- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Biotech Lab Construction Market Size & Forecast | CAGR 9.3%

Global Biotech Lab Construction Market Size, Share, Growth & Industry Analysis By Facility Type (cGMP Manufacturing Suites, BSL-2 & BSL-3 Labs, Genomics & HTS Labs, Vivaria, Pilot Labs), By Construction Type (Ground-Up, Renovation & Adaptive Reuse, Modular & Prefabricated), By End-User (Biopharma, CDMOs, Academic Institutes, Diagnostics, Biotech Startups) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

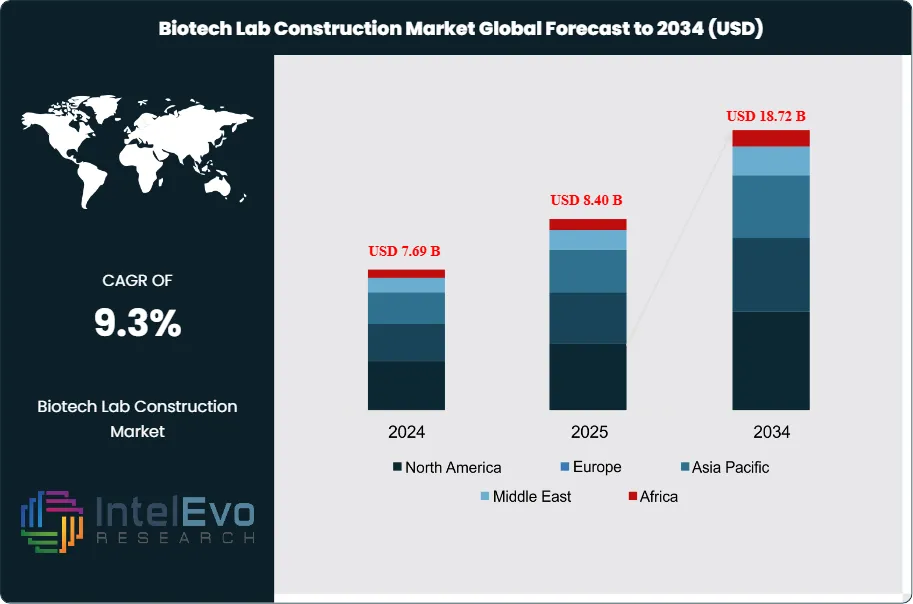

| USD 8.40 Billion | USD 18.72 Billion | 9.3% | North America, 42.3% |

The Biotech Lab Construction Market was valued at approximately USD 7.69 Billion in 2024 and reached USD 8.40 Billion in 2025. The market is projected to grow to USD 18.72 Billion by 2034, expanding at a CAGR of 9.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 10.32 Billion over the analysis period, driven by accelerating investment in life sciences infrastructure, clinical-stage biologic manufacturing, and gene and cell therapy facilities across developed and emerging economies.

Get More Information about this report -

Request Free Sample ReportBiotech lab construction encompasses the design, engineering, and construction of specialized facilities including biosafety level (BSL) 2, 3, and 4 laboratories, cGMP manufacturing suites, cleanrooms, vivaria, genomics and proteomics processing centers, and biocontainment research units. Demand for these highly regulated environments has risen sharply as biopharmaceutical companies expand pipeline capacity in oncology, immunotherapy, rare disease, and infectious disease verticals. The RMAT designation and accelerated approval pathways from the FDA have compressed timelines from discovery to manufacturing readiness, compelling organizations to begin facility planning substantially earlier in the development cycle.

The biotech lab construction market is also being shaped by intensified National Institutes of Health (NIH) funding streams, with domestic research funding reaching USD 47.4 Billion in fiscal year 2025 across universities, research hospitals, and independent institutes. This capital flows directly into construction and renovation budgets for specialized lab environments. Parallel to government investment, private venture capital commitments to biotech companies exceeded USD 38.0 Billion in 2025, a significant portion of which is earmarked for facility buildout ahead of clinical milestones and IND submissions.

