- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global CAR-T Cell Therapy Market Size, Share & Forecast | CAGR 16.1%

Global CAR-T Cell Therapy Market Size, Share, Growth Analysis By Therapy Type (Autologous, Allogeneic), By Target Antigen (CD19, BCMA, CD20, CD22), By Indication (ALL, DLBCL, Multiple Myeloma, CLL), By Manufacturing Model (Centralized, Decentralized Point-of-Care, Hybrid) Industry Regional Outlook, Key Players – Market Dynamics, Competitive Landscape, Oncology & Cell Therapy Industry Trends, Investment Analysis & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 6.30 Billion | USD 24.20 Billion | 16.1% | North America, 47.0% |

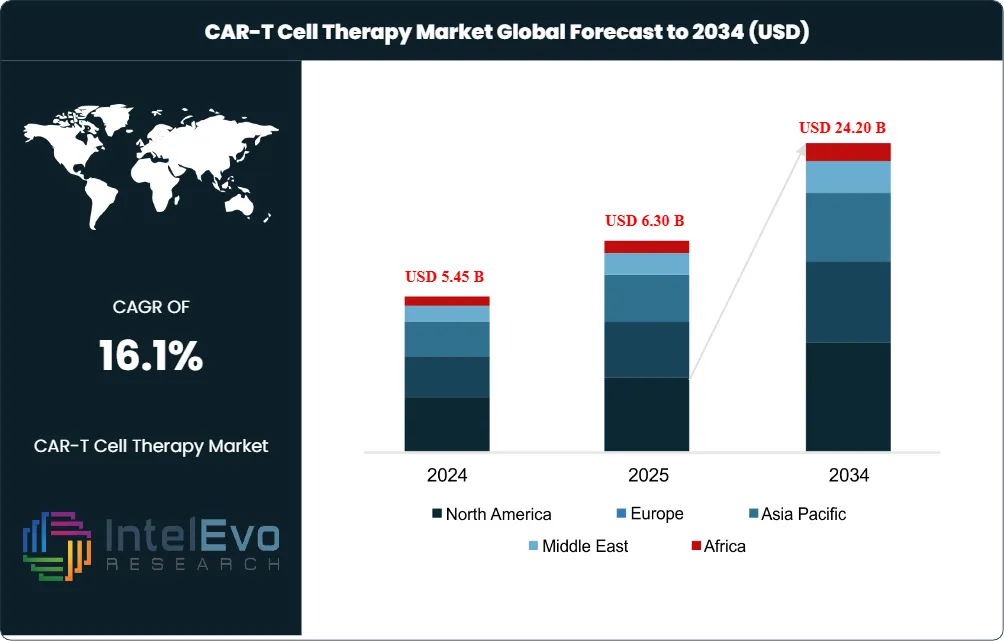

The CAR-T Cell Therapy Market was valued at USD 5.45 Billion in 2024 and is estimated to reach USD 6.30 Billion in 2025. The market is projected to reach USD 24.20 Billion by 2034, expanding at a CAGR of 16.1% during the forecast period (2026–2034). This represents an absolute dollar opportunity of USD 17.90 Billion over the analysis period, driven by earlier-line use in multiple myeloma, broader lymphoma labels, and manufacturing capacity built by Gilead Sciences, Johnson & Johnson, Bristol Myers Squibb, Novartis, and Autolus Therapeutics.

Get More Information about this report -

Request Free Sample ReportThe CAR-T cell therapy market entered 2026 with a wider regulatory base than in 2024. The U.S. Food and Drug Administration lists Kymriah, Yescarta, Tecartus, Breyanzi, Abecma, Carvykti, and Aucatzyl among licensed CAR-T products, while European Medicines Agency and Japan MHLW approvals support commercial supply in Europe and Japan. FDA elimination of REMS requirements for BCMA- and CD19-directed autologous CAR-T products in June 2025 reduced site certification friction because safety communication moved into labeling and medication guides.

Commercial demand is concentrated in hematologic malignancies, not broad oncology. Johnson & Johnson reported Carvykti as a fast-rising multiple myeloma franchise in 2025, while Gilead disclosed USD 1.8 Billion in 2025 cell therapy product sales from Yescarta and Tecartus. Bristol Myers Squibb widened Breyanzi use to marginal zone lymphoma in December 2025, making label breadth a primary commercial weapon against older CD19 products.

