- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Bulk Material Handling System Market Size & Forecast 2034 | CAGR 4.7%

Global Bulk Material Handling System Market Size, Share, Analysis By Product (Conveyor Belts, Case Conveyors, Pallet Conveyors, Stackers, Reclaimers, Elevators), By Application (3PL, E-Commerce, General Merchandise, Food Retail, Food & Beverage, Manufacturing, Pharmaceutical/Healthcare), By Sales Channel (Manufacturers, Distributors) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Automation Trends & Forecast 2025–2034

Report Overview

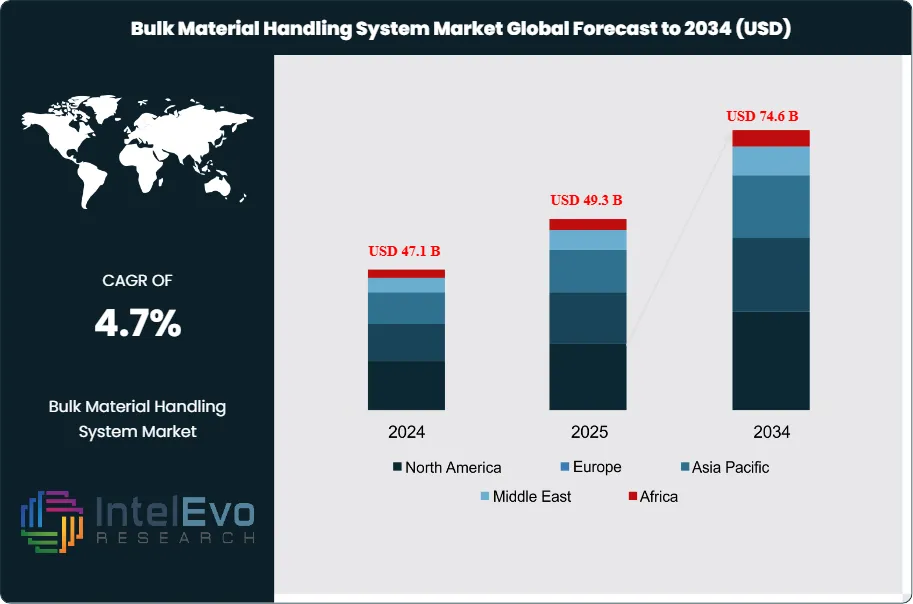

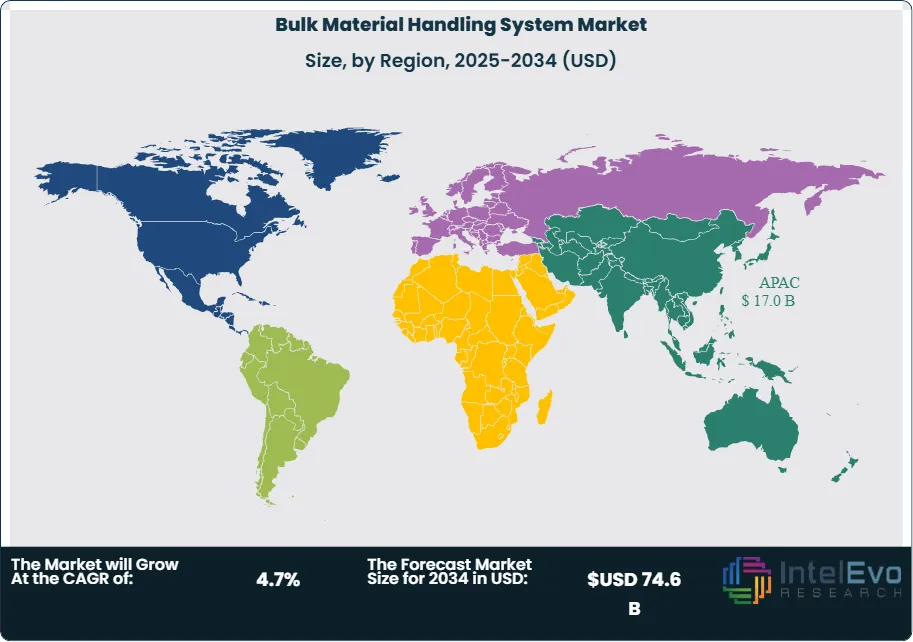

The Bulk Material Handling System Market was valued at approximately USD 47.1 billion in 2024 and is projected to reach nearly USD 74.6 billion by 2034, reflecting steady expansion across industrial, mining, construction, and manufacturing sectors. Based on the projected growth trajectory, the market size for 2025 is estimated at around USD 49.3 billion. Beginning in 2026, the market is expected to grow at a compound annual growth rate (CAGR) of about 4.7% from 2026 to 2034, ultimately reaching an estimated valuation of approximately USD 74.6 billion by 2034.

Get More Information about this report -

Request Free Sample ReportDemand concentrates in mining, ports and terminals, agriculture, construction, and power generation, where operators move high volumes of ores, coal, grains, aggregates, and other commodities. Systems integrate conveyors, stacker-reclaimers, ship loaders, cranes, feeders, and storage solutions into automated, continuous material flow networks.