From a supply side, the construction industry has responded by developing dedicated life sciences practices with deep expertise in HVAC redundancy systems, high-purity water distribution, containment airlock design, and vibration-controlled structural environments. Architecture, engineering, and construction (AEC) firms with biotech specialization command premium pricing and continue to see backlog expansion. The biotech lab construction market is benefiting from modular and prefabricated construction techniques that reduce project delivery timelines by 20–35% compared to conventional stick-built methods.

Asia Pacific and Europe are emerging as high-growth regions for biotech lab construction, with China's national bioeconomy strategy allocating CNY 800 Billion over five years to life sciences infrastructure, and the United Kingdom investing GBP 650 Million through its Life Sciences Investment Programme. North America retains the largest share of the biotech lab construction market at 42.3% in 2025, anchored by Boston-Cambridge, San Francisco Bay Area, San Diego, and Research Triangle Park. These clusters continue to absorb the majority of global lab real estate investment due to their proximity to top-tier research institutions, talent pools, and regulatory infrastructure.

, By Construction Type (Ground-Up, Renovation & Adaptive Reuse, Modular & Prefabricated), By End-User (Biopharma, CDMOs, Academic Institutes, Diagnostics, Biotech Startups) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global biotech lab construction market was valued at USD 8.40 Billion in 2025 and is projected to reach USD 18.72 Billion by 2034, registering a CAGR of 9.3% over the forecast period 2026–2034.

- Segment Dominance: By facility type, cGMP manufacturing suites represent the leading sub-segment with 34.2% of the biotech lab construction market in 2025, driven by surge capacity investment from CDMOs and cell and gene therapy producers building commercial-scale operations.

- Segment Dominance: By end-user, pharmaceutical and biopharmaceutical companies account for 48.6% of biotech lab construction spending in 2025, with CDMOs comprising the fastest-growing sub-segment at 12.1% CAGR through 2034 due to outsourcing momentum in biologics manufacturing.

- Driver: Expansion of cell and gene therapy pipelines globally has created demand for specialized cleanroom and biosafety infrastructure; the number of active CGT clinical trials exceeded 2,800 in 2025, each requiring dedicated manufacturing and QC lab environments.

- Restraint: High capital costs and extended regulatory approval timelines for specialized biotech facilities constrain market growth; a typical BSL-3 laboratory costs USD 450–650 per square foot to construct and requires 24–36 months for design, permitting, and commissioning.

- Opportunity: Modular and prefabricated lab construction represents an estimated USD 2.8 Billion addressable opportunity by 2034, offering 20–35% faster project delivery and 15–25% cost reduction compared to traditional construction methods.

- Trend: Digital twin integration in biotech lab design is gaining adoption, with 38% of major life sciences AEC firms deploying building information modeling (BIM) and digital simulation tools in 2025 to validate lab workflows prior to physical construction.

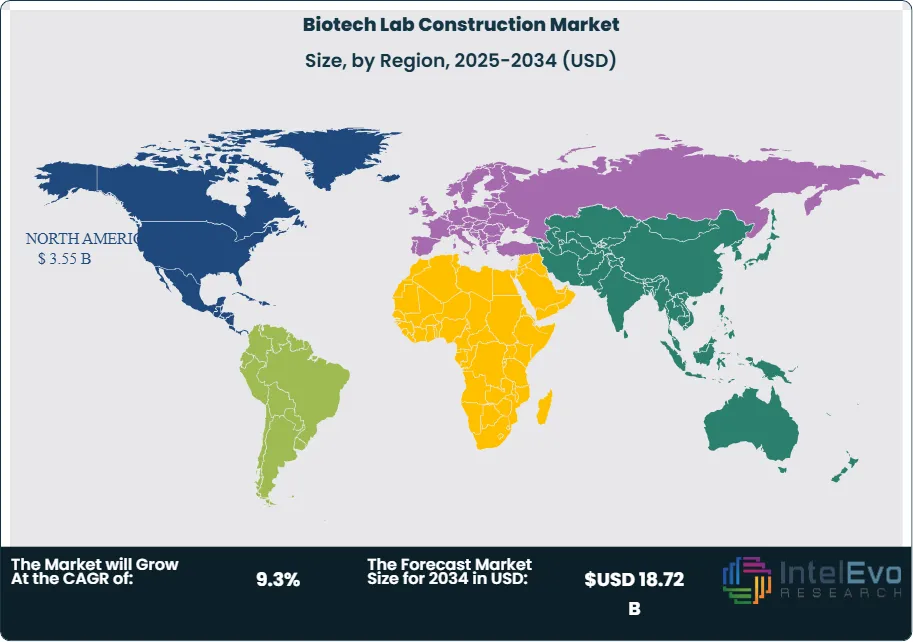

- Regional Analysis: North America leads the biotech lab construction market with 42.3% share and USD 3.55 Billion in revenue in 2025, anchored by high-density life sciences clusters in Massachusetts, California, and North Carolina and sustained NIH research funding.

