- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Brainwave-Sensing Headband Market Size, Share | CAGR 15.1%

Global Brainwave-Sensing Headband Market Size, Share, Analysis By Product Type (EEG Headbands, fNIRS Headbands, EMG Wearables, Hybrid Multi-Sensor Platforms), By Application (Sleep Quality Monitoring, Meditation & Mindfulness, Cognitive Training, Neurological Diagnosis, Elite Sports Performance), By End-User (Hospitals & Clinics, Research Institutes, Personal Consumer Wellness) Industry Region & Key Players-Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

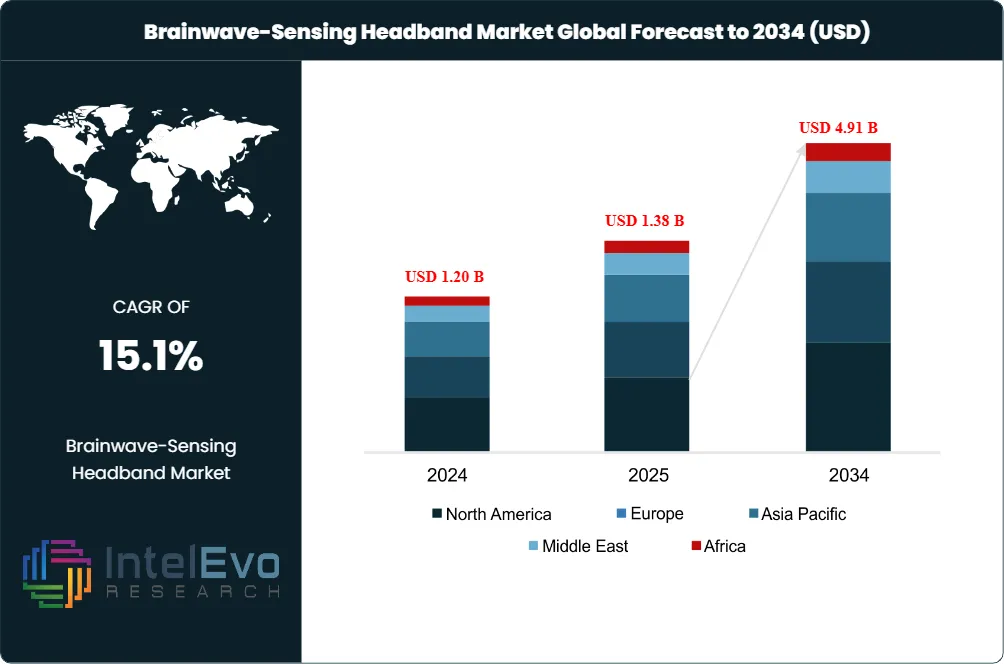

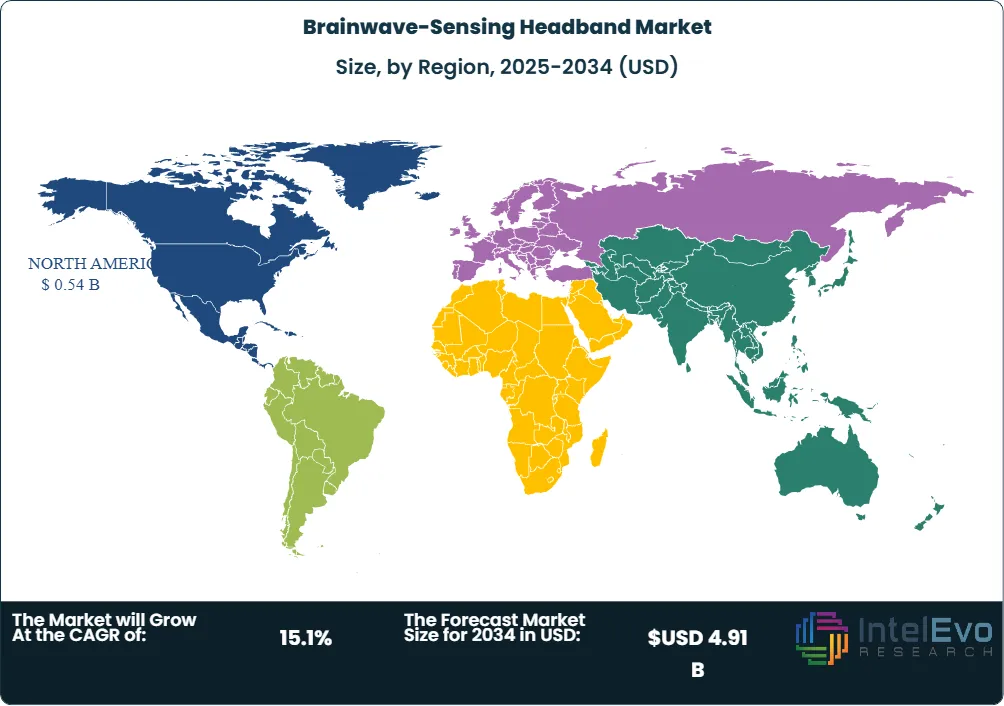

| USD 1.38 Billion | USD 4.91 Billion | 15.1% | North America, 39.2% |

The Brainwave-Sensing Headband Market was valued at USD 1.20 Billion in 2024 and USD 1.38 Billion in 2025. The market is projected to reach USD 4.91 Billion by 2034, expanding at a CAGR of 15.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 3.53 Billion over the analysis period. The brainwave-sensing headband market covers non-invasive electroencephalography headbands, head-mounted EEG modules, software analytics, and subscription services that convert cortical electrical signals into sleep, focus, stress, cognitive-load, seizure-screening, and research data.

Get More Information about this report -

Request Free Sample ReportDemand is rising because neurological care, mental fitness, and consumer sleep technology are converging around lower-friction brain monitoring. World Health Organization reporting in 2024 and 2025 placed neurological conditions above 3 billion affected people worldwide, creating demand for earlier screening and remote observation. At the same time, Muse by InteraXon, Neurable, EMOTIV, OpenBCI, Zeto, Neuroelectrics, Natus Medical, Ceribell, and NaoX Technologies are pushing EEG from clinics into headbands, headphones, caps, and ear-worn systems. The commercial logic is direct: reduced setup time expands EEG use from specialist labs to homes, schools, sports facilities, emergency departments, and human-performance programs.

