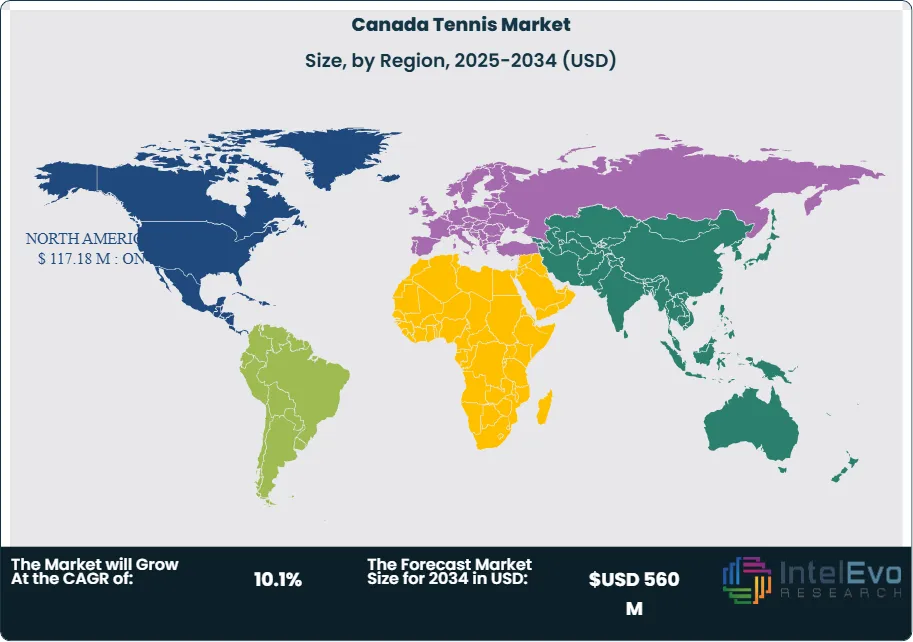

TheCanada Tennis Equipment Market is estimated at USD 215 million in 2025 and is on track to reach approximately USD 560 million by 2035, reflecting a strong CAGR of 10.1% over 2025–2035.Growth is driven by rising participation in racket sports, expanding tennis academies, and increasing demand for high-performance rackets, balls, and court accessories. The surge in youth training programs and celebrity-driven sports culture is further boosting equipment sales across Canada. With social media fitness trends, community sports investments, and the rise of pickleball crossover players fueling interest, the market is gaining strong momentum across retail, e-commerce, and sports facility segments.

While the market forms a niche segment within the broader sporting goods industry—accounting for under 0.3% of global share—it plays a critical role in racquet sports, contributing approximately 22–25% of the total segment that includes badminton, squash, and padel. Unlike categories such as football or basketball, tennis equipment demand is shaped less by major tournaments and more by community-level and recreational participation. Recent buyer trends confirm this shift, with Nielsen data indicating that 60% of new players now purchase their first racket from general retail rather than sports-specialist outlets.

The landscape continues to evolve on the supply side as well. Manufacturers have strategically repositioned inventory hubs closer to secondary cities to shorten fulfillment times. Contract manufacturing in Southeast Asia—particularly in Thailand and Vietnam—has largely stabilized post-2022. However, European distributors still report lead times 12–15% longer than pre-pandemic levels. These logistical dynamics are prompting a reconfiguration of sourcing and delivery models to meet steady consumer demand.

Product innovation remains a central growth driver. In January 2025, Babolat launched the Pure Drive Gen11, designed for competitive players emphasizing power and topspin. Featuring a reengineered frame for increased stability and a larger sweet spot, the Gen11 reflects a broader shift toward performance-enhancing design elements. This innovation aligns with rising demand for rackets that balance spin potential with control in high-speed play.

Regionally, North America and Europe lead the market in per capita expenditure, driven by long-standing tennis infrastructure, club culture, and consistent replacement cycles. These mature markets also benefit from established retail ecosystems and regular professional events. Asia Pacific shows strong participation growth through school initiatives and rising viewership of international tournaments, though average spending remains moderate. In contrast, Latin America and the Middle East & Africa lag in both adoption and spend, with demand largely confined to urban populations and channeled through digital platforms.

Looking ahead, the tennis equipment market is expected to grow steadily, supported by recreational demand, product updates, and expanding access in emerging regions.

Key Takeaways

Market Growth: The Canada tennis market is projected to grow at a CAGR of 10.1% between 2025 and 2035, supported by rising recreational participation, youth engagement through school programs, and expanding access to community courts.

Product Type: Tennis racquets remain the leading product segment, accounting for approximately 38% of total market revenue in 2024. Growth is driven by frequent replacement cycles among active players and increased demand for advanced frame technologies.