Competitive Landscape Overview

The biotech lab construction market is moderately consolidated, with the top four players collectively accounting for approximately 38% of global revenue in 2025. Competition is differentiated primarily by technical specialization, regulatory track record, and geographic presence rather than price. Leading firms compete on depth of life sciences engineering expertise, speed of delivery through modular solutions, and relationships with repeat biopharmaceutical clients. Merger and acquisition activity has increased significantly since 2023, as general contractors seek to acquire specialized life sciences construction firms to capture backlog growth. Three new entrants from the broader industrial construction sector entered the biotech lab market in 2024–2025, intensifying competition in the mid-market project tier.

Competitive Landscape Matrix

| Company | HQ | Position | Key Solution | Geo Strength | Recent Strategic Move |

| Jacobs Engineering Group | USA | Leader | Life Sciences Lab Design-Build | North America | Acquired a Boston-based biotech facility consulting firm in Jan 2025 to expand cGMP design capabilities |

| AECOM | USA | Leader | Integrated Lab & CDMO Facility Solutions | North America / Europe | Secured a USD 420M contract for a multi-site biotech campus in San Diego in Mar 2025 |

| DPR Construction | USA | Leader | cGMP Cleanroom & BSL Lab Construction | North America | Completed a 180,000 sq ft gene therapy manufacturing facility in Philadelphia in Feb 2025 |

| Skanska USA Building | USA | Leader | Modular Biotech Lab Systems | North America / Europe | Launched its dedicated Life Sciences Prefab Division in Nov 2024 targeting CDMO clients |

| IPS (Integrated Project Services) | USA | Challenger | GMP Engineering & Commissioning | North America / Asia Pacific | Opened a Singapore regional office in Jan 2025 to capture APAC biotech construction demand |

| Turner Construction | USA | Challenger | Full-Cycle Lab Construction | North America | Partnered with a digital twin software provider in Dec 2024 to integrate BIM workflows |

| HDR Inc. | USA | Challenger | Research & Vivarium Facility Design | North America | Completed a USD 310M research complex for a top-20 U.S. university in Apr 2025 |

| Bam Construct (BAM Group) | Netherlands | Niche Player | European Biotech Campus Build-Out | Europe | Won a GBP 180M contract for a life sciences hub in Cambridge, UK in Jun 2025 |

| Linesight | Ireland | Niche Player | Cost & Project Management for Labs | Europe / Middle East | Expanded into the UAE biotech construction advisory market in Mar 2025 |

| Kajima Corporation | Japan | Niche Player | High-Spec Lab & Cleanroom Construction | Asia Pacific | Awarded a JPY 15B biotech manufacturing campus contract in Osaka in May 2025 |

By Facility Type

The biotech lab construction market by facility type is led by cGMP manufacturing suites, which captured 34.2% of market revenue in 2025, equivalent to approximately USD 2.87 Billion. The surge in approvals for biologics, cell therapies, and mRNA-based products has elevated demand for compliant manufacturing environments capable of meeting FDA 21 CFR Parts 210 and 211 standards. Clients require specialized HVAC systems with HEPA filtration, positive and negative pressure zones, cleanroom classifications between ISO 5 and ISO 8, and segregated processing areas. Vivaria and animal research facilities represent 14.8% of the market, driven by preclinical study requirements across oncology and immunology pipelines. Biosafety level 2 and 3 laboratories account for 22.6% of spending, primarily from academic medical centers, research hospitals, and public health agencies expanding infectious disease and pandemic preparedness capacity. Genomics, proteomics, and high-throughput screening labs account for 16.5%, reflecting demand from precision medicine companies and diagnostic developers. Pilot and process development labs hold the remaining 11.9% share and are expanding rapidly as biotech companies build in-house early-stage manufacturing capability before transferring to CDMOs.

