- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Caprolactone Market to Hit USD 2.56 Bn by 2034 | CAGR 7.6%

Global Caprolactone Market Size, Share, Analysis Report By Type (PCL, Copolymers, Oligomers), Application (Medical Devices, Drug Delivery, Adhesives & Sealants, Coatings, Elastomers, Packaging, Construction), End-Use Industry (Healthcare & Medical, Automotive & Transportation, Packaging, Construction, Consumer Goods, Electronics) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034

Report Overview

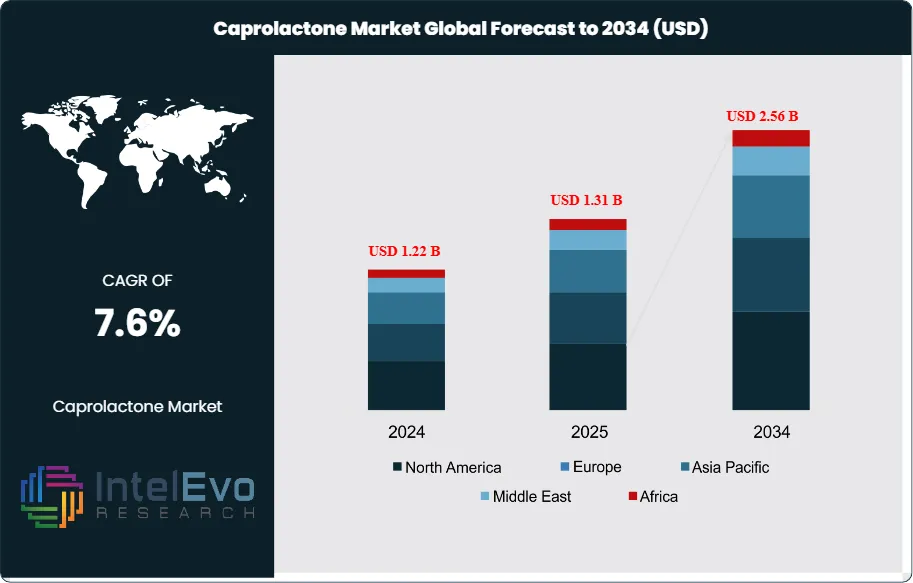

The Caprolactone Market size is projected to reach approximately USD 2.56 Billion by 2034, up from USD 1.22 Billion in 2024, growing at a healthy CAGR of 7.6% during the forecast period from 2025 to 2034. This growth is driven by increasing demand for high-performance polymers, biodegradable materials, and specialty coatings across automotive, electronics, and healthcare industries. As industries shift toward sustainability and lightweight materials, caprolactone is emerging as a key ingredient in advanced composites and bio-based polyurethanes. The market’s upward trajectory reflects its expanding applications in modern manufacturing, medical devices, and 3D printing — making it one of the most dynamic chemical segments of the decade.

Get More Information about this report -

Request Free Sample ReportCaprolactone is a highly versatile cyclic ester, most notably used as the primary monomer in the synthesis of polycaprolactone (PCL)—a biodegradable polyester. PCL’s unique combination of properties, such as flexibility, low melting point, and compatibility with a wide range of other polymers, makes it a sought-after material in numerous industries. The versatility of caprolactone extends its reach into adhesives, coatings, elastomers, biomedical devices, and specialty polymers, where it imparts critical performance characteristics like biodegradability, low toxicity, and processability. The expansion of the caprolactone market is fundamentally driven by the global shift toward sustainable and biodegradable materials. As environmental concerns and regulatory pressures mount, industries are increasingly seeking alternatives to conventional, non-degradable plastics. Caprolactone-based polymers, especially PCL, offer a compelling solution: they are not only biodegradable but also possess mechanical and chemical properties that rival or surpass traditional plastics. This makes them especially attractive in packaging, where single-use plastics are under scrutiny, and in medical and consumer goods, where safety and environmental impact are paramount. The integration of caprolactone in high-performance adhesives and elastomers is another growth vector. These materials are valued for their superior flexibility, resilience, and processability, which are essential in automotive, construction, and electronics applications. As manufacturers seek to improve product performance while meeting sustainability goals, caprolactone’s unique properties make it a material of choice.

