- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Blockchain Technology in BFSI Market Size, Share & Forecast | 46.8% CAGR

Global Blockchain Technology in BFSI Market Size, Share & Analysis By Type (Public, Private, Consortium), By Deployment Mode (Cloud, On-Premise), By Enterprise Size (SMEs, Large Enterprises), Digital Finance Transformation, Investment Trends & Forecast 2025–2034

Report Overview

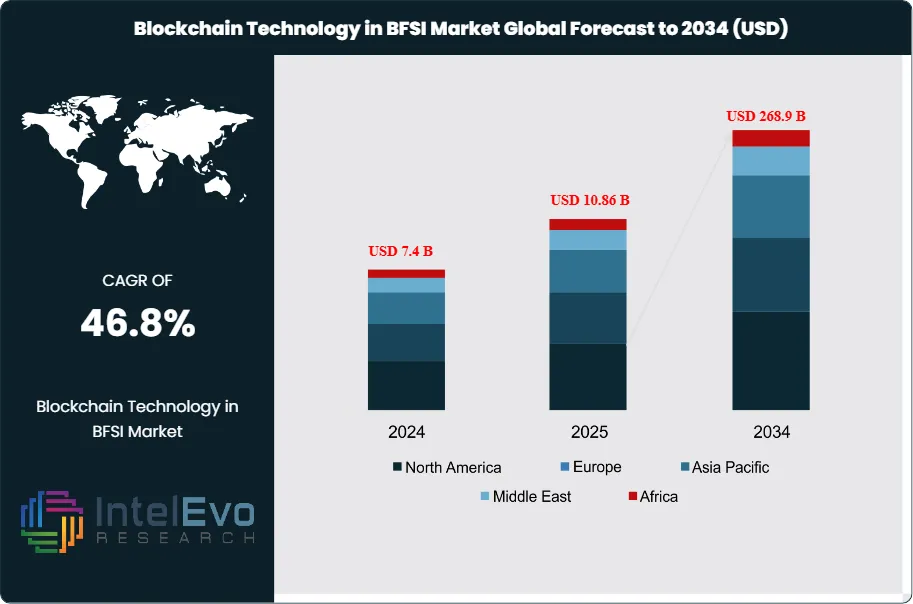

The Blockchain Technology in BFSI Market is projected to grow from USD 7.4 Billion in 2024 to approximately USD 268.9 Billion by 2034, expanding at a CAGR of around 46.8% during 2025–2034. Rising demand for secure, transparent, and real-time financial transactions is accelerating blockchain adoption across banking, insurance, and fintech sectors. AI-integrated smart contracts, decentralized identity systems, and cross-border payment automation are reshaping the next generation of financial infrastructure. As financial institutions rapidly digitize operations, blockchain is emerging as a foundational technology powering trust, resilience, and future-ready BFSI ecosystems. This exponential growth trajectory reflects the transformative role of blockchain in reshaping banking, financial services, and insurance operations, underpinned by its ability to enhance security, transparency, and operational efficiency. What began as the foundational technology for cryptocurrencies has rapidly evolved into a core enabler of applications such as smart contracts, fraud prevention, digital identity management, and cross-border payments.

Get More Information about this report -

Request Free Sample ReportHistorical trends indicate that blockchain adoption in BFSI gained traction as institutions sought to reduce manual errors, strengthen compliance frameworks, and streamline costly, paper-intensive processes. In recent years, the shift has accelerated as banks and insurers recognized blockchain’s potential to reduce infrastructure costs by up to 30%, translating into projected annual savings exceeding USD 27 billion by 2030. Investment banks alone could save nearly USD 12 billion annually through blockchain-enabled efficiencies, according to industry estimates. Furthermore, real-time data visibility and immutable transaction records have positioned blockchain as a cornerstone of future-ready financial ecosystems.

The market’s expansion is fueled by multiple demand- and supply-side dynamics. On the demand side, rising volumes of digital transactions, growing concerns around cyber threats, and the push for faster settlements are compelling institutions to adopt distributed ledger technologies. On the supply side, regulatory environments in key regions are becoming more favorable, with governments and central banks piloting digital currencies and frameworks to facilitate blockchain adoption. However, challenges remain, including interoperability issues, evolving compliance requirements, and the high initial cost of system integration.

Technological innovation is a key accelerator, with blockchain increasingly integrated with artificial intelligence, cloud platforms, and automation to enable scalable solutions. Use cases now extend beyond payments to trade finance, KYC/AML compliance, and insurance claim management. Notably, blockchain has been shown to cut error rates by 50% and reduce average transaction costs by as much as 99%, underscoring its disruptive potential.

Regionally, North America and Europe remain frontrunners, with more than 90% of banks in these regions actively exploring blockchain initiatives. Meanwhile, Asia-Pacific is emerging as a strategic hotspot, driven by rapid fintech adoption, supportive government policies, and rising cross-border trade activity. Global spending on blockchain solutions is projected to surpass USD 15.9 billion in 2024, with sustained growth anticipated as institutional adoption deepens, making blockchain a pivotal investment area in BFSI.

