- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Blue Hydrogen Market Size & Forecast | CAGR 11.4%

Global Blue Hydrogen Production from Natural Gas Market Size, Share, Growth & Industry Analysis By Production Technology (Steam Methane Reforming SMR-CCS, Autothermal Reforming ATR-CCS, Partial Oxidation POx-CCS), By End-Use Application (Ammonia, Refining, Methanol, Power Generation, Steel, Mobility), By Carbon Capture Rate (High, Medium, Low), By Distribution Mode (On-Site, Pipeline, Liquefied Transport) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

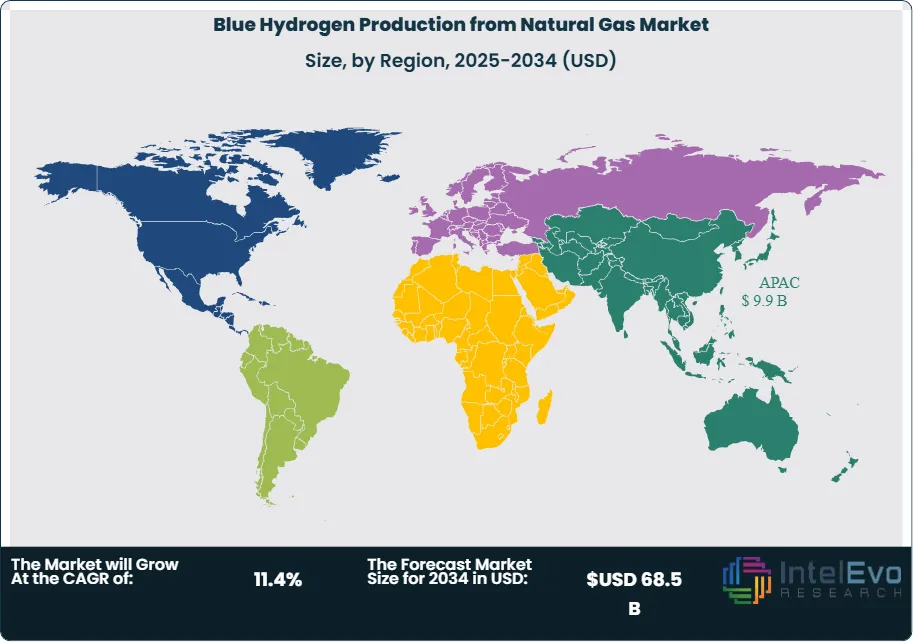

| USD 25.8 Billion | USD 68.5 Billion | 11.4% | Asia Pacific, 38.2% |

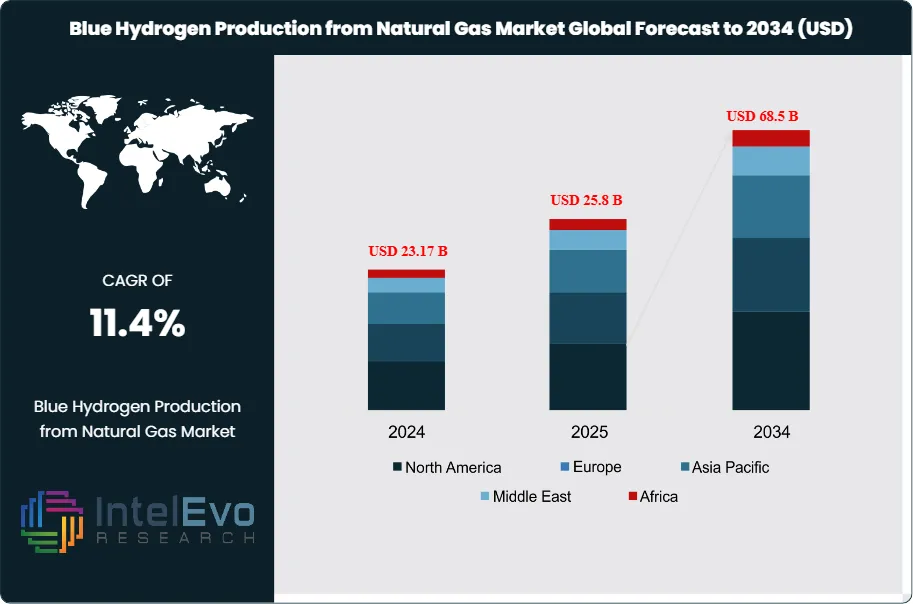

The Blue Hydrogen Production from Natural Gas Market was valued at approximately USD 23.17 Billion in 2024 and reached USD 25.8 Billion in 2025. The market is projected to grow to USD 68.5 Billion by 2034, expanding at a CAGR of 11.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 42.7 Billion over the analysis period. Blue hydrogen, produced through steam methane reforming (SMR) or autothermal reforming (ATR) of natural gas with integrated carbon capture, utilization, and storage (CCUS), has emerged as a commercially viable bridge fuel between conventional grey hydrogen and fully renewable green hydrogen.

Get More Information about this report -

Request Free Sample ReportGlobal hydrogen demand reached approximately 97 million tonnes in 2025, of which less than 4% qualified as low-carbon production. Government policy frameworks are accelerating the shift from unabated grey hydrogen to blue hydrogen. The U.S. Inflation Reduction Act (IRA) provides a production tax credit (PTC) of up to USD 3.00 per kilogram for clean hydrogen meeting lifecycle emissions thresholds below 0.45 kg CO2e/kg H2, directly incentivizing blue hydrogen projects paired with high-rate CCUS. The European Union Hydrogen Strategy targets 10 million tonnes of domestic clean hydrogen production and an additional 10 million tonnes of imports by 2030, creating substantial demand pull for blue hydrogen producers in Norway, the Netherlands, and the United Kingdom.