The CAR-T cell therapy market also shifted toward in vivo and autoimmune programs during the trailing 12 months. AbbVie agreed to acquire Capstan Therapeutics for up to USD 2.10 Billion in June 2025, Gilead unit Kite Pharma agreed to buy Interius BioTherapeutics for USD 350 Million in August 2025, Eli Lilly agreed to acquire Orna Therapeutics for up to USD 2.40 Billion in February 2026, and Lilly followed with a Kelonia Therapeutics deal valued up to USD 7.00 Billion in April 2026. These transactions show that investors are pricing the next growth wave around bypassing ex vivo manufacturing rather than only adding new cancer targets.

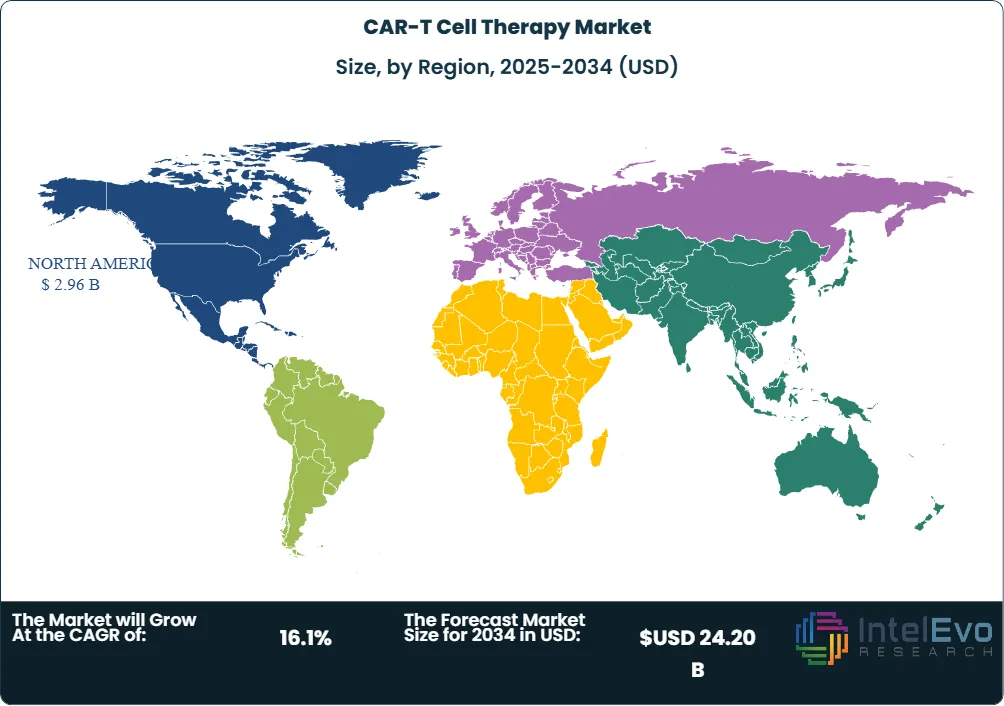

North America held 47.0% of 2025 revenue because the United States combines FDA product approvals, CMS hospital payment infrastructure, National Cancer Institute centers, and commercial launch scale. Asia Pacific is forecast to post the fastest CAGR through 2034, supported by China NMPA approvals for domestic CAR-T products, Japan public reimbursement, and expanding cell-processing capacity in South Korea and Singapore. By 2034, the field should remain autologous in commercial revenue, but in vivo CAR-T could reset pricing, capacity, and treatment-site economics if Phase 1 and Phase 2 safety data hold.

Market Definition & Scope

The CAR-T cell therapy market is defined as commercial activity around chimeric antigen receptor T-cell medicines that genetically modify T lymphocytes to recognize cancer or immune-disease antigens. The market encompasses autologous CAR-T products such as Yescarta, Tecartus, Breyanzi, Abecma, Carvykti, Kymriah, and Aucatzyl; allogeneic investigational programs; viral-vector manufacturing; cell processing; cryopreservation; treatment-center services; and future in vivo CAR-T platforms using lentiviral or lipid nanoparticle delivery.

