- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Biological Crop Protection Market Size & Forecast 2034| CAGR 11.9%

Global Biological Crop Protection Market Size, Share, Growth & Industry Analysis By Product Type (Microbial Biopesticides, Biochemical Biopesticides, Semiochemicals & Pheromones, Beneficial Macro-Organisms, RNAi-Based Products), By Crop Type (Fruits & Vegetables, Cereals & Grains, Oilseeds & Pulses, Turf & Ornamentals, Plantation Crops), By Mode of Action (Biofungicides, Bioinsecticides, Bionematicides, Bioherbicides) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

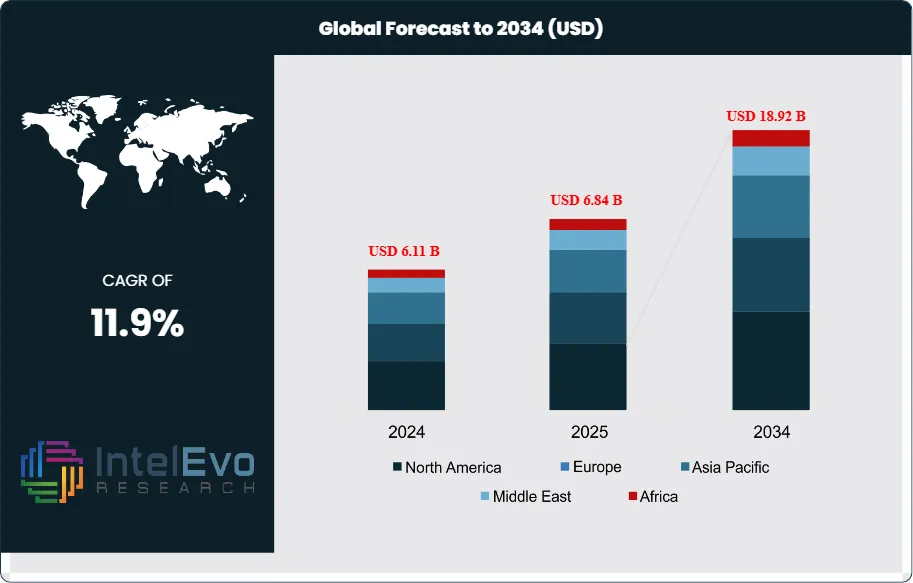

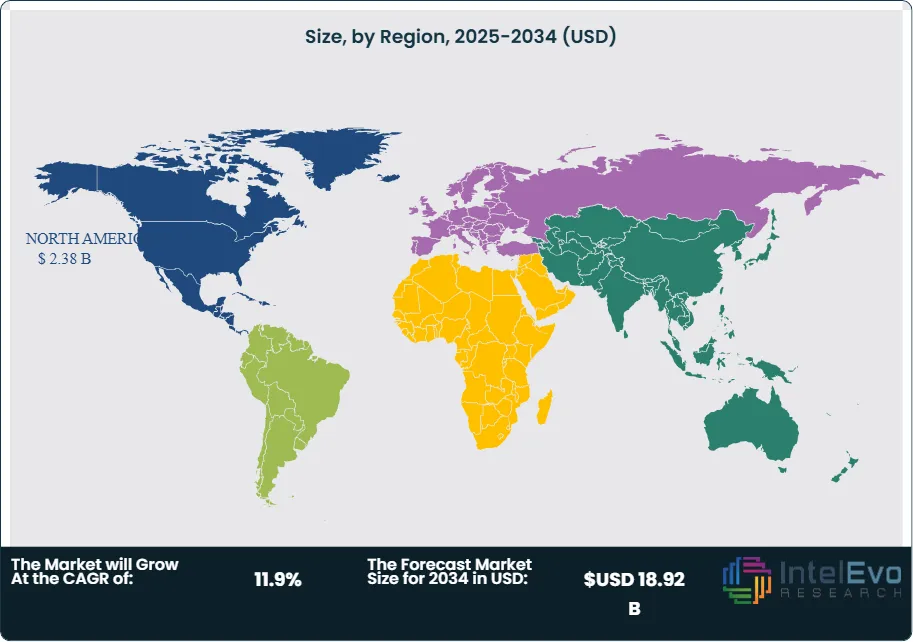

| USD 6.84 Billion | USD 18.92 Billion | 11.9% | North America, 34.8% |

The Biological Crop Protection Market was valued at approximately USD 6.11 Billion in 2024 and reached USD 6.84 Billion in 2025. The market is projected to grow to USD 18.92 Billion by 2034, expanding at a CAGR of 11.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 12.08 Billion over the analysis period, driven by accelerating regulatory restriction of synthetic chemical pesticides, surging demand for certified organic and residue-free produce, and the commercial maturation of microbial biocontrol, biopesticide, and RNAi-based crop protection technologies.

Get More Information about this report -

Request Free Sample ReportThe biological crop protection market encompasses microbial biopesticides, biochemical biopesticides, semiochemicals and pheromones, plant-incorporated protectants, and beneficial macro-organisms used to manage insect pests, plant pathogens, nematodes, and weeds in agricultural production systems. These products operate through naturally occurring mechanisms including competitive exclusion, induced systemic resistance, parasitism, predation, and disruption of pest reproductive cycles, providing pest and disease management efficacy without the environmental persistence, non-target toxicity, or consumer residue concerns associated with synthetic chemical pesticides. As of 2025, biological crop protection products represent approximately 5.8% of the total global crop protection market, up from 3.2% in 2018, reflecting consistent share gains against the broader synthetic pesticide sector.

