- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Bioresorbable Polymer Market Size & Forecast 2034 | CAGR 11.9%

Global Bioresorbable Polymer Market Size, Share, Growth Analysis By Polymer Type (Polylactic Acid - PLA, Polyglycolic Acid - PGA, Polycaprolactone - PCL, Polydioxanone - PDO), By Application (Drug Delivery, Orthopedic, Cardiovascular Devices, Wound Care), By Form (Fibers, Films, Microspheres, Implants), By End-User (Hospitals, Medical Device Firms, Pharma) Regional Outlook, Key Players – Dynamics, Biomedical Material Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 1.70 Billion | USD 4.67 Billion | 11.9% | North America, 38.0% |

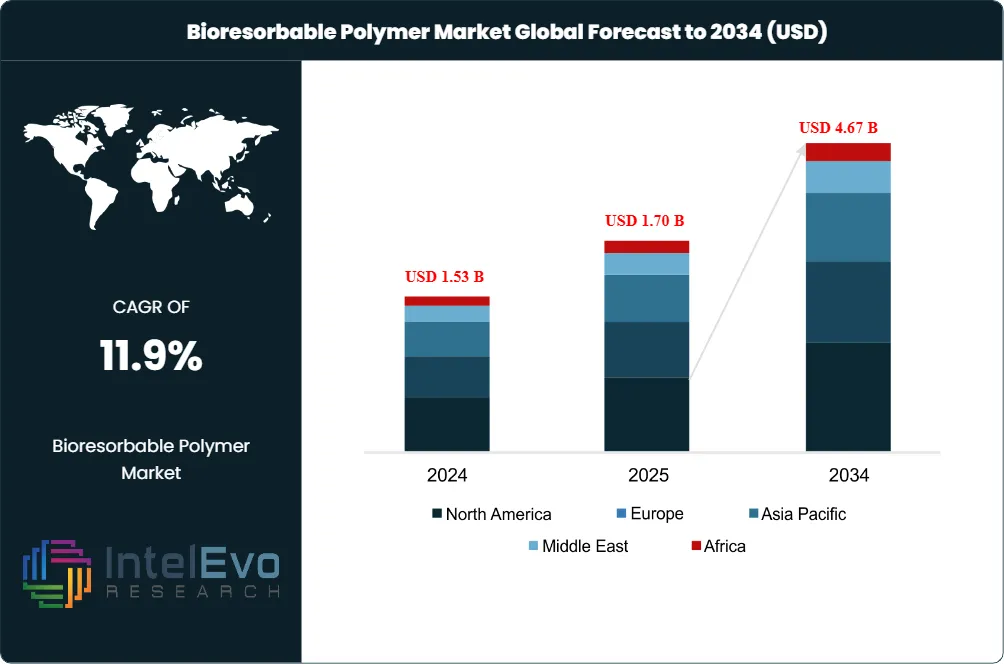

The Bioresorbable Polymer Market was valued at USD 1.53 Billion in 2024 and is estimated to reach USD 1.70 Billion in 2025. The market is projected to reach USD 4.67 Billion by 2034, expanding at a CAGR of 11.9% during the forecast period (2026–2034). This represents an absolute dollar opportunity of USD 2.97 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportThe bioresorbable polymer market is advancing because orthopedic fixation, drug delivery, soft-tissue repair, and vascular scaffolding now require temporary mechanical performance rather than permanent implant residence. Demand is concentrated in medical-grade poly(L-lactide), poly(D,L-lactide), poly(lactic-co-glycolic acid), polycaprolactone, polydioxanone, and poly-4-hydroxybutyrate materials used by Abbott, Evonik Industries, Corbion, Ashland, and Poly-Med.

Regulatory acceptance improved after the U.S. Food and Drug Administration approved Abbott Medical's Esprit BTK Everolimus Eluting Resorbable Scaffold System on 26 April 2024. The device uses a PLLA scaffold backbone, a PDLLA-everolimus coating, and a total scaffolding length up to 170 mm for infrapopliteal lesions in chronic limb-threatening ischemia.

