- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Bioprocess Chromatography Market Size, Share & Forecast | CAGR 11.6%

Global Bioprocess Chromatography Market Size, Share, Growth Analysis By Product Type (Chromatography Resins & Media, Chromatography Systems & Hardware, Pre-Packed Chromatography Columns, Membrane Adsorbers), By Chromatography Mode (Affinity Chromatography, Ion Exchange Chromatography, Hydrophobic Interaction Chromatography, Size Exclusion Chromatography, Mixed-Mode & Multimodal Chromatography), By Application, End-User, Industry Trends, Competitive Landscape, Regional Outlook & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 7.18 Billion | USD 19.24 Billion | 11.6% | North America, 41.8% |

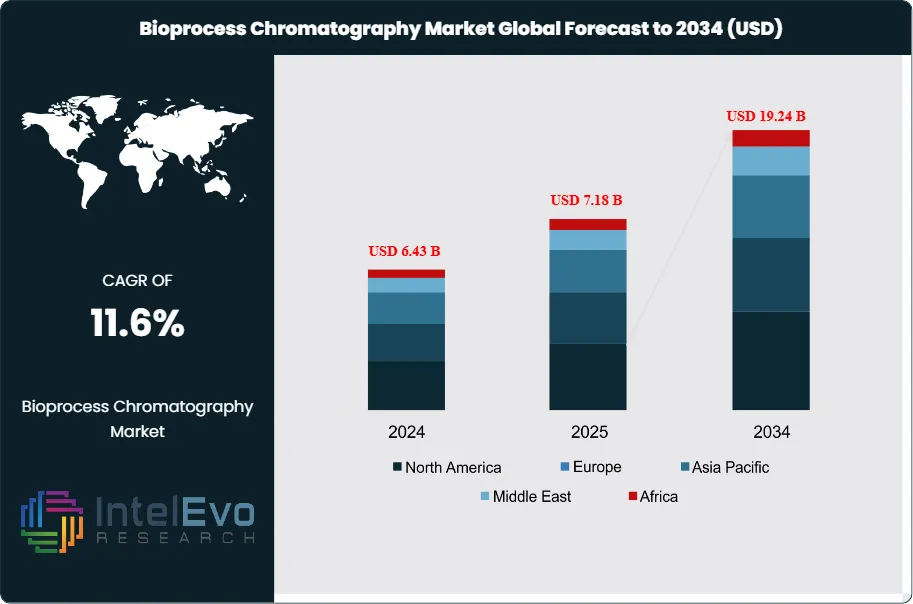

The Bioprocess Chromatography Market was valued at approximately USD 6.43 Billion in 2024 and reached USD 7.18 Billion in 2025. The market is projected to grow to USD 19.24 Billion by 2034, expanding at a CAGR of 11.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 12.06 Billion over the analysis period, driven by the accelerating commercial expansion of biologic drug manufacturing, the global biosimilar wave, and structural shifts toward continuous and integrated downstream bioprocessing that are increasing the volume and complexity of chromatography operations per manufacturing campaign.

Get More Information about this report -

Request Free Sample ReportBioprocess chromatography encompasses the downstream purification unit operations used in biopharmaceutical manufacturing to isolate and purify recombinant proteins, monoclonal antibodies, viral vectors, plasmid DNA, and other biological drug substances from complex fermentation or cell culture harvest streams. The principal chromatography modes applied in biopharmaceutical downstream processing include Protein A affinity chromatography — the dominant capture step for monoclonal antibodies — ion exchange chromatography (both cation exchange and anion exchange), hydrophobic interaction chromatography, size exclusion chromatography, and mixed-mode chromatography. Each of these modes is applied across multi-step purification trains that typically achieve host cell protein removal to below 10 parts per million and DNA clearance to below 1 ng per dose, as required by FDA and EMA biologic approval guidelines.

Demand within the bioprocess chromatography market is fundamentally driven by the biologics manufacturing sector. The global market for biologic drug products exceeded USD 450 Billion in 2025, with monoclonal antibodies representing the largest single product class at over USD 230 Billion in annual sales. Each kilogram of purified mAb produced commercially requires processing through 3–6 chromatography column steps, consuming substantial volumes of chromatography resin, buffer solutions, and column hardware. As biologic manufacturing capacity expands globally — with both integrated pharmaceutical manufacturers and CDMOs investing in large-scale bioreactor and downstream processing infrastructure — the demand for chromatography resins, columns, and systems grows proportionally.