The brainwave-sensing headband market is also supported by consumer wellness behavior. Muse positions its headband around meditation and sleep feedback, Elemind targets sleep onset using real-time brainwave response, and Neurable embeds EEG sensors into headphones for focus scoring and cognitive-fatigue signals. These devices use fewer electrodes than clinical EEG systems, but they compensate through app workflows, signal-quality filters, and cloud analytics. This trade-off explains why wellness and sleep accounted for the largest application share in 2025, while regulated clinical use grew more slowly because FDA clearance, CE marking, data privacy, and validation evidence remain strict purchase barriers.

Regulation is becoming a growth filter rather than a simple obstacle. FDA 510(k) clearances for wearable or rapid EEG systems from Epitel, Forest Devices, Ceribell, Natus Medical, and NaoX Technologies during 2025 created a clearer approval pathway for portable brain monitoring. In Europe, the Medical Device Regulation applies when headbands make medical claims, while consumer neurotechnology remains more exposed to GDPR, product safety, AI governance, and consumer protection scrutiny. This bifurcation favors vendors that can sell wellness products without overstating clinical benefit, while maintaining a separate regulatory dossier for healthcare channels.

North America held 39.2% of the brainwave-sensing headband market in 2025, equal to USD 0.54 Billion, supported by U.S. neurotechnology funding, FDA regulatory precedents, and early adoption by wellness buyers. Asia Pacific is forecast to post the fastest regional CAGR through 2034 because China, Japan, South Korea, Singapore, and India are expanding mental-health, sleep-tech, and digital-health procurement. Through 2034, the market will shift from single-purpose meditation headbands toward multimodal head-worn systems that combine EEG, accelerometry, photoplethysmography, acoustic stimulation, app coaching, and AI-based brain-state interpretation.