The bioresorbable polymer market benefits from the shift from removal-dependent implants toward temporary materials that degrade through hydrolysis, enzymatic action, or surface erosion. ISO 10993-1 biological evaluation, ISO 10993-13 polymer degradation-product analysis, ISO 10993-17 toxicological risk assessment, and EU MDR 2017/745 technical documentation now shape purchasing decisions because degradation chemistry must be proved before launch.

North America led with 38.0% share in 2025, equal to USD 0.65 Billion, because the United States combines FDA PMA pathways, cardiovascular device adoption, orthopedic procedure volume, and a large outsourced medical-device manufacturing base. Europe followed with 30.0% share, supported by Corbion's Netherlands operations, Evonik's German RESOMER portfolio, dsm-firmenich biomedical processing capability, and EU MDR demand for documented material traceability.

Through 2034, the bioresorbable polymer market will grow fastest in controlled-release drug delivery and cardiovascular scaffolds, while sutures and surgical meshes remain durable revenue anchors. The most attractive procurement opportunities sit in polymers that combine narrow molecular-weight distribution, endotoxin control, predictable loss of strength, and regulatory master-file support for Class IIb and Class III medical devices.

Market Definition & Scope

The bioresorbable polymer market is defined as the global commercial activity surrounding medical-grade polymers that temporarily perform inside the body and then break down into metabolites, soluble products, or absorbable fragments after their function is complete. The market encompasses PLA, PLLA, PDLLA, PLGA, PCL, PDO, PGA, P4HB, lactide-caprolactone copolymers, and custom blends used in implants, sutures, meshes, scaffolds, coatings, and long-acting injectables.

This analysis includes polymer resin, custom synthesis, compounding, extrusion, fiber, film, scaffold, and implant-grade intermediate materials sold into medical devices and drug delivery. It excludes general compostable packaging polymers, non-resorbable medical polymers such as PEEK and UHMWPE, permanent metallic implants, and finished device revenue unless polymer value is separable. The bioresorbable polymer market sits inside the broader medical biomaterials category, where polymer suppliers capture a smaller but higher-validation portion of device economics.

, By Application (Drug Delivery, Orthopedic, Cardiovascular Devices, Wound Care), By Form (Fibers, Films, Microspheres, Implants), By End-User (Hospitals, Medical Device Firms, Pharma) Regional Outlook, Key Players – Dynamics, Biomedical Material Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The bioresorbable polymer market increased to USD 1.70 Billion in 2025 and is projected to reach USD 4.67 Billion by 2034 at an 11.9% CAGR.

- Segment Dominance: PLA, PLLA, and PDLLA materials led by type with 36.5% share in 2025, equal to about USD 0.62 Billion.

- Segment Dominance: Orthopedic and sports-medicine implants led by application with 31.0% share in 2025, equal to USD 0.53 Billion.

- Driver: The primary driver is avoidance of secondary removal surgery, supported by FDA-cleared resorbable scaffolds and broader Class III implant adoption.

- Restraint: Processing risk remains material, because hydrolytic degradation, residual monomer content, and sterilization effects can shift strength retention by months.

- Opportunity: Controlled-release drug delivery represents approximately USD 1.28 Billion in incremental 2025-2034 opportunity as PLGA and PCL systems move into long-acting injectables.

- Trend: Cardiovascular scaffolds re-entered clinical use after Abbott's Esprit BTK approval and August 2025 CE Mark, creating demand for PLLA and PDLLA coatings.

- Regional: North America led the bioresorbable polymer market with 38.0% share and USD 0.65 Billion in 2025, ahead of Europe at USD 0.51 Billion.

Key Insights Summary

- Abbott Medical's Esprit BTK PMA, approved on 26 April 2024, covers infrapopliteal chronic limb-threatening ischemia lesions up to 170 mm in total scaffolding length.