The biosimilar market is adding substantial incremental demand to the bioprocess chromatography market. Each biosimilar program requires its own downstream purification process, validated independently of the originator product's manufacturing process. With more than 30 major originator biologics facing patent expiration before 2030 — collectively representing over USD 150 Billion in global annual revenue — biosimilar development and manufacturing programs are generating a new and growing procurement stream for chromatography consumables and equipment. FDA and EMA regulatory requirements for biosimilar process characterization and analytical comparability add technical rigor to purification process development, driving demand for high-resolution chromatography analytics alongside production-scale resins and columns.

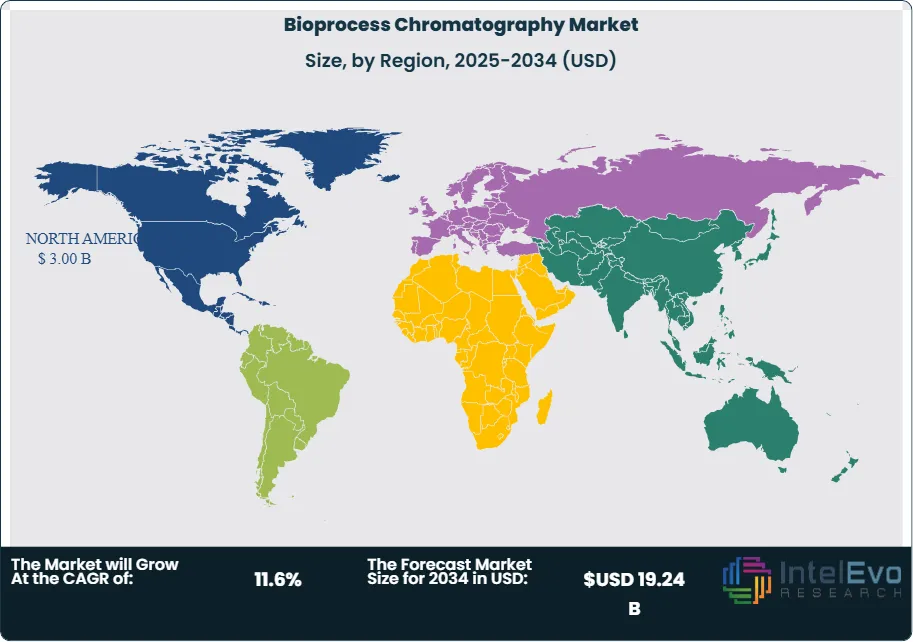

North America leads the bioprocess chromatography market with a 41.8% share in 2025, generating approximately USD 3.00 Billion, anchored by the United States' dominant biopharmaceutical manufacturing base and CDMO infrastructure. Europe holds 29.2% of the market. Asia Pacific represents 20.4% and is the fastest-growing region at a projected CAGR of 14.2% through 2034. Continuous bioprocessing adoption — which integrates periodic counter-current (PCC) chromatography into continuous manufacturing platforms — is the most consequential technology trend reshaping competitive dynamics within the bioprocess chromatography market through 2034.

, By Chromatography Mode (Affinity Chromatography, Ion Exchange Chromatography, Hydrophobic Interaction Chromatography, Size Exclusion Chromatography, Mixed-Mode & Multimodal Chromatography), By Application, End-User, Industry Trends, Competitive Landscape, Regional Outlook & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global bioprocess chromatography market was valued at USD 7.18 Billion in 2025 and is projected to reach USD 19.24 Billion by 2034, expanding at a CAGR of 11.6% over the forecast period 2026–2034.

- Segment Dominance: By product type, chromatography resins and media account for approximately 54.2% of bioprocess chromatography market revenue in 2025, driven by their consumable nature and the high resin volumes required per commercial mAb purification campaign.

- Segment Dominance: By application, monoclonal antibody purification dominates the bioprocess chromatography market at 48.6% of revenue in 2025, reflecting the commercial scale of the global mAb manufacturing sector and the structured multi-step Protein A-based purification platform applied universally across mAb products.