Market Definition & Scope

The brainwave-sensing headband market is defined as the global commercial activity surrounding head-worn devices that measure electrical brain activity through electroencephalography electrodes and convert those signals into user-facing or clinician-facing digital outputs. The market encompasses consumer EEG meditation bands, sleep-assistance headbands, research-grade wireless EEG caps, gaming and productivity headsets with embedded brain sensors, and regulated portable EEG systems used for neurological monitoring or triage.

This analysis includes hardware, replacement electrodes, headbands, conductive pads, charging accessories, mobile applications, cloud dashboards, algorithm subscriptions, developer tools, and enterprise analytics sold by Muse, Neurable, EMOTIV, OpenBCI, Zeto, Neuroelectrics, Natus Medical, Ceribell, Elemind, NaoX Technologies, and related vendors. It excludes implantable brain-computer interfaces, hospital stationary EEG consoles, polysomnography systems without wearable EEG headbands, and non-EEG wellness bands that only measure heart rate, motion, skin temperature, or photoplethysmography. The parent category is wearable neurotechnology, with brainwave-sensing headbands representing the commercial layer closest to consumer adoption.

, By Application (Sleep Quality Monitoring, Meditation & Mindfulness, Cognitive Training, Neurological Diagnosis, Elite Sports Performance), By End-User (Hospitals & Clinics, Research Institutes, Personal Consumer Wellness) Industry Region & Key Players-Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The brainwave-sensing headband market increased to USD 1.38 Billion in 2025 and is projected to reach USD 4.91 Billion by 2034 at a 15.1% CAGR.

- Segment Dominance: Consumer wellness and sleep headbands led the product mix with 46.5% share in 2025, equal to approximately USD 0.64 Billion.

- Segment Dominance: Sleep, focus, and mental-fitness applications held 42.6% share in 2025, ahead of meditation, clinical monitoring, research, and gaming use cases.

- Driver: The leading demand driver is low-friction brain monitoring, supported by more than 3 billion people living with neurological conditions and rising consumer spend on sleep technology.

- Restraint: Signal reliability remains the principal constraint because four-channel or six-channel consumer EEG provides narrower diagnostic coverage than 19-channel clinical EEG.

- Opportunity: Clinical triage and remote neurological monitoring represent a USD 1.05 Billion opportunity by 2034 as rapid EEG, ambulatory EEG, and cloud review tools expand.

- Trend: Multimodal head-worn devices are replacing single-signal headbands, with EEG being combined with motion, heart-rate, fNIRS, audio stimulation, and AI analytics.

- Regional: North America led the brainwave-sensing headband market with 39.2% share and USD 0.54 Billion in 2025 revenue.

Key Insights Summary

- The brainwave-sensing headband market benefits from a large clinical need base, with WHO-linked neurological burden analysis showing more than 3 billion people living with neurological conditions in 2021.

- Portable EEG regulation accelerated in 2025, with FDA 510(k) actions covering wearable systems from Epitel, Forest Devices, Ceribell, Natus Medical, and NaoX Technologies.

- Muse by InteraXon markets consumer EEG meditation and sleep headbands supported by more than 200 published research studies and institutional use cases across wellness and research.

- Neurable secured USD 35 Million in Series A funding in December 2025 and moved in April 2026 toward a licensing model for embedding EEG analytics into third-party head-worn products.

- Elemind sells a sleep-focused neurotechnology headband priced around USD 349 in the United States, using EEG-responsive acoustic stimulation to shorten sleep onset.

- OpenBCI offers open-source EEG hardware and the Galea multimodal headset for researchers and extended-reality developers, reinforcing the developer segment of the market.

- Consumer neurotechnology faces rising policy scrutiny in Europe because non-medical brain-data devices sit between wellness regulation, GDPR, AI rules, and medical-device law.

