- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Carbon Accounting Software Market Size, Share | CAGR 22.2%

Global Carbon Accounting Software Market Size, Share, Analysis By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Component (Software Platforms, Consulting Services, Implementation & Integration Services, Managed Services, Support & Maintenance), By Enterprise Size (Large Enterprises, SMEs), By Industry Vertical (BFSI, Manufacturing, Energy & Utilities, IT & Telecommunications, Retail & E-Commerce, Healthcare) Industry Trends, ESG Reporting Solutions & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 22.51 Billion | USD 136.44 Billion | 22.2% | North America, 39.0% |

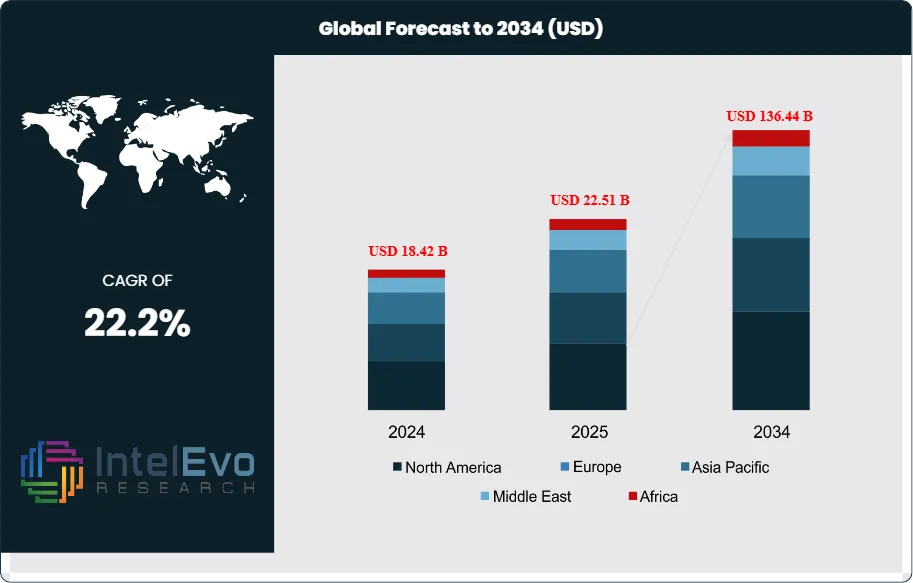

The Carbon Accounting Software Market was valued at approximately USD 18.42 Billion in 2024 and reached USD 22.51 Billion in 2025. The market is projected to grow to USD 136.44 Billion by 2034, expanding at a CAGR of 22.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 113.93 Billion over the analysis period. The Carbon Accounting Software Market covers enterprise platforms, APIs, and services that enable organizations to measure, track, disclose, and reduce greenhouse gas (GHG) emissions across Scope 1, Scope 2, and Scope 3 categories in alignment with the GHG Protocol, ISSB IFRS S1 and S2 standards, CDP questionnaires, and jurisdiction-specific disclosure rules.

Get More Information about this report -

Request Free Sample ReportDemand growth is anchored in a tightening global disclosure regime. The EU Corporate Sustainability Reporting Directive (CSRD) Wave 1 entities began reporting for fiscal year 2024 with disclosures published in 2025. Under the Omnibus I package approved by the European Parliament in December 2025, CSRD scope narrowed to companies with 1,000+ employees and EUR 450 million turnover, with Wave 2 reporting postponed from 2026 to 2028. California Senate Bill 261 first reports were due 1 January 2026 with SB 253 first reports expected 30 June 2026 per California Air Resources Board (CARB) guidance. Over 90% of S&P 500 companies disclose climate-related information, with approximately 60% providing quantitative emissions data.

Technology adoption is accelerating through AI integration. Persefoni AI raised USD 23 million in Series C funding in March 2025, bringing total capital to USD 179 million, and continued scaling PersefoniGPT and smart emission factor matching. AI-powered platforms extract activity data from unstructured PDF invoices with up to 95% accuracy in emissions factor mapping, reducing manual data entry by 80%. Machine learning enables Scope 3 supplier emissions visibility with 85% less manual effort versus legacy spreadsheet workflows. Microsoft Cloud for Sustainability, IBM Envizi, SAP Sustainability Control Tower, and Salesforce Net Zero Cloud lead the enterprise ERP-adjacent vendor cohort.