Asia Pacific held the largest regional share at 38.2% of global blue hydrogen market revenue in 2025, driven by Japan and South Korea importing blue ammonia for co-firing in thermal power generation, and China investing in large-scale SMR-CCS clusters in Xinjiang and Inner Mongolia. North America accounted for 28.5%, fueled by Gulf Coast project development and abundant low-cost natural gas from the Permian Basin and Appalachian shale formations. The blue hydrogen production from natural gas market is shaped by three converging forces: tightening carbon pricing mechanisms across OECD nations, declining CCUS costs that fell 18% between 2021 and 2025, and rising corporate net-zero commitments that now cover over 65% of global GDP. The IEA reported that announced blue hydrogen projects with final investment decisions (FID) exceeded 1.8 million tonnes per annum of capacity globally by mid-2025, a threefold increase from 2022 levels. Technology advances in ATR-based designs with CO2 capture rates exceeding 95% are reducing lifecycle emissions intensity, strengthening the environmental case for blue hydrogen as a decarbonization solution for hard-to-abate sectors including steelmaking, ammonia synthesis, refining, and heavy-duty transport.

, By End-Use Application (Ammonia, Refining, Methanol, Power Generation, Steel, Mobility), By Carbon Capture Rate (High, Medium, Low), By Distribution Mode (On-Site, Pipeline, Liquefied Transport) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The blue hydrogen production from natural gas market was valued at USD 25.8 Billion in 2025 and is projected to reach USD 68.5 Billion by 2034 at a CAGR of 11.4% over the nine-year forecast period.

- Segment Dominance (By Production Technology): Steam methane reforming with CCS accounted for 62.4% of global blue hydrogen revenue in 2025, reflecting the mature installed base and lower capital intensity relative to ATR pathways.

- Segment Dominance (By End-Use Application): Ammonia production represented 29.8% of blue hydrogen demand in 2025, driven by large-scale fertilizer manufacturing and emerging blue ammonia export supply chains.

- Driver: Government incentives and carbon pricing mechanisms contributed an estimated USD 6.2 Billion in direct subsidies and tax credits to blue hydrogen projects globally in 2025, reducing levelized costs by 22–28% for qualifying facilities.

- Restraint: Upstream methane leakage concerns and inconsistent measurement, reporting, and verification (MRV) standards threaten lifecycle emission claims, with studies estimating 0.5–3.0% fugitive emission rates across supply chains.

- Opportunity: Blue ammonia as a hydrogen carrier for long-distance maritime trade represents a USD 14.5 Billion addressable segment by 2034, with Japan and South Korea alone contracting 8.2 million tonnes per annum in offtake agreements.

