- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Biometric Wearable Market Size, Share & Forecast | CAGR 11.8%

Global Biometric Wearable Market Size, Share, Analysis By Device Type (Smartwatches, Fitness Bands & Activity Trackers, Smart Rings, Smart Patches, Smart Clothing & Wearable Sensors, Other Biometric Wearables), By Biometric Parameter Monitored (Heart Rate & HRV, Blood Oxygen Saturation, ECG, Blood Pressure, Body Temperature, Sleep & Stress Monitoring, Glucose Monitoring), By Application (Health & Wellness Monitoring, Chronic Disease Management, Fitness & Sports Performance Tracking, Remote Patient Monitoring, Workplace Safety, Military & Defense), By End-User and Distribution Channel Industry Region & Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 13.80 Billion | USD 37.65 Billion | 11.8% | North America, 38.0% |

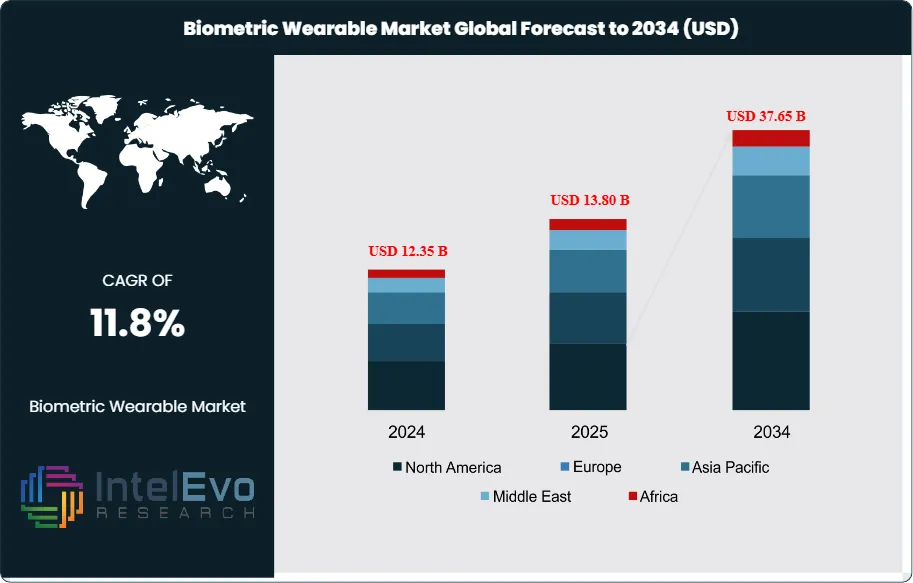

The Biometric Wearable Market was valued at approximately USD 12.35 Billion in 2024 and reached USD 13.80 Billion in 2025. The market is projected to grow to USD 37.65 Billion by 2034, expanding at a CAGR of 11.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 23.85 Billion over the analysis period. The market growth is driven by increasing consumer adoption of smartwatches, fitness trackers, smart rings, and advanced health-monitoring wearables, coupled with rising awareness regarding preventive healthcare and personal wellness management. Growing demand for continuous monitoring of vital parameters such as heart rate, blood oxygen levels, ECG, sleep quality, stress levels, and glucose levels is further supporting market expansion globally.

Get More Information about this report -

Request Free Sample ReportGrowth in the biometric wearable market is anchored in three demand shifts. First, continuous physiological monitoring migrated from experimental fitness gadgets to a mainstream health category, evidenced by Oura Health crossing 5.5 million cumulative rings sold and projecting USD 1 Billion in 2025 revenue, double its USD 500 Million figure in 2024. Second, medical-grade positioning is producing a new biometric wearable tier, with Whoop MG carrying FDA 510(k) clearance for its ECG feature since April 2025 and Biolinq Shine receiving FDA approval on September 25, 2025, as the first insertion-free glucose sensor. Third, clinical integration is expanding, with Dexcom's Stelo Glucose Biosensor System cleared as the first over-the-counter continuous glucose monitor in March 2024 and Oura partnering with Dexcom to funnel glucose data into the Oura app.

