- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Building Maintenance Services Market Size & Forecast | 8.3% CAGR

Global Building Maintenance Services Market Size, Share & Industry Analysis By Service Type (Landscaping, Interior Building Cleaning, Exterior Cleaning, Pest Control, HVAC Maintenance, Elevator Maintenance, Security Services), By Application (Residential, Commercial, Healthcare, Education, Hotels & Resorts), By End-User (Facility Management Companies, Property Owners, Government Organizations, Outsourced Providers), Regional Outlook, Competitive Landscape, Market Trends & Forecast 2025–2034

Report Overview

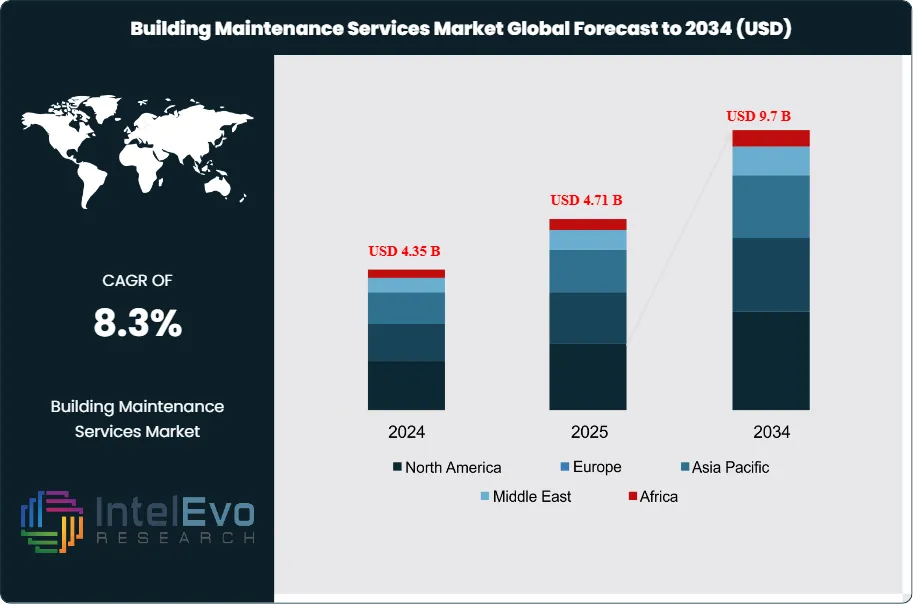

The Building Maintenance Services Market was valued at USD 4.35 Billion in 2024 and is projected to reach approximately USD 9.7 Billion by 2034. The market is estimated to grow to around USD 4.71 Billion in 2025. Based on projected expansion from 2026 onward, the industry is expected to register a compound annual growth rate (CAGR) of approximately 8.3% during 2026–2034.

Get More Information about this report -

Request Free Sample ReportBuilding maintenance services cover routine and corrective work that keeps assets safe, compliant, and efficient across commercial, residential, and institutional sites. Service scopes span janitorial and deep cleaning, minor repairs, HVAC servicing, electrical and plumbing work, landscaping, and pest control. Demand expands as owners move spending from reactive interventions to structured preventive programs that protect building uptime, support tenant satisfaction, and extend asset life. Aging infrastructure in mature cities and heavier utilization in mixed-use properties add steady service volume and shorten maintenance cycles.

Sustainability priorities now shape procurement and operating standards. Energy and emissions regulations, indoor-air requirements, and building-performance disclosure programs push portfolios toward mechanical optimization and auditable maintenance records. Buyers increasingly favor vendors that can document outcomes such as reduced energy intensity, fewer critical failures, and longer equipment run time between overhauls. On the supply side, the market remains fragmented, but consolidation continues as integrated facilities managers acquire local specialists to widen geographic coverage and add technical capabilities.

Digitalization is changing both economics and risk. CMMS platforms, connected sensors, and digital twins improve asset visibility and reduce unplanned downtime. AI-enabled scheduling and predictive analytics improve technician dispatch, parts planning, and preventive work sequencing, while automation in cleaning and inspection lifts productivity in airports, hospitals, and large office campuses. These advances support performance-based contracts, yet they also increase exposure to service-level penalties, cybersecurity incidents, and data-quality gaps. Wage inflation, skills shortages in HVAC and electrical trades, and contractor safety liabilities remain central cost and execution risks.