- The Esprit BTK scaffold uses a 100% poly(L-lactide) backbone and a poly(D,L-lactide)-everolimus coating with 100 micrograms per square centimeter of everolimus.

- FDA's September 2023 ISO 10993-1 guidance applies biological evaluation to PMAs, IDEs, HDEs, 510(k)s, and De Novo requests, raising documentation expectations for degradable polymer devices.

- ISO 10993-13 addresses identification and quantification of degradation products from polymeric medical devices, making degradation-product toxicology central to resorbable implant approvals.

- Corbion generated EUR 1,267.4 Million in 2025 sales, while its Pharma and Biomaterials businesses supplied resorbable polymers for medicines, medical devices, and controlled drug delivery.

- Ashland added viatel bioresorbable polymer grades in June 2025 for long-acting injectables, medical devices, regenerative medicine, dermal fillers, and aesthetic-medicine uses.

- An IISc and Aster CMI Hospital team licensed a polydioxanone Asthana Stent in April 2026 after laboratory and bile testing, targeting bile-duct healing after abdominal surgery.

Competitive Landscape Overview

The bioresorbable polymer market is moderately consolidated by medical-grade chemistry capability, regulatory file depth, and long-cycle customer validation. Evonik Industries, Corbion, Ashland, and Poly-Med hold an estimated 48% combined share of commercial medical-grade bioresorbable polymer supply in 2025, while BASF, dsm-firmenich, Foster Corporation, and Zeus compete through compounding, processing, and specialty grades.

Competition is less price-based than validation-based because customers require ISO 13485 supply discipline, biocompatibility data packages, stability history, sterilization support, and lot-to-lot molecular-weight consistency. The competitive shift in 2025 and 2026 favors suppliers that can bridge resin synthesis, custom copolymer design, drug-release tuning, extrusion, and regulatory documentation rather than selling only catalog PLA or PLGA.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Evonik Industries AG | Germany | Leader | RESOMER bioresorbable polymers | Europe, North America, Asia | Expanded medical-device RESOMER positioning during 2025 with tunable degradation polymers for implants and drug delivery. |

| Corbion N.V. | Netherlands | Leader | PURASORB medical-grade resorbable polymers | Europe, North America, Asia | Reported 2025 Pharma and Biomaterials activity tied to medicines, medical devices, and controlled-release formulations. |

| Ashland Inc. | United States | Leader | viatel bioresorbable polymers | North America, Europe | Added viatel grades in June 2025 for devices, long-acting injectables, regenerative medicine, and aesthetics. |

| Poly-Med, Inc. | United States | Leader | PDO, PGLA, Glycoprene, Lactoprene, Strataprene | North America, device outsourcing hubs | Promoted vertically integrated polymer-to-device manufacturing for absorbable textiles, fibers, and films during 2025. |

| BASF SE | Germany | Challenger | Medical polymers and biodegradable intermediates | Europe, Asia, Americas | Focused specialty materials toward medical applications and circular polymer chemistry in 2025 reporting. |

| dsm-firmenich Biomedical | Switzerland | Challenger | Bioresorbable processing and polymer composites | Europe, United States | Advanced implant processing and polymer-composite services across orthopedic, vascular, and wound-care uses. |

| Foster Corporation | United States | Challenger | Custom medical polymer compounding | North America, Europe | Supported resorbable polymer compounding programs for device OEMs. |

| Zeus Company LLC | United States | Niche Player | Medical polymer tubing and processing | North America, global OEMs | Expanded medical polymer processing services for implantable-device applications. |

Segmentation Analysis

The bioresorbable polymer market segments by polymer type, application, form, and end-user, with economics determined by polymer chemistry, device risk class, validation burden, and the buyer's ability to qualify an alternate supplier.

