- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Bispecific Antibody Market Size, Share & Growth Analysis| CAGR 15.4%

Global Bispecific Antibody Market Size, Share & Industry Analysis By Therapeutic Area (Oncology, Ophthalmology, Hematology & Bleeding Disorders, Immunology Inflammation and Emerging Indications), By Mechanism Class (CD3-Engaging T-Cell Redirector Bispecific Antibodies, Dual-Pathway Receptor Blocking Bispecific Antibodies, Coagulation-Factor Mimetic Bispecific Antibodies, Dual-Checkpoint and Immune-Modulatory Bispecifics), By Route of Administration (Intravenous, Subcutaneous, Intravitreal), By End User (Hospital Oncology Centers, Specialty Infusion Clinics, Ophthalmology Clinics, Academic Hospitals) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

| USD 15.6 Billion, 2025 | USD 56.6 Billion, 2034 | 15.4%, 2026–2034 | North America, 39.00%, 2025 |

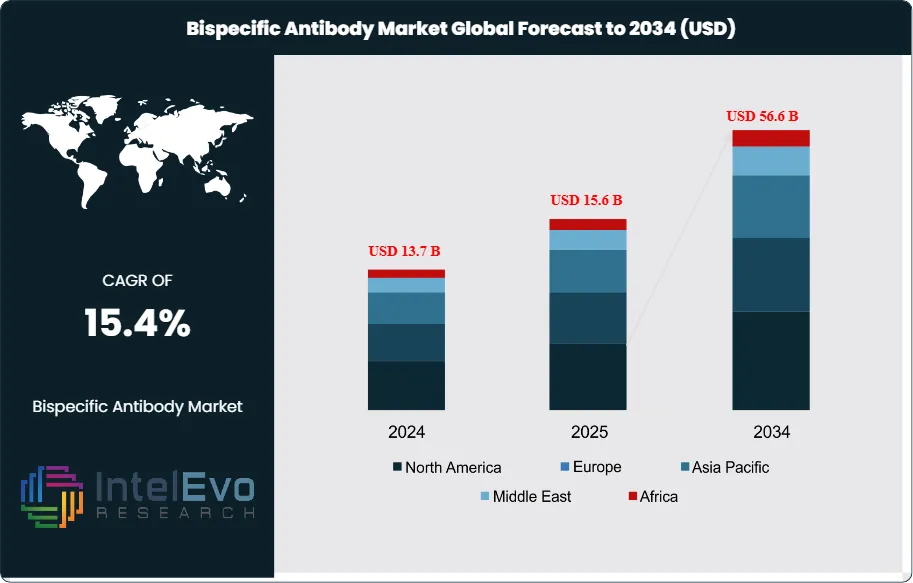

The Bispecific Antibody Market was valued at approximately USD 13.7 Billion in 2024 and increased to USD 15.6 Billion in 2025. The market is projected to reach nearly USD 56.6 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 15.4% during the forecast period from 2026 to 2034. Market expansion is primarily driven by the rapid clinical and commercial adoption of bispecific antibody therapies across oncology, hematological malignancies, and emerging autoimmune disease applications. In addition, increasing regulatory approvals, strong late-stage pipeline activity, and growing investment in next-generation immunotherapies are accelerating the development and commercialization of bispecific antibody platforms worldwide.

Get More Information about this report -

Request Free Sample ReportThe Bispecific Antibody Market entered 2025 with stronger commercial depth than at any prior point in the class history. The market is no longer defined by a single hematology product. It now spans oncology, ophthalmology, hemophilia, and emerging immunology programs. Amgen reported USD 1.56 Billion of 2025 BLINCYTO sales and USD 627 Million of IMDELLTRA sales. Johnson & Johnson reported first-nine-month 2025 sales of USD 518 Million for RYBREVANT plus LAZCLUZE, USD 494 Million for TECVAYLI, and USD 314 Million for TALVEY. Genmab reported USD 468 Million of 2025 global EPKINLY and TEPKINLY net sales. These results confirm that the class has moved into scaled commercialization.