Competitive Landscape Overview

The brainwave-sensing headband market is fragmented, with the top four vendors estimated to account for approximately 34% of 2025 revenue. Muse by InteraXon leads consumer meditation and sleep headbands, EMOTIV holds a strong position in research-grade consumer EEG, Neurable leads embedded EEG headphone licensing, and OpenBCI anchors the developer and academic community. Clinical vendors such as Zeto, Neuroelectrics, Natus Medical, Ceribell, Epitel, and NaoX Technologies compete from the regulated side rather than the wellness channel.

Competition is shaped by five purchase criteria: electrode comfort, signal quality, battery life, software interpretation, and regulatory claim discipline. Consumer buyers compare Muse, Elemind, Neurable, and EMOTIV by app experience and subscription utility. Hospitals and research buyers compare Zeto, Natus Medical, Neuroelectrics, OpenBCI, and Ceribell by setup time, cloud review, channel count, clinical validation, and data export. The competitive shift in 2026 is toward platform licensing, because Neurable's Powered by Neurable AI model and OpenBCI's open hardware approach can place brainwave sensing inside products that already sit on the head.

Competitive Landscape Matrix

| Company Name | Headquarters (Country) | Market Position | Key Product/Solution in this market | Geographic Strength | Recent Strategic Move |

| Muse by InteraXon Inc. | Canada | Leader | Muse S and Muse EEG meditation and sleep headbands | North America, Europe | Introduced expanded sleep and mental-fitness positioning with Muse S Athena in 2025 |

| EMOTIV Inc. | United States | Leader | EPOC X, Insight, MN8, EmotivPRO, EmotivIQ | North America, Asia Pacific, Europe | Expanded enterprise EEG analytics and research software content in 2026 |

| Neurable Inc. | United States | Leader | Neurable AI and MW75 Neuro brain-sensing headphones | North America, Europe | Raised USD 35 Million in December 2025 and moved to third-party licensing in April 2026 |

| OpenBCI Inc. | United States | Leader | Galea, Ultracortex, Cyton, Ganglion, OpenBCI GUI | Global developer base | Continued Galea shipments and open-source software updates through 2026 |

| Elemind Technologies, Inc. | United States | Challenger | Elemind EEG sleep headband | United States, Canada | Commercialized a sleep headband with EEG-responsive acoustic stimulation in 2025 |

| Zeto, Inc. | United States | Challenger | Wireless EEG headset and cloud EEG platform | United States | Secured USD 31 Million Series B funding in January 2025 |

| Neuroelectrics Corporation | Spain / United States | Challenger | Starstim and Enobio EEG/tES head-worn systems | Europe, United States | Advanced cloud-connected at-home neuromodulation and EEG programs in 2025-2026 |

| Natus Medical Incorporated | United States | Challenger | BrainWatch point-of-care EEG solution | North America, Europe | Received FDA clearance for electrographic status epilepticus indication in December 2025 |

| Ceribell, Inc. | United States | Challenger | Rapid EEG headband and Clarity AI monitoring | United States | Received FDA clearance for delirium monitoring in December 2025 |

| NaoX Technologies SAS | France | Niche Player | Naox Link in-ear EEG system | Europe, United States | Received FDA 510(k) clearance in November 2025 |

Segmentation Analysis

The brainwave-sensing headband market segments by product type, application, and end-user, with economics determined by electrode architecture, software subscription depth, and regulatory claims.

By Product Type

Consumer wellness and sleep headbands dominated the brainwave-sensing headband market with 46.5% share in 2025, equivalent to USD 0.64 Billion. Muse by InteraXon, Elemind, Neurable, and EMOTIV compete in this segment by reducing friction around daily use. Muse converts EEG into meditation and sleep feedback, while Elemind uses EEG-responsive audio to support sleep onset. Neurable's headphone format shows how the product definition is widening beyond forehead bands into devices worn around the head. Consumer products carry lower average selling prices than clinical systems, but they support recurring revenue through apps, coaching, data dashboards, and premium analytics.