This analysis includes approved therapies, late-stage pipeline assets, product revenue, manufacturing services linked to CAR-T production, and treatment-center commercialization across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. It excludes tumor-infiltrating lymphocyte therapies such as Amtagvi, T-cell engagers, TCR-T products, NK-cell therapies, and broad gene-therapy manufacturing not tied to CAR-T programs. Within the broader cell and gene therapy category, CAR-T cell therapy represented approximately one-third of commercial therapy revenue in 2025.

, By Target Antigen (CD19, BCMA, CD20, CD22), By Indication (ALL, DLBCL, Multiple Myeloma, CLL), By Manufacturing Model (Centralized, Decentralized Point-of-Care, Hybrid) Industry Regional Outlook, Key Players – Market Dynamics, Competitive Landscape, Oncology & Cell Therapy Industry Trends, Investment Analysis & Forecast 2026-2034")

Key Takeaways

- Market Growth: The CAR-T cell therapy market grew from USD 6.30 Billion in 2025 toward a projected USD 24.20 Billion by 2034 at a 16.1% CAGR, adding USD 17.90 Billion in forecast-period revenue.

- Segment Dominance: Autologous CAR-T therapy led by therapy type with 88.0% share in 2025 because every major commercial product remains patient-specific and ex vivo manufactured.

- Segment Dominance: Hematologic malignancies held 96.0% application share in 2025, with multiple myeloma and B-cell lymphoma accounting for most paid infusions.

- Driver: Earlier-line multiple myeloma expansion is the leading growth driver because Carvykti and Abecma moved into less heavily pretreated patients in 2024 and broadened eligible U.S. demand.

- Restraint: Manufacturing complexity remains the main constraint because vein-to-vein timelines often span weeks and product list prices commonly exceed USD 400,000 per infusion in the United States.

- Opportunity: In vivo CAR-T programs represent the largest technology opportunity, with more than USD 11.85 Billion in announced acquisition value from Kelonia, Orna, Capstan, and Interius during the trailing 12 months.

- Trend: Regulatory burden eased in June 2025 when FDA removed REMS requirements for approved BCMA- and CD19-directed autologous CAR-T immunotherapies.

- Regional: North America led with 47.0% market share in 2025, equivalent to USD 2.96 Billion, because U.S. centers capture most commercial CAR-T infusion volume.

Key Insights Summary

- FDA listed seven U.S. CAR-T cell therapy brands as licensed cellular and gene therapy products in April 2026, covering CD19 and BCMA targets across leukemia, lymphoma, and multiple myeloma.

- Gilead Sciences disclosed USD 1.8 Billion in full-year 2025 cell therapy sales, with Yescarta at USD 1.5 Billion and Tecartus at USD 344 Million after competitive pressure in lymphoma and mantle-cell indications.

- Novartis reported Kymriah sales of USD 85 Million in Q4 2025, down 21.0% year over year, illustrating the revenue compression faced by first-wave CD19 CAR-T products.

- FDA removed REMS requirements for approved autologous BCMA- and CD19-directed CAR-T products in June 2025, affecting Abecma, Breyanzi, Carvykti, Kymriah, Tecartus, and Yescarta.

- Bristol Myers Squibb received FDA approval for Breyanzi in relapsed or refractory marginal zone lymphoma on December 4, 2025, after at least two prior systemic therapies.

- Eli Lilly committed up to USD 7.00 Billion for Kelonia Therapeutics in April 2026, including USD 3.25 Billion upfront, to access a Phase 1 in vivo CAR-T program for multiple myeloma.

- EMA safety review data reported 38 secondary T-cell malignancy cases among approximately 42,500 treated CAR-T patients in 2024, which led Europe to require written label warnings and lifelong monitoring.

Competitive Landscape Overview

The CAR-T cell therapy market is moderately consolidated, with Gilead Sciences/Kite Pharma, Johnson & Johnson/Janssen with Legend Biotech, Bristol Myers Squibb, and Novartis accounting for an estimated 78.0% of commercial product revenue in 2025. Competition is organized around antigen targets, label breadth, hospital network depth, manufacturing reliability, and post-infusion safety support. Carvykti is gaining share in multiple myeloma, while Yescarta remains a core lymphoma product despite lower 2025 revenue.

