- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Bipedal Service Robot Market Size & Forecast | CAGR 31.7%

Global Bipedal Service Robot Market Size, Share, Growth & Industry Analysis By End-Use Application (Manufacturing & Industrial Operations, Logistics & Warehousing, Commercial Services, Healthcare & Elder Care, R&D), By Robot Type (General-Purpose AI Bipedal Platforms, Task-Specific Robots, Research Humanoids, Teleoperated Systems), By Payload Capacity (Light, Medium, Heavy, Ultra-Heavy) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

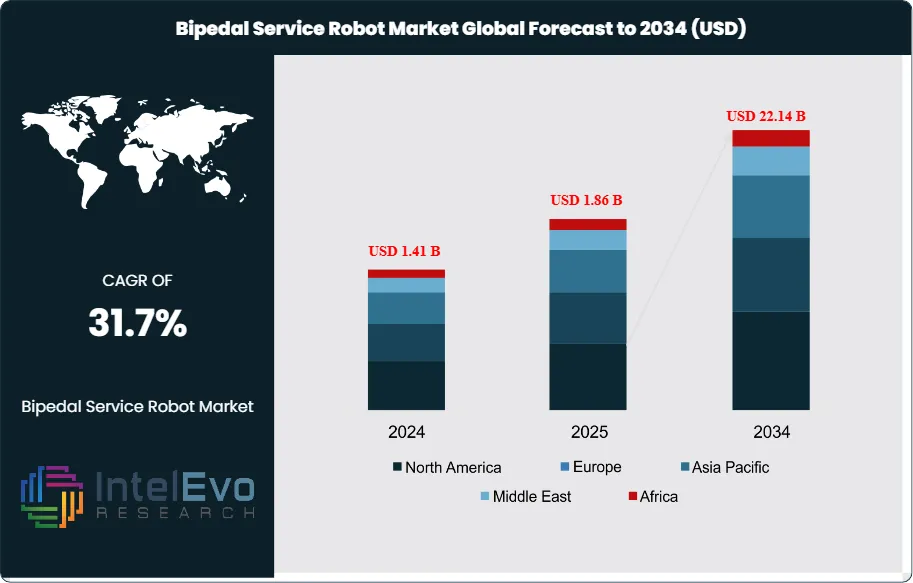

| USD 1.86 Billion | USD 22.14 Billion | 31.7% | North America, 42.5% |

The Bipedal Service Robot Market was valued at approximately USD 1.41 Billion in 2024 and reached USD 1.86 Billion in 2025. The market is projected to grow to USD 22.14 Billion by 2034, expanding at a CAGR of 31.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 20.28 Billion over the analysis period, driven by rapid advances in AI locomotion control, computer vision, and dexterous manipulation, combined with accelerating commercial deployments in automotive manufacturing, logistics, and industrial inspection environments where human-form robots can operate in spaces originally designed for people.

Get More Information about this report -

Request Free Sample ReportBipedal service robots, also referred to as humanoid robots, are autonomous or semi-autonomous robotic systems designed with two legs and an upright posture to navigate and interact with physical environments built around human dimensions and movement patterns. Unlike wheeled or tracked robots, bipedal platforms can ascend stairs, step over obstacles, operate standard hand tools, and access storage systems, vehicle interiors, and workstations without facility modification. The bipedal service robot market spans commercial, industrial, healthcare, and research applications, with commercial and industrial use cases accounting for the majority of 2025 revenues as real-world deployment pilots transition to production-scale contracts.

Several technological and commercial forces are converging to accelerate bipedal service robot market growth. AI foundation models trained on massive robotics datasets are enabling general-purpose manipulation and navigation that allow a single bipedal robot platform to perform dozens of distinct task types without task-specific reprogramming, fundamentally changing the economic calculus of robot deployment. Tesla's internal Optimus deployment program in its Fremont factory, targeting 1,000 units by end 2025, represents the first industrial-scale deployment of bipedal robots in a commercial manufacturing environment and provides public proof of concept that compressed the market's perceived commercial timeline by 3-5 years. Venture capital investment in bipedal service robot companies exceeded USD 3.2 Billion in 2024-2025 combined, with 14 companies reaching or exceeding USD 100 Million in cumulative funding.