Structural demand-side momentum remains strong. Rising global commodity trade, projected to add more than USD 350 billion in goods and services value in 2024, increases throughput requirements at mines, ports, and logistics hubs. High-capacity systems already account for an estimated 55% of new installations, as operators shift from labor-intensive handling toward continuous, enclosed, and higher-speed conveying. On the supply side, leading OEMs expand modular platforms and localized manufacturing to shorten lead times and address project-specific engineering requirements.

Technology reshapes competitive positioning. Automation-ready and digitally enabled systems represent roughly 35% of 2024 revenue and could exceed 50% by 2030. Vendors embed AI-based analytics for predictive maintenance, intelligent routing, and dynamic load optimization, which can reduce unplanned downtime by 15–25% and energy consumption by up to 10%. Digital twins and IIoT connectivity support real-time monitoring across dispersed assets, allowing operators to centralize control rooms and tighten integration with warehouse management and terminal operating systems.

Regulation and risk factors also influence capital allocation. Stricter safety codes and occupational health requirements push operators toward enclosed conveyors, dust suppression, and advanced collision-avoidance solutions. Energy-efficiency and emissions policies in Europe and parts of Asia encourage the adoption of variable-frequency drives and regenerative braking. At the same time, project pipelines face risks from commodity price volatility, permitting delays, and supply chain disruptions in critical components such as drives, bearings, and electronic controls, which can extend project timelines and pressure margins.

Regional dynamics shape the next wave of investment hotspots. Asia Pacific is expected to command about 40% of global revenue in 2024, supported by large-scale mining, port expansion, and industrial infrastructure in China, India, and Southeast Asia. North America and Europe together hold roughly 45%, underpinned by modernization of aging assets and automation upgrades. Emerging corridors in the Middle East, Africa, and Latin America, particularly in bulk terminals and greenfield mining projects, present attractive opportunities for differentiated, high-efficiency, and digitally integrated systems over the coming decade.

, By Application (3PL, E-Commerce, General Merchandise, Food Retail, Food & Beverage, Manufacturing, Pharmaceutical/Healthcare), By Sales Channel (Manufacturers, Distributors) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Automation Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The bulk material handling system market records a size of 47.1 billion USD, 2024 and is projected to reach 74.6 billion USD, 2034, reflecting a 4.7% CAGR, 2024-2034.

- Segment Dominance: Conveyor belts lead the product segment with a 34.8% revenue share, 2024, anchored in their efficiency for high-throughput material transport within the 47.1 billion USD market, 2024.

- Segment Dominance: Manufacturers dominate the sales channel with a 68.2% share, 2024, as industrial buyers prioritize direct procurement for large-scale systems within the 47.1 billion USD market, 2024.

- Driver: Rapid expansion of online retail acts as a core demand driver, with e-commerce applications contributing 21.2% of system demand, 2024 and supporting the market’s rise toward 74.6 billion USD, 2034.

- Restraint: High upfront investment and integration complexity constrain adoption, with estimated: 8.0 billion USD, 2024 in deferred or postponed projects across capital-intensive end-user industries and pressure on smaller buyers.

- Opportunity: Vendors capture a growing opportunity in value-added automation and lifecycle services, with estimated: 6.5 billion USD, 2034 in incremental revenue potential tied to upgrades of conveyor, warehousing, and port handling assets.

- Trend: The channel mix continues to favor direct and digital-first ordering, as manufacturers’ 68.2% share, 2024 evolves toward more integrated digital platforms targeting estimated: 72.0% channel share, 2034 for combined direct and online models.

- Regional Analysis: APAC stands out as the core regional demand hub with a 36.1% share of global revenue, 2024 and market value of 17.0 billion USD, 2024, with industrial and infrastructure projects positioning the region to reach estimated: 24.0 billion USD, 2034.

By Type

The market continues to shift toward high throughput material handling equipment in 2025 as demand from mining, manufacturing, and port operations increases. Stackers and stacker cum reclaimers remain central to large-volume storage yards. Their installed base expands steadily, particularly in iron ore and coal facilities, where operators prioritize consistent discharge rates and controlled material flow. Band conveyors account for a substantial share of new installations. They support continuous transport at lower operating costs, which positions them as a preferred option for facilities handling grains, aggregates, and packaged products.

Bucket wheel excavators and stripping shovels retain strong relevance in large mines. Their capacity to remove overburden at scale drives uptake in regions expanding open-pit operations. Rope shovels complement this segment by offering high mechanical reliability in harsh environments. Bucket elevators continue to gain traction in vertical transport applications across cement plants and industrial processing. Ship loaders and unloaders record rising adoption as port operators increase berth handling capacity to match growth in bulk commodity trade volumes. Industry assessments indicate that combined demand across these equipment types will expand at roughly 4.5 percent CAGR through 2034 as operators upgrade aging systems and automate material flow.