The biometric wearable market's regulatory environment is consolidating around three frameworks. The US Food and Drug Administration reviews biometric wearables under the 510(k) clearance pathway, with Whoop, Dexcom, Abbott, and Biolinq among recent recipients. The European Union Medical Device Regulation (MDR) 2017/745 governs CE-marking of clinical-grade biometric wearables, while the EU AI Act's general-purpose AI provisions entered force on August 2, 2025, affecting AI-coached health devices. Data-privacy obligations sit outside HIPAA for most consumer biometric wearable vendors including Apple, Fitbit, Oura, and Garmin, shifting enforcement to California's CCPA, Illinois' BIPA, and the EU GDPR.

Demand is structurally broadening across consumer, enterprise, and clinical channels. Apple held approximately 20% of the global smartwatch market in Q1 2025 per IDC data, while Samsung held 6%, and Oura held over 80% of the smart ring sub-segment. Corporate wellness programs, military fatigue tracking by the US Department of Defense on Oura devices, and insurer partnerships such as the November 2025 Standard Chartered-Bupa Global-Whoop agreement extend the biometric wearable market beyond direct-to-consumer channels.

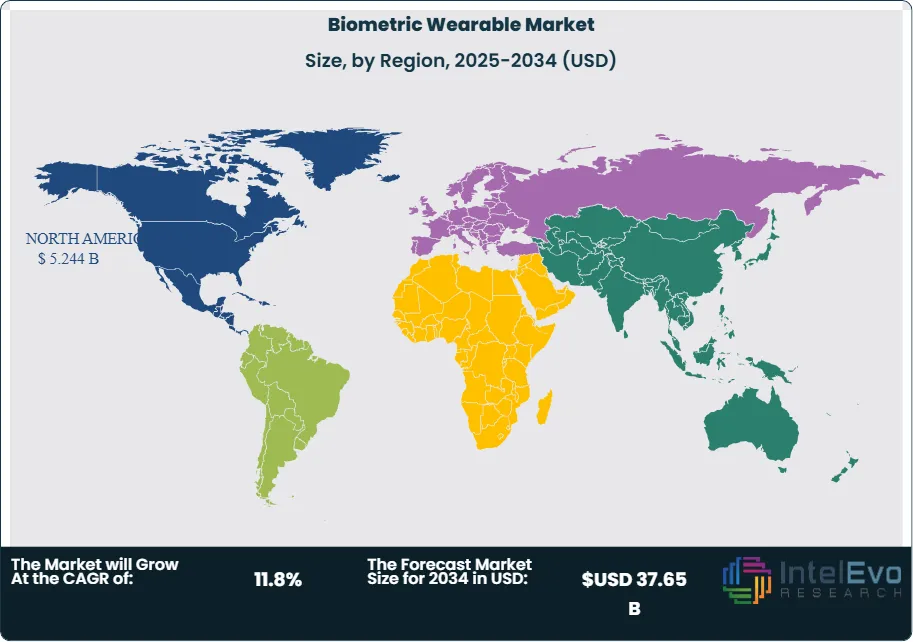

North America held the largest biometric wearable market share at 38.0% in 2025, anchored by Apple, Google's Fitbit, Garmin, Dexcom, Abbott, Whoop, and Oura's US operations. Asia Pacific recorded the fastest regional growth through Huawei Technologies, Xiaomi Corporation, Samsung Electronics, and local smart-ring entrants. The technology roadmap through 2034 will tilt toward non-invasive continuous biomarkers, AI coaching layers such as Oura's February 2026 women's health large language model, and sensor fusion between consumer wearables and clinical diagnostics.

Market Definition & Scope

The biometric wearable market is defined as the global commercial activity in body-worn devices that continuously or intermittently measure physiological or behavioural parameters using embedded sensors and associated software or subscription services. The market encompasses smartwatches including Apple Watch Series 11 and Galaxy Watch 8, smart rings such as Oura Ring 4 and Galaxy Ring, fitness bands, recovery straps including Whoop 5.0 and Whoop MG, continuous glucose monitors including Dexcom G7 and Abbott FreeStyle Libre, smart patches, smart clothing with integrated sensors, and clinical-grade remote-patient-monitoring devices.

Included in the scope are hardware revenues, subscription and membership revenues, enterprise licensing, and data services tied to biometric wearable devices. Explicitly excluded are implantable medical devices, non-body-worn remote monitors, pure fitness apps without associated hardware, and traditional non-sensing watches. The biometric wearable market is a subset of the broader USD 67 Billion wearable technology category and sits adjacent to the USD 51.6 Billion biometric system market, which includes fingerprint and facial identification infrastructure rather than physiological monitoring.