Several interconnected regulatory and market forces are accelerating biological crop protection market growth. The European Union's Farm to Fork Strategy targets a 50% reduction in chemical pesticide use by 2030, directly mandating increased adoption of biological alternatives across EU member state agricultural systems. The US EPA's registration review process has revoked or restricted more than 120 synthetic active ingredient registrations since 2020 under the Federal Insecticide, Fungicide, and Rodenticide Act (FIFRA), creating formulation gaps that biological alternatives are positioned to fill. In Brazil, MAPA's Agrofit database reflects a 34% increase in registered biological crop protection products between 2020 and 2025, and Brazil's government offers accelerated registration pathways for biologicals, reducing approval timelines from 36 months to 6-12 months for low-risk microbial active ingredients. The Chinese Ministry of Agriculture and Rural Affairs has similarly launched initiatives to reduce chemical pesticide use by 30% by 2035, stimulating domestic biological product development and adoption.

Large agrochemical companies including BASF, Bayer, Syngenta, and Corteva have accelerated biological portfolio expansion through acquisitions, partnerships, and internal R&D investment, collectively committing over USD 2.5 Billion to biological crop protection development since 2020. North America led the biological crop protection market with a 34.8% share in 2025, equivalent to USD 2.38 Billion. Latin America is the fastest-growing region, advancing at a projected CAGR of 14.8% through 2034, driven by Brazil's large-scale soybean and sugarcane production systems and government support for biological input adoption. AI-assisted screening of microbial libraries for bioactive compounds is compressing bioactive discovery timelines from years to months, further strengthening the biological crop protection product pipeline.

, By Crop Type (Fruits & Vegetables, Cereals & Grains, Oilseeds & Pulses, Turf & Ornamentals, Plantation Crops), By Mode of Action (Biofungicides, Bioinsecticides, Bionematicides, Bioherbicides) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global biological crop protection market was valued at USD 6.84 Billion in 2025 and is forecast to reach USD 18.92 Billion by 2034, registering a CAGR of 11.9% during the 2026-2034 forecast period.

- Segment Dominance: By product type, microbial biopesticides held the largest share at 46.3% of the biological crop protection market in 2025, led by Bacillus-based fungicides and insecticides that provide broad-spectrum crop protection with favorable regulatory profiles across all major agricultural markets.

- Segment Dominance: By crop type, fruits and vegetables accounted for 38.7% of the biological crop protection market in 2025, driven by strict MRL (Maximum Residue Limit) enforcement, premium fresh produce buyer specifications, and organic certification requirements that favor biological over synthetic inputs.