By Polymer Type

The bioresorbable polymer market by polymer type is led by PLA, PLLA, and PDLLA materials, which represented 36.5% share and USD 0.62 Billion in 2025. Evonik RESOMER, Corbion PURASORB, and Abbott's Esprit BTK supply chain illustrate why lactide-based chemistry remains the default for load-bearing scaffolds, sutures, orthopedic fixation, and drug-eluting coatings. PLLA offers strength retention for months to years, while PDLLA coatings can tune drug release and resorption around cardiovascular and orthopedic healing windows.

PLGA accounted for 27.0% share and USD 0.46 Billion in 2025 because lactide-glycolide ratios permit degradation windows from weeks to months. Ashland viatel, Corbion PURASORB, and Evonik RESOMER platforms address long-acting injectables, microspheres, and implantable drug depots where polymer molecular weight, end-group chemistry, and residual solvent control determine release kinetics. PLGA will outgrow PLLA through 2034 because GLP-1, oncology, veterinary, and endocrine formulations increasingly require multi-month release profiles.

PCL, PDO, PGA, P4HB, and specialty copolymers represented the remaining 36.5% share in 2025, equal to USD 0.62 Billion. Poly-Med offers PDO and PGLA materials for absorbable fibers, films, and textiles, while BD's Tepha-related P4HB technology supports soft-tissue repair and surgical mesh. PCL is slower to degrade than PLGA, making it suited to drug delivery and regenerative medicine where mechanical or release function must persist beyond six months.

By Application

The bioresorbable polymer market by application is led by orthopedic and sports-medicine implants, which held 31.0% share and USD 0.53 Billion in 2025. KLS Martin, Osteopore, Poly-Med, Evonik, and dsm-firmenich serve screws, pins, plates, suture anchors, craniofacial meshes, and osteoconductive constructs. Orthopedic users value predictable strength loss because premature mass loss can weaken fixation, while delayed degradation can create long-term inflammation risk.

Drug delivery accounted for 27.2% share and USD 0.46 Billion in 2025, with the fastest CAGR through 2034. PLGA microspheres, PCL depots, lactide-caprolactone copolymers, and injectable matrices are used to release small molecules, peptides, hormones, vaccines, and nucleic-acid cargos. Ashland's June 2025 viatel additions and Corbion's controlled-release activity show why procurement teams now assess polymer vendor qualification alongside formulation-development support.

Cardiovascular scaffolds, sutures, surgical meshes, tissue engineering, and dental or craniofacial uses made up 41.8% share in 2025. Abbott's Esprit BTK system restored confidence in PLLA scaffold designs for below-the-knee disease, while IISc's 2026 polydioxanone bile-duct stent indicates a broader pipeline of temporary hollow-organ devices. Sutures remain the volume base, but cardiovascular and regenerative medicine deliver higher value per kilogram of polymer.

By Form

Resin and pellet form led the bioresorbable polymer market with 44.0% share and USD 0.75 Billion in 2025 because medical-device OEMs and contract manufacturers often perform extrusion, molding, fiber spinning, and coating in qualified facilities. Evonik, Corbion, Ashland, and BASF sell polymer grades into validated production chains where small changes in inherent viscosity or residual monomer can require device revalidation.

Fibers, films, tubes, microspheres, coatings, and custom-compounded forms represented 56.0% share in 2025 and are growing faster than commodity resin. Poly-Med's absorbable textiles, dsm-firmenich polymer processing, Foster Corporation compounding, and Zeus tubing demonstrate the value shift toward intermediate forms that reduce OEM process risk. In procurement terms, pre-processed forms lower the implementation timeline but create deeper supplier dependency.

By End-User

Medical-device OEMs accounted for 55.5% of bioresorbable polymer market revenue in 2025, equivalent to USD 0.94 Billion. Abbott, BD, KLS Martin, Osteopore, and specialized contract manufacturers pull demand through vascular, soft-tissue, sports-medicine, and craniofacial device programs. OEM qualification cycles typically run 18 to 36 months because polymer selection affects biocompatibility, mechanical testing, sterilization, packaging, and shelf-life evidence.