- Trend: Autothermal reforming (ATR) adoption is accelerating, with ATR-based project announcements increasing from 12% of new capacity in 2022 to 34% in 2025, owing to CO2 capture rates above 95%.

- Regional Analysis: Asia Pacific led the global blue hydrogen production from natural gas market with a 38.2% share valued at USD 9.9 Billion in 2025, anchored by Japanese and South Korean import programs and Chinese domestic production expansion.

Competitive Landscape Overview

The blue hydrogen production from natural gas market is moderately consolidated, with the top four players — Air Liquide, Linde, Air Products, and Shell — commanding an estimated 44% of global project capacity in 2025. Competition is driven primarily by CCUS technology capability, access to low-cost natural gas feedstock, and long-term offtake security with industrial and utility buyers. Merger and acquisition activity intensified through 2024–2025 as integrated energy companies sought to secure carbon storage permits, pipeline infrastructure, and electrolyzer-agnostic production optionality. New entrants from the Middle East, including ADNOC and Saudi Aramco, are scaling blue ammonia export capacity to penetrate Asian demand centers.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product/Solution | Geo Strength | Recent Strategic Move (2024–2026) |

| Air Liquide | France | Leader | Autothermal Reforming with CCS | Europe | Commissioned 200 kt/yr blue H2 unit in Netherlands, Q1 2025 |

| Linde plc | Ireland/UK | Leader | Large-Scale SMR-CCS Platforms | North America | Signed 15-year offtake with Gulf Coast ammonia producer, Mar 2025 |

| Air Products | United States | Leader | NEOM Green/Blue H2 JV Complex | Middle East & Africa | FID on Louisiana blue H2 facility at USD 4.5B, Feb 2025 |

| Shell plc | Netherlands | Leader | Polaris CCS-Linked H2 Project | Europe | Expanded Holland Hydrogen I capacity target to 250 MW, Jun 2025 |

| TotalEnergies | France | Challenger | Normandy H2 Hub with CCS | Europe | Partnered with ADNOC on blue ammonia corridor to Europe, Jan 2026 |

| bp plc | United Kingdom | Challenger | H2Teesside Blue Hydrogen Project | Europe | Received UK CCUS Track-1 cluster approval, Dec 2024 |

| ExxonMobil | United States | Challenger | Baytown Low-Carbon H2 Complex | North America | Commenced construction on 1 Bn cfd hydrogen plant, Sep 2025 |

| Equinor ASA | Norway | Challenger | H2H Saltend Project (SMR+CCS) | Europe | Signed CO2 transport agreement with Northern Lights JV, Apr 2025 |

| Saudi Aramco | Saudi Arabia | Niche Player | Blue Ammonia Export Operations | Middle East | Shipped 50th blue ammonia cargo to Japan, Nov 2025 |

| ADNOC | UAE | Niche Player | Ta'ziz Blue Hydrogen Derivatives | Middle East | Awarded EPC for 1 MTPA blue ammonia plant, Jul 2025 |

By Production Technology.

Steam methane reforming with carbon capture (SMR-CCS) dominated the blue hydrogen production from natural gas market in 2025, accounting for 62.4% of total revenue at approximately USD 16.1 Billion. SMR-CCS benefits from decades of commercial deployment; over 500 large-scale SMR units operate globally, and retrofitting existing units with post-combustion capture requires 30–40% lower capital expenditure than greenfield ATR builds. However, CO2 capture rates for SMR-CCS typically range between 55–90% depending on configuration, which has prompted tighter regulatory scrutiny under EU and U.S. lifecycle emission standards.

Autothermal reforming with CCS (ATR-CCS) held a 26.3% share valued at USD 6.8 Billion in 2025. ATR technology is gaining ground due to inherently higher CO2 capture efficiency, with leading configurations achieving 95–97% capture rates. Projects such as the H2H Saltend facility in the UK and Air Liquide's Normandy hub are built on ATR platforms. Partial oxidation with CCS (POx-CCS) comprised the remaining 11.3% of the market at USD 2.9 Billion, serving niche applications where heavy hydrocarbon or high-sulfur gas feedstocks limit SMR viability, particularly in refinery-integrated hydrogen production across the Middle East and Russia.

By End-Use Application.