Distribution Channel: Online retail has gained significant traction, capturing nearly 34% of total sales in 2024. Consumers prioritize convenience and product variety, with platforms like TennisWarehouse.ca and Amazon seeing strong growth in order volume.

Driver: Participation growth among youth and casual players is driving equipment sales. According to Tennis Canada, active player registration rose by 11.3% in 2024, aided by public facility investments and national programs like “Let’s Play.”

Restraint: Seasonal limitations continue to constrain year-round market potential. With outdoor play restricted in colder months, indoor facility access remains uneven across provinces, limiting consistent player engagement.

Opportunity: Women's participation is growing steadily, creating a demand surge for gender-specific racquets, apparel, and accessories. Brands that tailor product lines for this demographic stand to benefit from rising interest across amateur and club-level circuits.

Trend: Smart racquets and sensor-enabled training tools are gaining popularity among performance-oriented players. Adoption of connected equipment rose by 22% year-over-year, with players seeking analytics-driven improvements in technique and match preparation.

Regional Analysis: Ontario and British Columbia account for over 60% of total tennis equipment sales in Canada, driven by population density, club access, and provincial-level investments in sports infrastructure. Alberta and Quebec show growth potential as urban participation increases.

Type Analysis

In 2025, apparel is expected to lead the tennis equipment market by product type, accounting for an estimated 32.5% share. Demand is growing steadily among both professionals and recreational players who prioritize performance, comfort, and durability. Moisture-wicking fabrics, supportive footwear, and UV-protective clothing are now standard expectations in tennis apparel. Brands such as Nike and Adidas continue to dominate this category with professional-grade collections widely used in major tournaments.

At the same time, players are showing increased interest in apparel that aligns with broader lifestyle and environmental values. Brands like Lacoste are expanding their eco-conscious product lines to meet demand from consumers who prioritize sustainable sourcing and low-impact materials. This dual focus on function and responsible design is reinforcing apparel’s dominant role in the tennis equipment value chain.

Sales Channel Analysis

Specialty sports and fitness stores remain the most influential sales channel in the tennis equipment market, projected to contribute 27.9% of total revenue in 2025. Retailers such as Dick’s Sporting Goods, Tennis Warehouse, and Sports Experts continue to attract consumers seeking hands-on shopping experiences. These stores offer a broad selection of racquets, footwear, strings, and accessories tailored to various skill levels.

Shoppers value in-store consultations and product testing options, particularly when selecting high-cost or performance-specific gear. Specialty outlets are also expanding their role as community hubs by offering demo days, racquet stringing services, and in-store events, helping to build brand loyalty and support local tennis engagement.

Application Analysis

Amateur players represent the largest application segment, projected to account for 61.1% of the Canadian tennis equipment market in 2025. Growth in this segment is being driven by increasing recreational participation, driven by school programs, public court investments, and grassroots initiatives. Entry-level equipment designed for ease of use and durability is gaining traction across age groups.

Companies like Wilson and Babolat are expanding their product portfolios with recreational-grade racquets, all-court shoes, and bundled starter kits. These offerings target casual players seeking functional, affordable gear without sacrificing quality. As access to tennis widens across community centers and private clubs, the amateur segment will remain central to equipment demand.

Regional Analysis

Regionally, North America continues to dominate the global tennis equipment market, supported by well-established retail infrastructure, organized club systems, and consistent tournament activity. The U.S. and Canada lead in per capita expenditure, driven by strong consumer interest and broad access to private and public playing facilities.

Asia Pacific shows the highest growth potential, driven by increasing participation rates in countries like China, Japan, and India. While average spend remains lower than in mature markets, rising awareness and access to global brands are expected to drive growth. Europe remains a stable market, with strong tennis culture in countries such as France, Germany, and the UK. Latin America and the Middle East & Africa continue to show lower adoption but offer localized growth in urban hubs.

By Product Type (Rackets , Tennis balls, strings, apparel, others), By Sales Channel (Direct sales, supermarkets & hypermarket, specialty sports & fitness stores, electronics & sports stores, , online retailers, , other sales channels), By Application (Professional usage, Amateur usage)

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

Tecnifibre, Wilson Sporting Goods Co., Adidas AG, Yonex Co., Ltd., Head Sports GmbH, Nike, Inc., Asics Corporation, Dunlop Sport, Babolat Vibration, Prince Global Sports LLC