, By Biometric Parameter Monitored (Heart Rate & HRV, Blood Oxygen Saturation, ECG, Blood Pressure, Body Temperature, Sleep & Stress Monitoring, Glucose Monitoring), By Application (Health & Wellness Monitoring, Chronic Disease Management, Fitness & Sports Performance Tracking, Remote Patient Monitoring, Workplace Safety, Military & Defense), By End-User and Distribution Channel Industry Region & Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The biometric wearable market expands from USD 13.80 Billion in 2025 to USD 37.65 Billion by 2034, a CAGR of 11.8% over the forecast period.

- Segment Dominance by Device Type: The smartwatches segment led in 2025 with 48.6% share, driven by Apple Watch Series 11, Samsung Galaxy Watch 8, and Google Pixel Watch 3.

- Segment Dominance by Application: Sports and fitness applications accounted for 39.0% of 2025 revenue, reflecting consumer adoption across Apple, Garmin, Fitbit, Whoop, and Oura platforms.

- Driver: US FDA 510(k) clearances for biometric wearable features, including Whoop MG ECG in April 2025 and Biolinq Shine glucose sensor in September 2025, unlocked clinical reimbursement paths.

- Restraint: Consumer biometric wearable vendors sit outside HIPAA protection, exposing Apple, Fitbit, Oura, and Garmin users to data-privacy complexity under CCPA, BIPA, and GDPR.

- Opportunity: Non-invasive continuous biomarkers represent an estimated USD 4.2 Billion incremental 2034 opportunity, supported by Dexcom Stelo OTC launch and Biolinq Shine FDA approval.

- Trend: AI coaching features shifted biometric wearables from recorders to recommenders, with Whoop Coach, Oura's proprietary women's health LLM launched in February 2026, and Samsung Health Bedtime Guidance.

- Regional: North America led the biometric wearable market with 38.0% share and USD 5.24 Billion in revenue in 2025, followed by Asia Pacific at 29.5%.

Key Insights Summary

- Oura Health closed a USD 900 Million Series E round on October 14, 2025, led by Fidelity Management & Research Company with ICONIQ, Whale Rock, and Atreides, at an approximately USD 11 Billion valuation, more than double the USD 5.2 Billion December 2024 Series D, alongside 5.5 million cumulative Oura Ring shipments.

- WHOOP, Inc. closed a USD 575 Million Series G on March 31, 2026, at a USD 10.1 Billion valuation led by TPG with Abbott Laboratories, Mayo Clinic, Cristiano Ronaldo, and LeBron James participating, on a reported USD 1.1 Billion run rate and 2.5 million members.

- The US Food and Drug Administration approved Biolinq Shine on September 25, 2025, as the first insertion-free wearable glucose biosensor, establishing a new regulatory category for non-insulin users and expanding the addressable prediabetes and Type 2 population.

- Apple held approximately 20% of the global smartwatch market in Q1 2025 per IDC data, against Samsung Electronics at 6%, while Oura Health held over 80% of the smart ring sub-segment based on IDC's 2024 estimate.

- Whoop MG's ECG received FDA 510(k) clearance in April 2025, but the FDA issued a warning letter in 2025 stating Whoop's Blood Pressure Insights feature was marketed without authorization, creating an open enforcement risk ahead of a planned IPO.

- Oura launched a proprietary large language model purpose-built for women's health in February 2026 on Oura-controlled infrastructure, following the August 2025 Perimenopause Check-In and Pregnancy Insights features and a partnership with Maven Clinic and Progyny.

- The National Institutes of Health reported that 36% of US adults used a wearable in 2022, up from 30% in 2019, and the Centers for Disease Control and Prevention estimated in 2024 that nearly half of US adults digitally monitored at least one health metric, framing the US biometric wearable procurement checklist at both the consumer and payer layers.

Competitive Landscape Overview

The biometric wearable market is moderately consolidated at the smartwatch and smart-ring tier and fragmented at the fitness band and clinical-grade tier. The top four companies, Apple, Samsung Electronics, Garmin, and Oura Health, accounted for an estimated 42.3% of combined 2025 biometric wearable revenue based on public filings and disclosed sales. Competition is increasingly platform-led rather than specification-led, because subscription-attached devices capture recurring revenue well above hardware margins.