- Driver: The EU Farm to Fork Strategy's mandate to reduce chemical pesticide use by 50% by 2030 is compelling European growers and retailers to shift input budgets toward biological alternatives, accelerating biological crop protection market share gains in the EU's USD 18 Billion crop protection market.

- Restraint: Inconsistent field efficacy of biological crop protection products under variable temperature, humidity, and UV exposure conditions constrains adoption, with an estimated 28% of first-time biological product users in Latin America and Asia Pacific reporting unsatisfactory pest control outcomes due to improper application timing and storage.

- Opportunity: The emerging RNAi-based biopesticide segment, with the first commercial RNA-based insecticide registered by the EPA in 2023 and a global RNAi biopesticide pipeline exceeding 40 development programs in 2025, represents an addressable market opportunity estimated at USD 1.8 Billion by 2034.

- Trend: Adoption of precision application systems including drone-based biological product delivery grew at approximately 22.6% annually in 2025, improving field efficacy of biological products by ensuring optimal canopy penetration and reducing UV-induced degradation of microbial active ingredients post-application.

- Regional Analysis: North America led the biological crop protection market with a 34.8% share, equivalent to USD 2.38 Billion in 2025, supported by EPA registration pathways for minimum-risk biopesticides under FIFRA Section 25(b) and strong organic produce sector demand in California, the Pacific Northwest, and the Great Lakes vegetable belt.

Competitive Landscape Overview

The biological crop protection market is moderately fragmented, with the top four companies — BASF, Bayer, Syngenta, and Corteva — collectively accounting for approximately 41% of global revenues in 2025. Despite large company entry, the market retains meaningful participation from specialist biological companies including Koppert, Biobest, Marrone Bio Innovations, and AgBiome, which compete on application expertise, greenhouse crop specialization, and speed of new microbial active ingredient commercialization. M&A activity has intensified, with over 35 biological crop protection acquisition transactions recorded between 2022 and 2025 as large agrochemical companies accelerate portfolio building through acquisition rather than internal development. New entrants from the synthetic biology and fermentation technology sectors are increasing competitive pressure on established formulators.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| BASF SE | Germany | Leader | Serenade & Velondis Bioinsecticide Portfolio | Europe & North America | Acquired a biologicals startup expanding its microbial fungicide pipeline; Q1 2025. |

| Bayer AG | Germany | Leader | Serenade ASO & Votivo Biological Suite | Europe & North America | Launched expanded Votivo II nematicide-biostimulant combination for corn and soybean; March 2025. |

| Syngenta Group | Switzerland | Leader | Taegro Biofungicide & Actellic Bioinsecticides | Global | Expanded biological crop protection portfolio in Brazil through partnership with local microbial formulator; Q2 2025. |

| Corteva Agriscience | USA | Leader | Isoclast & Utrisha N Biological Nitrogen Fixation | North America & Latin America | Signed agreement with a UK microbial biocontrol company to expand its bio-nematicide pipeline; Jan 2025. |

| Marrone Bio Innovations (AMVAC) | USA | Challenger | Regalia Biofungicide & Grandevo Bioinsecticide | North America | Expanded distribution of Grandevo bioinsecticide to five new Latin American markets; 2025. |

| Koppert Biological Systems | Netherlands | Challenger | Mycotal & Trianum Biocontrol Products | Europe & Asia Pacific | Launched Trianum Shield biofungicide for high-value vegetable crops in Southeast Asia; Q3 2025. |

| Biobest Group | Belgium | Challenger | Biocontrol Agent Portfolio for Greenhouse Crops | Europe | Completed acquisition of a Spanish biological crop protection company to expand Mediterranean market; 2025. |

| Novozymes (Novonesis) | Denmark | Niche Player | Taegro & JumpStart Microbial Solutions | Europe & North America | Expanded JumpStart rhizobial inoculant line for pulse crops in Canada and Australia; Jan 2026. |

| Certis Biologicals | USA | Niche Player | Regalia CG & BoteGHA Biofungicides | North America | Launched BoteGHA ES bioinsecticide targeting specialty crop whitefly and thrips in California; 2025. |

| AgBiome Inc. | USA | Niche Player | Howler & Venerate CG Biological Products | North America | Entered commercialization partnership for Howler biofungicide expansion into Mexican avocado production; 2025. |