By Construction Type

Within biotech lab construction by construction type, ground-up new construction accounts for the largest share at 44.7% in 2025, valued at USD 3.76 Billion. This segment is driven by greenfield CDMO campuses, new academic research buildings, and purpose-built cell and gene therapy manufacturing sites that require purpose-designed utility infrastructure, structural vibration isolation, and high-capacity electrical systems. Renovation and adaptive reuse of existing buildings represents 31.4% of the biotech lab construction market, as organizations convert commercial office or industrial warehouse spaces into compliant laboratory environments. This approach reduces land acquisition costs and accelerates project timelines in dense urban markets such as Boston, New York, and London. Modular and prefabricated lab construction holds 23.9% of the market in 2025 and is the fastest-growing construction type, expanding at an estimated 13.4% CAGR through 2034. Modular solutions allow parallel off-site manufacturing of lab modules while site preparation occurs simultaneously, compressing delivery timelines by 25–35% and reducing on-site labor requirements in markets facing skilled trades shortages.

By End-User

The biotech lab construction market by end-user is dominated by pharmaceutical and biopharmaceutical companies, which account for 48.6% of total construction spending in 2025. This reflects the sector's sustained capital investment in expanding both R&D and commercial manufacturing infrastructure. CDMOs represent 19.4% of the market in 2025 and are the fastest-growing end-user segment, as outsourced biologics and gene therapy manufacturing demand accelerates. Academic and government research institutions account for 17.8% of spending, supported by federal research grants from NIH, NSF, and BARDA, as well as state-level economic development funds targeting life sciences cluster formation. Diagnostic and medical device companies contribute 8.3% to total biotech lab construction revenue, primarily through expansion of molecular diagnostic and assay development facilities. Emerging biotech startups and seed-stage companies, often housed in incubator and shared-lab environments, represent 5.9% of the market but are influencing design trends toward flexible, multi-tenant lab configurations with shared utility infrastructure.

By Service Type

Biotech lab construction service segmentation divides the market into architecture and engineering design services, general contracting and construction management, specialty MEP (mechanical, electrical, plumbing) services, commissioning and qualification services, and facility validation and regulatory documentation support. Architecture and engineering design captures 26.3% of total market value in 2025, as highly specialized life sciences AEC firms command premium fees for regulatory-aligned lab design. General contracting and construction management holds 38.7% of the market, the largest service segment, reflecting the labor intensity of physical construction. Specialty MEP services account for 18.6%, driven by the complexity of biotech-grade HVAC systems, high-purity water systems, compressed gas distribution, and electrical redundancy infrastructure. Commissioning, qualification, and regulatory documentation services hold 16.4% and are growing rapidly as clients prioritize IQ/OQ/PQ compliance documentation for FDA and EMA inspection readiness immediately upon facility handover.

Regional Analysis

North America

North America leads the global biotech lab construction market with a 42.3% share and USD 3.55 Billion in revenue in 2025. The United States is the dominant country market, accounting for over 90% of regional spending. The Boston-Cambridge corridor, San Francisco Bay Area, San Diego, and Research Triangle Park remain the most active construction markets, collectively absorbing over USD 1.8 Billion in annual lab construction investment. Federal funding from the NIH, BARDA, and the Advanced Research Projects Agency for Health (ARPA-H) is a primary demand driver, with ARPA-H alone committing USD 2.5 Billion in its first three years toward high-priority biomedical research infrastructure. Canada contributes an estimated 8.2% of North American biotech lab construction revenue, supported by Toronto's MaRS Discovery District and Vancouver's growing gene therapy sector. The U.S. CHIPS and Science Act provisions supporting life sciences R&D have added an estimated USD 480 Million in incremental lab construction demand since passage. Regulatory clarity from the FDA on biologics manufacturing standards continues to incentivize domestic facility investment over offshore alternatives.

