donor agencies, multinational seed companies, and national agricultural research institutes.

Get More Information about this report -

Request Free Sample ReportCereals and grains led 2025 application revenue at approximately 71% share, anchored by zinc-enriched rice (Bangladesh, India, Philippines), vitamin A maize (Sub-Saharan Africa), zinc-fortified wheat (India, Pakistan, China), and iron-pearl-millet (India, West Africa). Pulses and legumes (iron beans, zinc lentils) captured 14% share, sweet potato (vitamin A orange-fleshed varieties from Uganda, Mozambique, Rwanda) accounted for 8%, and cassava (vitamin A yellow varieties) and other crops the residual 7%. Conventional plant breeding represented approximately 58% of 2025 technique-segmented revenue, agronomic biofortification 22%, and genetic engineering 20% with the highest projected growth rate at 12.2% CAGR through 2034.

Demand growth is anchored by three structural forces. First, hidden hunger reduction: WHO and FAO data attribute approximately 2 Billion people globally to micronutrient deficiencies (iron, zinc, vitamin A, iodine, folate), creating sustained demand for nutrient-dense staple crop alternatives. Second, government and donor procurement: Bangladesh's National School Feeding Program supplies zinc-enriched rice to approximately 14 Million students, anchoring institutional demand. The HarvestPlus NutriHarvest collaboration with Cargill committed USD 3 Million to direct nutrient-enhanced seeds to approximately 119,000 farmers, building private-sector market connections. Third, technology innovation: CRISPR-based gene editing, marker-assisted selection, and CGIAR-led trait pyramiding compress biofortified variety development cycles from 8-12 years toward 3-5 years.