Competitive intensity is moving from first-generation CD19 lymphoma therapy toward BCMA myeloma, outpatient delivery, and in vivo cell engineering. Gilead’s February 2026 Arcellx agreement and Lilly’s April 2026 Kelonia agreement indicate that strategic buyers now value platform control and speed-to-patient as highly as current product sales. Smaller companies compete through target specialization, split-dose kinetics, or regional manufacturing access rather than global commercial reach.

Competitive Landscape Matrix

| Company Name | Headquarters | Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Gilead Sciences / Kite Pharma | United States | Leader | Yescarta, Tecartus, anito-cel collaboration | United States, Europe, Japan | Agreed to acquire Arcellx for up to USD 7.80 Billion in February 2026 |

| Johnson & Johnson / Janssen with Legend Biotech | United States / China | Leader | Carvykti | United States, Europe, Japan | Reported Carvykti expansion in earlier-line multiple myeloma through 2025 |

| Bristol Myers Squibb | United States | Leader | Breyanzi, Abecma | United States, Europe | Received FDA approval for Breyanzi in marginal zone lymphoma in December 2025 |

| Novartis AG | Switzerland | Leader | Kymriah, T-Charge platform | Europe, United States, Japan | Reported Kymriah pressure in 2025 while maintaining CAR-T platform investment |

| Autolus Therapeutics | United Kingdom | Challenger | Aucatzyl | United States, United Kingdom | Commercialized Aucatzyl after November 2024 FDA approval and expanded treatment-center authorization in 2025 |

| JW Therapeutics | China | Challenger | Carteyva | China, Macao | Secured Macao approval for Carteyva in June 2025 |

| AbbVie Inc. | United States | Challenger | Capstan in vivo CAR-T platform | United States | Agreed to buy Capstan Therapeutics for up to USD 2.10 Billion in June 2025 |

| Eli Lilly and Company | United States | Challenger | Orna and Kelonia in vivo CAR-T platforms | United States | Signed Kelonia deal valued up to USD 7.00 Billion in April 2026 |

| Allogene Therapeutics | United States | Niche Player | AlloCAR-T pipeline | United States, Europe | Continued allogeneic CAR-T clinical development through 2025 |

| Curocell Inc. | South Korea | Niche Player | Anbalcabtagene autoleucel programs | South Korea | Advanced Korean CAR-T commercialization and clinical expansion in 2025 |

By Therapy Type

The CAR-T cell therapy market by therapy type was led by autologous products with 88.0% share in 2025, equal to approximately USD 5.54 Billion. Autologous manufacturing dominates because Yescarta, Tecartus, Breyanzi, Abecma, Carvykti, Kymriah, and Aucatzyl are all made from patient-derived T cells. Gilead, Bristol Myers Squibb, Johnson & Johnson, Novartis, and Autolus compete on collection logistics, release testing, cryopreserved distribution, and treatment-center onboarding. The model offers proven clinical durability, but it ties revenue growth to cleanroom capacity, batch success, and hospital scheduling.

Allogeneic and in vivo CAR-T models represented the remaining 12.0% of market-linked revenue and investment value in 2025, mostly through clinical programs, partnerships, and manufacturing contracts rather than approved-product sales. Allogene Therapeutics, Cellectis, CRISPR Therapeutics, AbbVie, Eli Lilly, Capstan Therapeutics, Orna Therapeutics, and Kelonia Therapeutics define this segment. The contrast with autologous therapy is clear: allogeneic and in vivo approaches seek lower unit cost and faster dosing, while autologous products retain the strongest regulatory and efficacy evidence. Procurement teams should treat allogeneic and in vivo CAR-T as pipeline exposure, not a direct 2026 substitute for approved therapies.

By Target Antigen

CD19-directed CAR-T therapy held 54.0% of 2025 revenue, supported by lymphoma and leukemia use across Yescarta, Tecartus, Breyanzi, Kymriah, and Aucatzyl. CD19 remains the anchor antigen because B-cell malignancies present a validated biology, broad physician familiarity, and multiple reimbursed labels. Gilead’s Yescarta and Bristol Myers Squibb’s Breyanzi compete directly in large B-cell lymphoma and follicular lymphoma, while Autolus positions Aucatzyl in adult acute lymphoblastic leukemia. The segment is mature compared with BCMA, so revenue growth depends more on label additions and center access than first-time clinical acceptance.