Europe

Europe accounts for 24.8% of the global biotech lab construction market in 2025, representing USD 2.08 Billion in revenue. The United Kingdom is the leading national market within Europe, with Cambridge, London's Knowledge Quarter, and Edinburgh's biocluster driving significant new lab development. The UK Government's Life Sciences Investment Programme has committed GBP 650 Million to expand research and manufacturing capacity through 2027. Germany is the second-largest European market, with Munich and Berlin attracting substantial private investment in biologic manufacturing and gene therapy infrastructure from companies such as BioNTech and CureVac. France's BioFrance initiative and the Netherlands' Leiden Bio Science Park cluster are contributing to a broadening European biotech infrastructure base. The European Medicines Agency's ATMP (advanced therapy medicinal product) regulatory framework has created demand for specialized cleanroom and manufacturing environments across the continent. Switzerland, while a smaller geographic market, hosts significant biotech construction investment tied to Novartis, Roche, and their CDMO network expansions.

Asia Pacific

Asia Pacific represents 22.4% of the biotech lab construction market in 2025 with USD 1.88 Billion in revenue and is the fastest-growing region, projected to expand at a 12.6% CAGR through 2034. China leads the region, with its 14th Five-Year Plan directing substantial capital toward bioeconomy infrastructure including biosafety laboratories, biomanufacturing facilities, and genomics research centers. Shanghai, Beijing, Suzhou, and Shenzhen are the primary biotech construction clusters, with construction activity concentrated in dedicated life sciences zones supported by local government subsidies. Japan is the second-largest Asia Pacific market, with strong demand for cell therapy and regenerative medicine manufacturing infrastructure aligned with PMDA regulatory guidelines. India is a rapidly emerging market, as domestic API producers and biosimilar manufacturers invest in upgrading GMP-compliant infrastructure to capture global CDMO demand. South Korea's Samsung Biologics and Celltrion expansions are driving significant local construction investment in Incheon and Songdo.

Latin America

Latin America holds a 6.2% share of the global biotech lab construction market in 2025, representing USD 0.52 Billion in revenue. Brazil is the dominant country market, accounting for approximately 58% of regional spending. Investments in the Butantan Institute, FIOCRUZ expansion, and private biopharmaceutical manufacturing facilities in Sao Paulo and Rio de Janeiro are the primary drivers. Mexico is the second-largest Latin American market, with pharmaceutical multinationals constructing regional manufacturing hubs near the U.S. border to benefit from USMCA trade provisions. ANVISA regulatory harmonization with international cGMP standards has improved investment confidence in Brazilian biotech construction. Argentina and Colombia represent smaller but growing markets as domestic biotech investment accelerates. The region benefits from lower construction labor costs compared to North America and Europe, though project execution timelines can be extended by supply chain and regulatory permitting challenges. Infrastructure financing from the Inter-American Development Bank is beginning to support life sciences facility development in the region.

Middle East & Africa

The Middle East and Africa region accounts for 4.3% of the global biotech lab construction market in 2025 with USD 0.36 Billion in revenue. The UAE is the most active construction market in the region, with Dubai and Abu Dhabi investing heavily in life sciences infrastructure as part of broader economic diversification strategies. The UAE's Operation 300bn initiative targets a tripling of the industrial sector's contribution to GDP by 2031, with life sciences identified as a priority vertical. Saudi Arabia's Vision 2030 has earmarked SAR 5 Billion for biotechnology and pharmaceutical manufacturing capacity development, including greenfield biosafety laboratory construction. South Africa is the leading African market for biotech lab construction, with Western Cape and Gauteng hosting the majority of private and public-sector research facility investment. GCC nations are attracting multinational biotech companies to establish regional headquarters and R&D facilities, creating demand for international-standard laboratory environments. Healthcare infrastructure investment by sovereign wealth funds in the region is also indirectly stimulating biotech lab construction through hospital-adjacent research facility development.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Facility Type

- cGMP Manufacturing Suites

- Biosafety Level (BSL) 2 & 3 Laboratories

- Genomics, Proteomics & High-Throughput Screening Labs

- Vivaria & Animal Research Facilities

- Pilot & Process Development Labs

By Construction Type

- Ground-Up New Construction

- Renovation & Adaptive Reuse

- Modular & Prefabricated Lab Construction

By End-User

- Pharmaceutical & Biopharmaceutical Companies

- CDMOs (Contract Development & Manufacturing Organizations)