Competitive dynamics shifted in 2025 and early 2026 as premium health positioning, FDA clearances, and AI coaching features reset category boundaries. Whoop's USD 10.1 Billion March 2026 Series G, Oura's USD 11 Billion October 2025 Series E, and Abbott Laboratories participating in Whoop's Series G signalled convergence between consumer fitness and clinical-grade monitoring. Garmin responded with the screenless Cirqa band and Fitbit continues integrating Loss of Pulse Detection and Readiness Score into Pixel Watch 3. Consolidation pressure is visible in Oura's April 2025 US International Trade Commission patent victory against Ultrahuman and RingConn, which banned infringing smart rings from the US market, and its licensing agreement with French startup Circular.

Competitive Landscape Matrix:

| Company | Headquarters | Position | Key Product | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Apple Inc. | United States | Leader | Apple Watch Series 11; Watch Ultra 3 | North America, Europe | Launched Apple Watch Series 11 with hypertension notifications in September 2025 |

| Samsung Electronics Co., Ltd. | South Korea | Leader | Galaxy Watch 8; Galaxy Ring | Asia Pacific, North America | Released Galaxy Watch 8 with Antioxidant Index and Vascular Load in July 2025 |

| Garmin Ltd. | United States | Leader | Forerunner, Fenix, Venu; Cirqa band | North America, Europe | Introduced Cirqa screenless band; reported USD 7 Billion annual revenues |

| Oura Health Oy | Finland | Leader | Oura Ring 4; Pregnancy Insights; women's LLM | North America, Europe, Japan | Closed USD 900 Million Series E at USD 11 Billion valuation in October 2025 |

| WHOOP, Inc. | United States | Challenger | Whoop 5.0; Whoop MG; Advanced Labs | North America, Europe | Closed USD 575 Million Series G at USD 10.1 Billion valuation on March 31, 2026 |

| Google LLC (Fitbit) | United States | Challenger | Fitbit Charge 6; Pixel Watch 3 | North America, Europe | Added Loss of Pulse Detection and Readiness Score to Pixel Watch 3 |

| Huawei Technologies Co., Ltd. | China | Challenger | Huawei Watch GT series; Band series | Asia Pacific, Middle East | Expanded TruSense health-monitoring sensor platform across 2024-2025 lineup |

| Xiaomi Corporation | China | Challenger | Mi Band; Xiaomi Watch S series | Asia Pacific, Europe | Scaled Mi Band and Watch S global shipments through value-tier distribution |

| Dexcom, Inc. | United States | Niche Player | Dexcom G7; Stelo Biosensor System | North America, Europe | Expanded FDA-cleared Stelo over-the-counter CGM availability through 2025 |

| Abbott Laboratories | United States | Niche Player | FreeStyle Libre 3 Plus; Lingo | North America, Europe | Integrated FreeStyle Libre data into clinical workflows and Whoop Series G investment |

Segmentation Analysis

The biometric wearable market segments by device type, biometric parameter monitored, application, end-user, and distribution channel. Each segmentation type maps to distinct buying criteria that a biometric wearable procurement checklist must address, including sensor accuracy, battery life, FDA or CE clearance status, subscription commitments, and data-portability compliance.

By Device Type

Smartwatches held 48.6% of the biometric wearable market in 2025, approximately USD 6.71 Billion, led by Apple Watch Series 11, Samsung Galaxy Watch 8, Google Pixel Watch 3, and Garmin's Forerunner and Fenix series. Apple captured roughly 20% of the global smartwatch sub-category in Q1 2025 per IDC, with Samsung at 6% and the remainder split among Huawei, Garmin, Xiaomi, and Amazfit. Apple Watch Series 11 introduced hypertension notifications in September 2025, while Samsung Galaxy Watch 8 added Antioxidant Index and Vascular Load features using bioactive sensors on the back of the watch.

Fitness bands and smart rings together held 28.4% of 2025 revenue, roughly USD 3.92 Billion, and are the fastest-growing biometric wearable sub-segment at an estimated 15.4% CAGR through 2034. Oura Health controls more than 80% of the smart ring niche based on IDC 2024 estimates, with Samsung Galaxy Ring, Ultrahuman, RingConn, Amazfit Helio, Velia, and Circular rounding out the field. Smart patches and continuous monitors, including Dexcom G7, Abbott FreeStyle Libre 3 Plus, Biolinq Shine, and BioIntelliSense BioSticker, contributed 12.5%, while smart clothing held 6.8% and biometric-enabled smart glasses or headbands captured 3.7%.