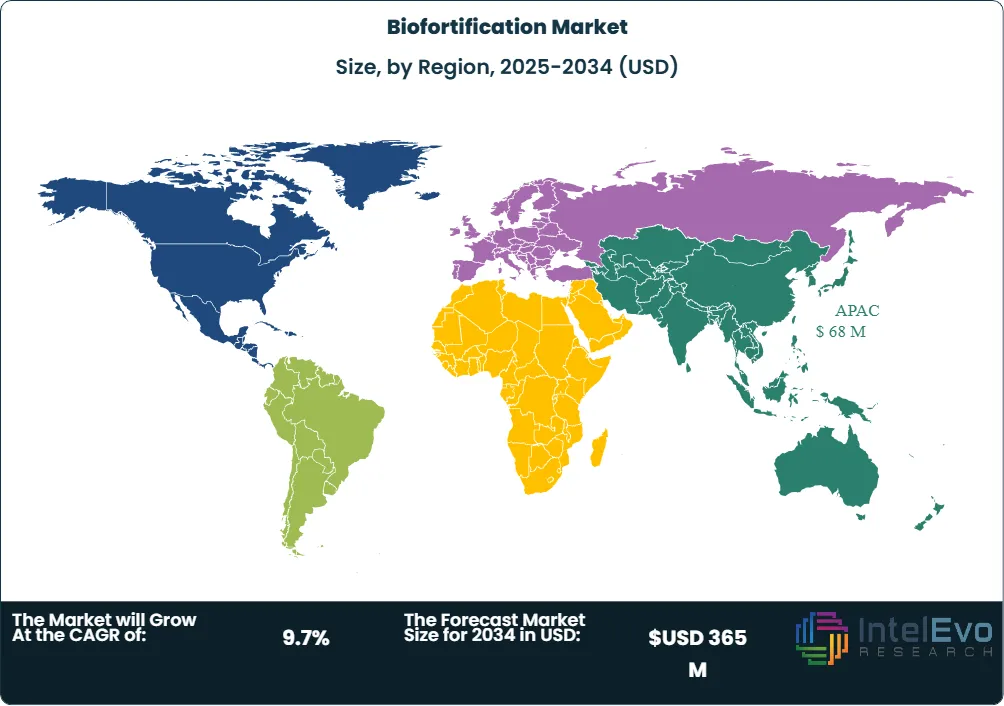

Asia Pacific led the biofortification market with approximately 43.0% share in 2025, anchored by India (HarvestPlus collaboration with IFFCO Kisan, IARI 109-variety release in August 2024), Bangladesh (zinc rice national distribution, school feeding program), Pakistan (zinc wheat), China (iron rice and zinc wheat genomics-based varieties scaling in eastern provinces), and the Philippines (Golden Rice commercial cultivation legalized July 2021). India generated USD 32 Million in 2025 biofortification revenue. Sub-Saharan Africa captured 28.0% share, propelled by HarvestPlus operations in Uganda, Rwanda, Tanzania, Nigeria, and the Democratic Republic of Congo (DRC). Latin America accounted for 12.0%, North America and Europe collectively held 14.0%, and Middle East and other regions covered 3.0%.

Forward to 2034, three structural shifts will define winners: government and nonprofit seed procurement will grow fastest at projected 7.2% CAGR through 2030 according to industry sizing, anchored by national programs scaling beyond pilot phases; CRISPR and gene-editing-based biofortification will outpace conventional breeding through 2034 because of compressed development cycles and trait stacking flexibility; and HarvestPlus's August 2025 Neutral Mark certification framework will scale into a global authentication standard supporting consumer-and-business confidence in biofortified product claims, opening retail-channel premium pricing economics.

Market Definition & Scope

The biofortification market is defined as the development, production, and distribution of staple crops with enhanced nutrient content (vitamins, minerals, amino acids, essential fatty acids, antioxidants) achieved through conventional plant breeding, agronomic biofortification (foliar or soil mineral application during cultivation), or modern biotechnology including genetic engineering, CRISPR/Cas9 gene editing, and marker-assisted selection. The market spans biofortified seed production, agronomic input supply, contract development services, public-private partnership program delivery, and downstream processing of biofortified harvest into end-consumer products.

This analysis includes commercialized and donor-distributed biofortified seed varieties (HarvestPlus iron beans, vitamin A maize, zinc rice, zinc wheat, vitamin A sweet potato, vitamin A cassava, iron pearl millet), seed-and-agronomic-input bundles distributed through public seed systems and private retail networks, biofortified processed food and ingredients (fortified flour, school feeding meals, complementary infant foods), and agronomic input services. Excluded from scope are post-harvest food fortification (industrial flour fortification with synthetic vitamins and minerals), dietary supplements and pills, full-spectrum food fortification of processed foods (covered by the broader USD 116 Billion food fortification market), and pure agricultural biotechnology research services billed separately from biofortified seed sales. The biofortification market is a sub-segment of the broader food and nutrition security market and represented approximately 0.14% of total global food fortification value in 2025.

, By Target Nutrient (Iron, Zinc, Vitamin A, Folate), By Technique (Conventional Breeding, Agronomic, Genetic Engineering, Genome Editing), By Distribution Channel (Direct Sales, Dealers, Cooperatives), By End-User (Farmers, Seed Companies, F&B) Regional Outlook, Key Players – Market Dynamics, Emerging Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The biofortification market expanded from USD 158 Million in 2025 toward a projected USD 365 Million by 2034, registering a 9.7% CAGR.

- Segment Dominance (Crop Type): Cereals and grains captured 71.0% of 2025 biofortification revenue, ahead of pulses and legumes at 14.0% and sweet potato and cassava together at 11.0%.

- Segment Dominance (Nutrient): Iron-fortified varieties held 30.0% of 2025 nutrient-segmented revenue, ahead of zinc at 28.0% and vitamin A at 24.0%.

- Driver: WHO and FAO data attribute approximately 2 Billion people globally to micronutrient deficiencies (hidden hunger), anchoring sustained demand for nutrient-dense staple crops.

- Restraint: Genetic-engineering regulatory hurdles in EU and African Union member states delay Golden Rice and other GM-biofortified variety approvals, capping addressable acreage by an estimated 35%.