, By Deployment Mode (Cloud, On-Premise), By Enterprise Size (SMEs, Large Enterprises), Digital Finance Transformation, Investment Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global blockchain technology in BFSI market was valued at USD 7.4 Billion in 2024 and is projected to reach USD 268.9 Billion by 2034, expanding at a robust CAGR of 46.8% during 2025–2034. Growth is underpinned by the rising demand for secure, transparent, and cost-efficient financial processes.

- Blockchain Type: Private Blockchains led the BFSI market in 2024, accounting for over 54.2% of total share, as financial institutions prioritize controlled, permissioned networks to meet compliance and data security requirements.

- Deployment Mode: The cloud-based segment captured 56.6% of the market in 2024, reflecting growing reliance on scalable, cost-efficient blockchain platforms integrated with digital banking and fintech ecosystems.

- End User: Small and Medium-sized Enterprises (SMEs) represented 57.8% of adoption in 2024, driven by the need to streamline cross-border payments, trade finance, and identity verification with minimal infrastructure investment.

- Driver: Cost savings remain a key growth catalyst, with blockchain projected to reduce banking infrastructure expenses by 30%, equating to potential annual savings exceeding USD 27 billion by 2030.

- Restraint: High implementation costs and interoperability challenges pose significant barriers, particularly for smaller institutions, slowing large-scale blockchain integration across fragmented financial systems.

- Opportunity: Asia-Pacific presents a strong growth opportunity, with rapid fintech adoption and supportive government initiatives projected to drive the region’s BFSI blockchain market at one of the fastest CAGRs globally.

- Trend: Adoption momentum is accelerating, with 40% of the world’s top 50 banks planning blockchain integration and nearly 50% of financial firms exploring the technology to enhance transparency and efficiency.

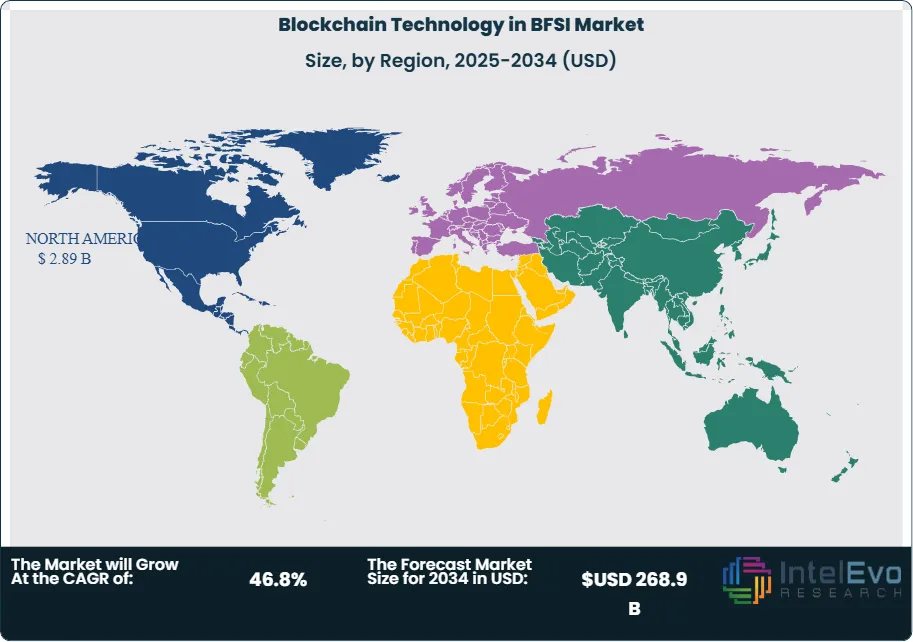

- Regional Analysis: North America dominated the market with a 38.5% share in 2024, supported by strong regulatory frameworks and high investment from U.S. and Canadian banks. Meanwhile, Europe shows deep adoption, with nearly 90% of regional banks piloting blockchain solutions, while Asia-Pacific is emerging as the next investment hotspot.

Type Analysis

Private blockchains continue to hold the largest share of adoption in the BFSI blockchain market, maintaining more than half of the market share as of 2024 and projected to strengthen further through 2030. Their dominance is rooted in superior data privacy, permissioned access, and compliance-driven design, which align with the security-sensitive requirements of banking and insurance institutions. Unlike public blockchains, which often face bottlenecks due to broad consensus mechanisms, private networks enable higher transaction throughput and faster processing, a critical factor for real-time settlement and high-frequency financial operations.

In addition to scalability, private blockchains offer enhanced auditability and regulatory alignment, enabling institutions to meet stringent standards across regions such as North America and Europe. Leading banks and insurance providers are leveraging these networks for applications such as cross-border payments, fraud detection, and secure transmission of policyholder data. With financial firms increasingly prioritizing operational efficiency and customer trust, private blockchains are expected to remain the dominant type, even as consortium blockchains gradually gain traction for interbank collaborations.