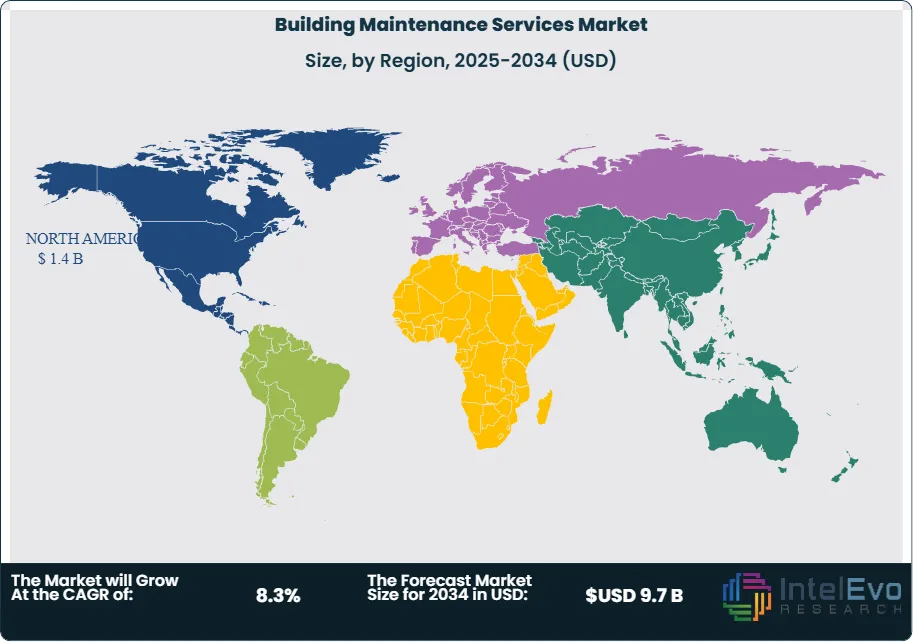

North America led in 2024, capturing more than 34% of revenue and generating about USD 1.4 billion, supported by high outsourcing penetration and strict safety compliance. Europe followed with an estimated 26% share, driven by retrofit cycles and efficiency mandates across public and commercial stock. Asia Pacific represented roughly 24% and delivers the fastest growth as urban development expands the installed base and raises compliance needs. Investment hotspots include U.S. Sun Belt metros, Western European retrofit corridors, and fast-growing Indian and Southeast Asian city clusters where premium commercial space and industrial parks are scaling quickly.

, By Application (Residential, Commercial, Healthcare, Education, Hotels & Resorts), By End-User (Facility Management Companies, Property Owners, Government Organizations, Outsourced Providers), Regional Outlook, Competitive Landscape, Market Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market expands from 4.35 billion USD, 2024 to 9.7 billion USD, 2034 and delivers 8.4% CAGR, 2024-2034. This trajectory reflects sustained demand scaling across core service lines at 9.7 billion USD, 2034.

- Segment Dominance: Interior Building Cleaning leads service mix with more than 22.0% share, 2024. This segment anchors recurring maintenance spend at 22.0% share, 2024.

- Segment Dominance: Commercial Buildings dominate end-use demand with more than 34.0% share, 2024. This concentration signals high contract density at 34.0% share, 2024.

- Driver: Facility Management Companies set the primary delivery model with more than 40.0% share, 2024. Scale-driven bundling and compliance execution accelerate adoption at 40.0% share, 2024.

- Restraint: The U.S. market grows at a slower 5.3% CAGR, 2024-2034 versus 8.4% CAGR, 2024-2034 globally. This gap indicates margin and expansion pressure in a mature base at 1.4 billion USD, 2024.

- Opportunity: Outsourced delivery remains the default with more than 41.0% share, 2024, creating room to upsell integrated and performance-linked contracts. Providers can capture incremental share through conversion programs at estimated: 2.0 percentage points, 2024-2034.

- Trend: Digital operations and automation expand use in service delivery to improve scheduling and quality control at estimated: 30.0% adoption, 2024. AI-enabled workflows increase utilization to estimate: 55.0% adoption, 2034.

- Regional Analysis: North America leads with more than 34.0% share, 2024 and records 1.4 billion USD revenue, 2024. The U.S. contributes 1.4 billion USD, 2024 and sustains 5.3% CAGR, 2024-2034.

By Type

Interior building cleaning remains the largest service category as the market moves into 2025, accounting for just over 22% of global revenue in 2024. You see this dominance across offices, healthcare facilities, education campuses, and residential complexes where hygiene standards directly influence occupancy rates, employee productivity, and regulatory compliance. High service frequency and contract-based delivery create steady recurring revenue, which keeps this segment structurally resilient even during economic slowdowns.

Outsourcing continues to reshape demand patterns. Organizations increasingly rely on third-party specialists rather than internal teams to control labor exposure and maintain consistent service quality. Industry surveys indicate that more than 60% of commercial properties globally outsource daily or weekly interior cleaning as of 2025. Adoption of automated scrubbers, sensor-based restroom monitoring, and low-chemical cleaning agents has reduced operating costs by an estimated 10–15% while meeting stricter indoor air quality and sanitation rules.

Regulatory pressure further supports long-term growth. Updated workplace safety and public health standards across North America and Europe now mandate documented cleaning protocols in offices, hospitals, and public buildings. These requirements increase contract durations and raise entry barriers, reinforcing the leading position of professional interior cleaning services.