- Opportunity: Government and nonprofit seed procurement programs unlock a USD 95 Million incremental opportunity by 2034, supported by national school feeding and food security frameworks.

- Trend: Certified biofortified seed kit sales rose 29% year-over-year in 2025, with bundled iron-enriched beans, zinc maize, and training services achieving 35% higher planting-area uptake within two growing seasons.

- Regional: Asia Pacific led the biofortification market with 43.0% share and USD 68 Million in 2025 revenue, anchored by India, Bangladesh, Pakistan, China, and the Philippines.

Key Insights Summary

- During August 2025, HarvestPlus Solutions (HPS) brought to market the Neutral Mark certification symbol, the first authentication framework guiding consumers and businesses toward verified biofortified products.

- On April 2025, Syngenta took up a U.S. zinc-enriched-wheat startup, broadening its North American biofortification footprint and addressing micronutrient deficiencies through commercial seed channels.

- During April 2025, the Democratic Republic of Congo (DRC) implemented systematic national standards for biofortified crops via collaboration between HarvestPlus and the National Standardization Committee (CNN).

- On August 2024, the Indian Agricultural Research Institute (IARI) brought to market 109 high-yielding, climate-resilient, and biofortified crop varieties spanning 34 field crops and 75 horticultural crops.

- During April 2024, HarvestPlus launched a biofortification initiative in Bangladesh and Uganda supported by The Church of Jesus Christ of Latter-day Saints, distributing iron beans and vitamin A crops to 58,000 smallholder farmers.

- The HarvestPlus NutriHarvest-Cargill collaboration committed USD 3 Million to direct nutrient-enhanced seeds to approximately 119,000 farmers, building private-sector market connections for biofortified produce.

- During January 2025, HarvestPlus launched a large-scale vitamin A maize distribution initiative across Sub-Saharan Africa, broadening nutritional security infrastructure for millions of households.

Competitive Landscape Overview

The biofortification market is moderately concentrated, with the top four players (HarvestPlus, Bayer, Syngenta, Corteva) collectively holding an estimated 58% of 2025 revenue. The structure splits across four lanes: nonprofit-and-public-research institutions (HarvestPlus operating under CGIAR/IFPRI co-leadership, IRRI, ICRISAT, ICAR/IARI, CIAT, ICTA Guatemala) leading variety development; multinational seed-and-biotech incumbents extending biofortified portfolios (Bayer AG, Syngenta Group, Corteva Agriscience, BASF SE, DuPont/IFF, KWS Saat); regional seed companies and parastatal seed enterprises (Mahyco India, IFFCO Kisan, Fedearroz Colombia, Kenya Seed Company, Nigeria's Premier Seed); and donor-and-funder networks (Bill & Melinda Gates Foundation, USAID, FCDO, GIZ, IFAD, World Bank, BMZ Germany).

Competition is restructuring around certification, public-private partnership scaling, and gene-editing technology adoption rather than traditional commercial crop competition. HarvestPlus's August 2025 Neutral Mark certification framework consolidates the authentication infrastructure across global biofortified products. Bayer AG's June 2024 take-up of a U.S. iron-rice biotechnology firm and Syngenta's April 2025 zinc-wheat startup acquisition validate multinational seed-company commitment to nutrient-dense crops. The competitive moat sits in three layers: regulatory approvals across multiple jurisdictions (EFSA, USDA, China NHC, India CSIR, African Union AU-IBAR), distribution-and-extension infrastructure built over 5-10 year farmer relationships, and integration with national school feeding and food security programs.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geographic Strength | Recent Strategic Move |

| HarvestPlus (CGIAR / IFPRI) | United States | Leader | Iron beans, vitamin A maize, zinc rice, zinc wheat | Sub-Saharan Africa, South Asia, Latin America | Released HarvestPlus Solutions Neutral Mark August 2025 |