By Product Type

The biological crop protection market by product type spans microbial biopesticides, biochemical biopesticides, semiochemicals and pheromones, beneficial macro-organisms, and plant-incorporated protectants. Microbial biopesticides held the dominant share at 46.3% of the biological crop protection market in 2025, equivalent to approximately USD 3.17 Billion. This segment includes bacterial bioinsecticides and biofungicides based on Bacillus thuringiensis, Bacillus subtilis, and Bacillus amyloliquefaciens; fungal bioinsecticides based on Beauveria bassiana and Metarhizium anisopliae; mycoparasitic biofungicides including Trichoderma species; and microbial bionematicides including Purpureocillium lilacinum. Bacillus-based products dominate within the microbial segment because of their broad-spectrum activity, heat-stable spore formulations with 18-24 month shelf life, and compatibility with conventional integrated pest management spray programs. BASF's Serenade biofungicide and Bayer's Votivo bionematicide are the highest-revenue individual microbial products in their respective categories.

Biochemical biopesticides, which include plant extracts, essential oils, fatty acid derivatives, and naturally derived repellents and pesticides, represented 22.6% of the biological crop protection market in 2025 and serve primarily as adjuncts to microbial programs in high-value specialty crops. Semiochemicals and pheromone systems, used for mating disruption of lepidopteran and coleopteran pest species, held 16.4% of the market in 2025, with adoption concentrated in wine grapes, apple orchards, and almonds in California, Europe, and Chile. Beneficial macro-organisms including predatory mites, parasitic wasps, and insect predators for greenhouse biocontrol accounted for 10.8% of the biological crop protection market in 2025. Plant-incorporated protectants (PIPs) and RNAi-based active ingredients collectively represented the remaining 3.9% of the biological crop protection market by product type in 2025 but represent the highest-growth sub-segment.

By Crop Type

The biological crop protection market by crop type reveals fruits and vegetables as the primary revenue segment, accounting for 38.7% of total revenues in 2025, equivalent to approximately USD 2.65 Billion. High-value specialty crops operate under strict supermarket supplier codes and organic certification requirements that impose MRL (Maximum Residue Limit) compliance far more stringent than statutory minimums, effectively mandating biological crop protection integration across many fruit and vegetable production systems in California, the Netherlands, Spain, and Chile. Tomatoes, strawberries, bell peppers, cucumbers, and lettuce together represent the highest-volume vegetable applications for biological products, while grapes, apples, citrus, and avocados lead in tree fruit and vine applications. Greenhouse vegetable and ornamental producers represent a particularly concentrated demand segment, as the enclosed growing environment supports consistent efficacy of biological products while limiting UV degradation of microbial active ingredients.

Cereals and grains represented 24.3% of the biological crop protection market in 2025. Wheat, corn, and rice are the primary targets, with biological seed treatments containing rhizobial inoculants, Trichoderma biofungicides, and Bacillus-based root inoculants gaining adoption for soil-borne disease management. Oilseeds and pulses accounted for 18.6% of the market in 2025, driven by soybean production in Brazil, Argentina, and the United States where biological nitrogen fixation inoculants and biological nematode management programs serve large commercial farming operations. Turf, ornamentals, and other non-food applications held 10.8% of the biological crop protection market in 2025. Plantation crops including coffee, cocoa, palm oil, and sugarcane represented 7.6% of the market, with growing biological product adoption driven by sustainability certification requirements from buyers including Rainforest Alliance and Bonsucro.