BCMA-directed CAR-T therapy accounted for 42.0% of 2025 revenue and is forecast to outgrow CD19 through 2034. Carvykti from Johnson & Johnson and Legend Biotech, plus Abecma from Bristol Myers Squibb, moved into earlier multiple myeloma lines in 2024, expanding the treated population. BCMA also attracts in vivo investment because multiple myeloma has a large relapsed population, measurable disease markers, and established clinician demand. Other antigen programs, including CD22, DLL3, GPRC5D, and dual-target constructs, represented 4.0% of 2025 revenue exposure, mostly through clinical trials and partnership spending.

By Indication

Hematologic malignancies dominated the CAR-T cell therapy market with 96.0% of 2025 revenue, or approximately USD 6.05 Billion. Multiple myeloma generated the fastest commercial growth because Carvykti and Abecma entered earlier-line settings, while diffuse large B-cell lymphoma remained the main CD19 revenue pool for Yescarta and Breyanzi. Acute lymphoblastic leukemia revenue expanded after Aucatzyl approval in November 2024, but adult ALL remains smaller than lymphoma and myeloma in treated-patient volume. For hospital buyers, disease mix matters because intensive care utilization, leukapheresis demand, and slot planning differ by indication.

Solid tumors and autoimmune disease programs represented approximately 4.0% of 2025 market-linked value, largely through trials, platform acquisitions, and manufacturing infrastructure. Solid tumors remain difficult because antigen heterogeneity, physical tumor barriers, and on-target off-tumor toxicity reduce response durability. Autoimmune disease became the more investable expansion route in 2025 and 2026 because CD19 B-cell reset strategies may fit lupus, myasthenia gravis, systemic sclerosis, and related diseases. Capstan, Orna, and Kelonia deals show that large pharmaceutical companies are positioning for immune reset indications before product revenue exists.

By Manufacturing Model

Ex vivo centralized manufacturing held 83.0% of the CAR-T cell therapy market in 2025 because commercial products rely on specialized manufacturing networks operated by Kite Pharma, Bristol Myers Squibb, Novartis, Johnson & Johnson, Legend Biotech, and Autolus. Central sites support controlled viral transduction, expansion, release testing, and cryopreserved shipping, which regulators understand. The weakness is operational: every patient requires a bespoke batch, and chain-of-identity control adds cost. Pricing benchmarks for U.S. commercial products commonly exceed USD 400,000 before hospitalization and toxicity management.

Decentralized and in vivo manufacturing models made up 17.0% of market-linked value in 2025, mostly as platform investment, contract development, and clinical-trial spend. Lonza, Catalent, Thermo Fisher Scientific, Charles River Laboratories, and regional CDMOs compete for viral-vector and cell-processing contracts, while Lilly, AbbVie, and Gilead acquired in vivo assets to reduce dependence on cleanroom capacity. The procurement checklist for CAR-T manufacturing now includes vector yield, batch failure rate, release-test cycle time, cold-chain qualification, and digital chain-of-custody capability. By 2034, in vivo approaches could reduce treatment-center complexity if safety monitoring requirements stay manageable.

Regional Analysis

North America

The CAR-T cell therapy market in North America held 47.0% share in 2025, equal to USD 2.96 Billion, with the United States representing over 90.0% of regional revenue. FDA approvals, CMS hospital reimbursement, National Cancer Institute cancer-center density, and commercial networks from Kite Pharma, Bristol Myers Squibb, Johnson & Johnson, Novartis, and Autolus support adoption. FDA’s June 2025 REMS removal lowered administrative burden for qualified treatment centers. Compared with Europe, North America has faster launch uptake and higher net prices, but payer prior authorization and inpatient capacity still limit patient flow.

Europe

The CAR-T cell therapy market in Europe accounted for 25.0% share in 2025, equivalent to USD 1.58 Billion. Germany, France, the United Kingdom, Italy, and Spain drive most regional use because EMA approvals must still pass national reimbursement and hospital funding pathways. EMA label-warning requirements after its 2024 safety review strengthened long-term monitoring duties for CAR-T recipients. Europe grows slower than the United States because health technology assessment bodies scrutinize cost per quality-adjusted life year, yet public reimbursement gives approved products durable access once agreements are reached.