Pharmaceutical and biotechnology companies represented 25.0% share and USD 0.43 Billion in 2025, mainly through controlled-release injectables and implantable depots. Academic hospitals, research institutes, and regenerative-medicine developers held 11.5% share, while dental, aesthetic, and veterinary users accounted for 8.0%. The bioresorbable polymer vendor procurement checklist differs by buyer: device firms prioritize master files and mechanical aging data, while drug developers prioritize release reproducibility, extractables, and CMC support.

Regional Analysis

The bioresorbable polymer market is concentrated in North America and Europe, while Asia Pacific records the fastest growth because medical-device manufacturing, local regulatory capacity, and hospital procedure volumes are expanding together.

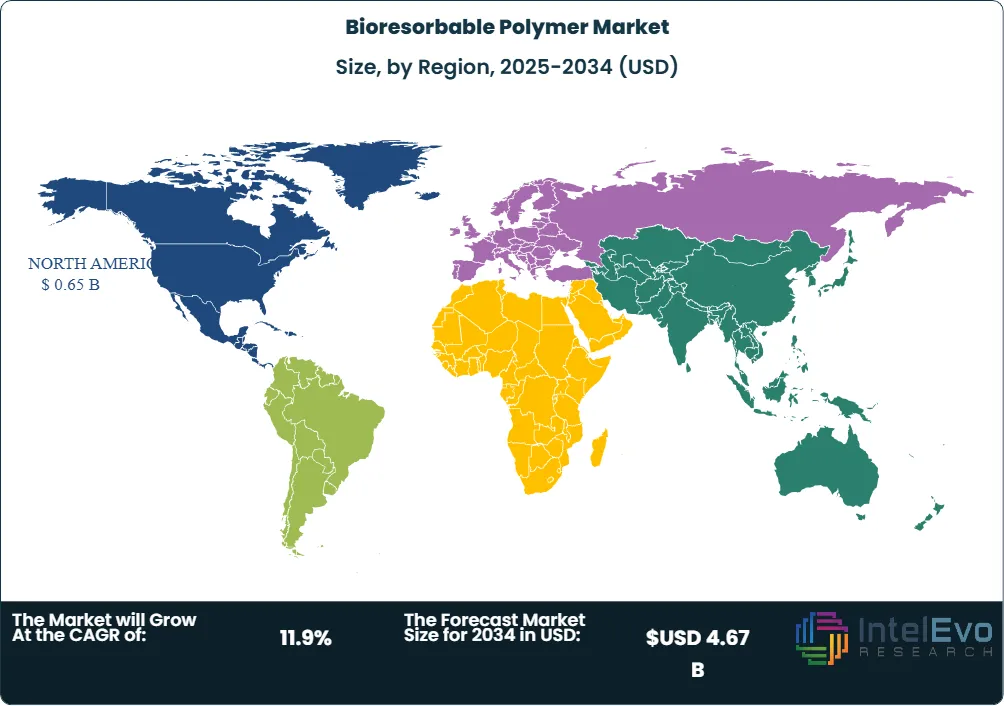

North America led the bioresorbable polymer market with 38.0% share and USD 0.65 Billion in 2025. The United States accounted for most regional value because FDA PMA, IDE, 510(k), and De Novo pathways create structured routes for absorbable medical devices. Abbott Medical, Ashland, Poly-Med, Foster Corporation, Zeus, BD, and major contract manufacturers anchor regional supply. The April 2024 FDA approval of Esprit BTK and FDA supplement activity through August 2025 strengthened buyer confidence in polymeric scaffold programs.