By Biometric Parameter Monitored

Heart rate and ECG monitoring led the biometric wearable market at 30.0% share in 2025, roughly USD 4.14 Billion, because optical photoplethysmography sensors and single-lead ECG are the most mature and FDA-cleared modalities. Activity and movement parameters held 22.0%, sleep tracking 18.0%, blood oxygen and respiratory monitoring 12.0%, skin temperature 8.0%, continuous glucose 7.0%, and blood pressure 3.0%. The glucose sub-segment is the fastest-growing at an estimated 18.6% CAGR through 2034, propelled by the March 2024 Stelo OTC clearance and the September 2025 Biolinq Shine approval.

Comparative feature depth is widening across device tiers. Whoop MG added FDA-cleared ECG in April 2025 through its 510(k) pathway, while Samsung Galaxy Watch 8 introduced Antioxidant Index as a novel carotenoid-based biomarker and Apple Watch Series 11 added hypertension notifications. This sensor stacking drives a biometric wearable pricing benchmarks shift, because each additional validated parameter extends a device's clinical and reimbursement relevance beyond general wellness.

By Application

Sports and fitness applications held the largest biometric wearable market share at 39.0% in 2025, approximately USD 5.38 Billion, anchored in consumer use of Apple Watch, Garmin Forerunner, Fitbit Charge, Whoop 5.0, and Oura Ring 4. Clinical health and remote patient monitoring applications held 31.0%, driven by Dexcom G7, Abbott FreeStyle Libre 3 Plus, Philips Healthcare solutions, VitalConnect VitalPatch, BioIntelliSense BioSticker, and Empatica EmbracePlus used across hospitals, clinics, and telehealth networks.

Authentication and security applications held 8.0%, including biometric unlock for Apple Watch and Samsung Galaxy Watch with Galaxy smartphones. Workplace and occupational safety held 10.0%, covering construction, logistics, and manufacturing deployments of heart rate and fatigue monitoring. Military and defense applications held 6.0%, anchored by the US Department of Defense's Oura Ring deployment for service-member fatigue tracking. Remaining applications, including pet and livestock monitoring adjacent categories, held 6.0%. The biometric wearable ROI calculation for clinical buyers typically centers on reduced hospital readmissions, with clinical-grade wearable deployments producing documented readmission-rate reductions across remote monitoring studies.

By End-User

Individual consumers represented the largest biometric wearable end-user share at 58.0% in 2025, reflecting direct-to-consumer scale across Apple, Samsung Electronics, Google's Fitbit, Garmin, Xiaomi, Huawei Technologies, and Oura Health. Healthcare providers held 22.0%, with hospitals, clinics, and remote-monitoring services deploying Dexcom, Abbott, Philips Healthcare, and VitalConnect devices. Corporate wellness and insurer programs held 9.0%, expanded by the Standard Chartered-Bupa Global-Whoop partnership announced November 27, 2025. Professional sports and athlete-focused users held 6.0%, supported by Whoop's Ferrari partnership announced January 20, 2026. Defense and military users held 3.0% and academic or research users held 2.0%.

By Distribution Channel

Online distribution led the biometric wearable market with 56.5% share in 2025, through direct-to-consumer sites and platforms including Amazon, Apple.com, Samsung.com, Google Store, and Oura.com. Offline channels held 43.5%, including Apple Retail, Samsung Experience stores, Best Buy, Target, and over 4,000 retail doors carrying the Oura Ring. Oura's expansion into Target and Amazon in April 2024 underlined the channel shift, and the US health savings account eligibility of selected biometric wearables including Oura Ring extended reimbursed-retail purchasing for US buyers across the 2025-2026 compliance window.

Regional Analysis

The biometric wearable market is geographically led by North America, Asia Pacific, and Europe, together accounting for 89.5% of 2025 revenue. Regional competitive structures differ sharply, with North America leading on platform revenue and FDA-cleared devices, Asia Pacific leading on shipment volume and manufacturing, and Europe leading on MDR-driven clinical integration.

North America

North America held 38.0% of the biometric wearable market in 2025, approximately USD 5.244 Billion. The United States dominates with Apple in Cupertino, Google's Fitbit, Garmin's US operations, Dexcom in San Diego, Abbott Laboratories, Whoop in Boston, and Biolinq in San Diego. Canada contributes a smaller share through Hexoskin's smart clothing and academic-health research deployments, while Mexico is expanding through consumer imports of Apple, Samsung, and Xiaomi devices. US FDA clearances in 2024 and 2025, including Stelo in March 2024, Whoop MG ECG in April 2025, and Biolinq Shine on September 25, 2025, reinforced North America's clinical biometric wearable leadership.