By Application

Commercial buildings continue to represent the largest application segment, contributing more than 34% of total market revenue in 2024. You see stronger demand in office towers, retail centers, and mixed-use developments where maintenance complexity is higher and downtime carries financial risk. Large floor areas, high foot traffic, and complex mechanical systems drive consistent service requirements across cleaning, HVAC, and technical maintenance.

Compliance obligations intensify spending. Commercial properties face stricter fire safety, energy performance, and occupational health audits compared to residential buildings. As a result, annual maintenance budgets for commercial facilities are typically 25–40% higher per square meter than residential assets. Property owners prioritize preventive maintenance to protect asset value and reduce insurance exposure.

Sustainability programs also influence service selection. Energy-efficient HVAC servicing, water-saving cleaning practices, and waste reduction initiatives increasingly form part of maintenance contracts. By 2026, more than 45% of new commercial maintenance agreements are expected to include measurable energy or environmental performance targets.

By End-Use

Facility management companies remain the dominant end-user group, holding over 40% of market share in 2024. You benefit from their integrated service models that combine cleaning, technical maintenance, security, and compliance management under single contracts. This structure reduces coordination risk for property owners and improves service accountability.

Technology adoption strengthens their position. Building management systems, predictive maintenance software, and remote monitoring tools allow these companies to reduce equipment failures by an estimated 20–25%. Cost transparency and performance reporting appeal strongly to corporate clients and public institutions.

As buildings adopt smart controls and energy monitoring systems, reliance on specialized facility managers increases. This trend positions facility management companies to capture additional share through long-term contracts and multi-site portfolios beyond 2025.

By Region

North America leads the global market with more than 34% share and approximately USD 1.4 billion in revenue in 2024. You see strong demand supported by dense commercial infrastructure, high outsourcing penetration, and strict safety enforcement. The U.S. alone accounts for nearly the full regional total and is projected to expand at a 5.3% CAGR through 2034.

Europe follows with steady growth driven by retrofit activity and tightening energy performance rules. Asia Pacific shows the fastest expansion, supported by urban construction, rising commercial stock, and growing acceptance of outsourced maintenance. Markets such as India, China, and Southeast Asia are expected to post high single-digit growth as professional maintenance adoption accelerates.

Latin America and the Middle East and Africa remain smaller but attractive. Investments in hospitality, healthcare, and transport infrastructure are increasing service demand, particularly in the Gulf states and major urban centers. These regions present medium-term growth potential as regulatory frameworks and service standards mature.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Landscaping

- Interior Building Cleaning

- Pest Control

- Exterior Building Cleaning

- Street & Parking Lot Cleaning

- Maintenance

- Swimming Pool Cleaning

- HVAC Maintenance

- Elevator Maintenance

- Security Services

- Others

By Application

- Residential Building

- Commercial Building

- Hotels and Resorts

- Healthcare

- Education

- Others

By End-User

- Facility Management Companies

- Property Owners/Managers

- Government Organizations

- Outsourced Service Providers

- Others

By Service Provider

- In-House

- Outsourced

- Franchise

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.71 B |

| Forecast Revenue (2034) | USD 9.7 B |

| CAGR (2025-2034) | 8.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Landscaping, Interior Building Cleaning, Pest Control, Exterior Building Cleaning, Street & Parking Lot Cleaning, Maintenance, Swimming Pool Cleaning, HVAC Maintenance, Elevator Maintenance, Security Services, Others), By Application (Residential Building, Commercial Building, Hotels and Resorts, Healthcare, Education, Others), By End-User (Facility Management Companies, Property Owners/Managers, Government Organizations, Outsourced Service Providers, Others), By Service Provider (In-House, Outsourced, Franchise) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Power Climber, Zarafa Group Ltd, Heightsafe Systems Limited, Alimak Group, Sky Rider Equipment Inc, Akrobat Pte Ltd., Workplace Access Safety, FBA Gomyl, NSS Group, Jomy, Andrew Engineering, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Residential, Commercial, Healthcare, Education, Hotels & Resorts), By End-User (Facility Management Companies, Property Owners, Government Organizations, Outsourced Providers), Regional Outlook, Competitive Landscape, Market Trends & Forecast 2025–2034")

, By Application (Residential, Commercial, Healthcare, Education, Hotels & Resorts), By End-User (Facility Management Companies, Property Owners, Government Organizations, Outsourced Providers), Regional Outlook, Competitive Landscape, Market Trends & Forecast 2025–2034")

, By Application (Residential, Commercial, Healthcare, Education, Hotels & Resorts), By End-User (Facility Management Companies, Property Owners, Government Organizations, Outsourced Providers), Regional Outlook, Competitive Landscape, Market Trends & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Building Maintenance Services Market

Published Date : 02 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date