| Bayer AG | Germany | Leader | Biofortified rice, wheat, and maize seed varieties | Global | Broadened zinc-wheat research with Asian institutes March 2025 |

| Syngenta Group | Switzerland | Leader | Biofortified seed portfolio and breeding programs | Global | Closed take-up of zinc-wheat startup during April 2025 |

| Corteva Agriscience | United States | Leader | Pioneer biofortified hybrid maize and soybean lines | North America, Latin America | Sustained climate-resilient biofortified hybrid expansion 2025 |

| BASF SE | Germany | Challenger | Cassava, corn, and rice biofortification programs | Global | Continued CIAT cassava partnership across 2024-2025 |

| DuPont (IFF) | United States | Challenger | Sorghum and rice biofortification through DuPont Pioneer | North America, Africa | Sustained Africa Harvest sorghum collaboration through 2025 |

| Arcadia Biosciences | United States | Challenger | Wheat biofortification with reduced gluten and high fiber | North America | Continued GoodWheat brand expansion 2024-2025 |

| KWS Saat SE & Co. KGaA | Germany | Challenger | Sugar beet, cereals, and oilseed biofortified lines | Europe | Sustained European biofortified seed portfolio expansion 2025 |

| IRRI (International Rice Research Institute) | Philippines | Niche Player | Golden Rice and zinc rice biofortified varieties | Asia, Africa | Continued Golden Rice cultivation rollout in the Philippines 2024-2025 |

| ICRISAT | India | Niche Player | Pearl millet and sorghum biofortified varieties | Africa, South Asia | Sustained iron-pearl-millet adoption across 2024-2025 |

| Mahyco Pvt. Ltd. | India | Niche Player | Biofortified rice, wheat, and pulses for South Asia | South Asia | Continued IFFCO Kisan-HarvestPlus partnership through 2025 |

| Bill & Melinda Gates Foundation / Funders | United States | Funder | Grant-funded biofortification programs across HarvestPlus | Global | Sustained CGIAR HarvestPlus funding through 2024-2025 |

By Crop Type

Cereals and grains dominated the biofortification market with 71.0% of 2025 crop-type revenue, anchored by zinc rice (Bangladesh, India, Philippines, China), vitamin A maize (Zambia, Nigeria, Tanzania, DRC), zinc wheat (India, Pakistan, Mexico, China), and iron pearl millet (India, West Africa). Pulses and legumes captured 14.0%, propelled by iron beans (Rwanda, DRC, Uganda, Colombia, Honduras) developed by CIAT in partnership with HarvestPlus. Sweet potato accounted for 8.0%, supported by vitamin A orange-fleshed sweet potato (OFSP) varieties from CIP (International Potato Center) deployed across Mozambique, Uganda, Rwanda, Burkina Faso, and Ghana. Cassava captured 4.0%, propelled by vitamin A yellow cassava varieties from IITA (International Institute of Tropical Agriculture) deployed across Nigeria and DRC. Other crops (sorghum, lentils, sweet sorghum, banana) covered the residual 3.0%.

By Target Nutrient

Iron-fortified biofortified varieties represented 30.0% of 2025 target-nutrient revenue, anchored by iron beans, iron pearl millet, and iron-enhanced wheat targeting iron-deficiency anemia affecting approximately 1.6 Billion people globally. Zinc-fortified varieties captured 28.0%, propelled by zinc rice, zinc wheat, and zinc maize addressing zinc deficiency that contributes to childhood stunting and immune dysfunction across South Asia and Sub-Saharan Africa. Vitamin A-fortified varieties accounted for 24.0%, projected to grow fastest at 11.5% CAGR through 2034, supported by vitamin A maize, OFSP sweet potato, vitamin A cassava, and Golden Rice. Multi-nutrient stacked biofortified varieties (combining iron-zinc-vitamin A) captured 8.0%, with the broadest growth potential as breeders pyramid traits. Folate, amino acid, and other targeted nutrients delivered 6.0%, and pro-vitamin and antioxidant biofortification covered the residual 4.0%.