- Driver: The global mAb market exceeded USD 230 Billion in annual sales in 2025 and is growing at approximately 9.4% annually, with each commercial manufacturing campaign consuming 3–6 chromatography steps and requiring resin replacement every 50–200 cycles, generating recurring and growing consumable demand across the bioprocess chromatography market.

- Restraint: High Protein A resin cost — with commercial manufacturing-grade Protein A resin priced at USD 6,000–USD 14,000 per liter — represents a significant manufacturing cost input for mAb producers, creating pressure to extend resin lifetime through validated multi-cycle usage programs, which moderates the total resin volume consumed per kilogram of purified mAb.

- Opportunity: Continuous bioprocessing chromatography, including periodic counter-current (PCC) systems replacing traditional batch column chromatography, represents an addressable opportunity exceeding USD 3.8 Billion through 2034, as biopharmaceutical manufacturers adopt integrated continuous processes that increase resin utilization and reduce buffer consumption by 40–60% per gram of purified protein.

- Trend: Single-use chromatography systems — including pre-packed single-use columns, disposable membrane adsorbers, and single-use multi-column PCC skids — are present in approximately 28.4% of new chromatography system installations in 2025, up from 11.6% in 2019, as downstream processing adopts single-use technology for clinical and some commercial manufacturing campaigns.

- Regional Analysis: North America leads the global bioprocess chromatography market with a 41.8% share in 2025, generating approximately USD 3.00 Billion in revenue, underpinned by the United States' status as the largest biopharmaceutical manufacturing market globally and its dense concentration of CDMO downstream processing infrastructure.

Competitive Landscape Overview

The bioprocess chromatography market is moderately consolidated, with the top four suppliers — Cytiva (Danaher), Merck KGaA (MilliporeSigma), Sartorius AG, and Bio-Rad Laboratories — collectively accounting for approximately 62.4% of global market revenue in 2025. Competition is technology-driven and IP-intensive, with Protein A ligand chemistry, resin bead structure, and multi-column chromatography system design representing the primary areas of competitive differentiation. M&A activity has been significant, with major life sciences groups acquiring niche resin chemistry and single-use chromatography companies to extend their downstream bioprocessing portfolios. The installed base of column hardware creates long-term customer relationships that make switching between leading resin platforms difficult and costly for biopharmaceutical manufacturers.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product | Geo Strength | Recent Strategic Move (2024–2026) |

| Cytiva (Danaher) | USA | Leader | MabSelect PrismA Protein A Resin | North America / Global | Feb 2025: Launched MabSelect PrismA Ultra — an optimized Protein A resin targeting 30% higher dynamic binding capacity for high-concentration mAb applications compared to the predecessor platform. |

| Merck KGaA (MilliporeSigma) | Germany | Leader | Eshmuno A Protein A Resin | Europe / Global | Apr 2025: Expanded Eshmuno A manufacturing capacity at its Darmstadt facility by 40% to address growing demand from biosimilar manufacturers entering commercial-scale mAb purification. |

| Sartorius AG | Germany | Leader | Sartobind Rapid A Membrane Adsorber | Europe / Global | Jan 2026: Launched a high-capacity Sartobind Rapid A membrane adsorber series targeting commercial-scale Protein A capture in single-use continuous bioprocessing configurations. |

| Bio-Rad Laboratories | USA | Leader | Nuvia HP-Q Ion Exchange Resin | North America / Europe | Sep 2025: Launched a new mixed-mode chromatography resin for polishing steps in bispecific antibody purification, addressing increasing customer complexity in downstream processing. |

| Thermo Fisher Scientific | USA | Challenger | POROS HS Cation Exchange Resin | North America / Global | Mar 2025: Expanded single-use pre-packed chromatography column portfolio, adding 20 L and 60 L clinical and commercial scale columns for cation exchange and anion exchange applications. |

| Repligen Corporation | USA | Challenger | OPUS Pre-Packed Chromatography Columns | North America / Europe | Jun 2025: Secured GMP qualification of its OPUS 45 large-scale pre-packed column for commercial mAb purification at multiple major CDMO sites across North America. |

| Tosoh Bioscience | Japan | Challenger | Toyopearl AF-rProtein A HC-650F | Asia Pacific / Global | Nov 2024: Introduced an alkali-stable Protein A resin variant enabling extended lifetime under CIP conditions, targeting biosimilar manufacturers seeking multi-cycle resin utilization programs. |