Europe

Europe accounted for 22.0% of the biometric wearable market in 2025, approximately USD 3.036 Billion. The United Kingdom and Germany lead platform revenue, Finland leads on Oura Health's Finnish-headquartered manufacturing and R&D scaling into a Texas facility for US defence production, and France contributes through Withings and Circular. Germany's GEMA AI copyright precedents and the EU AI Act's August 2, 2025 general-purpose AI enforcement reinforce European biometric wearable AI-coaching compliance. The EU Medical Device Regulation 2017/745 governs CE-marking for clinical-grade biometric wearables sold into the 27-member EU market.

Asia Pacific

Asia Pacific held 29.5% of the biometric wearable market in 2025, approximately USD 4.071 Billion, and recorded the fastest regional growth. China dominates on shipment volume through Huawei Technologies, Xiaomi Corporation, Amazfit's parent Zepp Health, and Zepp Clarity. South Korea anchors premium smartwatches through Samsung Electronics and the Galaxy Ring and Galaxy Watch 8 releases. Japan contributes through consumer adoption of Oura Ring, Apple Watch, and Casio's domestic smartwatches, with Oura launching its latest ring in Japan in 2025. India is expanding through Boat, Noise, and Fitbit distribution, with a biometric wearable penetration gap that represents a structural 2026-2030 growth vector.

Latin America

Latin America held 6.5% of the biometric wearable market in 2025, approximately USD 897 Million. Brazil and Mexico lead adoption, driven by Apple Watch, Samsung Galaxy Watch, Xiaomi Mi Band, and growing Oura Ring imports. Independent consumers and corporate wellness buyers represent the primary channels, with subscription-tier biometric wearable pricing benchmarks typically 20% to 30% below North American equivalents because of currency dynamics. Regional healthcare-digitization programs in Brazil's Sistema Unico de Saude and Mexico's IMSS are expected to open a clinical-grade biometric wearable procurement channel through 2028.

Middle East & Africa

Middle East & Africa accounted for 4.0% of the biometric wearable market in 2025, approximately USD 552 Million. The United Arab Emirates and Saudi Arabia lead regional adoption, supported by state-backed digital health programs including Saudi Arabia's Vision 2030 health initiative and the UAE's Reaching the Next Generation strategy. South Africa anchors sub-Saharan adoption through corporate wellness programs and private-hospital remote-monitoring pilots. The regional biometric wearable compliance requirements sit under national health authorities including the Saudi Food and Drug Authority and the UAE Ministry of Health and Prevention, which align with FDA 510(k) and EU MDR standards for clinical-grade biometric wearables.

Country Analysis

Four national biometric wearable markets, the United States, China, Germany, and Japan, collectively accounted for approximately 57.8% of 2025 revenue. These markets concentrate vendor headquarters, manufacturing capacity, FDA and CE clearances, and payer-reimbursement pilots.

United States

The United States represented approximately USD 3.80 Billion in 2025 biometric wearable revenue, with a country CAGR estimated at 12.1% through 2034. Federal activity concentrated around the FDA Center for Devices and Radiological Health, which cleared Dexcom Stelo as the first OTC CGM on March 5, 2024, Whoop MG ECG via 510(k) in April 2025, and Biolinq Shine on September 25, 2025. The National Institutes of Health reported that 36% of US adults used a wearable in 2022, up from 30% in 2019, and Centers for Disease Control and Prevention 2024 estimates showed nearly half of US adults digitally monitoring at least one health parameter. US Department of Health and Human Services signals through early 2026, including public statements by the Health Secretary on extending wearables to Medicare beneficiaries, reinforce biometric wearable reimbursement tailwinds. State-level data-privacy activity through California CCPA, Illinois BIPA, and Washington's MyHealth My Data Act defines consumer-wearable compliance requirements.