- Academic & Government Research Institutions

- Diagnostic & Medical Device Companies

- Emerging Biotech Startups & Incubators

By Service Type

- Architecture & Engineering Design Services

- General Contracting & Construction Management

- Specialty MEP Services

- Commissioning, Qualification & Validation Services

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.40 B |

| Forecast Revenue (2034) | USD 18.72 B |

| CAGR (2025-2034) | 9.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Facility Type, (cGMP Manufacturing Suites, Biosafety Level (BSL) 2 & 3 Laboratories, Genomics, Proteomics & High-Throughput Screening Labs, Vivaria & Animal Research Facilities, Pilot & Process Development Labs), By Construction Type, (Ground-Up New Construction, Renovation & Adaptive Reuse, Modular & Prefabricated Lab Construction), By End-User, (Pharmaceutical & Biopharmaceutical Companies, CDMOs (Contract Development & Manufacturing Organizations), Academic & Government Research Institutions, Diagnostic & Medical Device Companies, Emerging Biotech Startups & Incubators), By Service Type, (Architecture & Engineering Design Services, General Contracting & Construction Management, Specialty MEP Services, Commissioning, Qualification & Validation Services) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | JACOBS ENGINEERING GROUP, AECOM, DPR CONSTRUCTION, SKANSKA USA BUILDING, IPS (INTEGRATED PROJECT SERVICES), TURNER CONSTRUCTION COMPANY, HDR INC., BAM CONSTRUCT (BAM GROUP), LINESIGHT, KAJIMA CORPORATION, STANTEC INC., GILBANE BUILDING COMPANY, HENSEL PHELPS, CLARK CONSTRUCTION GROUP, PERKINS AND WILL, HEERY INTERNATIONAL, KITCHELL CORPORATION, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Construction Type (Ground-Up, Renovation & Adaptive Reuse, Modular & Prefabricated), By End-User (Biopharma, CDMOs, Academic Institutes, Diagnostics, Biotech Startups) Industry Trends & Forecast 2026–2034")

, By Construction Type (Ground-Up, Renovation & Adaptive Reuse, Modular & Prefabricated), By End-User (Biopharma, CDMOs, Academic Institutes, Diagnostics, Biotech Startups) Industry Trends & Forecast 2026–2034")

, By Construction Type (Ground-Up, Renovation & Adaptive Reuse, Modular & Prefabricated), By End-User (Biopharma, CDMOs, Academic Institutes, Diagnostics, Biotech Startups) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Biotech Lab Construction Market?

Global Biotech lab construction market valued at USD 7.69B in 2024, reaching USD 18.72B by 2034, growing at a CAGR of 9.3% from 2026–2034.

Who are the major players in the Biotech Lab Construction Market?

JACOBS ENGINEERING GROUP, AECOM, DPR CONSTRUCTION, SKANSKA USA BUILDING, IPS (INTEGRATED PROJECT SERVICES), TURNER CONSTRUCTION COMPANY, HDR INC., BAM CONSTRUCT (BAM GROUP), LINESIGHT, KAJIMA CORPORATION, STANTEC INC., GILBANE BUILDING COMPANY, HENSEL PHELPS, CLARK CONSTRUCTION GROUP, PERKINS AND WILL, HEERY INTERNATIONAL, KITCHELL CORPORATION, Others

Which segments covered the Biotech Lab Construction Market?

By Facility Type, (cGMP Manufacturing Suites, Biosafety Level (BSL) 2 & 3 Laboratories, Genomics, Proteomics & High-Throughput Screening Labs, Vivaria & Animal Research Facilities, Pilot & Process Development Labs), By Construction Type, (Ground-Up New Construction, Renovation & Adaptive Reuse, Modular & Prefabricated Lab Construction), By End-User, (Pharmaceutical & Biopharmaceutical Companies, CDMOs (Contract Development & Manufacturing Organizations), Academic & Government Research Institutions, Diagnostic & Medical Device Companies, Emerging Biotech Startups & Incubators), By Service Type, (Architecture & Engineering Design Services, General Contracting & Construction Management, Specialty MEP Services, Commissioning, Qualification & Validation Services)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Biotech Lab Construction Market

Published Date : 28 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date