Clinical and medical EEG headbands accounted for 23.0% share, or USD 0.32 Billion in 2025. Zeto, Natus Medical, Ceribell, Epitel, Forest Devices, NaoX Technologies, and Neuroelectrics serve hospitals, emergency departments, ambulatory neurology practices, and remote monitoring programs. This segment grows through FDA 510(k) activity, remote neurologist review, and labor savings caused by faster sensor placement. Clinical buyers accept higher hardware prices because seizure triage, delirium monitoring, ambulatory EEG, and refractory epilepsy programs require validated workflows. The segment is smaller than wellness in unit volume, but revenue per system and service contract value are higher.

Research and developer EEG headbands represented 18.0% share in 2025, equal to USD 0.25 Billion. EMOTIV, OpenBCI, Neuroelectrics, g.tec medical engineering, Brain Products, and Bitbrain serve universities, human-computer interaction labs, neuroscience groups, and neurofeedback developers. OpenBCI's Cyton, Ganglion, Ultracortex, and Galea products make data access central to the purchase decision. EMOTIV competes through software, API, and research metrics. This category is technically demanding because buyers inspect channel count, sample rate, impedance reporting, data export, synchronization, and compatibility with Unity, Lab Streaming Layer, Python, MATLAB, and virtual-reality engines.

Gaming, productivity, and enterprise cognitive-state headsets held 12.5% share in 2025, or USD 0.17 Billion. Neurable, HyperX, EMOTIV, and OpenBCI are visible in this sub-segment because gaming headsets, productivity headphones, and extended-reality devices already occupy the correct body position. The HyperX and Neurable CES 2026 prototype showed a route toward cognitive priming, reaction-time improvement, and fatigue prevention in esports. Enterprise buyers evaluate brainwave-sensing headband vendor selection through privacy terms, brain-data retention, workflow fit, and measurable productivity benefit rather than electrode count alone.

By Application

The brainwave-sensing headband market by application was led by sleep, focus, and mental fitness at 42.6% share in 2025, equivalent to USD 0.59 Billion. Muse, Elemind, Neurable, and EMOTIV address this demand by translating EEG into coaching, relaxation feedback, cognitive-load scores, or sleep-onset support. Sleep is commercially attractive because users already buy Oura Ring, Fitbit, Apple Watch, Eight Sleep, and CPAP-adjacent products, creating a receptive market for brain-specific data. The limitation is retention: a headband must remain comfortable across a full night, and subscriptions must provide enough daily value to avoid churn.

Meditation, stress management, and neurofeedback accounted for 21.8% share in 2025, or USD 0.30 Billion. Muse helped define this use case by using EEG-driven feedback for guided meditation, while EMOTIV and Neuroelectrics support research and neurofeedback protocols. The segment benefits from corporate wellness, school mindfulness programs, therapist-led neurofeedback, and athlete recovery. Compared with sleep products, meditation headbands face shorter daily session lengths and lower tolerance for complex setup. Vendors win when they pair simple session design with credible signal metrics and clear privacy disclosures.

Clinical monitoring and neurological triage captured 18.7% share in 2025, equal to USD 0.26 Billion. Zeto, Ceribell, Natus Medical, Epitel, Forest Devices, and NaoX Technologies are central to this segment because they sell into regulated healthcare settings. Hospitals use rapid or wearable EEG to screen seizures, monitor delirium signals, support ambulatory review, and lower dependence on scarce EEG technologists. Clinical adoption is slower than consumer adoption because reimbursement, physician trust, false-positive management, and software validation determine procurement. Yet the value per deployment is higher because each system can support multiple monitored patients per week.

Academic research, human-computer interaction, and brain-computer interface prototyping represented 10.4% share in 2025. OpenBCI, EMOTIV, Neuroelectrics, Bitbrain, and g.tec medical engineering support this segment with developer documentation, raw data access, and hardware that can be integrated into experiments. Buyers compare brainwave-sensing headband pricing benchmarks against medical EEG amplifiers, VR headsets, eye trackers, and motion-capture systems. The segment is valuable beyond revenue because research labs validate algorithms that later migrate into wellness, gaming, and medical products.