By Technique

Conventional plant breeding represented 58.0% of 2025 technique-segmented biofortification revenue, anchored by HarvestPlus-CGIAR partnerships using marker-assisted selection across rice, wheat, maize, beans, pearl millet, sweet potato, and cassava. Agronomic biofortification (foliar mineral application, zinc and iron soil amendments) captured 22.0%, propelled by zinc-fertilizer adoption across India and Turkey wheat-growing regions. Genetic engineering accounted for 20.0% with the highest projected growth rate at 12.2% CAGR through 2034, supported by Golden Rice (vitamin A), iron-fortified rice (Bayer collaboration with IRRI from August 2020), and emerging CRISPR/Cas9 base-editing programs. Marker-assisted selection cuts breeding cycles by approximately 50% versus traditional breeding, while CRISPR enables targeted single-base substitutions without introducing foreign DNA, addressing GMO regulatory friction in EU and African Union markets.

By Distribution Channel

Government and nonprofit seed procurement represented 42.0% of 2025 distribution-channel biofortification revenue, projected to grow fastest at 7.2% CAGR through 2030 per industry sizing data, anchored by Bangladesh's National School Feeding Program (zinc rice to 14 Million students), India's Public Distribution System pilots, and African school feeding programs across Rwanda, Uganda, and Nigeria. Private retail seed sales captured 28.0%, propelled by IFFCO Kisan-HarvestPlus partnerships in India, Cargill NutriHarvest distribution, and direct-to-farmer commercial channels. Public seed systems accounted for 18.0%, supported by national agricultural research and extension services. Digital agronomy apps and e-commerce captured 8.0% with the highest projected growth rate at 14.5% CAGR through 2034, anchored by India's Krishi platform, China's Pinduoduo agricultural marketplace, and Sub-Saharan African mobile-platform farmer kits. Cooperatives and NGO-bundled kits delivered the residual 4.0%.

By End-User

Smallholder farmers represented 65.0% of 2025 biofortification end-user revenue, anchored by HarvestPlus's targeting of approximately 119,000 farmers (NutriHarvest-Cargill program), 38,000 farmers in Bangladesh, and 20,000 farmers in Uganda within HarvestPlus's 12-month rollout windows. Government agencies (school feeding programs, public distribution systems, agricultural extension services) captured 22.0%, projected to grow fastest at 11.2% CAGR through 2034 driven by national-scale rollouts. Commercial-scale farmers and agribusinesses accounted for 8.0%, supported by Latin American and Asian commercial seed adoption. NGOs and donor-implementing partners captured 5.0%, anchored by Vitamin Angels, Helen Keller International, GAIN, and Global Affairs Canada-funded programs.

Regional Analysis

Asia Pacific led the global biofortification market in 2025 with 43.0% share and USD 68 Million in revenue, anchored by India, Bangladesh, Pakistan, China, and the Philippines. India generated USD 32 Million, supported by IARI's August 2024 release of 109 biofortified crop varieties, the IFFCO Kisan-HarvestPlus partnership extending biofortified pearl millet, wheat, and lentil distribution across food subsidy networks, and ICAR-led research. Bangladesh contributed USD 14 Million through HarvestPlus zinc rice rollout to 38,000 farmers and the National School Feeding Program supplying 14 Million students. China added USD 12 Million via genomics-based zinc rice and selenium wheat scaling in eastern provinces. Pakistan delivered USD 6 Million through zinc wheat adoption, and the Philippines (Golden Rice cultivation legalized July 2021), Vietnam, Indonesia, and other ASEAN markets together accounted for USD 4 Million.