| Purolite (Ecolab) | UK | Challenger | Praesto AC Protein A Resin | Europe / North America | May 2025: Expanded Purolite Praesto AC Protein A resin production at its UK facility, adding 30% additional capacity to reduce lead times for clinical and commercial CDMO customers. |

| Astrea Bioseparations | UK | Niche Player | HyperCel STAR AX Mixed-Mode Resin | Europe / North America | Aug 2025: Launched a new HyperCel STAR AX variant optimized for AAV vector purification, expanding its mixed-mode resin portfolio to address the growing gene therapy downstream processing market. |

| BioChrom (Reprocell) | UK | Niche Player | BioChrom Cell Culture Media & Buffer Solutions | Europe | Jan 2025: Partnered with a European biosimilar CDMO to supply custom buffer and resin solutions as part of an integrated downstream development support agreement. |

By Product Type

The bioprocess chromatography market by product type is led by chromatography resins and media, which account for approximately 54.2% of total market revenue in 2025 at USD 3.89 Billion. Chromatography resins are the consumable element of downstream bioprocessing — they are used for a defined number of cycles before replacement, creating a predictable recurring revenue stream for suppliers tied directly to biopharmaceutical manufacturing output volume. Protein A affinity resins represent the highest-value segment within the resin category, with commercial-grade resins from Cytiva, Merck KGaA, Sartorius, Tosoh, and Purolite priced at USD 6,000–14,000 per liter and consumed in quantities ranging from tens of liters for clinical manufacturing to thousands of liters for large-scale commercial campaigns. Ion exchange resins — including cation exchange media such as SP Sepharose and Capto SP ImpRes, and anion exchange media including Q Sepharose and Capto Q — account for the second-largest resin sub-segment, with applications across antibody polishing, DNA clearance, and bispecific antibody intermediate purification. Membrane adsorbers, which use functionalized membrane structures rather than packed bead columns for high-capacity capture and flow-through polishing applications, are a growing subset of the resin/media category at approximately 8.4% of total market revenue in 2025. Chromatography systems and hardware account for 26.4% of market revenue at USD 1.90 Billion. Pre-packed columns account for 19.4% at USD 1.39 Billion.

By Chromatography Mode

By chromatography mode, affinity chromatography — primarily Protein A affinity capture — leads the bioprocess chromatography market with approximately 46.8% of revenue in 2025 at USD 3.36 Billion. Protein A chromatography is the universal capture step for IgG monoclonal antibodies, functioning as the first purification step after bioreactor harvest clarification. Protein A ligands bind specifically to the Fc region of IgG antibodies with high affinity, enabling one-step capture from clarified cell culture supernatant at purities exceeding 95% in a single column pass. The dominance of Protein A affinity in the mAb purification platform is structurally locked in by regulatory precedent: hundreds of approved mAb products have been purified using Protein A capture, and any deviation from this platform requires extensive comparative process characterization during BLA or MAA submissions. Ion exchange chromatography accounts for 30.2% of market revenue in 2025 at USD 2.17 Billion, encompassing both capture and polishing applications across mAb, recombinant protein, and biosimilar purification trains. Hydrophobic interaction chromatography (HIC) contributes 10.6% of market revenue, primarily as an intermediate polishing step for mAb and recombinant protein purification where aggregate and misfolded protein removal is required. Size exclusion chromatography (SEC), primarily used as an analytical tool and final polishing step, accounts for 7.4% of revenue. Mixed-mode and multimodal chromatography resins represent the remaining 5.0% and are the fastest-growing mode at an estimated 16.8% CAGR through 2034.

By Application

By application, monoclonal antibody purification accounts for 48.6% of bioprocess chromatography market revenue in 2025 at USD 3.49 Billion. This segment encompasses affinity capture, cation exchange polishing, anion exchange flow-through, and SEC final polishing steps across commercial and clinical mAb manufacturing campaigns globally. The commercial mAb market's scale — exceeding USD 230 Billion in annual sales in 2025 — ensures that mAb purification remains the primary application by revenue in the bioprocess chromatography market through 2034. Recombinant protein and enzyme purification accounts for 20.4% of market revenue at USD 1.47 Billion, including purification of recombinant clotting factors, enzymes for enzyme replacement therapy, and growth factors. Biosimilar manufacturing represents 15.8% of market revenue at USD 1.13 Billion, a share growing at 14.6% annually as the biosimilar development pipeline matures. Viral vector purification for gene therapy drug substances accounts for 9.2% of revenue at USD 0.66 Billion and is the fastest-growing application segment at an estimated 22.4% CAGR through 2034, as commercial gene therapy manufacturing increasingly requires scalable downstream chromatography processes for AAV and lentiviral vector purification. Vaccine and plasma protein fractionation applications contribute the remaining 6.0%.