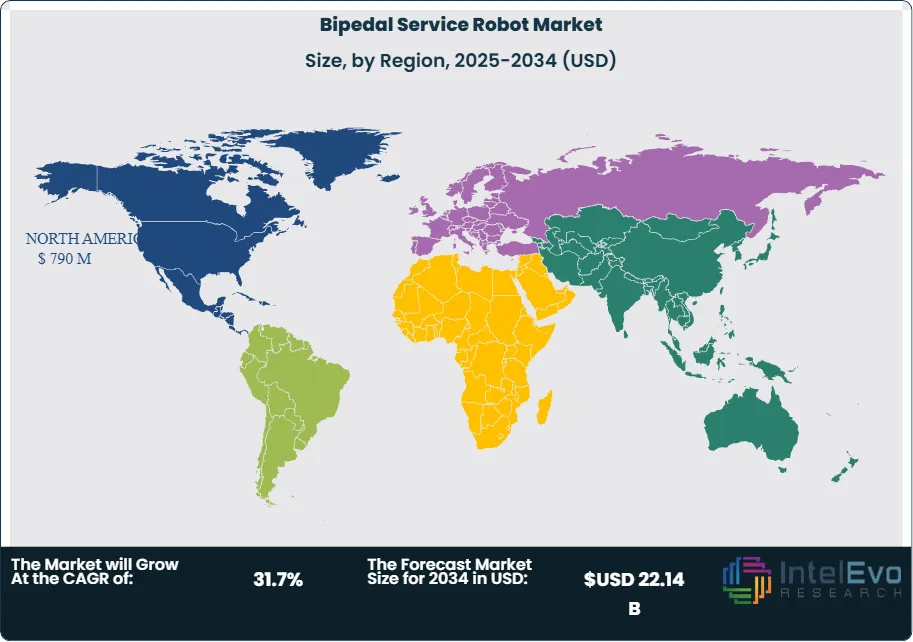

The EU AI Act's classification of autonomous humanoid robots in high-risk application categories under Annex III creates compliance obligations for European deployers but simultaneously establishes a clear regulatory framework that reduces uncertainty for enterprise procurement decisions. The US Executive Order on AI Safety and Standards applies to autonomous robotic systems used in critical infrastructure, requiring developers to provide safety documentation that is shaping product certification approaches. North America led the bipedal service robot market with a 42.5% share in 2025, equivalent to USD 790 Million, concentrated in US-based development and pilot deployment activities. Asia Pacific is the fastest-growing region, advancing at a projected CAGR of 35.2% through 2034, driven by Chinese government robotics policy support and Japan's established precision manufacturing sector.

, By Robot Type (General-Purpose AI Bipedal Platforms, Task-Specific Robots, Research Humanoids, Teleoperated Systems), By Payload Capacity (Light, Medium, Heavy, Ultra-Heavy) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Global Bipedal Service Robot Market was valued at USD 1.86 Billion in 2025 and is forecast to reach USD 22.14 Billion by 2034, registering a CAGR of 31.7% during the 2026-2034 forecast period.

- Segment Dominance: By end-use application, manufacturing and industrial operations held the largest share at 44.8% of the bipedal service robot market in 2025, driven by automotive assembly pilot deployments, parts picking operations, and quality inspection tasks at facilities from multiple global automakers.

- Segment Dominance: By robot type, general-purpose bipedal service robots with AI multi-task capability accounted for 58.6% of the bipedal service robot market in 2025, reflecting commercial preference for platforms that can be redeployed across multiple task types within a single facility without hardware modification.

- Driver: Structural manufacturing labor shortages in North America, Europe, and Asia Pacific, where BLS data indicates US manufacturing job vacancies exceeded 600,000 in 2025 and Japan's manufacturing workforce has contracted by 12% since 2010, are compelling enterprises to accelerate bipedal robot deployments as labor-equivalent production assets.