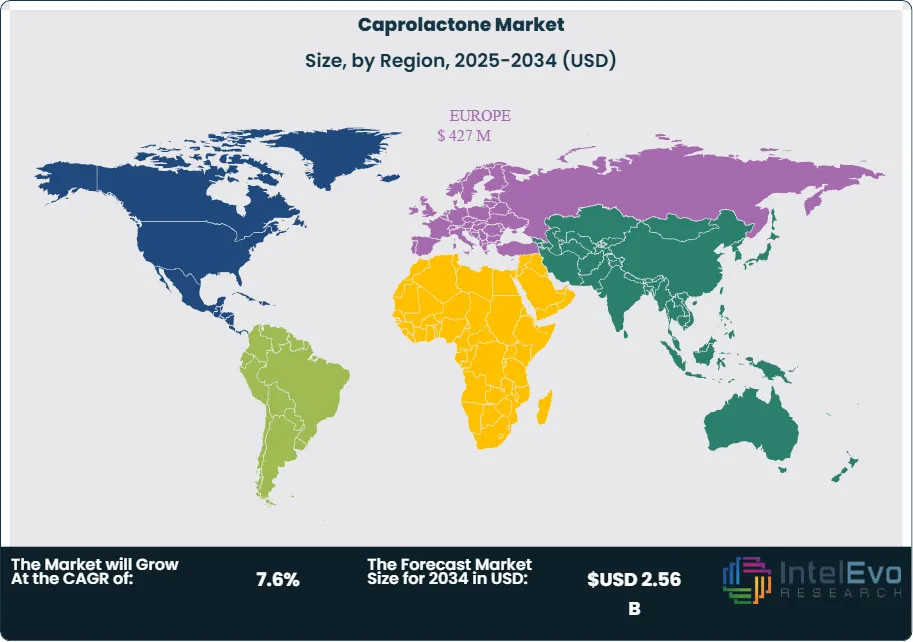

Europe is the clear market leader, propelled by stringent environmental regulations, a robust healthcare sector, and a strong commitment to sustainable materials. The region’s advanced R&D infrastructure and the presence of major chemical companies foster innovation in caprolactone-based technologies. European manufacturers are at the forefront of developing medical-grade PCL and specialty polymers for high-value applications. Asia-Pacific is the fastest-growing region, with countries like China, Japan, South Korea, and India investing heavily in green chemistry, healthcare infrastructure, and advanced manufacturing. Rapid industrialization and urbanization are driving demand for sustainable materials in packaging, automotive, and construction. The region’s expanding healthcare sector is also a major consumer of caprolactone-based biomedical devices and drug delivery systems.North America maintains a significant share of the market, supported by advanced manufacturing capabilities, a strong biomedical research ecosystem, and regulatory incentives for biodegradable materials. The U.S. and Canada are key markets for medical devices, specialty polymers, and sustainable packaging solutions.

The COVID-19 pandemic had a notable impact on the caprolactone market. The surge in demand for medical devices, personal protective equipment, and safe packaging highlighted the value of caprolactone-based polymers, which are both biocompatible and biodegradable. The pandemic also accelerated digital transformation and innovation in supply chains, prompting companies to invest in resilient, sustainable materials. Geopolitical factors—including trade policies, raw material supply chain dynamics, and evolving environmental standards—continue to influence market strategies. For example, fluctuations in the availability and price of raw materials (such as cyclohexanone, a precursor for caprolactone) can impact production costs and supply stability. Additionally, stricter environmental regulations and the global push for circular economy practices are encouraging investment in bio-based and renewable caprolactone production methods.

, Application (Medical Devices, Drug Delivery, Adhesives & Sealants, Coatings, Elastomers, Packaging, Construction), End-Use Industry (Healthcare & Medical, Automotive & Transportation, Packaging, Construction, Consumer Goods, Electronics) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Key Takeaways

- Market Growth: The Caprolactone Market is expected to reach USD 2.56 Billion by 2034, driven by demand for biodegradable polymers, medical devices, and high-performance specialty materials.

- Type Dominance: Polycaprolactone (PCL) dominates as the primary derivative, widely used in biodegradable plastics, medical implants, and specialty adhesives.

- Application Dominance: The medical and healthcare sector leads due to the use of caprolactone-based polymers in drug delivery, sutures, and tissue engineering.

- Drivers: Key drivers include sustainability mandates, advances in polymer science, and the need for high-performance, eco-friendly materials.

- Restraints: Market growth is hindered by high production costs, limited raw material availability, and technical challenges in large-scale synthesis.

- Opportunities: The market is positioned for expansion through innovations in biomedical applications, smart packaging, and green construction materials.

- Trends: Notable trends include the shift toward bio-based caprolactone, integration in 3D printing, and development of functionalized copolymers.

- Regional Analysis: Europe leads with over 35% market share due to regulatory support and innovation, while Asia-Pacific shows the highest growth potential.