By End-User

By end-user, biopharmaceutical manufacturers are the largest purchaser segment within the bioprocess chromatography market, generating 52.8% of revenue in 2025 at USD 3.79 Billion. Large integrated pharmaceutical companies operating their own bioreactor and downstream processing infrastructure — including manufacturers of approved mAbs, recombinant proteins, and vaccines — account for the majority of commercial-scale resin and system procurement. CDMOs represent 31.6% of market revenue at USD 2.27 Billion, with their multiple parallel client campaigns creating high aggregate chromatography consumable consumption. CDMO operators are particularly significant buyers of Protein A resins, ion exchange resins, and pre-packed columns that enable rapid turnover between client product campaigns without full column regeneration and re-packing. Academic research institutes and biopharmaceutical research organizations account for 10.4% of market revenue, purchasing smaller quantities of analytical and preparative chromatography resins for process development and research activities. Government and public health biologic manufacturers account for the remaining 5.2%.

Regional Analysis

North America Bioprocess Chromatography Market

North America holds the leading position in the global bioprocess chromatography market with a 41.8% share in 2025, generating approximately USD 3.00 Billion in revenue. The United States is the world's largest individual bioprocess chromatography market, anchored by the highest concentration of FDA-approved biologic drug products, the most extensive CDMO downstream processing infrastructure globally, and a sustained pipeline of biologic drug manufacturing capacity investments. Major integrated pharmaceutical companies in New Jersey, Massachusetts, Indiana, and California operate large-scale downstream bioprocessing suites consuming substantial volumes of Protein A resin, ion exchange media, and chromatography hardware. US-based biologic CDMOs — including Lonza Portsmouth, Baxter BioPharma Solutions, and Catalent Biologics — are significant buyers of commercial-grade resins and pre-packed columns for multi-product, multi-client downstream processing campaigns. The FDA's process validation guidance and its downstream process characterization expectations under the BLA review framework define quality and documentation requirements for US-market purification processes, reinforcing demand for well-characterized, FDA-accepted chromatography platforms. Canada contributes incrementally through biopharmaceutical development and manufacturing programs in Ontario and Quebec. North America's bioprocess chromatography market is projected to grow at a 10.8% CAGR through 2034, reaching approximately USD 7.24 Billion.

Europe Bioprocess Chromatography Market

Europe represents 29.2% of the global bioprocess chromatography market in 2025 at approximately USD 2.10 Billion. Germany, Switzerland, Ireland, and the United Kingdom are the primary national markets, collectively hosting major biopharmaceutical manufacturing operations, world-class CDMO downstream processing capacity, and the principal bioprocess chromatography resin and equipment manufacturers. Germany-headquartered Cytiva (its European operations) and Merck KGaA are among the two most significant bioprocess chromatography companies globally, providing Europe with both supply-side dominance and substantial domestic demand generation from their respective R&D and applications development operations. Switzerland's biopharma cluster — with Novartis, Roche, and Lonza Visp operating major biologics manufacturing sites — generates significant recurring Protein A and ion exchange resin procurement. Ireland's growing biopharmaceutical manufacturing hub, hosting the European operations of Pfizer, AstraZeneca, and MSD, drives demand for downstream processing consumables at commercial scale. The EMA's downstream process characterization requirements for BLA and MAA submissions in the EU reinforce the use of well-validated, recognized chromatography platforms. Europe's bioprocess chromatography market is projected to grow at a 11.2% CAGR through 2034.