- Restraint: Bipedal service robot unit costs remain in the USD 50,000-250,000 range for commercial platforms in 2025, with per-unit autonomy levels insufficient for fully unsupervised operation in unstructured environments, constraining rapid commercial adoption beyond controlled industrial pilot programs.

- Opportunity: The global logistics and e-commerce warehouse automation market, where bipedal robots can address unstructured picking, sorting, and material handling tasks that fixed automation cannot perform, represents an addressable bipedal robot market estimated at USD 4.8 Billion by 2034 as platforms achieve the dexterity and reliability thresholds required for high-throughput warehouse operation.

- Trend: AI imitation learning and reinforcement learning from human demonstration, which trains bipedal robots to perform complex manipulation tasks by observing human teleoperation data, grew at approximately 38.4% adoption rate among commercial bipedal robot development programs in 2025, reducing task programming costs from weeks to days.

- Regional Analysis: North America led the bipedal service robot market with a 42.5% share, equivalent to USD 790 Million in 2025, driven by concentrated US-based humanoid robot company formation, enterprise pilot deployment programs at automotive and logistics companies, and the highest density of AI robotics R&D investment globally.

Competitive Landscape Overview

The bipedal service robot market is moderately fragmented, with Boston Dynamics, Figure AI, Agility Robotics, and Tesla collectively accounting for approximately 58% of global revenues in 2025. Competition is intensely technology-driven, centered on AI locomotion stability, manipulation dexterity, battery endurance, task generalization capability, and deployment support infrastructure. Competitive intensity has accelerated sharply since 2023, with over 40 companies globally now developing commercial bipedal robot platforms and venture capital investment exceeding USD 3.2 Billion across the sector in 2024-2025. Chinese companies including Unitree Robotics, UBTECH, and Fourier Intelligence are expanding international distribution rapidly, with Unitree's G1 platform offered at USD 16,000, introducing aggressive price competition against premium Western platforms priced at USD 100,000+.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Boston Dynamics | USA | Leader | Atlas Humanoid Service Robot | North America & Global | Launched Atlas commercial service pilot with automotive manufacturing partners; deployed 10+ units; Q1 2025. |

| Figure AI | USA | Leader | Figure 02 Bipedal Service Robot | North America | Signed commercial deployment agreement with BMW for Figure 02 automotive plant operations; Q2 2025. |

| Agility Robotics | USA | Leader | Digit Bipedal Logistics Robot | North America | Expanded Digit deployment to Amazon fulfillment centers; surpassed 1,000 cumulative commercial hours; 2025. |

| Tesla (Optimus) | USA | Leader | Tesla Optimus Gen 2 Humanoid Robot | North America | Deployed Optimus Gen 2 in Tesla Fremont factory; targeting 1,000 units internal deployment by end 2025. |

| Unitree Robotics | China | Challenger | H1 & G1 Bipedal Service Robots | Asia Pacific & Global | Launched G1 commercial service robot at USD 16,000; expanded to 30+ countries through distributor network; 2025. |

| UBTECH Robotics | China | Challenger | Walker S Humanoid Service Robot | Asia Pacific | Deployed Walker S in automotive manufacturing and retail; signed JD.com logistics partnership; Q3 2025. |

| Sanctuary AI | Canada | Challenger | Phoenix Bipedal Service Robot | North America | Completed carbon capture facility deployment pilot with 5 Phoenix units; received Series C funding; 2025. |

| Fourier Intelligence | China | Niche Player | GR-1 & GR-2 Humanoid Robots | Asia Pacific & Europe | Launched GR-2 with 35kg payload capacity; targeted industrial and rehabilitation applications; Q2 2025. |

| PAL Robotics | Spain | Niche Player | TALOS Industrial Bipedal Robot | Europe | Expanded TALOS deployment to four European research and industrial pilot sites; 2025. |

| 1X Technologies | Norway | Niche Player | NEO Beta Bipedal Service Robot | Europe & North America | Raised USD 100M to accelerate NEO Beta manufacturing and deployment in commercial facilities; Jan 2026. |