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

1.1. MARKET SNAPSHOT

1.2. KEY FINDINGS & INSIGHTS

1.3. ANALYST RECOMMENDATIONS

1.4. FUTURE OUTLOOK

2. RESEARCH METHODOLOGY

2.1. MARKET DEFINITION & SCOPE

2.2. RESEARCH OBJECTIVES: PRIMARY & SECONDARY DATA SOURCES

2.3. DATA COLLECTION SOURCES

2.3.1. COVERAGE OF 100+ PRIMARY RESEARCH/CONSULTATION CALLS WITH INDUSTRY STAKEHOLDERS

FIGURE 17 CANADA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 18 CANADA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 19 CANADA TENNIS CURRENT AND FUTURE MARKET KEY COUNTRY LEVEL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 20 FINANCIAL OVERVIEW:

Key Player Analysis

Wilson Sporting Goods Co.: Wilson maintains its position as a market leader in the Canadian tennis equipment space, supported by a deep product portfolio that spans racquets, strings, balls, bags, and apparel. Its strong brand equity, built through decades of association with elite players and tournaments, continues to drive consumer trust and retailer preference. In 2025, Wilson remains a top choice for both amateur and competitive players across major provinces, with strong shelf presence in specialty retailers and online platforms.

The company has prioritized product innovation and athlete-led design. Its latest racquet series includes integrated frame vibration dampening and data compatibility with third-party sensors, aligning with growing demand for performance-enhancing gear. Wilson also invests in local partnerships with tennis academies and regional tournaments, ensuring direct engagement with Canada’s active player base. Its balanced pricing strategy across entry-level and premium categories enables the brand to capture market share across all skill levels.

Babolat Vibration: Babolat operates as a challenger brand in the Canadian tennis market, with a sharp focus on performance equipment and youth player development. Known for its racquet engineering and expertise in string technology, the brand appeals to intermediate and advanced users looking for precision and customization. Its flagship Pure Drive and Pure Aero racquet lines maintain strong sales traction in Canadian clubs and retail outlets.

Babolat continues to differentiate through digital integration. Its “Babolat Play” platform, which enables smart racquet connectivity and training data tracking, has gained popularity among junior athletes and performance coaches. In 2025, Babolat expanded its presence in Canada through new distribution partnerships and localized content marketing targeting tennis communities in Ontario and British Columbia. This regional strategy supports brand awareness and aligns with its growth goals in North America.

Head Sports GmbH: Head positions itself as a technology-forward brand in Canada’s mid- to premium-tier tennis segment. Its portfolio includes racquets, strings, footwear, and accessories, with consistent updates driven by athlete feedback and R&D. The Radical and Speed racquet series remain core to its Canadian performance line, favored by competitive juniors and seasoned club players.

In 2025, Head enhanced its Canadian retail visibility by launching exclusive product drops through national sports chains and direct-to-consumer platforms. The company also emphasizes sustainability, using recycled materials in packaging and product construction. With a focus on material science and ergonomic design, Head targets players seeking control and comfort without compromising power.

Prince Global Sports: Prince functions as a niche player in Canada, maintaining a loyal base among long-time enthusiasts and select competitive segments. While its mainstream market share has narrowed over the past decade, Prince has preserved relevance through legacy racquet models and consistent product quality. Its classic frame designs appeal to a subset of players who favor control-heavy equipment with traditional feel.

Strategically, Prince has shifted focus toward digital retail and limited-edition releases to capitalize on brand nostalgia. It has also expanded distribution via Canadian e-commerce platforms and independent pro shops. Though not dominant in volume, Prince holds competitive positioning in specific market pockets, particularly among experienced adult players and those with long-standing brand affinity.

Market Key Players

Tecnifibre

Wilson Sporting Goods Co.

Adidas AG

Yonex Co., Ltd.

Head Sports GmbH

Nike, Inc.

Asics Corporation

Dunlop Sport

Babolat Vibration

Prince Global Sports LLC

Driver:

National Programs Boost Grassroots Tennis Participation Across Canada

As of 2025, recreational participation is the primary force behind growth in the Canadian tennis market. National programs such as Tennis Canada's “Let’s Play” initiative and municipal investments in public courts have increased access across age groups. Youth registration alone grew by 11.3% in 2024, with a notable rise in school-based tennis activity and community club engagement.

Growing Recreational Play Drives Demand for Entry-Level Gear & Facilities

This grassroots momentum is translating into stronger demand for entry-level equipment, apparel, and facility usage. The expansion of casual tennis as a year-round fitness activity also creates new product replacement cycles, especially for racquets, footwear, and training aids. For brands and retailers, this shift presents sustained growth potential beyond the professional segment.

Restraint:

Seasonal Weather Limits Court Availability and Player Retention

Seasonal limitations continue to restrict consistent growth in Canada’s tennis market. Outdoor court usage drops significantly between November and March, especially in provinces with limited access to heated or covered facilities. This climate-related challenge compresses the annual playing window and disrupts customer retention.