Gaming and performance training held 6.5% share in 2025, but it is forecast to grow faster than the total market through 2034. Neurable and HyperX demonstrated the strongest current signal after the CES 2026 gaming headset prototype. The value proposition is specific: monitor cognitive load before and during play, guide priming routines, and reduce performance crashes. This application will remain constrained until hardware becomes lighter, battery life improves, and publishers or esports teams accept brain-data analytics as fair and privacy-compliant.

By End-User

Consumers accounted for 51.3% of brainwave-sensing headband market revenue in 2025, equal to USD 0.71 Billion. Purchases came from sleep optimization, meditation, stress management, productivity, and quantified-self behavior. Muse, Elemind, Neurable, and EMOTIV compete for this buyer with app design, daily metrics, comfort, and price. Consumers are less interested in EEG channel count than in a repeatable benefit, such as falling asleep faster, sustaining focus, or building a meditation habit. This forces vendors to translate complex neurophysiology into simple, non-medical claims.

Healthcare providers and clinical networks represented 21.6% of 2025 revenue, or USD 0.30 Billion. Zeto, Ceribell, Natus Medical, Epitel, Forest Devices, NaoX Technologies, and Neuroelectrics sell into this channel with regulated products, cloud review, and clinical workflows. Hospitals compare implementation timelines, technician training, cybersecurity, FDA status, electrode replacement cost, and integration with electronic medical records. Compared with consumer adoption, clinical adoption requires more evidence but generates more durable account revenue.

Universities, research institutes, and developers held 15.7% share in 2025. OpenBCI, EMOTIV, Neuroelectrics, g.tec, and Bitbrain benefit from this group because researchers value hackability, raw EEG streams, and reproducible signal processing. Enterprise, sports, education, and gaming buyers represented the remaining 11.4% share. This segment is still young, but it is strategically important because Neurable's licensing model can place EEG inside products from audio, gaming, workplace, and extended-reality brands.

Regional Analysis

North America

North America led the brainwave-sensing headband market with 39.2% share and USD 0.54 Billion in 2025 revenue. The United States accounted for most regional demand because Muse, Neurable, EMOTIV, OpenBCI, Zeto, Ceribell, Epitel, and Forest Devices have strong commercial or regulatory footprints. FDA 510(k) clearances during 2025 for wearable and rapid EEG systems gave buyers clearer pathways for clinical procurement. U.S. consumer demand is also supported by sleep-technology spending, employer wellness programs, esports performance training, and mental-health awareness. Canada contributes through InteraXon and university neuroscience research, while Mexico remains a smaller market focused on private neurology clinics and wellness imports.

Europe

Europe held 25.5% share of the brainwave-sensing headband market in 2025, equivalent to USD 0.35 Billion. Demand is concentrated in Germany, the United Kingdom, France, Spain, the Netherlands, Switzerland, and the Nordic countries. Europe has strong research infrastructure, but commercialization is filtered by GDPR, the EU Medical Device Regulation, CE marking, consumer protection law, and AI governance. Neuroelectrics in Spain and NaoX Technologies in France strengthen the regional supplier base, while Muse, EMOTIV, OpenBCI, and Neurable sell into wellness and research channels. The policy issue is brain-data handling: consumer neurotechnology must prove that signal interpretation, consent, and storage practices match European expectations.

Asia Pacific

Asia Pacific represented 26.0% of 2025 revenue, or USD 0.36 Billion, and is forecast to record the fastest regional CAGR through 2034. Japan, China, South Korea, Singapore, Australia, and India are the main demand centers. Japan has a large sleep-health and aging population market, South Korea has esports and consumer electronics strength, and China is increasing BCI investment through research grants and private capital. India remains price-sensitive but has a large mental-health and education market for low-cost neurofeedback tools. Local vendors and import distributors will compete on affordability, language localization, and clinician training.

Latin America

Latin America accounted for 5.8% of the brainwave-sensing headband market in 2025, equal to USD 0.08 Billion. Brazil and Mexico are the largest country markets, supported by private neurology, university neuroscience labs, sleep clinics, and wellness buyers in large urban centers. Adoption is constrained by import duties, limited reimbursement, and uneven access to EEG-trained clinicians. Consumer wellness purchases occur through online channels, but clinical procurement depends on local distributors that can provide training and maintenance. Research-grade systems from EMOTIV, OpenBCI, and Neuroelectrics are more accessible than premium hospital systems in many public institutions.