By End-Use Application

The bipedal service robot market by end-use application spans manufacturing and industrial operations, logistics and warehousing, commercial services, healthcare and elder care, and research and development. Manufacturing and industrial operations held the dominant application share at 44.8% of the bipedal service robot market in 2025, equivalent to approximately USD 833 Million. Automotive manufacturing has emerged as the primary commercial deployment environment, where bipedal robots perform parts picking, assembly line material transport, quality inspection in confined vehicle interiors, and spot welding fixture positioning. BMW's deployment agreement with Figure AI, Tesla's internal Optimus program, and Agility Robotics' automotive facility pilots collectively represent the most commercially advanced bipedal robot deployment programs globally as of 2025. These automotive deployments are significant because they expose bipedal robots to genuine industrial productivity measurement, generating operational data that will define commercial viability standards for broader manufacturing adoption.

Logistics and warehousing represented 24.6% of the bipedal service robot market in 2025 and is the fastest-growing application segment at an estimated CAGR of 36.8% through 2034. Amazon's deployment of Agility Robotics' Digit in fulfillment centers for unstructured goods movement tasks is the highest-profile logistics bipedal robot program globally. Bipedal robots address the specific challenge in e-commerce logistics where conveyor and fixed automation systems cannot handle the enormous diversity of package shapes, sizes, and weights that characterize modern e-commerce fulfillment. Commercial services including hotel concierge, retail assistance, airport guidance, and building security held 14.8% of the bipedal service robot market in 2025. Healthcare and elder care applications, where bipedal robots assist with patient mobility, medication delivery, and companionship in aged care facilities, accounted for 9.4%. Research and development applications held the remaining 6.4%.

By Robot Type

The bipedal service robot market by robot type covers general-purpose AI-enabled platforms, task-specific bipedal service robots, research-grade humanoid platforms, and teleoperation-primary systems. General-purpose bipedal service robots with AI multi-task capability held the largest type share at 58.6% of the bipedal service robot market in 2025, equivalent to approximately USD 1.09 Billion. Enterprise buyers demonstrated strong commercial preference for platforms that can be reconfigured for multiple task types through software updates rather than hardware changes, as this flexibility justifies higher upfront investment through longer asset useful lives and broader deployment applicability across facility sections. Figure AI's Figure 02, Boston Dynamics' Atlas, and Tesla's Optimus Gen 2 each compete in this general-purpose segment with distinct AI architecture approaches and capability profiles.

Task-specific bipedal service robots, optimized for a defined set of repetitive industrial or logistics tasks with constrained AI general capability in exchange for higher task-specific reliability, held 24.8% of the bipedal service robot market in 2025. Agility Robotics' Digit represents this category within the logistics picking context. Research-grade humanoid platforms used in university and corporate research programs accounted for 10.2% of the market in 2025, with PAL Robotics' TALOS and Fourier Intelligence's GR-2 serving this segment. Teleoperation-primary bipedal systems, where human operators remotely control the robot for hazardous or complex tasks, represented the remaining 6.4% of the bipedal service robot market by robot type in 2025.

By Payload Capacity

The bipedal service robot market by payload capacity segments into light payload (under 5kg), medium payload (5-20kg), heavy payload (20-50kg), and ultra-heavy payload (over 50kg). Medium payload platforms (5-20kg) held the dominant share at 46.4% of the bipedal service robot market in 2025, corresponding to the payload range most useful for parts picking, box manipulation, and assembly assist tasks in manufacturing and logistics environments. This payload class enables bipedal robots to handle the majority of discrete manufacturing component and package handling tasks without the additional structural mass and energy consumption required for higher payload ratings. Light payload platforms under 5kg represented 22.6% of the market in 2025, serving commercial service, reception, and companion robot applications where task loads are primarily informational or involve small object manipulation. Heavy payload platforms in the 20-50kg range accounted for 19.8% of the market, targeting industrial material transport and heavy assembly operations. Ultra-heavy payload platforms above 50kg held the remaining 11.2%.