Sub-Saharan Africa accounted for 28.0% of the biofortification market in 2025 with USD 44 Million in revenue. Nigeria led the region with USD 11 Million, propelled by vitamin A cassava and vitamin A maize adoption through IITA-HarvestPlus partnerships. Uganda contributed USD 7 Million, anchored by HarvestPlus iron beans and OFSP sweet potato distribution to 20,000 farmers per 12-month rollout windows. Rwanda added USD 6 Million through iron beans and OFSP scaling. Tanzania, Zambia, and Mozambique together delivered USD 9 Million via vitamin A maize and OFSP programs. The Democratic Republic of Congo (DRC) contributed USD 5 Million through April 2025 national standards implementation in collaboration with HarvestPlus and the National Standardization Committee (CNN). Kenya, Ethiopia, and other markets together accounted for USD 6 Million.

Latin America held 12.0% of the biofortification market in 2025 with USD 19 Million in revenue. Colombia represented USD 6 Million, anchored by Fedearroz BioZn035 zinc rice (Colombia's first biofortified zinc rice introduced October 2021) and CIAT-HarvestPlus iron bean development at the Cali, Valle del Cauca research base. Brazil contributed USD 4 Million via Embrapa-HarvestPlus partnerships covering biofortified rice, beans, and sweet potato. Honduras delivered USD 3 Million through iron bean and OFSP adoption. Guatemala, Bolivia, Peru, Ecuador, and other markets together accounted for USD 6 Million via cooperative-distributed biofortified varieties and donor-funded school feeding programs.

North America accounted for 9.5% of the biofortification market in 2025 with USD 15 Million in revenue. The United States generated USD 13 Million, supported by Corteva Agriscience (Indianapolis), Arcadia Biosciences (Davis, California) GoodWheat brand, Bayer Crop Science U.S. operations (St. Louis), HarvestPlus headquarters operations, and U.S. donor-funder networks including the Bill & Melinda Gates Foundation, USAID Bureau for Resilience and Food Security, and Bureau for Global Health. Canada contributed USD 2 Million through Global Affairs Canada-funded HarvestPlus programs and University of Guelph and University of Saskatchewan biofortification research.

Europe held 4.5% of the biofortification market in 2025 with USD 7 Million in revenue, propelled by KWS Saat (Einbeck, Germany), BASF SE (Ludwigshafen), Bayer Crop Science (Monheim), Syngenta Group (Basel, Switzerland), and donor-led programs through GIZ Germany, FCDO UK, AFD France, and EU Horizon Europe research grants exceeding EUR 35 Million. The Middle East and Africa outside Sub-Saharan Africa together accounted for 3.0% of the market with USD 5 Million in revenue, supported by Egypt, Morocco, Turkey, and Iran biofortified wheat programs and Gulf Cooperation Council food security investments.

Country Analysis

India's biofortification market reached USD 32 Million in 2025 with a 9.6% projected CAGR through 2034, the largest single-country market globally. The country anchors three structural pillars: IARI's August 2024 release of 109 high-yielding, climate-resilient, biofortified crop varieties spanning cereals, millets, forage crops, oilseeds, pulses, sugarcane, cotton, fiber, and 75 horticultural crops; the HarvestPlus-IFFCO Kisan partnership scaling biofortified pearl millet, wheat, and lentil distribution through food subsidy networks; and ICAR (Indian Council of Agricultural Research) infrastructure across 100+ research institutes including IARI, IIRR, IIWBR, and ICAR-IIPR. Government-backed initiatives target iron and zinc deficiencies through fortified cereals and pulses distributed via Public Distribution System pilots.

China's biofortification market reached USD 12 Million in 2025 with a 11.5% projected CAGR through 2034. The country anchors genomics-based zinc rice and selenium wheat scaling in eastern provinces (Jiangsu, Zhejiang, Anhui, Shandong), research institution-led precision-farming protocols for micronutrient uptake, and e-commerce-led iron-rich fortified-staple urban market expansion through JD.com, Alibaba Tmall, and Pinduoduo agricultural marketplaces. Chinese Academy of Agricultural Sciences (CAAS), China National Rice Research Institute (CNRRI), and Beijing Institute of Genomics anchor research, supported by Made in China 2025 advanced agricultural technology pillars and 14th Five-Year Plan agri-tech strategy. Export-oriented production of fortified grains supports Belt and Road agricultural cooperation programs.