Ammonia production was the largest end-use application for blue hydrogen in 2025, representing 29.8% of market demand at USD 7.7 Billion. Industrial ammonia synthesis consumes roughly 33 million tonnes of hydrogen annually worldwide, and the transition from grey to blue hydrogen in fertilizer feedstock is accelerating in regions with carbon tax exposure above USD 50 per tonne of CO2. Refining operations accounted for 26.1% (USD 6.7 Billion), as petroleum refiners use hydrogen for hydrocracking and desulfurization; regulatory mandates such as the EU Carbon Border Adjustment Mechanism (CBAM) are pushing refiners to decarbonize hydrogen supply. Methanol production held 14.5% (USD 3.7 Billion), supported by rising demand for low-carbon methanol in maritime fuel and chemical feedstock applications.

Power generation captured 12.9% of blue hydrogen demand (USD 3.3 Billion) in 2025, primarily through ammonia co-firing in Japanese and South Korean coal-fired power stations and hydrogen blending in natural gas turbines across Europe. Steel and iron production represented 9.4% (USD 2.4 Billion), as direct reduced iron (DRI) processes increasingly substitute blue hydrogen for metallurgical coal. Mobility and transport applications comprised the remaining 7.3% (USD 1.9 Billion), covering fuel cell vehicle refueling and heavy-duty trucking corridors in California, Germany, and South Korea.

By Carbon Capture Rate.

High-capture-rate systems (above 90% CO2 capture) accounted for 41.7% of global blue hydrogen project capacity in 2025, valued at USD 10.8 Billion. These installations qualify for the highest tier of U.S. IRA production tax credits and meet the EU delegated act threshold for renewable and low-carbon hydrogen certification. Medium-capture-rate systems (60–90%) represented the bulk of the installed base at 45.6% (USD 11.8 Billion), reflecting the large fleet of SMR units retrofitted with amine-based post-combustion capture. Low-capture-rate systems (below 60%) held 12.7% (USD 3.3 Billion), concentrated in legacy refinery hydrogen plants where full capture upgrades are not yet economically justified.

By Distribution Mode.

On-site (captive) production dominated blue hydrogen distribution in 2025, capturing 58.3% of the market at USD 15.0 Billion. Large industrial consumers such as refineries, ammonia plants, and steel mills operate dedicated SMR-CCS or ATR-CCS units within facility boundaries, eliminating transport logistics and compression costs. Merchant (pipeline-delivered) hydrogen held 28.9% (USD 7.5 Billion), concentrated in the U.S. Gulf Coast hydrogen pipeline network spanning over 2,600 km and Northwest European industrial corridors linking Rotterdam, Antwerp, and the Ruhr Valley. Merchant (compressed/liquefied transport) comprised 12.8% (USD 3.3 Billion), serving distributed industrial users and emerging mobility refueling stations that lack pipeline access.

Regional Analysis

Asia Pacific.

Asia Pacific led the blue hydrogen production from natural gas market with a 38.2% share, generating USD 9.9 Billion in revenue in 2025. Japan anchored regional demand through its Strategic Hydrogen Roadmap, which targets 12 million tonnes of annual hydrogen supply by 2040 with blue hydrogen and blue ammonia as primary transition fuels. JERA, Japan's largest power generator, contracted 500,000 tonnes per annum of blue ammonia imports for co-firing at the Hekinan thermal power station. South Korea's Hydrogen Economy Promotion Roadmap allocated KRW 2.3 trillion (approximately USD 1.7 Billion) in subsidies for clean hydrogen infrastructure between 2025 and 2030. China deployed over 1.2 GW of blue hydrogen capacity in 2025 across state-owned enterprise-led projects in Xinjiang, Shaanxi, and Inner Mongolia, leveraging low-cost coal-bed methane and pipeline gas from the Central Asian corridor. India's National Green Hydrogen Mission, while focused on electrolytic hydrogen, has indirectly stimulated blue hydrogen interest among domestic fertilizer producers seeking near-term decarbonization at lower capital intensity. Australia's CarbonNet and Hydrogen Energy Supply Chain (HESC) projects continued progressing toward commercial-scale blue hydrogen liquefaction for export to Japan.

North America.