By Autonomy Level

The bipedal service robot market by autonomy level covers supervised autonomy requiring remote human oversight, semi-autonomous operation with human exception handling, fully autonomous operation within defined zones, and adaptive autonomous operation in unstructured environments. Supervised autonomy requiring remote human oversight held the largest autonomy level share at 42.6% of the bipedal service robot market in 2025. Most commercially deployed bipedal robots in 2025 operate under supervised autonomy frameworks, where human operators monitor robot status through telemetry and remote video feeds and intervene when the robot encounters situations outside its trained operational parameters. This reflects the current state of AI capability for manipulation and locomotion, where task success rates for unstructured manipulation in real commercial environments average 85-95%, below the 99%+ threshold enterprise buyers require for fully unsupervised operation. Semi-autonomous operation with human exception handling held a 34.8% share, fully autonomous within defined zones accounted for 16.4%, and adaptive autonomous operation in unstructured environments represented the remaining 6.2%, reflecting the most advanced AI capability frontier that leading platforms are progressively approaching.

Regional Analysis

North America

North America bipedal service robot market held a 42.5% share in 2025, generating approximately USD 790 Million in revenue. The United States dominates the regional market and is home to the world's highest concentration of bipedal service robot companies, with Boston Dynamics, Figure AI, Agility Robotics, Tesla, Sanctuary AI, and Apptronik all headquartered in the US and conducting primary commercial deployments in American manufacturing and logistics facilities. US-based enterprise buyers in automotive manufacturing (BMW, Ford, GM, Tesla), e-commerce logistics (Amazon), and general manufacturing (GE Aerospace, ABB) are the most commercially active bipedal robot deployment clients globally. The National Science Foundation's National Robotics Initiative program, with annual funding of approximately USD 30 Million, supports foundational AI locomotion and manipulation research that feeds directly into commercial bipedal robot development pipelines. The US Executive Order on AI Safety and Standards establishes documentation requirements for autonomous robotic systems in critical infrastructure, creating a compliance burden that simultaneously raises barriers for poorly resourced competitors and provides a quality signal for enterprise buyers evaluating commercial platforms. Canada contributes through Sanctuary AI's Phoenix program and the Vector Institute's robotics AI research ecosystem in Toronto. Mexico represents an emerging bipedal robot deployment market as its automotive manufacturing sector receives overflow investment from US OEM supply chain reconfiguration.

Europe

Europe held approximately 18.6% of the global bipedal service robot market in 2025, generating approximately USD 346 Million. Germany is the largest European national market, driven by its dominant automotive and industrial machinery manufacturing sectors where BMW's Figure AI partnership represents the highest-profile European bipedal robot deployment to date. German engineering culture's familiarity with advanced robotics integration creates favorable enterprise adoption conditions for bipedal platforms that can demonstrate measurable productivity contributions. The EU AI Act's classification of autonomous robotic systems in consequential physical environments as high-risk AI under Annex III requires conformity assessment, CE marking, and registration in the EU AI database, creating compliance requirements that European deployers must address through technical documentation and safety testing. While this adds deployment overhead, it provides a regulatory framework that large enterprises find preferable to the ambiguity of unregulated deployment. The UK maintains an active bipedal robotics research environment through the Engineering and Physical Sciences Research Council and 1X Technologies' NEO Beta deployments in European facilities. Spain's PAL Robotics serves the European research and industrial pilot market with its TALOS platform. France and Sweden represent secondary European deployment markets where automotive and aerospace manufacturing applications drive bipedal robot adoption interest.