Asia Pacific

The CAR-T cell therapy market in Asia Pacific reached 22.0% share in 2025, or USD 1.39 Billion, and is forecast to post the fastest CAGR through 2034. China has domestic products including Fucaso and Carteyva, Japan reimburses several imported CAR-T brands, and South Korea supports local development through Curocell and university hospitals. JW Therapeutics secured Macao approval for Carteyva in June 2025, showing that Greater China access is widening beyond mainland regulatory pathways. Asia Pacific differs from North America because domestic pricing and insurance coverage are more variable, but manufacturing build-out is faster.

Latin America

The CAR-T cell therapy market in Latin America held 3.5% share in 2025, equivalent to USD 0.22 Billion. Brazil, Mexico, Argentina, and Colombia are the main markets, with private hospitals and academic cancer centers handling most patient referrals. ANVISA and COFEPRIS frameworks support cell therapy evaluation, but public reimbursement remains narrow compared with Europe. Regional demand is shaped by medical tourism, philanthropic access programs, and manufacturer-supported referral pathways. High product prices and cross-border cell logistics keep Latin America behind Asia Pacific despite a large lymphoma and leukemia patient pool.

Middle East & Africa

The CAR-T cell therapy market in Middle East & Africa represented 2.5% share in 2025, equal to USD 0.16 Billion. Saudi Arabia, the United Arab Emirates, Israel, and South Africa account for most regional demand, with Gulf programs using national health investment to fund advanced oncology centers. Saudi Vision 2030 and UAE biotech investment support local treatment infrastructure, while Israeli hospitals contribute clinical expertise in cellular immunotherapy. The region trails Europe because qualified manufacturing, apheresis networks, and payer coverage are concentrated in a small number of urban hospitals.

Country Analysis

United States

The United States CAR-T cell therapy market reached approximately USD 2.68 Billion in 2025 and is forecast to grow at a 15.2% CAGR through 2034. FDA approvals across seven CAR-T brands, CMS new-technology payment infrastructure, and more than 100 qualified treatment centers support uptake. FDA removal of REMS requirements in June 2025 reduced certification workload for BCMA- and CD19-directed autologous therapies. U.S. demand is led by multiple myeloma and lymphoma, with Carvykti, Yescarta, Breyanzi, Abecma, and Tecartus forming the commercial core.

China

China’s CAR-T cell therapy market reached approximately USD 0.58 Billion in 2025 and is forecast to grow at a 20.8% CAGR through 2034. NMPA-approved domestic and partnered products, including Carteyva and Fucaso, create a local alternative to imported therapy pathways. China differs from the United States because pricing is lower and provincial reimbursement remains uneven, but patient volume is larger. JW Therapeutics, IASO Biotherapeutics, Nanjing Legend, Fosun Kite, and major cancer hospitals support commercial scaling.

Germany

Germany’s CAR-T cell therapy market reached approximately USD 0.44 Billion in 2025 and is projected to grow at a 13.8% CAGR through 2034. Germany is Europe’s largest CAR-T market because statutory reimbursement, university hospital capacity, and early EMA product uptake align better than in most EU peers. Kymriah, Yescarta, Breyanzi, Abecma, Carvykti, and Tecartus are available through specialist centers. National benefit assessment still shapes pricing, so manufacturers use outcomes evidence and registry follow-up to protect reimbursement.

Japan

Japan’s CAR-T cell therapy market reached approximately USD 0.31 Billion in 2025 and is forecast to grow at a 14.6% CAGR through 2034. MHLW approvals and public insurance coverage support adoption of Kymriah, Yescarta, Breyanzi, Abecma, and Carvykti. Japan’s aging population raises demand in lymphoma and multiple myeloma, while high treatment prices keep access concentrated in certified hospitals. Takeda, Novartis, Bristol Myers Squibb, Johnson & Johnson, and local academic centers define commercial and clinical activity.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Therapy Type

- Autologous CAR-T Therapy

- Allogeneic CAR-T Therapy

By Target Antigen

- CD19

- BCMA

- CD20

- CD22

- Others

By Indication

- Acute Lymphoblastic Leukemia (ALL)

- Diffuse Large B-Cell Lymphoma (DLBCL)

- Multiple Myeloma

- Chronic Lymphocytic Leukemia (CLL)