By Mode of Action

The biological crop protection market by mode of action covers bioinsecticides, biofungicides, bionematicides, bioherbicides, and bioviricides. Biofungicides held the largest mode-of-action segment at 38.2% of the biological crop protection market in 2025, equivalent to approximately USD 2.61 Billion. Plant-pathogenic fungi and bacteria cause estimated global crop losses of USD 200-250 Billion annually, creating the largest addressable market for biological management among all pest categories. Bacillus-based biofungicides targeting Botrytis, Powdery Mildew, Alternaria, and Fusarium species are the volume leaders, while Trichoderma-based products dominate soil-borne pathogen management. Bioinsecticides represented 32.4% of the biological crop protection market in 2025, with Bacillus thuringiensis products and fungal entomopathogenic species serving both conventional and organic production systems across multiple crop categories.

Bionematicides held a 16.8% share of the biological crop protection market in 2025, serving a pest management segment with particularly limited synthetic options following the withdrawal of methyl bromide and multiple organophosphate nematicides under international conventions and national regulatory review processes. The bionematicide segment is growing at approximately 14.6% annually, the fastest growth rate among all biological crop protection mode-of-action segments, as growers in vegetable, citrus, and ornamental production seek viable nematode management tools. Bioherbicides, which remain technically challenging due to the demanding weed control efficacy expectations of growers accustomed to synthetic herbicides, held 8.4% of the biological crop protection market in 2025. Bioviricides and other specialty biological pest management tools accounted for the remaining 4.2%.

By Formulation

The biological crop protection market by formulation type covers wettable powders, liquid formulations, granules, and seed treatment formulations. Wettable powder and dry granule formulations held the largest combined share at 42.6% of the biological crop protection market in 2025, favored for their superior shelf stability — particularly important for spore-based microbial active ingredients that require viability maintenance across distribution and storage. Liquid suspension concentrate and oil dispersion formulations held a 34.8% share in 2025, preferred by growers for ease of spray tank mixing and compatibility with precision application equipment. Seed treatment formulations, which deliver biological active ingredients directly to the seed surface for protection during germination and early plant establishment, accounted for 16.2% of the biological crop protection market in 2025 and are the fastest-growing formulation segment. Granular soil-applied formulations for bionematicide and soil biofungicide applications represented the remaining 6.4% of the market by formulation type in 2025.

Regional Analysis

North America

North America biological crop protection market held a 34.8% share in 2025, generating approximately USD 2.38 Billion in revenue. The United States is the dominant national market, driven by California's large specialty crop sector, where strict MRL enforcement and premium retailer supplier codes have made biological crop protection integration standard practice in strawberry, lettuce, tomato, and wine grape production. The EPA's FIFRA Section 25(b) minimum-risk biopesticide exemption creates a highly accessible regulatory pathway for certain botanical and microbial active ingredients, enabling rapid product launches that sustain competitive product innovation in the US biological market. The National Organic Program under the USDA prohibits most synthetic pesticides from certified organic production, directly mandating biological crop protection adoption across the approximately 5.5 Million acres of certified organic farmland in the US as of 2025. Canada contributes through organic produce production in British Columbia and Ontario and has implemented pesticide reduction targets under the Canadian Environmental Protection Act that favor biological alternatives. Mexico is a significant biological product consumer in its export-oriented fruit and vegetable production regions, where supermarket retail buyers in the US and Europe impose MRL specifications that mandate biological program integration.

Europe

Europe biological crop protection market represented 28.6% of global revenues in 2025, equivalent to approximately USD 1.96 Billion. The EU Farm to Fork Strategy mandate to reduce chemical pesticide use by 50% by 2030, combined with the Sustainable Use of Pesticides Directive (SUD) revision process and national pesticide reduction action plans across member states, creates the most aggressive regulatory driver for biological crop protection adoption of any major global region. The Netherlands leads European market activity through its world-leading greenhouse horticulture sector, where biological crop protection through beneficial insects, fungal bioinsecticides, and predatory mites is integrated practice across the majority of commercial tomato, pepper, and cucumber production under glass. Spain is the largest outdoor vegetable producer in Europe and is experiencing rapid biological adoption driven by export market retailer MRL requirements. Germany and France each represent significant demand markets for biological fungicides in wine grape production, where restrictions on copper fungicide applications are compelling growers toward microbial and biochemical alternatives. Italy's intensive fruit and vegetable production, combined with strong government co-financing of biological product adoption through Programmi di Sviluppo Rurale, sustains broad biological product use across its agricultural sector.