Middle East & Africa

Middle East & Africa held 3.5% share in 2025, equivalent to USD 0.05 Billion. The United Arab Emirates, Saudi Arabia, Israel, South Africa, and Qatar account for most demand. Gulf healthcare modernization programs support digital-health pilots, while Israel contributes neurotechnology research and startup activity. South Africa has university and hospital-based demand, but broader African adoption is limited by device pricing, specialist availability, and clinical infrastructure. Through 2034, the region is likely to adopt cloud-reviewed portable EEG in private hospitals first, followed by wellness and school-based neurofeedback programs where privacy governance is explicit.

Country Analysis

United States

The United States brainwave-sensing headband market reached approximately USD 0.49 Billion in 2025 and is forecast to grow at a 14.5% country CAGR through 2034. Demand is supported by FDA-cleared portable EEG systems, consumer sleep-tech spending, remote neurological monitoring, and human-performance pilots. Neurable raised USD 35 Million in December 2025 and shifted toward broader licensing in April 2026, while Zeto secured USD 31 Million in January 2025 for EEG brain monitoring. Ceribell and Natus Medical received 2025 FDA clearances that strengthened point-of-care EEG confidence.

Canada

Canada's brainwave-sensing headband market reached approximately USD 0.05 Billion in 2025, with a projected 13.8% CAGR through 2034. InteraXon, the Toronto company behind Muse, gives Canada a meaningful role in the consumer EEG category despite the country's smaller population. Canadian buyers include wellness consumers, universities, sleep researchers, and private clinics. Provincial healthcare procurement remains cautious for medical claims, but Muse's research base and app-led wellness model support international demand. Canada's intellectual-property and commercialization programs also help smaller neurotechnology developers protect software, signal-processing, and head-worn hardware designs.

Germany

Germany's brainwave-sensing headband market reached approximately USD 0.08 Billion in 2025 and is forecast to grow at a 14.2% CAGR through 2034. Demand comes from university neuroscience, sleep clinics, digital therapeutics, occupational health, and private wellness buyers. German procurement is rigorous because MDR compliance, data protection, and clinical evidence affect hospital purchasing. EMOTIV, Muse, Neuroelectrics, OpenBCI, Natus Medical, and Zeto compete through distributors and direct enterprise relationships. German buyers tend to favor devices with transparent data export, documented signal quality, and clear separation between wellness claims and medical claims.

China

China's brainwave-sensing headband market reached approximately USD 0.16 Billion in 2025 and is forecast to expand at an 18.4% CAGR through 2034. Demand is supported by BCI research programs, education technology interest, sleep-health purchases, and large consumer-electronics distribution. Chinese neurotechnology investment accelerated in early 2026, with brain-computer interface financing drawing attention from venture and industrial investors. Local manufacturers will pressure global brands on price, while premium research and clinical channels still value validated signal quality. China will likely become the largest Asia Pacific growth contributor by 2034.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Product Type