The market in 2025 was led by oncology, but the revenue base remained more balanced than many investors assume. Roche's Hemlibra and Vabysmo remained major growth drivers, while Columvi and Lunsumio continued to expand in blood cancers. The FDA granted traditional approval to tarlatamab-dlle in November 2025, approved EPKINLY with lenalidomide and rituximab for follicular lymphoma in November 2025, and granted accelerated approval to Lynozyfic in July 2025. The class also broadened in solid tumors after BIZENGRI became the first HER2 x HER3 bispecific approval in December 2024.

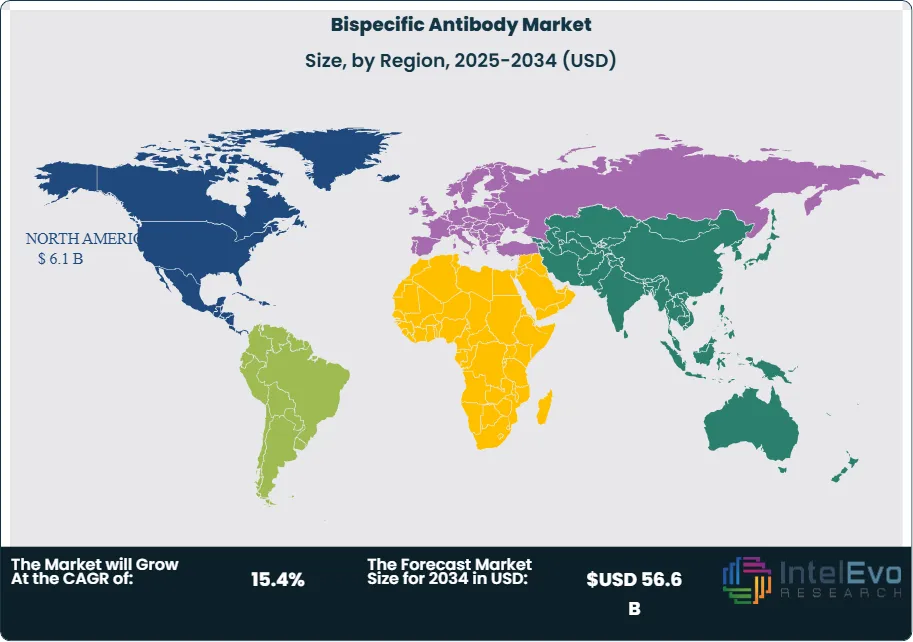

Demand is being driven by off-the-shelf immune redirection in hematologic malignancies, premium pricing in ophthalmology and rare disease, and a much larger late-stage pipeline in solid tumors. Supply remains constrained by manufacturing complexity, cytokine release syndrome management, REMS requirements for selected T-cell engagers, and the need for specialist administration centers. Companies are now combining dual-target biology with subcutaneous delivery, longer dosing intervals, outpatient administration, and AI-guided target selection. Regionally, North America held 39.0% of the market in 2025, equal to USD 6.1 Billion, followed by Europe at 27.0% and Asia Pacific at 21.0%. North America led due to earlier approvals, broader reimbursement, and faster uptake in oncology and retina care. Asia Pacific emerged as the leading pipeline and partnering hotspot.

, By Mechanism Class (CD3-Engaging T-Cell Redirector Bispecific Antibodies, Dual-Pathway Receptor Blocking Bispecific Antibodies, Coagulation-Factor Mimetic Bispecific Antibodies, Dual-Checkpoint and Immune-Modulatory Bispecifics), By Route of Administration (Intravenous, Subcutaneous, Intravitreal), By End User (Hospital Oncology Centers, Specialty Infusion Clinics, Ophthalmology Clinics, Academic Hospitals) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Bispecific Antibody Market stood at USD 15.6 Billion in 2025 and is projected to reach USD 56.6 Billion by 2034 at a 15.4% CAGR across 2026-2034.