China

China represented approximately USD 2.07 Billion in 2025 biometric wearable revenue, with a country CAGR estimated at 13.4% through 2034. Huawei Technologies and Xiaomi Corporation dominate shipments through value-tier fitness bands and mid-tier smartwatches, with Huawei's TruSense sensor platform and Xiaomi's Mi Band series anchoring the market. Amazfit's parent Zepp Health and Honor extend domestic competition. China's National Medical Products Administration regulates clinical-grade biometric wearables through the Class II and Class III pathways, and the Cyberspace Administration of China's Personal Information Protection Law (PIPL) governs biometric data handling. Tencent Holdings and Ant Group-linked health services expanded biometric data integration across consumer health platforms in 2025.

Germany

Germany represented approximately USD 847 Million in 2025 biometric wearable revenue, with a country CAGR estimated at 11.2% through 2034. Adoption concentrates in Apple Watch, Samsung Galaxy Watch, Oura Ring (with Oura launching its latest ring in Germany in 2025), Garmin Fenix, Fitbit, and Withings. Germany's statutory health insurers (GKV) reimburse selected digital health applications (DiGA) under the 2019 Digital Healthcare Act, creating a defined biometric wearable reimbursement pathway when paired with approved software. The EU Medical Device Regulation 2017/745 and the 2024 EU AI Act govern clinical-grade and AI-coached biometric wearables, with the Federal Institute for Drugs and Medical Devices (BfArM) as the national competent authority.

Japan

Japan represented approximately USD 1.26 Billion in 2025 biometric wearable revenue, with a country CAGR estimated at 10.6% through 2034. Apple Watch and Samsung Galaxy Watch dominate smartwatch demand, Oura Ring 4 expanded into Japan in 2025, and domestic brands including Casio, Omron Healthcare, and Seiko contribute specialized devices. Omron Healthcare's HeartGuide wearable blood pressure monitor holds Pharmaceuticals and Medical Devices Agency (PMDA) approval, and Japan's national insurance system reimburses selected clinical-grade biometric wearables for hypertension and arrhythmia monitoring. The Japanese ageing demographic, with more than 29% of the population over 65, underwrites the demand base through 2034.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Device Type

- Smartwatches

- Fitness Bands & Activity Trackers

- Smart Rings

- Smart Patches

- Smart Clothing & Wearable Sensors

- Other Biometric Wearables

By Biometric Parameter Monitored

- Heart Rate & Heart Rate Variability (HRV)

- Blood Oxygen Saturation (SpO2)

- Electrocardiogram (ECG)

- Blood Pressure Monitoring

- Body Temperature Monitoring

- Sleep & Stress Monitoring

- Glucose Monitoring

- Multi-Parameter Monitoring

By Application

- Health & Wellness Monitoring

- Chronic Disease Management

- Fitness & Sports Performance Tracking

- Remote Patient Monitoring (RPM)