Bangladesh's biofortification market reached USD 14 Million in 2025 with a 10.8% projected CAGR through 2034, the second-largest single-country market in Asia Pacific. The country anchors HarvestPlus zinc rice distribution via partnerships with local seed cooperatives and major seed corporations targeting 38,000 farmers within 12-month rollout windows, the National School Feeding Program supplying zinc-enriched rice to approximately 14 Million students, and BARC (Bangladesh Agricultural Research Council)-led variety development. The Bangladesh Rice Research Institute (BRRI) develops domestic biofortified rice lines, with BRRI dhan62, BRRI dhan64, and BRRI dhan72 anchoring zinc-fortified commercial release.

Nigeria's biofortification market reached USD 11 Million in 2025 with a 11.2% projected CAGR through 2034, the largest single-country market in Sub-Saharan Africa. The country anchors vitamin A cassava and vitamin A maize distribution via IITA (International Institute of Tropical Agriculture)-HarvestPlus partnerships across Premier Seed, Maslaha Seeds, and other domestic seed companies, supported by federal government Agricultural Promotion Policy targets. The Bill & Melinda Gates Foundation's continued grant funding (including the 2018 USD 6 Million HarvestPlus-India grant template applied to Nigerian programs) anchors donor-side capital. Adoption tracks IITA Yaba, IAR Zaria, NRCRI Umudike, and other national agricultural research institute releases.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Crop Type

- Cereals

- Pulses

- Fruits & Vegetables

- Oilseeds

- Others

By Target Nutrient

- Iron

- Zinc

- Vitamin A

- Folate

- Others

By Technique

- Conventional Plant Breeding

- Agronomic Biofortification

- Genetic Engineering (GM)

- Genome Editing

By Distribution Channel

- Direct Sales

- Agricultural Input Dealers

- Cooperatives

- Online Channels

By End-User

- Farmers

- Seed Companies

- Food & Beverage Manufacturers

- Government & NGOs

- Research Institutions

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 158 M |

| Forecast Revenue (2034) | USD 365 M |

| CAGR (2025-2034) | 9.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Crop Type, (Cereals, Pulses, Fruits & Vegetables, Oilseeds, Others), By Target Nutrient, (Iron, Zinc, Vitamin A, Folate, Others), By Technique, (Conventional Plant Breeding, Agronomic Biofortification, Genetic Engineering (GM), Genome Editing), By Distribution Channel, (Direct Sales, Agricultural Input Dealers, Cooperatives, Online Channels), By End-User, (Farmers, Seed Companies, Food & Beverage Manufacturers, Government & NGOs, Research Institutions), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | HARVESTPLUS (CGIAR / IFPRI), BAYER AG, SYNGENTA GROUP, CORTEVA AGRISCIENCE, BASF SE, DUPONT / INTERNATIONAL FLAVORS & FRAGRANCES (IFF), ARCADIA BIOSCIENCES, INC., KWS SAAT SE & CO. KGAA, INTERNATIONAL RICE RESEARCH INSTITUTE (IRRI), ICRISAT, MAHYCO PVT. LTD., INTERNATIONAL CENTER FOR TROPICAL AGRICULTURE (CIAT), INTERNATIONAL POTATO CENTER (CIP), INTERNATIONAL INSTITUTE OF TROPICAL AGRICULTURE (IITA), INDIAN COUNCIL OF AGRICULTURAL RESEARCH (ICAR), INDIAN AGRICULTURAL RESEARCH INSTITUTE (IARI), BANGLADESH RICE RESEARCH INSTITUTE (BRRI), BANGLADESH AGRICULTURAL RESEARCH COUNCIL (BARC), FEDEARROZ, EMBRAPA, VITAMIN ANGELS, HELEN KELLER INTERNATIONAL, GLOBAL ALLIANCE FOR IMPROVED NUTRITION (GAIN), AFRICA HARVEST BIOTECH FOUNDATION INTERNATIONAL, EVOGENE LTD., INTREXON CORPORATION, OKANAGAN SPECIALTY FRUITS INC., ARBORGEN INC., BILL & MELINDA GATES FOUNDATION, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Target Nutrient (Iron, Zinc, Vitamin A, Folate), By Technique (Conventional Breeding, Agronomic, Genetic Engineering, Genome Editing), By Distribution Channel (Direct Sales, Dealers, Cooperatives), By End-User (Farmers, Seed Companies, F&B) Regional Outlook, Key Players – Market Dynamics, Emerging Trends & Forecast 2026-2034")