Deployment Mode Analysis

Cloud-based blockchain deployments have emerged as the preferred mode for BFSI institutions, accounting for more than 57% of the market share in 2024 and anticipated to expand further. Their leadership is attributed to lower upfront infrastructure costs, scalability, and ease of integration with digital banking ecosystems. For small and medium-sized financial enterprises, the cloud model reduces barriers to entry by eliminating the need for extensive IT infrastructure, accelerating blockchain adoption across diverse geographies.

The inherent flexibility of cloud platforms allows financial organizations to integrate blockchain seamlessly with existing applications such as digital wallets, payment gateways, and insurance claim management systems. Additionally, cloud deployment enhances resilience through redundancy and advanced disaster recovery capabilities, ensuring uninterrupted operations in case of security breaches or system failures. As the sector prioritizes agility and innovation, cloud-based solutions are expected to solidify their dominance, while on-premise models remain relevant for institutions requiring maximum control over sensitive data.

Enterprise Size Analysis

Small and medium-sized enterprises (SMEs) are emerging as the most dynamic adopters of blockchain in the BFSI sector, capturing nearly 58% of the market in 2024. Their agility in implementing new technologies, combined with the need to minimize costs and increase transparency, positions blockchain as an ideal fit. SMEs are particularly leveraging blockchain for cross-border payments, identity verification, and trade financing—processes that often involve high fees and slow settlement when conducted through traditional channels.

Blockchain also provides SMEs access to new financing avenues through tokenization and smart contracts, allowing them to tap into innovative funding models outside conventional banking systems. The ability to establish immutable audit trails and ensure secure transactions further enhances customer trust, enabling smaller institutions to compete more effectively against established incumbents. As blockchain solutions become more modular and affordable, SME adoption is projected to accelerate, shaping this segment into a long-term growth driver for the global BFSI blockchain market.

Regional Analysis

North America remains the leading regional market, capturing nearly 39% of global blockchain in BFSI revenue in 2024, underpinned by a concentration of financial hubs, strong venture funding, and progressive regulatory frameworks. The U.S. in particular is spearheading adoption through initiatives by Wall Street banks, fintech startups, and technology leaders, supported by government pilot projects in digital currencies and blockchain-based identity verification. The region’s emphasis on cybersecurity and fraud prevention further drives blockchain adoption across banks, insurers, and asset management firms.

Europe follows closely, with nearly 90% of major banks experimenting with blockchain applications in payments and compliance. The region’s regulatory clarity, particularly under the European Union’s Markets in Crypto-Assets (MiCA) framework, is accelerating integration. Meanwhile, Asia-Pacific is emerging as the fastest-growing regional market, fueled by large-scale fintech adoption in China and India, proactive government programs in Singapore, and the rapid digitization of cross-border trade. Latin America and the Middle East & Africa are in earlier stages of adoption but present high-potential opportunities as blockchain is increasingly leveraged to address financial inclusion and remittance challenges.

Would you like me to expand this into a comparative data table (e.g., Type, Deployment, Enterprise Size, Region with 2024 market shares and 2030 projections) to make it more executive-friendly?

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Public

- Private

- Consortium

By Deployment Mode

- Cloud

- On-Premise

By Enterprise Size

- SMEs

- Large Enterprises

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 7.4 B |

| Forecast Revenue (2034) | USD 268.9 B |

| CAGR (2024-2034) | 46.8% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Public, Private, Consortium), By Deployment Mode (Cloud, On-Premise), By Enterprise Size (SMEs, Large Enterprises) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | JP Morgan, Oracle, Accenture, Bitfury Group Limited, Infosys Limited, Amazon Web Services, SAP, Auxesis Group, IBM, Microsoft |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment Mode (Cloud, On-Premise), By Enterprise Size (SMEs, Large Enterprises), Digital Finance Transformation, Investment Trends & Forecast 2025–2034")

, By Deployment Mode (Cloud, On-Premise), By Enterprise Size (SMEs, Large Enterprises), Digital Finance Transformation, Investment Trends & Forecast 2025–2034")

, By Deployment Mode (Cloud, On-Premise), By Enterprise Size (SMEs, Large Enterprises), Digital Finance Transformation, Investment Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Blockchain Technology in BFSI Market?

The Blockchain Technology in BFSI Market is projected to grow from USD 7.4 Billion in 2024 to USD 268.9 Billion by 2034, at a CAGR of 46.8%. Rapid adoption of decentralized finance, smart contracts, and secure digital transactions is transforming global banking, insurance, and fintech ecosystems.

Who are the major players in the Blockchain Technology in BFSI Market?

JP Morgan, Oracle, Accenture, Bitfury Group Limited, Infosys Limited, Amazon Web Services, SAP, Auxesis Group, IBM, Microsoft

Which segments covered the Blockchain Technology in BFSI Market?

By Type (Public, Private, Consortium), By Deployment Mode (Cloud, On-Premise), By Enterprise Size (SMEs, Large Enterprises)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Blockchain Technology In BFSI Market

Published Date : 14 Nov 2025 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date