Asia Pacific

Asia Pacific held approximately 28.4% of the global bipedal service robot market in 2025, generating approximately USD 528 Million, and is the fastest-growing regional market at a projected CAGR of 35.2% through 2034. China is the dominant and fastest-developing national market, where the Ministry of Industry and Information Technology's 2023 Humanoid Robot Innovation Development Guidance document committed government support for domestic humanoid robot development as a strategic emerging industry. Chinese government-backed investment in bipedal robot companies including Unitree Robotics, UBTECH, Fourier Intelligence, and Kepler exceeded USD 800 Million in disclosed funding through 2025. Unitree's G1 platform, priced at USD 16,000 for commercial units, represents the most aggressively priced commercial bipedal platform globally and is expanding distribution across 30+ countries, competing directly with US platforms priced at 5-15 times higher. Japan represents the second-largest Asia Pacific market, with Honda's legacy ASIMO research program having established foundational bipedal locomotion knowledge that informs multiple domestic bipedal robot development programs. Japanese automotive and electronics manufacturers are evaluating bipedal service robots for factory floor applications with methodical testing protocols consistent with Japanese engineering adoption norms. South Korea contributes through Samsung and Hyundai's robotics subsidiaries, the latter being the parent company of Boston Dynamics, providing a strategic technology bridge between US-developed platforms and Korean manufacturing applications.

Latin America

Latin America held approximately 6.2% of the global bipedal service robot market in 2025, generating approximately USD 115 Million. Brazil is the dominant regional market, driven by its large and diversifying manufacturing sector that is integrating advanced automation to maintain export competitiveness. Brazil's SENAI National Service for Industrial Learning has incorporated robotics training into advanced manufacturing programs, and several Brazilian automotive plants affiliated with European and US parent companies are participating in bipedal robot pilot evaluation programs that leverage their parent organizations' experience. Mexico is the second-largest Latin American bipedal robot market, where proximity to US automotive manufacturing clusters and participation in North American supply chains drives early enterprise adoption of automation technologies being deployed by US and European corporate partners. The Mexico-based automotive manufacturing cluster spanning Guanajuato, Nuevo Leon, and Mexico City is the primary bipedal robot deployment test ground within the region. Argentina, Chile, and Colombia represent smaller individual national markets where bipedal robot interest is concentrated in research institutions, technology demonstration events, and early commercial evaluation programs rather than production deployments. The region's overall market remains in an early commercial stage, constrained by infrastructure readiness, total cost of ownership economics, and limited local technical support infrastructure for enterprise-grade bipedal robot maintenance.

Middle East & Africa

The Middle East and Africa region held approximately 4.3% of the global bipedal service robot market in 2025, generating approximately USD 80 Million. The UAE is the most active regional market, driven by Dubai and Abu Dhabi's aggressive smart city and technology adoption programs. The Dubai Future Foundation and Abu Dhabi's Department of Economic Development have both engaged with bipedal service robot demonstration programs, with bipedal robots deployed in hospitality, retail, and government service contexts at flagship locations including Expo City Dubai and several premium hotel properties. Saudi Arabia's Vision 2030 technology diversification agenda includes robotics as a strategic sector, and NEOM's smart city development program has included bipedal service robot evaluation as part of its automated service infrastructure planning. The Saudi government's Public Investment Fund has indirectly supported robotics through its technology sector portfolio investments. South Africa leads the African market through its more developed technology adoption infrastructure and the presence of global automotive manufacturers' production facilities that are beginning to evaluate bipedal robot concepts being piloted at their European and US facilities. Israel contributes disproportionately to the regional bipedal robot technology base through its advanced computer vision and AI research community, several of whose spinout companies are developing manipulation and perception software that feeds into global bipedal robot development programs.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By End-Use Application

- Manufacturing & Industrial Operations

- Logistics & Warehousing

- Commercial Services

- Healthcare & Elder Care

- Research & Development

By Robot Type

- General-Purpose AI-Enabled Bipedal Platforms

- Task-Specific Bipedal Service Robots

- Research-Grade Humanoid Platforms

- Teleoperation-Primary Bipedal Systems

By Payload Capacity

- Light Payload (Under 5kg)

- Medium Payload (5-20kg)

- Heavy Payload (20-50kg)

- Ultra-Heavy Payload (Over 50kg)