Europe held 30.0% share and USD 0.51 Billion in 2025, led by Germany, the Netherlands, Switzerland, France, and Ireland. Evonik, Corbion, dsm-firmenich, BASF, Seqens, and KLS Martin make Europe the deepest region for polymer chemistry, medical-device engineering, and regulatory documentation. EU MDR 2017/745 creates demanding clinical and post-market evidence requirements, which favors suppliers with long master-file histories and traceable quality systems. Abbott's August 2025 CE Mark for Esprit BTK added a near-term demand catalyst for resorbable cardiovascular materials.

Asia Pacific accounted for 23.0% share and USD 0.39 Billion in 2025 and is forecast to outpace other regions through 2034. Japan, China, India, Singapore, and South Korea combine device manufacturing, clinical research, and hospital infrastructure investment. India's IISc-Aster polydioxanone Asthana Stent licensing in April 2026 shows how domestic research can create region-specific resorbable devices. Japan's PMDA, China's NMPA, and India's CDSCO are increasing technical scrutiny, which supports premium suppliers that can provide degradation and toxicology evidence.

Latin America represented 5.5% share and USD 0.09 Billion in 2025, with Brazil and Mexico leading consumption. Demand is tied to orthopedic trauma, dental surgery, soft-tissue repair, and private-hospital adoption. Import dependence remains high, so procurement teams often favor globally validated polymer suppliers working through regional device OEMs. Currency volatility and slower reimbursement limit high-value cardiovascular scaffold uptake.

Middle East and Africa held 3.5% share and USD 0.06 Billion in 2025. Saudi Arabia, the United Arab Emirates, Israel, South Africa, and Türkiye drive most demand through specialty hospitals and medical-device distributors. Adoption is concentrated in premium orthopedic, wound, and reconstructive procedures. Local manufacturing is limited, but Saudi Vision 2030, UAE health-tech investment, and Israeli biomaterials research create selective opportunities for resorbable meshes, craniofacial implants, and drug-delivery systems.

Country Analysis

The United States bioresorbable polymer market reached USD 0.58 Billion in 2025 and is projected to grow at an 11.4% country CAGR through 2034. Demand is supported by FDA-regulated implant pathways, high orthopedic procedure volume, and cardiovascular adoption following Esprit BTK approval. Abbott Medical's PMA and FDA ISO 10993-1 guidance raised the importance of supplier evidence packages. Ashland, Poly-Med, Foster Corporation, Zeus, BD, and device-focused contract manufacturers create a local supply base for custom copolymers, absorbable fibers, films, and resorbable implant components.

Germany's bioresorbable polymer market reached USD 0.16 Billion in 2025, with a 10.8% country CAGR projected through 2034. Evonik Industries and BASF anchor specialty-polymer chemistry, while KLS Martin and German hospital networks support craniofacial, orthopedic, and reconstructive-device demand. EU MDR technical documentation, ISO 10993 testing, and notified-body capacity are central constraints. Germany's advantage is integration between polymer synthesis, medical engineering, sterilization validation, and high-value export manufacturing.

The Netherlands bioresorbable polymer market reached USD 0.12 Billion in 2025 and is forecast to grow at an 11.6% CAGR through 2034. Corbion's PURASORB portfolio makes the country a global node for lactide-based medical polymers and drug-delivery materials. Dutch strength sits in lactic-acid chemistry, controlled-release formulation support, and access to EU clinical and regulatory infrastructure. Corbion's 2025 reporting tied its Pharma and Biomaterials businesses to resorbable polymers used in medicines and medical devices.