- Workplace Safety & Occupational Health

- Military & Defense Applications

By End-User

- Consumers

- Healthcare Providers & Hospitals

- Fitness & Sports Organizations

- Enterprises & Corporate Wellness Programs

- Government & Defense Organizations

By Distribution Channel

- Online Retail & E-Commerce

- Brand-Owned Stores

- Consumer Electronics Retailers

- Pharmacies & Healthcare Channels

- Specialty Fitness & Sports Stores

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 13.80 B |

| Forecast Revenue (2034) | USD 37.65 B |

| CAGR (2025-2034) | 11.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Device Type, (Smartwatches, Fitness Bands & Activity Trackers, Smart Rings, Smart Patches, Smart Clothing & Wearable Sensors, Other Biometric Wearables), By Biometric Parameter Monitored, (Heart Rate & Heart Rate Variability (HRV), Blood Oxygen Saturation (SpO2), Electrocardiogram (ECG), Blood Pressure Monitoring, Body Temperature Monitoring, Sleep & Stress Monitoring, Glucose Monitoring, Multi-Parameter Monitoring), By Application, (Health & Wellness Monitoring, Chronic Disease Management, Fitness & Sports Performance Tracking, Remote Patient Monitoring (RPM), Workplace Safety & Occupational Health, Military & Defense Applications), By End-User, (Consumers, Healthcare Providers & Hospitals, Fitness & Sports Organizations, Enterprises & Corporate Wellness Programs, Government & Defense Organizations), By Distribution Channel, (Online Retail & E-Commerce, Brand-Owned Stores, Consumer Electronics Retailers, Pharmacies & Healthcare Channels, Specialty Fitness & Sports Stores) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | APPLE INC., SAMSUNG ELECTRONICS CO., LTD., GARMIN LTD., OURA HEALTH OY, WHOOP, INC., GOOGLE LLC (FITBIT), HUAWEI TECHNOLOGIES CO., LTD., XIAOMI CORPORATION, DEXCOM, INC., ABBOTT LABORATORIES, KONINKLIJKE PHILIPS N.V., POLAR ELECTRO OY, WITHINGS SA, BIOLINQ INCORPORATED, BIOINTELLISENSE, INC., VITALCONNECT, INC., EMPATICA INC., ZEPP HEALTH CORPORATION (AMAZFIT), ULTRAHUMAN HEALTHCARE PRIVATE LIMITED, OMRON HEALTHCARE CO., LTD., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Biometric Parameter Monitored (Heart Rate & HRV, Blood Oxygen Saturation, ECG, Blood Pressure, Body Temperature, Sleep & Stress Monitoring, Glucose Monitoring), By Application (Health & Wellness Monitoring, Chronic Disease Management, Fitness & Sports Performance Tracking, Remote Patient Monitoring, Workplace Safety, Military & Defense), By End-User and Distribution Channel Industry Region & Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Biometric Parameter Monitored (Heart Rate & HRV, Blood Oxygen Saturation, ECG, Blood Pressure, Body Temperature, Sleep & Stress Monitoring, Glucose Monitoring), By Application (Health & Wellness Monitoring, Chronic Disease Management, Fitness & Sports Performance Tracking, Remote Patient Monitoring, Workplace Safety, Military & Defense), By End-User and Distribution Channel Industry Region & Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Biometric Parameter Monitored (Heart Rate & HRV, Blood Oxygen Saturation, ECG, Blood Pressure, Body Temperature, Sleep & Stress Monitoring, Glucose Monitoring), By Application (Health & Wellness Monitoring, Chronic Disease Management, Fitness & Sports Performance Tracking, Remote Patient Monitoring, Workplace Safety, Military & Defense), By End-User and Distribution Channel Industry Region & Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Biometric Wearable Market?

The Global Biometric Wearable Market was valued at USD 12.35 Billion in 2024 and is projected to reach USD 37.65 Billion by 2034, growing at a CAGR of 11.8% from 2026 to 2034. Growth is driven by increasing adoption of smartwatches, fitness trackers, smart rings, remote patient monitoring solutions, AI-powered health analytics, wearable biosensors, digital healthcare platforms, chronic disease management technologies, and preventive healthcare initiatives worldwide.

Who are the major players in the Biometric Wearable Market?

APPLE INC., SAMSUNG ELECTRONICS CO., LTD., GARMIN LTD., OURA HEALTH OY, WHOOP, INC., GOOGLE LLC (FITBIT), HUAWEI TECHNOLOGIES CO., LTD., XIAOMI CORPORATION, DEXCOM, INC., ABBOTT LABORATORIES, KONINKLIJKE PHILIPS N.V., POLAR ELECTRO OY, WITHINGS SA, BIOLINQ INCORPORATED, BIOINTELLISENSE, INC., VITALCONNECT, INC., EMPATICA INC., ZEPP HEALTH CORPORATION (AMAZFIT), ULTRAHUMAN HEALTHCARE PRIVATE LIMITED, OMRON HEALTHCARE CO., LTD., Others

Which segments covered the Biometric Wearable Market?

By Device Type, (Smartwatches, Fitness Bands & Activity Trackers, Smart Rings, Smart Patches, Smart Clothing & Wearable Sensors, Other Biometric Wearables), By Biometric Parameter Monitored, (Heart Rate & Heart Rate Variability (HRV), Blood Oxygen Saturation (SpO2), Electrocardiogram (ECG), Blood Pressure Monitoring, Body Temperature Monitoring, Sleep & Stress Monitoring, Glucose Monitoring, Multi-Parameter Monitoring), By Application, (Health & Wellness Monitoring, Chronic Disease Management, Fitness & Sports Performance Tracking, Remote Patient Monitoring (RPM), Workplace Safety & Occupational Health, Military & Defense Applications), By End-User, (Consumers, Healthcare Providers & Hospitals, Fitness & Sports Organizations, Enterprises & Corporate Wellness Programs, Government & Defense Organizations), By Distribution Channel, (Online Retail & E-Commerce, Brand-Owned Stores, Consumer Electronics Retailers, Pharmacies & Healthcare Channels, Specialty Fitness & Sports Stores)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date