- Others

By Manufacturing Model

- Centralized Manufacturing

- Decentralized (Point-of-Care) Manufacturing

- Hybrid Manufacturing

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 6.30 B |

| Forecast Revenue (2034) | USD 24.20 B |

| CAGR (2025-2034) | 16.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Therapy Type, (Autologous CAR-T Therapy, Allogeneic CAR-T Therapy), By Target Antigen, (CD19, BCMA, CD20, CD22, Others), By Indication, (Acute Lymphoblastic Leukemia (ALL), Diffuse Large B-Cell Lymphoma (DLBCL), Multiple Myeloma, Chronic Lymphocytic Leukemia (CLL), Others), By Manufacturing Model, (Centralized Manufacturing, Decentralized (Point-of-Care) Manufacturing, Hybrid Manufacturing), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | GILEAD SCIENCES, INC. / KITE PHARMA, JOHNSON & JOHNSON / JANSSEN BIOTECH, LEGEND BIOTECH CORPORATION, BRISTOL MYERS SQUIBB COMPANY, NOVARTIS AG, AUTOLUS THERAPEUTICS PLC, JW THERAPEUTICS, FOSUN KITE BIOTECHNOLOGY, IASO BIOTHERAPEUTICS, CARSgen THERAPEUTICS, ABBVIE INC., ELI LILLY AND COMPANY, ALLOGENE THERAPEUTICS, INC., CUROCELL INC., CRISPR THERAPEUTICS AG, CELLECTIS S.A., LONZA GROUP AG, THERMO FISHER SCIENTIFIC INC., CHARLES RIVER LABORATORIES, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Target Antigen (CD19, BCMA, CD20, CD22), By Indication (ALL, DLBCL, Multiple Myeloma, CLL), By Manufacturing Model (Centralized, Decentralized Point-of-Care, Hybrid) Industry Regional Outlook, Key Players – Market Dynamics, Competitive Landscape, Oncology & Cell Therapy Industry Trends, Investment Analysis & Forecast 2026-2034")

, By Target Antigen (CD19, BCMA, CD20, CD22), By Indication (ALL, DLBCL, Multiple Myeloma, CLL), By Manufacturing Model (Centralized, Decentralized Point-of-Care, Hybrid) Industry Regional Outlook, Key Players – Market Dynamics, Competitive Landscape, Oncology & Cell Therapy Industry Trends, Investment Analysis & Forecast 2026-2034")

, By Target Antigen (CD19, BCMA, CD20, CD22), By Indication (ALL, DLBCL, Multiple Myeloma, CLL), By Manufacturing Model (Centralized, Decentralized Point-of-Care, Hybrid) Industry Regional Outlook, Key Players – Market Dynamics, Competitive Landscape, Oncology & Cell Therapy Industry Trends, Investment Analysis & Forecast 2026-2034")

Frequently Asked Questions

How big is the CAR-T Cell Therapy Market?

Global CAR-T Cell Therapy Market was valued at USD 5.45 billion in 2024 and is projected to reach USD 24.20 billion by 2034, growing at a CAGR of 16.1% (2026–2034).

Who are the major players in the CAR-T Cell Therapy Market?

GILEAD SCIENCES, INC. / KITE PHARMA, JOHNSON & JOHNSON / JANSSEN BIOTECH, LEGEND BIOTECH CORPORATION, BRISTOL MYERS SQUIBB COMPANY, NOVARTIS AG, AUTOLUS THERAPEUTICS PLC, JW THERAPEUTICS, FOSUN KITE BIOTECHNOLOGY, IASO BIOTHERAPEUTICS, CARSgen THERAPEUTICS, ABBVIE INC., ELI LILLY AND COMPANY, ALLOGENE THERAPEUTICS, INC., CUROCELL INC., CRISPR THERAPEUTICS AG, CELLECTIS S.A., LONZA GROUP AG, THERMO FISHER SCIENTIFIC INC., CHARLES RIVER LABORATORIES, Others

Which segments covered the CAR-T Cell Therapy Market?

By Therapy Type, (Autologous CAR-T Therapy, Allogeneic CAR-T Therapy), By Target Antigen, (CD19, BCMA, CD20, CD22, Others), By Indication, (Acute Lymphoblastic Leukemia (ALL), Diffuse Large B-Cell Lymphoma (DLBCL), Multiple Myeloma, Chronic Lymphocytic Leukemia (CLL), Others), By Manufacturing Model, (Centralized Manufacturing, Decentralized (Point-of-Care) Manufacturing, Hybrid Manufacturing),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date