Asia Pacific Bioprocess Chromatography Market

Asia Pacific accounts for 20.4% of the global bioprocess chromatography market in 2025 at USD 1.46 Billion and is the fastest-growing region with a projected CAGR of 14.2% through 2034. China is the largest and fastest-growing national market, driven by an expanding domestic biopharmaceutical manufacturing sector that is building commercial-scale downstream bioprocessing capability to serve both the domestic market and global pharmaceutical outsourcing clients. Chinese biopharmaceutical manufacturers are procuring Protein A resins from both international suppliers — Cytiva, Merck KGaA — and from domestic resin producers including Bestchrom and NanoMicro Technology, with domestic resins gaining share on cost grounds for biosimilar manufacturing campaigns. South Korea's Samsung Biologics operates one of the world's largest single-site biologics CDMO campuses, consuming substantial quantities of downstream bioprocessing resins and hardware annually. Japan's biopharmaceutical sector, with established downstream processing infrastructure at companies including Chugai (Roche subsidiary) and Daiichi Sankyo, provides a mature but growing market for bioprocess chromatography. India's expanding biosimilar manufacturing sector is a growing buyer of Protein A resins and ion exchange media, as domestic biosimilar producers pursue FDA and EMA approvals for the global market. Asia Pacific's bioprocess chromatography market is the primary growth opportunity for established suppliers through 2034.

Latin America Bioprocess Chromatography Market

Latin America holds a 5.2% share of the bioprocess chromatography market in 2025 at approximately USD 0.37 Billion. Brazil is the dominant regional market, where biopharmaceutical manufacturers including Fiocruz — which operates large-scale vaccine and biologic drug manufacturing — procure chromatography resins and systems for downstream processing. Fiocruz's technology transfer programs with global vaccine manufacturers include downstream purification process transfer, driving demand for international-specification chromatography resins aligned with BLA or WHO PQ submissions. Mexico's pharmaceutical sector, while primarily small-molecule oriented, includes some biopharmaceutical development capacity generating chromatography demand. Argentina's domestic pharmaceutical industry contributes incremental demand through biologic development programs targeting regional markets. The Latin American bioprocess chromatography market is primarily dependent on imported resins and systems from North American and European suppliers. Lead times, import duties, and currency volatility add procurement complexity. Nonetheless, growing regional biopharmaceutical manufacturing ambition is attracting investment from international chromatography suppliers establishing regional distribution and technical support infrastructure. Latin America's bioprocess chromatography market is projected to grow at a 9.8% CAGR through 2034.

Middle East & Africa Bioprocess Chromatography Market

The Middle East and Africa region accounts for 3.4% of global bioprocess chromatography market revenue in 2025 at approximately USD 0.24 Billion. The GCC countries — particularly Saudi Arabia and the UAE — are the primary demand centers, where national biopharmaceutical manufacturing programs under Vision 2030 and equivalent strategies are investing in biologic drug production infrastructure including downstream purification capability. Saudi Arabia's SFDA and the UAE's Ministry of Health have adopted GMP standards aligned with WHO and ICH guidelines, supporting regulatory acceptance of chromatography process documentation prepared to international standards. South Africa's biopharmaceutical sector — the most developed in sub-Saharan Africa — contributes downstream bioprocessing demand through biosimilar and vaccine manufacturing programs. The African Vaccine Manufacturing Accelerator (AVMA) is supporting investment in African vaccine manufacturing, which includes downstream purification infrastructure requiring chromatography equipment and resins. MEA's bioprocess chromatography market is expected to grow at a 12.4% CAGR through 2034, driven by healthcare infrastructure investment, domestic biologic manufacturing programs, and biosimilar development initiatives across the GCC and key African markets.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Chromatography Resins & Media

- Chromatography Systems & Hardware

- Pre-Packed Chromatography Columns

- Membrane Adsorbers

By Chromatography Mode

- Affinity Chromatography (Protein A / Protein G / Others)

- Ion Exchange Chromatography (Cation & Anion Exchange)

- Hydrophobic Interaction Chromatography (HIC)

- Size Exclusion Chromatography (SEC)

- Mixed-Mode & Multimodal Chromatography

By Application

- Monoclonal Antibody Purification

- Recombinant Protein & Enzyme Purification

- Biosimilar Manufacturing

- Viral Vector Purification (Gene Therapy)

- Vaccine & Plasma Protein Fractionation

By End-User

- Biopharmaceutical Manufacturers

- Contract Development & Manufacturing Organizations (CDMOs)