Asia Pacific

Asia Pacific held approximately 19.4% of the global biological crop protection market in 2025, generating approximately USD 1.33 Billion, and represents a rapidly growing market driven by government-mandated pesticide reduction programs across China, India, and Southeast Asia. China is the largest national market in the region, where the Ministry of Agriculture and Rural Affairs' Zero Growth Action Plan for chemical fertilizers and pesticides, targeting a 30% reduction in chemical pesticide use by 2035, is driving institutional support for biological alternatives in rice, vegetables, and fruit production. China's domestic biological crop protection industry is among the most active globally in terms of new product registrations, with over 800 registered biological active ingredients as of 2025 across microbial and biochemical categories. India represents the second-largest Asia Pacific biological crop protection market, driven by government Paramparagat Krishi Vikas Yojana organic farming promotion programs and strong demand for biopesticide alternatives in rice, cotton, vegetables, and pulse production. Japan's highly regulated pesticide approval environment and premium agricultural standards drive adoption of biological products in high-value horticultural production, particularly for export-grade produce. Australia contributes through its organic agriculture sector and premium wine grape production regions, where biological pest management programs are integrated with precision viticulture systems.

Latin America

Latin America held approximately 13.4% of the global biological crop protection market in 2025, generating approximately USD 916 Million, and is the fastest-growing regional market at a projected CAGR of 14.8% through 2034. Brazil is both the largest and the most strategically significant national market, where MAPA's accelerated registration pathway for biological crop protection products has enabled over 200 new biological active ingredient registrations since 2020. Brazil's large-scale soybean, sugarcane, corn, and coffee production systems are the primary volume applications for biological products, with biological seed treatments for soybean nitrogen fixation and biological nematode management programs representing multi-hundred-million-dollar annual markets. Brazil's public research enterprise EMBRAPA has played a central role in developing biological crop protection technologies adapted to tropical conditions, including high-temperature-stable Bacillus formulations and locally isolated Trichoderma strains. Argentina represents the second-largest Latin American biological crop protection market, with soybean and grape production driving demand. Colombia, Mexico, and Chile are the next-largest markets, with specialty crops including coffee, avocado, berries, and fresh vegetables for export driving biological adoption under retailer MRL and sustainability certification requirements.

Middle East & Africa

The Middle East and Africa region held approximately 3.8% of the global biological crop protection market in 2025, generating approximately USD 260 Million. South Africa leads the African biological crop protection market, with its export-oriented deciduous fruit and wine grape production in the Western Cape adopting biological programs to meet European MRL and GlobalGAP certification requirements. Kenya and Ethiopia are growing biological crop protection markets in Sub-Saharan Africa, driven by fresh flower and vegetable export sectors where European supermarket buyer specifications mandate biological pest management programs. The UAE and Saudi Arabia represent the primary Middle Eastern demand centers, where intensive greenhouse vegetable production in climate-controlled facilities adopts biological biocontrol programs adapted from Dutch and Spanish production models. Morocco is an important North African market for biological crop protection, with its export-oriented citrus, tomato, and pepper production serving EU markets subject to strict residue requirements. Government-funded agricultural modernization programs across the region, including Saudi Arabia's National Agricultural Development Strategy and Kenya's Big Four Agriculture Agenda, are creating institutional support frameworks for biological crop protection technology transfer and adoption at scale.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Microbial Biopesticides