, By Target Nutrient (Iron, Zinc, Vitamin A, Folate), By Technique (Conventional Breeding, Agronomic, Genetic Engineering, Genome Editing), By Distribution Channel (Direct Sales, Dealers, Cooperatives), By End-User (Farmers, Seed Companies, F&B) Regional Outlook, Key Players – Market Dynamics, Emerging Trends & Forecast 2026-2034")

, By Target Nutrient (Iron, Zinc, Vitamin A, Folate), By Technique (Conventional Breeding, Agronomic, Genetic Engineering, Genome Editing), By Distribution Channel (Direct Sales, Dealers, Cooperatives), By End-User (Farmers, Seed Companies, F&B) Regional Outlook, Key Players – Market Dynamics, Emerging Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Biofortification Market?

Global Biofortification Market was valued at USD 145 million in 2024 and is projected to reach USD 365 million by 2034, growing at a CAGR of 9.7% (2026–2034).

Who are the major players in the Biofortification Market?

HARVESTPLUS (CGIAR / IFPRI), BAYER AG, SYNGENTA GROUP, CORTEVA AGRISCIENCE, BASF SE, DUPONT / INTERNATIONAL FLAVORS & FRAGRANCES (IFF), ARCADIA BIOSCIENCES, INC., KWS SAAT SE & CO. KGAA, INTERNATIONAL RICE RESEARCH INSTITUTE (IRRI), ICRISAT, MAHYCO PVT. LTD., INTERNATIONAL CENTER FOR TROPICAL AGRICULTURE (CIAT), INTERNATIONAL POTATO CENTER (CIP), INTERNATIONAL INSTITUTE OF TROPICAL AGRICULTURE (IITA), INDIAN COUNCIL OF AGRICULTURAL RESEARCH (ICAR), INDIAN AGRICULTURAL RESEARCH INSTITUTE (IARI), BANGLADESH RICE RESEARCH INSTITUTE (BRRI), BANGLADESH AGRICULTURAL RESEARCH COUNCIL (BARC), FEDEARROZ, EMBRAPA, VITAMIN ANGELS, HELEN KELLER INTERNATIONAL, GLOBAL ALLIANCE FOR IMPROVED NUTRITION (GAIN), AFRICA HARVEST BIOTECH FOUNDATION INTERNATIONAL, EVOGENE LTD., INTREXON CORPORATION, OKANAGAN SPECIALTY FRUITS INC., ARBORGEN INC., BILL & MELINDA GATES FOUNDATION, Others

Which segments covered the Biofortification Market?

By Crop Type, (Cereals, Pulses, Fruits & Vegetables, Oilseeds, Others), By Target Nutrient, (Iron, Zinc, Vitamin A, Folate, Others), By Technique, (Conventional Plant Breeding, Agronomic Biofortification, Genetic Engineering (GM), Genome Editing), By Distribution Channel, (Direct Sales, Agricultural Input Dealers, Cooperatives, Online Channels), By End-User, (Farmers, Seed Companies, Food & Beverage Manufacturers, Government & NGOs, Research Institutions),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date