- Academic Research Institutes & Process Development Labs

- Government & Public Health Manufacturers

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 7.18 B |

| Forecast Revenue (2034) | USD 19.24 B |

| CAGR (2025-2034) | 11.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Chromatography Resins & Media, Chromatography Systems & Hardware, Pre-Packed Chromatography Columns, Membrane Adsorbers), By Chromatography Mode, (Affinity Chromatography (Protein A / Protein G / Others), Ion Exchange Chromatography (Cation & Anion Exchange), Hydrophobic Interaction Chromatography (HIC), Size Exclusion Chromatography (SEC), Mixed-Mode & Multimodal Chromatography), By Application, (Monoclonal Antibody Purification, Recombinant Protein & Enzyme Purification, Biosimilar Manufacturing, Viral Vector Purification (Gene Therapy), Vaccine & Plasma Protein Fractionation), By End-User, (Biopharmaceutical Manufacturers, Contract Development & Manufacturing Organizations (CDMOs), Academic Research Institutes & Process Development Labs, Government & Public Health Manufacturers) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CYTIVA (DANAHER), MERCK KGAA (MILLIPORESIGMA), SARTORIUS AG, BIO-RAD LABORATORIES, THERMO FISHER SCIENTIFIC, REPLIGEN CORPORATION, TOSOH BIOSCIENCE, PUROLITE (ECOLAB), ASTREA BIOSEPARATIONS, BIOCHROM (REPROCELL), BESTCHROM (SUZHOU), KANEKA CORPORATION, JSR CORPORATION (JSRBIO), AVANTOR (VWR), PALL CORPORATION (DANAHER), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Chromatography Mode (Affinity Chromatography, Ion Exchange Chromatography, Hydrophobic Interaction Chromatography, Size Exclusion Chromatography, Mixed-Mode & Multimodal Chromatography), By Application, End-User, Industry Trends, Competitive Landscape, Regional Outlook & Forecast 2026-2034")

, By Chromatography Mode (Affinity Chromatography, Ion Exchange Chromatography, Hydrophobic Interaction Chromatography, Size Exclusion Chromatography, Mixed-Mode & Multimodal Chromatography), By Application, End-User, Industry Trends, Competitive Landscape, Regional Outlook & Forecast 2026-2034")

, By Chromatography Mode (Affinity Chromatography, Ion Exchange Chromatography, Hydrophobic Interaction Chromatography, Size Exclusion Chromatography, Mixed-Mode & Multimodal Chromatography), By Application, End-User, Industry Trends, Competitive Landscape, Regional Outlook & Forecast 2026-2034")

Frequently Asked Questions

How big is the Bioprocess Chromatography Market?

The Global Bioprocess Chromatography Market was valued at USD 6.43 Billion in 2024 and is projected to reach USD 19.24 Billion by 2034, growing at a CAGR of 11.6% from 2026 to 2034, driven by high-titer cell line adoption and intelligent mixed-mode resin innovations.

Who are the major players in the Bioprocess Chromatography Market?

CYTIVA (DANAHER), MERCK KGAA (MILLIPORESIGMA), SARTORIUS AG, BIO-RAD LABORATORIES, THERMO FISHER SCIENTIFIC, REPLIGEN CORPORATION, TOSOH BIOSCIENCE, PUROLITE (ECOLAB), ASTREA BIOSEPARATIONS, BIOCHROM (REPROCELL), BESTCHROM (SUZHOU), KANEKA CORPORATION, JSR CORPORATION (JSRBIO), AVANTOR (VWR), PALL CORPORATION (DANAHER), Others

Which segments covered the Bioprocess Chromatography Market?

By Product Type, (Chromatography Resins & Media, Chromatography Systems & Hardware, Pre-Packed Chromatography Columns, Membrane Adsorbers), By Chromatography Mode, (Affinity Chromatography (Protein A / Protein G / Others), Ion Exchange Chromatography (Cation & Anion Exchange), Hydrophobic Interaction Chromatography (HIC), Size Exclusion Chromatography (SEC), Mixed-Mode & Multimodal Chromatography), By Application, (Monoclonal Antibody Purification, Recombinant Protein & Enzyme Purification, Biosimilar Manufacturing, Viral Vector Purification (Gene Therapy), Vaccine & Plasma Protein Fractionation), By End-User, (Biopharmaceutical Manufacturers, Contract Development & Manufacturing Organizations (CDMOs), Academic Research Institutes & Process Development Labs, Government & Public Health Manufacturers)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Bioprocess Chromatography Market

Published Date : 06 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date