The shortage of indoor courts also limits program scalability. While demand is growing, particularly in urban centers, infrastructure expansion has not kept pace. This gap restricts year-round player development and suppresses off-season equipment sales, reducing revenue consistency for retailers and manufacturers.

Opportunity:

Rising Women’s Participation Creates a High-Growth Consumer Segment

Women’s participation is emerging as a high-growth segment in Canada’s tennis market. Increased visibility of female athletes and greater gender equity in sports programming have encouraged more women to take up the game, both recreationally and competitively. Equipment makers are responding with gender-specific product lines that include lighter racquets, tailored footwear, and performance apparel.

Gender-Focused Products and Inclusive Retail Strategies Drive Market Expansion

Retailers offering inclusive sizing, design variety, and targeted marketing stand to capture a growing share of this demographic. With female participation expected to rise at a CAGR of over 6% through 2030, companies positioned to meet the distinct needs of this customer group can build brand loyalty and expand their market footprint.

Trend:

Smart Gear and Performance Tech Transform Canadian Tennis Training

Technology adoption is reshaping how Canadian tennis players train and shop. Smart racquets, wearable sensors, and mobile coaching apps are gaining traction, particularly among younger players and competitive amateurs. In 2025, sensor-enabled gear saw a 22% increase in adoption, driven by the demand for data-backed performance insights.

E-commerce platforms are also integrating virtual fitting tools and AI-assisted recommendations, improving the online shopping experience for tennis equipment. This digital shift is creating new entry points for brands and reshaping how players engage with training tools, performance metrics, and product selection.

Recent Developments

Dec 2024 – Wilson Sporting Goods Co.: Wilson launched the Blade V9 racquet line in Canada, featuring a refined frame geometry and new string mapping for enhanced ball pocketing. The release targets intermediate and competitive players, with projected Q1 sales expected to account for 18% of Wilson’s racquet revenue in Canada. This launch strengthens Wilson’s leadership in the mid-to-premium performance segment.

Feb 2025 – Babolat: Babolat expanded its retail presence through a new distribution agreement with Sport Chek, adding over 150 stores to its Canadian retail footprint. The agreement includes in-store displays and exclusive colorways for the Pure Aero and Pure Drive lines. This move significantly increases brand accessibility in high-traffic suburban and metropolitan areas.

Apr 2025 – Tennis Canada x Head Sports GmbH: Head entered a multi-year partnership with Tennis Canada to become the official equipment partner for junior development programs. The agreement includes product supply, athlete sponsorships, and co-branded promotional campaigns. This partnership positions Head to grow market share among emerging players and gain visibility at the grassroots level.

Jul 2025 – Prince Global Sports: Prince re-entered select Canadian specialty retailers with a limited-release reissue of its Graphite Classic racquet, targeting long-time enthusiasts and veteran players. The collection sold out in under three weeks, with 70% of sales coming through pro shops and independent stores. The release supports Prince’s brand revival strategy focused on legacy models and niche segments.

Sep 2025 – Nike Canada: Nike announced the launch of its Canada-exclusive tennis apparel line designed for climate adaptability and local court conditions. The line features temperature-regulating fabrics tailored for Canada’s variable outdoor playing season. This strategic product localization enhances Nike’s positioning in premium performance wear tailored to regional conditions.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

-Size-by-Region.png.png)

, By Sales Channel (Direct sales, supermarkets & hypermarket, specialty sports & fitness stores, electronics & sports stores, , online retailers, , other sales channels), By Application (Professional usage, Amateur usage) Industry Outlook, Market Dynamics, Competitive Landscape, Trends & Forecast 2025–2034")

, By Sales Channel (Direct sales, supermarkets & hypermarket, specialty sports & fitness stores, electronics & sports stores, , online retailers, , other sales channels), By Application (Professional usage, Amateur usage) Industry Outlook, Market Dynamics, Competitive Landscape, Trends & Forecast 2025–2034")

, By Sales Channel (Direct sales, supermarkets & hypermarket, specialty sports & fitness stores, electronics & sports stores, , online retailers, , other sales channels), By Application (Professional usage, Amateur usage) Industry Outlook, Market Dynamics, Competitive Landscape, Trends & Forecast 2025–2034")

, By Sales Channel (Direct sales, supermarkets & hypermarket, specialty sports & fitness stores, electronics & sports stores, , online retailers, , other sales channels), By Application (Professional usage, Amateur usage) Industry Outlook, Market Dynamics, Competitive Landscape, Trends & Forecast 2025–2034")