Type Analysis

Polycaprolactone (PCL) Leads With Over 60% Market Share, Polycaprolactone (PCL) is the dominant type in the global caprolactone market, accounting for more than 60% of total consumption. PCL is a biodegradable, semi-crystalline polyester synthesized by the ring-opening polymerization of caprolactone. PCL’s versatility makes it the material of choice for a variety of high-value applications, especially in the medical field (e.g., sutures, drug delivery systems, tissue scaffolds) and in the development of biodegradable packaging. Beyond PCL, the market is seeing growth in copolymers and functionalized derivatives of caprolactone, which are engineered to provide specific mechanical, thermal, or chemical properties. These advanced materials are increasingly used in adhesives, coatings, elastomers, and specialty industrial products. The “Others” category includes specialty oligomers and blends, which are typically used in niche research or industrial applications where unique performance characteristics are required.

Application Analysis

Medical and Healthcare Applications Dominate, The medical and healthcare sector is the largest application segment for caprolactone-based polymers, reflecting the material’s unique combination of biocompatibility, biodegradability, and processability. Following healthcare, the adhesives and coatings segment is a major consumer of caprolactone. Here, caprolactone imparts flexibility, chemical resistance, and durability to adhesives, sealants, and specialty coatings used in demanding environments such as automotive, construction, and electronics. In the construction and automotive industries, caprolactone-based materials are valued for their performance in high-stress applications. They are used in high-performance sealants, elastomers, and specialty coatings that require a balance of flexibility, strength, and environmental resistance. Packaging is an emerging and rapidly growing application area. Caprolactone-based bioplastics offer a sustainable alternative to conventional plastics, providing the necessary mechanical properties for packaging while being fully biodegradable. This is particularly important as regulatory and consumer pressure mounts to reduce plastic waste and promote circular economy solutions.

Regional Analysis

Europe Leads With Over 35% Market Share in Caprolactone Market, Europe maintains market leadership due to its advanced regulatory environment, strong R&D ecosystem, and early adoption of sustainable materials in healthcare and packaging. The region’s focus on circular economy initiatives and green chemistry drives innovation and market expansion. Asia-Pacific is the fastest-growing region, propelled by rapid industrialization, expanding healthcare infrastructure, and increasing investments in sustainable manufacturing. North America holds a significant share, supported by biomedical research, advanced manufacturing, and regulatory incentives for biodegradable materials. Latin America and Middle East & Africa are emerging markets, benefiting from infrastructure development and growing demand for eco-friendly materials.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

Type

- Polycaprolactone (PCL)

- Copolymers

- Oligomers

- Others

Application:

- Medical Devices

- Drug Delivery

- Adhesives & Sealants

- Coatings

- Elastomers

- Packaging

- Construction

- Others

End-Use Industry:

- Healthcare & Medical

- Automotive & Transportation

- Packaging

- Construction

- Consumer Goods

- Electronics

- Others

Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.31 B |

| Forecast Revenue (2034) | USD 2.56 B |

| CAGR (2025-2034) | 7.6% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Type (Polycaprolactone (PCL), Copolymers, Oligomers, Others), Application (Medical Devices, Drug Delivery, Adhesives & Sealants, Coatings, Elastomers, Packaging, Construction, Others), End-Use Industry (Healthcare & Medical, Automotive & Transportation, Packaging, Construction, Consumer Goods, Electronics, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Perstorp Holding AB, BASF SE, Daicel Corporation, Merck KGaA, Solvay S.A., Ingevity Corporation, Shenzhen Prechem New Material Co., Ltd., Sigma-Aldrich Corporation, Santa Cruz Biotechnology, Inc., Alfa Aesar, Tokyo Chemical Industry Co., Ltd., TCI Chemicals (India) Pvt. Ltd., VWR International, LLC, Acros Organics, Oxea GmbH, Eastman Chemical Company, Ashland Global Holdings Inc., Evonik Industries AG, Arkema Group, Croda International Plc, Huntsman Corporation, Ube Industries, Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Application (Medical Devices, Drug Delivery, Adhesives & Sealants, Coatings, Elastomers, Packaging, Construction), End-Use Industry (Healthcare & Medical, Automotive & Transportation, Packaging, Construction, Consumer Goods, Electronics) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

, Application (Medical Devices, Drug Delivery, Adhesives & Sealants, Coatings, Elastomers, Packaging, Construction), End-Use Industry (Healthcare & Medical, Automotive & Transportation, Packaging, Construction, Consumer Goods, Electronics) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

, Application (Medical Devices, Drug Delivery, Adhesives & Sealants, Coatings, Elastomers, Packaging, Construction), End-Use Industry (Healthcare & Medical, Automotive & Transportation, Packaging, Construction, Consumer Goods, Electronics) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date