- Segment Dominance: By mechanism class, CD3-engaging T-cell redirector bispecific antibodies led with 44.0% share in 2025, or USD 6.9 Billion.

- Segment Dominance: By therapeutic area, oncology held the largest share at 67.0% in 2025, equal to USD 10.5 Billion.

- Driver: Commercial expansion of approved products is the main growth driver. Amgen reported USD 1.56 Billion of 2025 BLINCYTO sales and USD 627 Million of IMDELLTRA sales.

- Restraint: Administration complexity and safety management remain the key restraint. LYNOZYFIC requires a REMS program and IMDELLTRA carries boxed warnings for cytokine release syndrome and neurologic toxicity.

- Opportunity: The largest opportunity sits in solid tumors and autoimmune disease. The BNT327 partnership covers more than 10 solid-tumor indications with more than 1,000 patients treated to date.

- Trend: Longer-interval and easier-delivery formats are the clearest trend. LYNOZYFIC can shift to every-two-week dosing and then every-four-week dosing in later therapy.

- Regional Analysis: North America led the market with 39.0% share and USD 6.1 Billion revenue in 2025.

Bispecific Antibody Market Competitive Landscape

The Bispecific Antibody Market is moderately consolidated. The top four companies controlled an estimated 49.0% of 2025 market revenue. Competition is technology-driven and platform-based, with commercial strength tied to approved-product breadth, target-selection capability, and manufacturing scale. Competitive intensity accelerated in 2025 and early 2026 as major companies expanded outside hematology into solid tumors and immunology.

Competitive Landscape Matrix

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| ROCHE | Switzerland | Leader | Vabysmo / Hemlibra / Columvi | North America, Europe | Three Phase III NXT007 studies are set to begin in 2026. |

| JOHNSON & JOHNSON | US | Leader | RYBREVANT / TECVAYLI / TALVEY | North America, Europe | RYBREVANT FASPRO won FDA approval in February 2026. |

| AMGEN | US | Leader | BLINCYTO / IMDELLTRA BiTE | North America, global oncology | IMDELLTRA received traditional FDA approval in November 2025. |

| GENMAB | Denmark | Leader | DuoBody platform / EPKINLY | North America, Europe | EPKINLY expanded in follicular lymphoma in November 2025. |

| ABBVIE | US | Challenger | RC148 pipeline | North America | Licensed RC148 from RemeGen in January 2026. |

| REGENERON | US | Challenger | Lynozyfic | North America, Europe | Lynozyfic gained FDA accelerated approval in July 2025. |

| BIONTECH | Germany | Challenger | BNT327 | Europe, global solid tumors | Partnered with Bristol Myers Squibb in June 2025. |

| BRISTOL MYERS SQUIBB | US | Challenger | BNT327 co-development | North America | Committed USD 1.5 Billion upfront in June 2025. |

| MERUS | Netherlands | Niche Player | BIZENGRI | North America, Europe | Secured first HER2 x HER3 bispecific approval in December 2024. |

| ASTRAZENECA | UK | Niche Player | Rilvegostomig / volrustomig | Europe, Asia Pacific | Continued broad bispecific pipeline expansion through 2026. |

By Therapeutic Area

Oncology dominated the market with 67.0% share in 2025, or USD 10.5 Billion. BLINCYTO, TECVAYLI, TALVEY, IMDELLTRA, Columvi, Lunsumio, EPKINLY, Elrexfio, Rybrevant, Lynozyfic, and BIZENGRI kept oncology far ahead of other uses. Ophthalmology held 19.0%, equal to USD 3.0 Billion, with Vabysmo anchoring the segment. Hematology and bleeding disorders accounted for 10.0%, or USD 1.6 Billion, supported largely by Hemlibra. Immunology, inflammation, and other emerging indications represented 4.0%, or USD 0.6 Billion, but remain the most strategically important whitespace.