North America accounted for 28.5% of global blue hydrogen market revenue at USD 7.4 Billion in 2025. The United States drove the overwhelming majority of regional activity, supported by the IRA Section 45V clean hydrogen PTC, Department of Energy Regional Clean Hydrogen Hub (H2Hub) awards totaling USD 7 Billion across seven designated hubs, and access to Henry Hub natural gas prices averaging below USD 3.00 per MMBtu. The Gulf Coast corridor from Houston to Lake Charles concentrates the highest density of announced blue hydrogen projects, benefiting from over 900 miles of dedicated hydrogen pipelines, prolific geological formations for CO2 sequestration, and proximity to petrochemical and refining offtakers. ExxonMobil's Baytown project (1 billion cubic feet per day of hydrogen) and Air Products' Louisiana complex (USD 4.5 Billion investment) represent flagship developments. Canada contributed approximately USD 1.1 Billion, anchored by Alberta's Industrial Heartland hydrogen cluster and the federal Clean Hydrogen Investment Tax Credit offering up to 40% of eligible capital costs. Mexico remained a nascent participant, with exploratory feasibility studies in Monterrey and Tampico linked to Pemex refinery modernization.

Europe.

Europe held 21.8% of the global blue hydrogen production from natural gas market in 2025, valued at USD 5.6 Billion. The United Kingdom led European blue hydrogen development, anchored by the East Coast Cluster and HyNet North West, both of which received Track-1 CCUS allocation from the UK government. BP's H2Teesside project (1.2 GW capacity) and Equinor's H2H Saltend facility represent the most advanced large-scale developments. The Netherlands invested heavily in port-based blue hydrogen infrastructure at Rotterdam, where Air Liquide commissioned a 200 kt/yr blue hydrogen unit integrated with Porthos CO2 storage. Norway leveraged its extensive North Sea CO2 storage capacity through the Northern Lights joint venture, offering transport and storage services to European blue hydrogen producers. Germany, despite its stated preference for green hydrogen, approved bridge funding for blue hydrogen in industrial applications where electrolytic alternatives remain cost-prohibitive before 2030. The EU Emissions Trading System (ETS) carbon price, which averaged EUR 68 per tonne in 2025, provided a strong economic incentive for heavy industry to switch from grey to blue hydrogen.

Latin America.

Latin America represented 5.8% of the global blue hydrogen market at USD 1.5 Billion in 2025. Brazil led regional activity, with Petrobras initiating a USD 600 Million blue hydrogen pilot at its Bahia refinery complex integrated with enhanced oil recovery CO2 injection. Argentina's Vaca Muerta shale gas basin offered feedstock cost advantages for potential blue hydrogen production, though infrastructure limitations and regulatory uncertainty delayed FID on proposed projects. Trinidad and Tobago, a major ammonia exporter, explored blue hydrogen conversion for its existing methanol and ammonia plants operated by Nutrien and Proman. Mexico's participation remained limited but growing, with SENER (Secretariat of Energy) publishing preliminary hydrogen strategy guidelines in late 2025 that include provisions for blue hydrogen linked to CCS in depleted oil fields along the Gulf of Campeche.

Middle East & Africa.

The Middle East & Africa region captured 5.7% of global blue hydrogen revenue at USD 1.5 Billion in 2025. The UAE and Saudi Arabia dominated regional production. Saudi Aramco operated the world's largest blue ammonia demonstration facility at Jubail, exporting certified cargos to Japanese and South Korean utilities. ADNOC advanced the Ta'ziz industrial complex in Ruwais, awarding EPC contracts for a 1 MTPA blue ammonia plant with carbon capture linked to the Al Reyadah CO2 injection network. Qatar explored integration of blue hydrogen with its North Field LNG expansion, leveraging surplus associated gas. Oman's Hydrogen Strategy positioned the Sultanate as a future blue and green hydrogen export hub, with the Duqm Special Economic Zone earmarked for production facilities. South Africa investigated blue hydrogen feasibility through Sasol's existing Fischer-Tropsch operations, evaluating CCS potential in the Mpumalanga basin. Low domestic natural gas prices across the Gulf Cooperation Council (GCC), averaging below USD 1.50 per MMBtu, provided unmatched feedstock cost advantages that positioned Middle Eastern producers as the lowest-cost blue hydrogen suppliers globally.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Production Technology