By Autonomy Level

- Supervised Autonomy (Remote Human Oversight)

- Semi-Autonomous (Human Exception Handling)

- Fully Autonomous (Within Defined Zones)

- Adaptive Autonomous (Unstructured Environments)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.86 B |

| Forecast Revenue (2034) | USD 22.14 B |

| CAGR (2025-2034) | 31.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By End-Use Application, (Manufacturing & Industrial Operations, Logistics & Warehousing, Commercial Services, Healthcare & Elder Care, Research & Development), By Robot Type, (General-Purpose AI-Enabled Bipedal Platforms, Task-Specific Bipedal Service Robots, Research-Grade Humanoid Platforms, Teleoperation-Primary Bipedal Systems), By Payload Capacity, (Light Payload (Under 5kg), Medium Payload (5-20kg), Heavy Payload (20-50kg), Ultra-Heavy Payload (Over 50kg)), By Autonomy Level, (Supervised Autonomy (Remote Human Oversight), Semi-Autonomous (Human Exception Handling), Fully Autonomous (Within Defined Zones), Adaptive Autonomous (Unstructured Environments)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | BOSTON DYNAMICS (HYUNDAI), FIGURE AI, AGILITY ROBOTICS (AMAZON), TESLA (OPTIMUS), UNITREE ROBOTICS, UBTECH ROBOTICS, SANCTUARY AI, FOURIER INTELLIGENCE, PAL ROBOTICS, 1X TECHNOLOGIES, APPTRONIK, CLONE ROBOTICS, AGILITE LABS, KEPLER (SHENZHEN KEPLER ROBOT CO.), OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Robot Type (General-Purpose AI Bipedal Platforms, Task-Specific Robots, Research Humanoids, Teleoperated Systems), By Payload Capacity (Light, Medium, Heavy, Ultra-Heavy) Industry Trends & Forecast 2026–2034")

, By Robot Type (General-Purpose AI Bipedal Platforms, Task-Specific Robots, Research Humanoids, Teleoperated Systems), By Payload Capacity (Light, Medium, Heavy, Ultra-Heavy) Industry Trends & Forecast 2026–2034")

, By Robot Type (General-Purpose AI Bipedal Platforms, Task-Specific Robots, Research Humanoids, Teleoperated Systems), By Payload Capacity (Light, Medium, Heavy, Ultra-Heavy) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Bipedal Service Robot Market?

Global Bipedal service robot market valued at USD 1.41B in 2024, reaching USD 22.14B by 2034, growing at a CAGR of 31.7% from 2026–2034.

Who are the major players in the Bipedal Service Robot Market?

BOSTON DYNAMICS (HYUNDAI), FIGURE AI, AGILITY ROBOTICS (AMAZON), TESLA (OPTIMUS), UNITREE ROBOTICS, UBTECH ROBOTICS, SANCTUARY AI, FOURIER INTELLIGENCE, PAL ROBOTICS, 1X TECHNOLOGIES, APPTRONIK, CLONE ROBOTICS, AGILITE LABS, KEPLER (SHENZHEN KEPLER ROBOT CO.), OTHERS

Which segments covered the Bipedal Service Robot Market?

By End-Use Application, (Manufacturing & Industrial Operations, Logistics & Warehousing, Commercial Services, Healthcare & Elder Care, Research & Development), By Robot Type, (General-Purpose AI-Enabled Bipedal Platforms, Task-Specific Bipedal Service Robots, Research-Grade Humanoid Platforms, Teleoperation-Primary Bipedal Systems), By Payload Capacity, (Light Payload (Under 5kg), Medium Payload (5-20kg), Heavy Payload (20-50kg), Ultra-Heavy Payload (Over 50kg)), By Autonomy Level, (Supervised Autonomy (Remote Human Oversight), Semi-Autonomous (Human Exception Handling), Fully Autonomous (Within Defined Zones), Adaptive Autonomous (Unstructured Environments))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Bipedal Service Robot Market

Published Date : 21 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date