By Mechanism Class

CD3-engaging T-cell redirector bispecific antibodies held the largest share at 44.0% in 2025, equivalent to USD 6.9 Billion. Dual-pathway signaling or receptor-blocking bispecific antibodies represented 32.0%, or USD 5.0 Billion. Coagulation-factor mimetic bispecific antibodies accounted for 13.0%, or USD 2.0 Billion. Dual-checkpoint, immune-modulatory, and other non-CD3 bispecifics represented 11.0%, or USD 1.7 Billion.

By Route of Administration

Intravenous and infusion-based bispecific antibodies led with 49.0% share in 2025, or USD 7.6 Billion. Subcutaneous bispecific antibodies held 33.0%, equal to USD 5.1 Billion, and this is the most commercially important format shift in the market. Intravitreal bispecific antibodies represented 18.0%, or USD 2.8 Billion, almost entirely because of Vabysmo.

By End User

Hospital oncology centers accounted for 47.0% of the market in 2025, or USD 7.3 Billion. Specialty infusion clinics held 24.0%, equal to USD 3.7 Billion. Ophthalmology clinics and retina centers represented 18.0%, or USD 2.8 Billion. Academic and research hospitals held 11.0%, or USD 1.7 Billion.

Regional Analysis

North America Bispecific Antibody Market

North America held 39.0% of the market in 2025, equal to USD 6.1 Billion. The United States led the region, followed by Canada and Mexico. The U.S. remained the global center of commercial uptake due to deep oncology infrastructure, broad FDA approval activity, higher biologics reimbursement, and faster launch scaling.

Europe Bispecific Antibody Market

Europe accounted for 27.0% of the market in 2025, or USD 4.2 Billion. Germany, France, the UK, and Italy formed the region's most relevant country group. Europe remains a premium biologics market with strong academic hematology and retina networks, but uptake is more reimbursement-sensitive than in the United States.

Asia Pacific Bispecific Antibody Market

Asia Pacific held 21.0% of the market in 2025, equal to USD 3.3 Billion. China, Japan, India, and South Korea were the most strategically relevant countries. The region is the fastest-rising innovation and partnership hub in the market and is gaining importance in both development and manufacturing.

Latin America Bispecific Antibody Market

Latin America represented 8.0% of the market in 2025, or USD 1.2 Billion. Brazil dominated the region, followed by Mexico and Argentina. The region remains underpenetrated relative to its disease burden and depends heavily on access expansion and outpatient-friendly formats.

Middle East & Africa Bispecific Antibody Market

Middle East & Africa held 5.0% of the market in 2025, equal to USD 0.8 Billion. The UAE, Saudi Arabia, and South Africa were the most relevant countries. High-cost biologics, site-of-care requirements, and the need for trained adverse-event management constrain uptake, but specialist demand remains positive.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Therapeutic Area