- Steam Methane Reforming with CCS (SMR-CCS)

- Autothermal Reforming with CCS (ATR-CCS)

- Partial Oxidation with CCS (POx-CCS)

By End-Use Application

- Ammonia Production

- Refining

- Methanol Production

- Power Generation

- Steel and Iron Production

- Mobility and Transport

By Carbon Capture Rate

- High Capture Rate (Above 90%)

- Medium Capture Rate (60–90%)

- Low Capture Rate (Below 60%)

By Distribution Mode

- On-Site (Captive) Production

- Merchant (Pipeline-Delivered)

- Merchant (Compressed/Liquefied Transport)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 25.8 B |

| Forecast Revenue (2034) | USD 68.5 B |

| CAGR (2025-2034) | 11.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Production Technology, (Steam Methane Reforming with CCS (SMR-CCS), Autothermal Reforming with CCS (ATR-CCS), Partial Oxidation with CCS (POx-CCS)), By End-Use Application, (Ammonia Production, Refining, Methanol Production, Power Generation, Steel and Iron Production, Mobility and Transport), By Carbon Capture Rate, (High Capture Rate (Above 90%), Medium Capture Rate (60–90%), Low Capture Rate (Below 60%)), By Distribution Mode, (On-Site (Captive) Production, Merchant (Pipeline-Delivered), Merchant (Compressed/Liquefied Transport)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | AIR LIQUIDE, LINDE PLC, AIR PRODUCTS, SHELL PLC, TOTALENERGIES, BP PLC, EXXONMOBIL, EQUINOR ASA, SAUDI ARAMCO, ADNOC, CHEVRON CORPORATION, TECHNIP ENERGIES, JOHNSON MATTHEY, TOPSOE A/S, KBR INC., INEOS, PLUG POWER (BLUE H2 JV DIVISION), WOODSIDE ENERGY, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-Use Application (Ammonia, Refining, Methanol, Power Generation, Steel, Mobility), By Carbon Capture Rate (High, Medium, Low), By Distribution Mode (On-Site, Pipeline, Liquefied Transport) Industry Trends & Forecast 2026–2034")

, By End-Use Application (Ammonia, Refining, Methanol, Power Generation, Steel, Mobility), By Carbon Capture Rate (High, Medium, Low), By Distribution Mode (On-Site, Pipeline, Liquefied Transport) Industry Trends & Forecast 2026–2034")

, By End-Use Application (Ammonia, Refining, Methanol, Power Generation, Steel, Mobility), By Carbon Capture Rate (High, Medium, Low), By Distribution Mode (On-Site, Pipeline, Liquefied Transport) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Blue Hydrogen Production from Natural Gas Market?

Global Blue hydrogen market valued at USD 23.17B in 2024, reaching USD 68.5B by 2034, growing at a CAGR of 11.4% from 2026–2034.

Who are the major players in the Blue Hydrogen Production from Natural Gas Market?

AIR LIQUIDE, LINDE PLC, AIR PRODUCTS, SHELL PLC, TOTALENERGIES, BP PLC, EXXONMOBIL, EQUINOR ASA, SAUDI ARAMCO, ADNOC, CHEVRON CORPORATION, TECHNIP ENERGIES, JOHNSON MATTHEY, TOPSOE A/S, KBR INC., INEOS, PLUG POWER (BLUE H2 JV DIVISION), WOODSIDE ENERGY, OTHERS

Which segments covered the Blue Hydrogen Production from Natural Gas Market?

By Production Technology, (Steam Methane Reforming with CCS (SMR-CCS), Autothermal Reforming with CCS (ATR-CCS), Partial Oxidation with CCS (POx-CCS)), By End-Use Application, (Ammonia Production, Refining, Methanol Production, Power Generation, Steel and Iron Production, Mobility and Transport), By Carbon Capture Rate, (High Capture Rate (Above 90%), Medium Capture Rate (60–90%), Low Capture Rate (Below 60%)), By Distribution Mode, (On-Site (Captive) Production, Merchant (Pipeline-Delivered), Merchant (Compressed/Liquefied Transport))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Blue Hydrogen Production from Natural Gas Market

Published Date : 24 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date