By Application

Mining remains the largest application area in 2025. Companies invest in higher-capacity machinery to support ore extraction and transport, particularly across Asia Pacific and Latin America. Construction firms expand their fleets of loaders, conveyors, and reclaiming equipment to meet rising demand for aggregates and raw materials. The packaging industry also increases adoption of automated conveying systems. It seeks to reduce manual handling and support faster throughput as order volumes rise.

Manufacturing facilities use stackers, elevators, and conveyors to support structured production flow and continuous processing. Sea ports and cargo terminals represent a fast-growing application. Operators upgrade ship loaders, unloaders, and yard conveyors to handle rising container and bulk cargo traffic. Market data suggests the ports segment will record some of the fastest growth from 2025 to 2034 as governments expand maritime infrastructure.

By End-Use

Residential construction drives consistent material flow needs, particularly in developing economies where new housing projects continue to scale. Bulk handling systems support the movement of cement, aggregates, and prefabricated materials within these sites. Commercial buildings create demand for mid-capacity equipment suited to large complexes, logistics hubs, and retail infrastructure. Operators prioritize equipment that supports predictable supply cycles and consistent site productivity.

Industrial buildings contribute the highest share of demand. These facilities rely on conveyors, elevators, and reclaiming equipment to maintain steady production lines across automotive, chemicals, metals processing, and food manufacturing. The expansion of high-volume industrial zones across Asia Pacific strengthens this segment’s long-term growth outlook.

By Region

North America records steady system upgrades in 2025 as companies replace legacy equipment to improve throughput and reliability. The United States remains the region’s anchor market due to its extensive mining, port, and industrial operations. Europe continues to prioritize automation and safety compliance. Demand rises in Germany, France, and the Nordic countries as operators integrate digital monitoring and energy-efficient conveying units into existing plants.

Asia Pacific holds the largest global share. China, India, and Japan remain the strongest contributors, supported by industrial expansion, major port developments, and large-volume mining operations. Latin America sees increased adoption of stackers and excavators in copper and iron ore mines. The Middle East and Africa show solid momentum. Large infrastructure projects, port expansions, and resource extraction activities position the region as an emerging growth center through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product

- Conveyor Belts

- Case Conveyors

- Pallet Conveyors

- Stackers

- Reclaimers

- Elevators

- Others

By Application

- 3PL

- E-commerce

- General Merchandise

- Food Retail

- Food & Beverage

- Manufacturing

- Pharmaceutical/Healthcare

By Sales Channel

- Manufacturers

- Distributors

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 49.3 B |

| Forecast Revenue (2034) | USD 74.6 B |

| CAGR (2025-2034) | 4.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product (Conveyor Belts, Case Conveyors, Pallet Conveyors, Stackers, Reclaimers, Elevators, Others), By Application (3PL, E-commerce, General Merchandise, Food Retail, Food & Beverage, Manufacturing, Pharmaceutical/Healthcare), By Sales Channel (Manufacturers, Distributors) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Beumer Group, TGW Logistics Group GmbH, Honeywell International Inc., Crown Equipment Corporation, Mitsubishi Electric Corporation, SSI Schaefer Group, Continental AG, Daifuku Co., Ltd., Jungheinrich AG, MHS Conveyor |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (3PL, E-Commerce, General Merchandise, Food Retail, Food & Beverage, Manufacturing, Pharmaceutical/Healthcare), By Sales Channel (Manufacturers, Distributors) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Automation Trends & Forecast 2025–2034")

, By Application (3PL, E-Commerce, General Merchandise, Food Retail, Food & Beverage, Manufacturing, Pharmaceutical/Healthcare), By Sales Channel (Manufacturers, Distributors) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Automation Trends & Forecast 2025–2034")

, By Application (3PL, E-Commerce, General Merchandise, Food Retail, Food & Beverage, Manufacturing, Pharmaceutical/Healthcare), By Sales Channel (Manufacturers, Distributors) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Automation Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Bulk Material Handling System Market?

Bulk Material Handling System Market was valued at USD 47.1 Billion in 2024 and is projected to reach USD 74.6 Billion by 2034, growing at a CAGR of 4.7%. Estimated at USD 49.3 Billion in 2025, driven by industrial automation, mining, and infrastructure demand.

Who are the major players in the Bulk Material Handling System Market?

Beumer Group, TGW Logistics Group GmbH, Honeywell International Inc., Crown Equipment Corporation, Mitsubishi Electric Corporation, SSI Schaefer Group, Continental AG, Daifuku Co., Ltd., Jungheinrich AG, MHS Conveyor

Which segments covered the Bulk Material Handling System Market?

By Product (Conveyor Belts, Case Conveyors, Pallet Conveyors, Stackers, Reclaimers, Elevators, Others), By Application (3PL, E-commerce, General Merchandise, Food Retail, Food & Beverage, Manufacturing, Pharmaceutical/Healthcare), By Sales Channel (Manufacturers, Distributors)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Bulk Material Handling System Market

Published Date : 27 Feb 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date