- Oncology

- Ophthalmology

- Hematology and Bleeding Disorders

- Immunology, Inflammation, and Other Emerging Indications

By Mechanism Class

- CD3-Engaging T-Cell Redirector Bispecific Antibodies

- Dual-Pathway Signaling or Receptor-Blocking Bispecific Antibodies

- Coagulation-Factor Mimetic Bispecific Antibodies

- Dual-Checkpoint, Immune-Modulatory, and Other Non-CD3 Bispecifics

By Route of Administration

- Intravenous and Infusion-Based Bispecific Antibodies

- Subcutaneous Bispecific Antibodies

- Intravitreal Bispecific Antibodies

By End User

- Hospital Oncology Centers

- Specialty Infusion Clinics

- Ophthalmology Clinics and Retina Centers

- Academic and Research Hospitals

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 15.6 B |

| Forecast Revenue (2034) | USD 56.6 B |

| CAGR (2025-2034) | 15.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Therapeutic Area (Oncology, Ophthalmology, Hematology and Bleeding Disorders, Immunology, Inflammation, and Other Emerging Indications), By Mechanism Class (CD3-Engaging T-Cell Redirector Bispecific Antibodies, Dual-Pathway Signaling or Receptor-Blocking Bispecific Antibodies, Coagulation-Factor Mimetic Bispecific Antibodies, Dual-Checkpoint, Immune-Modulatory, and Other Non-CD3 Bispecifics), By Route of Administration (Intravenous and Infusion-Based Bispecific Antibodies, Subcutaneous Bispecific Antibodies, Intravitreal Bispecific Antibodies), By End User (Hospital Oncology Centers, Specialty Infusion Clinics, Ophthalmology Clinics and Retina Centers, Academic and Research Hospitals) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ROCHE, JOHNSON & JOHNSON, AMGEN, GENMAB, ABBVIE, REGENERON PHARMACEUTICALS, BIONTECH, BRISTOL MYERS SQUIBB, MERUS, ASTRAZENECA, UCB, PFIZER, MERCK KGAA, NOVARTIS, COMPUGEN, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Mechanism Class (CD3-Engaging T-Cell Redirector Bispecific Antibodies, Dual-Pathway Receptor Blocking Bispecific Antibodies, Coagulation-Factor Mimetic Bispecific Antibodies, Dual-Checkpoint and Immune-Modulatory Bispecifics), By Route of Administration (Intravenous, Subcutaneous, Intravitreal), By End User (Hospital Oncology Centers, Specialty Infusion Clinics, Ophthalmology Clinics, Academic Hospitals) Industry Trends & Forecast 2026–2034")

, By Mechanism Class (CD3-Engaging T-Cell Redirector Bispecific Antibodies, Dual-Pathway Receptor Blocking Bispecific Antibodies, Coagulation-Factor Mimetic Bispecific Antibodies, Dual-Checkpoint and Immune-Modulatory Bispecifics), By Route of Administration (Intravenous, Subcutaneous, Intravitreal), By End User (Hospital Oncology Centers, Specialty Infusion Clinics, Ophthalmology Clinics, Academic Hospitals) Industry Trends & Forecast 2026–2034")

, By Mechanism Class (CD3-Engaging T-Cell Redirector Bispecific Antibodies, Dual-Pathway Receptor Blocking Bispecific Antibodies, Coagulation-Factor Mimetic Bispecific Antibodies, Dual-Checkpoint and Immune-Modulatory Bispecifics), By Route of Administration (Intravenous, Subcutaneous, Intravitreal), By End User (Hospital Oncology Centers, Specialty Infusion Clinics, Ophthalmology Clinics, Academic Hospitals) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Bispecific Antibody Market?

The Global Bispecific Antibody Market was valued at USD 13.7 Billion in 2024 and USD 15.6 Billion in 2025, projected to reach USD 56.6 Billion by 2034 at a CAGR of 15.4% from 2026–2034. Market growth is driven by rising adoption of bispecific immunotherapies, increasing oncology approvals, strong clinical pipelines, and expanding applications in autoimmune and hematologic diseases.

Who are the major players in the Bispecific Antibody Market?

ROCHE, JOHNSON & JOHNSON, AMGEN, GENMAB, ABBVIE, REGENERON PHARMACEUTICALS, BIONTECH, BRISTOL MYERS SQUIBB, MERUS, ASTRAZENECA, UCB, PFIZER, MERCK KGAA, NOVARTIS, COMPUGEN, Others

Which segments covered the Bispecific Antibody Market?

By Therapeutic Area (Oncology, Ophthalmology, Hematology and Bleeding Disorders, Immunology, Inflammation, and Other Emerging Indications), By Mechanism Class (CD3-Engaging T-Cell Redirector Bispecific Antibodies, Dual-Pathway Signaling or Receptor-Blocking Bispecific Antibodies, Coagulation-Factor Mimetic Bispecific Antibodies, Dual-Checkpoint, Immune-Modulatory, and Other Non-CD3 Bispecifics), By Route of Administration (Intravenous and Infusion-Based Bispecific Antibodies, Subcutaneous Bispecific Antibodies, Intravitreal Bispecific Antibodies), By End User (Hospital Oncology Centers, Specialty Infusion Clinics, Ophthalmology Clinics and Retina Centers, Academic and Research Hospitals)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date