India's bioresorbable polymer market reached USD 0.07 Billion in 2025 and is forecast to grow at a 14.8% CAGR through 2034. Domestic demand is driven by trauma care, abdominal surgery, dental implants, wound repair, and lower-cost device manufacturing. The IISc and Aster CMI Asthana Stent program, licensed in April 2026 with Indian patent protection, demonstrates local development of polydioxanone resorbable devices. CDSCO approval pathways and ICMR-supported clinical translation will determine whether India becomes a supplier base rather than only an import market.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Polymer Type

- Polylactic Acid (PLA)

- Polyglycolic Acid (PGA)

- Polycaprolactone (PCL)

- Polydioxanone (PDO)

- Others

By Application

- Drug Delivery

- Orthopedic Devices

- Cardiovascular Devices

- Wound Care

- Tissue Engineering

- Others

By Form

- Fibers

- Films

- Microspheres

- Implants

- Others

By End-User

- Hospitals

- Medical Device Manufacturers

- Pharmaceutical Companies

- Research Institutes

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.70 B |

| Forecast Revenue (2034) | USD 4.67 B |

| CAGR (2025-2034) | 11.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Polymer Type, (Polylactic Acid (PLA), Polyglycolic Acid (PGA), Polycaprolactone (PCL), Polydioxanone (PDO), Others), By Application, (Drug Delivery, Orthopedic Devices, Cardiovascular Devices, Wound Care, Tissue Engineering, Others), By Form, (Fibers, Films, Microspheres, Implants, Others), By End-User, (Hospitals, Medical Device Manufacturers, Pharmaceutical Companies, Research Institutes, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | EVONIK INDUSTRIES AG, CORBION N.V., ASHLAND INC., POLY-MED, INC., BASF SE, DSM-FIRMENICH BIOMEDICAL, FOSTER CORPORATION, ZEUS COMPANY LLC, SEQENS GROUP, KLS MARTIN GROUP, BD / TEPHA, INC., ABBOTT MEDICAL, REVA MEDICAL, LLC, OSTEOPORE LIMITED, NOMISMA HEALTHCARE PVT. LTD., ROQUETTE FRERES, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Drug Delivery, Orthopedic, Cardiovascular Devices, Wound Care), By Form (Fibers, Films, Microspheres, Implants), By End-User (Hospitals, Medical Device Firms, Pharma) Regional Outlook, Key Players – Dynamics, Biomedical Material Trends & Forecast 2026-2034")

, By Application (Drug Delivery, Orthopedic, Cardiovascular Devices, Wound Care), By Form (Fibers, Films, Microspheres, Implants), By End-User (Hospitals, Medical Device Firms, Pharma) Regional Outlook, Key Players – Dynamics, Biomedical Material Trends & Forecast 2026-2034")

, By Application (Drug Delivery, Orthopedic, Cardiovascular Devices, Wound Care), By Form (Fibers, Films, Microspheres, Implants), By End-User (Hospitals, Medical Device Firms, Pharma) Regional Outlook, Key Players – Dynamics, Biomedical Material Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Bioresorbable Polymer Market?

Global Bioresorbable Polymer Market was valued at USD 1.53 billion in 2024 and is projected to reach USD 4.67 billion by 2034, at a CAGR of 11.9% (2026–2034).

Who are the major players in the Bioresorbable Polymer Market?

EVONIK INDUSTRIES AG, CORBION N.V., ASHLAND INC., POLY-MED, INC., BASF SE, DSM-FIRMENICH BIOMEDICAL, FOSTER CORPORATION, ZEUS COMPANY LLC, SEQENS GROUP, KLS MARTIN GROUP, BD / TEPHA, INC., ABBOTT MEDICAL, REVA MEDICAL, LLC, OSTEOPORE LIMITED, NOMISMA HEALTHCARE PVT. LTD., ROQUETTE FRERES, OTHERS

Which segments covered the Bioresorbable Polymer Market?

By Polymer Type, (Polylactic Acid (PLA), Polyglycolic Acid (PGA), Polycaprolactone (PCL), Polydioxanone (PDO), Others), By Application, (Drug Delivery, Orthopedic Devices, Cardiovascular Devices, Wound Care, Tissue Engineering, Others), By Form, (Fibers, Films, Microspheres, Implants, Others), By End-User, (Hospitals, Medical Device Manufacturers, Pharmaceutical Companies, Research Institutes, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Bioresorbable Polymer Market

Published Date : 08 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date