- Electroencephalography (EEG) Headbands

- Neurofeedback Headbands

- Sleep Monitoring Headbands

- Meditation and Mindfulness Headbands

- Fitness and Cognitive Performance Headbands

- Clinical Brain Monitoring Headbands

- Consumer Wellness Headbands

- Others

By Application

- Mental Health Monitoring

- Sleep Monitoring and Improvement

- Meditation and Stress Management

- Cognitive Training

- Neurorehabilitation

- Clinical Diagnosis and Research

- Sports Performance Optimization

- Brain-Computer Interface (BCI) Applications

- Others

By End-User

- Individual Consumers

- Hospitals and Clinics

- Research and Academic Institutes

- Neurology Centers

- Mental Health Centers

- Sports and Fitness Organizations

- Rehabilitation Centers

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.38 B |

| Forecast Revenue (2034) | USD 4.91 B |

| CAGR (2025-2034) | 15.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Electroencephalography (EEG) Headbands, Neurofeedback Headbands, Sleep Monitoring Headbands, Meditation and Mindfulness Headbands, Fitness and Cognitive Performance Headbands, Clinical Brain Monitoring Headbands, Consumer Wellness Headbands, Others), By Application, (Mental Health Monitoring, Sleep Monitoring and Improvement, Meditation and Stress Management, Cognitive Training, Neurorehabilitation, Clinical Diagnosis and Research, Sports Performance Optimization, Brain-Computer Interface (BCI) Applications, Others), By End-User, (Individual Consumers, Hospitals and Clinics, Research and Academic Institutes, Neurology Centers, Mental Health Centers, Sports and Fitness Organizations, Rehabilitation Centers, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MUSE BY INTERAXON INC., EMOTIV INC., NEURABLE INC., OPENBCI INC., ELEMIND TECHNOLOGIES, INC., ZETO, INC., NEUROELECTRICS CORPORATION, NATUS MEDICAL INCORPORATED, CERIBELL, INC., NAOX TECHNOLOGIES SAS, EPITEL, INC., FOREST DEVICES, INC., G.TEC MEDICAL ENGINEERING GMBH, BITBRAIN TECHNOLOGIES, BRAIN PRODUCTS GMBH, ANT NEURO B.V., MINDMAZE SA, NEUROSKY, INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Sleep Quality Monitoring, Meditation & Mindfulness, Cognitive Training, Neurological Diagnosis, Elite Sports Performance), By End-User (Hospitals & Clinics, Research Institutes, Personal Consumer Wellness) Industry Region & Key Players-Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Application (Sleep Quality Monitoring, Meditation & Mindfulness, Cognitive Training, Neurological Diagnosis, Elite Sports Performance), By End-User (Hospitals & Clinics, Research Institutes, Personal Consumer Wellness) Industry Region & Key Players-Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Application (Sleep Quality Monitoring, Meditation & Mindfulness, Cognitive Training, Neurological Diagnosis, Elite Sports Performance), By End-User (Hospitals & Clinics, Research Institutes, Personal Consumer Wellness) Industry Region & Key Players-Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Brainwave-Sensing Headband Market?

The Global Brainwave-Sensing Headband Market was valued at USD 1.20 Billion in 2024 and USD 1.38 Billion in 2025, and is projected to reach USD 4.91 Billion by 2034, growing at a CAGR of 15.1% from 2026 to 2034. Market growth is driven by wearable neurotechnology, EEG monitoring, and AI-powered mental wellness solutions.

Who are the major players in the Brainwave-Sensing Headband Market?

MUSE BY INTERAXON INC., EMOTIV INC., NEURABLE INC., OPENBCI INC., ELEMIND TECHNOLOGIES, INC., ZETO, INC., NEUROELECTRICS CORPORATION, NATUS MEDICAL INCORPORATED, CERIBELL, INC., NAOX TECHNOLOGIES SAS, EPITEL, INC., FOREST DEVICES, INC., G.TEC MEDICAL ENGINEERING GMBH, BITBRAIN TECHNOLOGIES, BRAIN PRODUCTS GMBH, ANT NEURO B.V., MINDMAZE SA, NEUROSKY, INC., Others

Which segments covered the Brainwave-Sensing Headband Market?

By Product Type, (Electroencephalography (EEG) Headbands, Neurofeedback Headbands, Sleep Monitoring Headbands, Meditation and Mindfulness Headbands, Fitness and Cognitive Performance Headbands, Clinical Brain Monitoring Headbands, Consumer Wellness Headbands, Others), By Application, (Mental Health Monitoring, Sleep Monitoring and Improvement, Meditation and Stress Management, Cognitive Training, Neurorehabilitation, Clinical Diagnosis and Research, Sports Performance Optimization, Brain-Computer Interface (BCI) Applications, Others), By End-User, (Individual Consumers, Hospitals and Clinics, Research and Academic Institutes, Neurology Centers, Mental Health Centers, Sports and Fitness Organizations, Rehabilitation Centers, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Brainwave-Sensing Headband Market

Published Date : 03 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date