- Biochemical Biopesticides

- Semiochemicals & Pheromones

- Beneficial Macro-Organisms

- Plant-Incorporated Protectants & RNAi-Based Products

By Crop Type

- Fruits & Vegetables

- Cereals & Grains

- Oilseeds & Pulses

- Turf, Ornamentals & Other Non-Food

- Plantation Crops

By Mode of Action

- Biofungicides

- Bioinsecticides

- Bionematicides

- Bioherbicides

- Bioviricides & Other

By Formulation

- Wettable Powder & Dry Granule

- Liquid Suspension Concentrate & Oil Dispersion

- Seed Treatment Formulations

- Granular Soil-Applied Formulations

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 6.84 B |

| Forecast Revenue (2034) | USD 18.92 B |

| CAGR (2025-2034) | 11.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Microbial Biopesticides, Biochemical Biopesticides, Semiochemicals & Pheromones, Beneficial Macro-Organisms, Plant-Incorporated Protectants & RNAi-Based Products), By Crop Type, (Fruits & Vegetables, Cereals & Grains, Oilseeds & Pulses, Turf, Ornamentals & Other Non-Food, Plantation Crops), By Mode of Action, (Biofungicides, Bioinsecticides, Bionematicides, Bioherbicides, Bioviricides & Other), By Formulation, (Wettable Powder & Dry Granule, Liquid Suspension Concentrate & Oil Dispersion, Seed Treatment Formulations, Granular Soil-Applied Formulations) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | BASF SE, BAYER AG, SYNGENTA GROUP, CORTEVA AGRISCIENCE, MARRONE BIO INNOVATIONS (AMVAC), KOPPERT BIOLOGICAL SYSTEMS, BIOBEST GROUP, NOVOZYMES (NOVONESIS), CERTIS BIOLOGICALS, AGBIOME INC., UPL LIMITED, ARYSTA LIFESCIENCE (UPL), BIOWORKS INC., VERDESIAN LIFE SCIENCES, STOCKTON GROUP, ITALPOLLINA SPA, ANDERMATT GROUP, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Crop Type (Fruits & Vegetables, Cereals & Grains, Oilseeds & Pulses, Turf & Ornamentals, Plantation Crops), By Mode of Action (Biofungicides, Bioinsecticides, Bionematicides, Bioherbicides) Industry Trends & Forecast 2026–2034")

, By Crop Type (Fruits & Vegetables, Cereals & Grains, Oilseeds & Pulses, Turf & Ornamentals, Plantation Crops), By Mode of Action (Biofungicides, Bioinsecticides, Bionematicides, Bioherbicides) Industry Trends & Forecast 2026–2034")

, By Crop Type (Fruits & Vegetables, Cereals & Grains, Oilseeds & Pulses, Turf & Ornamentals, Plantation Crops), By Mode of Action (Biofungicides, Bioinsecticides, Bionematicides, Bioherbicides) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the ?

Global Biological crop protection market valued at USD 6.11B in 2024, reaching USD 18.92B by 2034, growing at a CAGR of 11.9% from 2026–2034.

Who are the major players in the ?

BASF SE, BAYER AG, SYNGENTA GROUP, CORTEVA AGRISCIENCE, MARRONE BIO INNOVATIONS (AMVAC), KOPPERT BIOLOGICAL SYSTEMS, BIOBEST GROUP, NOVOZYMES (NOVONESIS), CERTIS BIOLOGICALS, AGBIOME INC., UPL LIMITED, ARYSTA LIFESCIENCE (UPL), BIOWORKS INC., VERDESIAN LIFE SCIENCES, STOCKTON GROUP, ITALPOLLINA SPA, ANDERMATT GROUP, OTHERS

Which segments covered the ?

By Product Type, (Microbial Biopesticides, Biochemical Biopesticides, Semiochemicals & Pheromones, Beneficial Macro-Organisms, Plant-Incorporated Protectants & RNAi-Based Products), By Crop Type, (Fruits & Vegetables, Cereals & Grains, Oilseeds & Pulses, Turf, Ornamentals & Other Non-Food, Plantation Crops), By Mode of Action, (Biofungicides, Bioinsecticides, Bionematicides, Bioherbicides, Bioviricides & Other), By Formulation, (Wettable Powder & Dry Granule, Liquid Suspension Concentrate & Oil Dispersion, Seed Treatment Formulations, Granular Soil-Applied Formulations)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Biological Crop Protection Market

Published Date : 20 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date