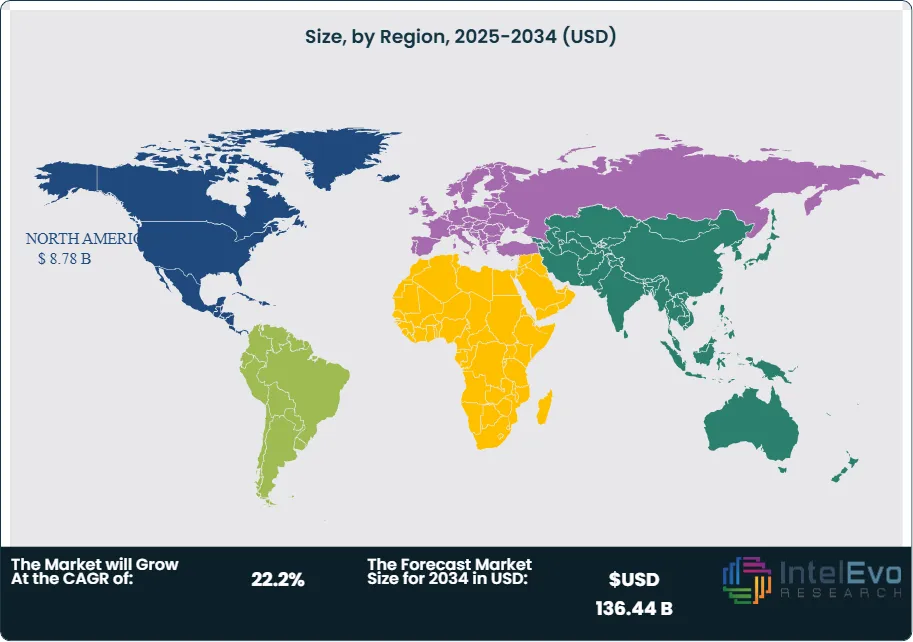

North America held 39.0% of global Carbon Accounting Software Market revenue in 2025, equivalent to USD 8.78 Billion, with the United States accounting for approximately 80% of regional spending. The SEC climate disclosure rule adopted in March 2024 mandates public companies to report material Scope 1 and Scope 2 emissions starting with fiscal year 2025 for large accelerated filers, though its implementation remains contested through 2025. Europe held approximately 30.0% share, reflecting the CSRD, European Sustainability Reporting Standards (ESRS), and EU Emissions Trading System compliance infrastructure. China accounted for 28.07% of the 2023 Asia Pacific subtotal, reflecting Ministry of Ecology and Environment carbon reporting mandates for listed companies.

Forward visibility through 2034 rests on three catalysts. First, CSRD Wave 4 entities, defined as non-EU parent companies generating more than EUR 150 million in EU turnover, must report for fiscal year 2028 with disclosures published in 2029, expanding addressable buyer count by tens of thousands globally. Second, the International Sustainability Standards Board (ISSB) IFRS S1 and S2 framework has been endorsed or adopted in 35+ jurisdictions through 2025, creating a converged global baseline. Third, AI-led automation of Scope 3 supplier data collection is unlocking platform deployments across mid-market companies that previously lacked budget for manual sustainability reporting. These forces together support the 22.2% forecast CAGR in the Carbon Accounting Software Market through 2034.

Market Definition & Scope

The Carbon Accounting Software Market is defined as the commercial space for enterprise software, SaaS subscriptions, APIs, and related managed services that enable organizations to measure, track, report, and reduce greenhouse gas emissions across Scope 1 (direct), Scope 2 (purchased energy), and Scope 3 (value chain) categories. The market encompasses emissions data ingestion, emission-factor matching, activity-based calculation engines, scenario modeling, audit-ready disclosure preparation, supplier engagement workflows, and integrations with ERP, finance, and energy management systems.

This analysis includes cloud-based (SaaS) and on-premise platforms sold to corporations, financial institutions, and public-sector buyers. The scope explicitly excludes voluntary carbon offset marketplaces (such as Patch standalone marketplace revenue), grid-decarbonization energy management software without GHG accounting modules, environmental health and safety (EHS) software without carbon modules, life-cycle assessment (LCA) consulting services without software subscription, and emissions-factor database publishing revenue. The parent enterprise sustainability software ecosystem reached approximately USD 60 Billion in 2025, with Carbon Accounting Software representing approximately 37% of the parent category.

, By Component (Software Platforms, Consulting Services, Implementation & Integration Services, Managed Services, Support & Maintenance), By Enterprise Size (Large Enterprises, SMEs), By Industry Vertical (BFSI, Manufacturing, Energy & Utilities, IT & Telecommunications, Retail & E-Commerce, Healthcare) Industry Trends, ESG Reporting Solutions & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Carbon Accounting Software Market grew from USD 22.51 Billion in 2025 to a projected USD 136.44 Billion in 2034, expanding at a 22.2% CAGR.

- Segment Dominance (By Deployment): Cloud-based deployment held 72.4% revenue share in 2025 and 73.3% in 2024, anchored by SaaS flexibility, lower capital expenditure, and integration with cloud ERP systems.

- Segment Dominance (By Industry): Energy and utilities accounted for the largest industry revenue share in 2024 and is projected to grow fastest at approximately 25% CAGR through 2034 under GHG Protocol Scope 1 exposure.

- Driver: Over 90% of S&P 500 companies disclose climate-related information in annual reports, with approximately 60% providing quantitative emissions data per 2025 disclosure tracking.

- Restraint: CSRD Omnibus I package approved in December 2025 narrowed scope to 1,000+ employee companies with EUR 450 million turnover, reducing addressable compliance-mandated buyers by 80% from the original CSRD design.

- Opportunity: California SB 253 (first reports 30 June 2026) and SB 261 (first reports 1 January 2026) apply to approximately 4,000 businesses per CARB preliminary list of 24 September 2025.

- Trend: AI-powered platforms reduce manual emissions data entry by 80% and achieve 95% accuracy in emissions factor mapping, enabling Scope 3 supplier visibility with 85% less manual effort.

- Regional: North America held 39.0% revenue share in 2025 at USD 8.78 Billion, followed by Europe at 30.0% at USD 6.75 Billion.

Key Insights Summary

- The European Parliament approved the Omnibus I package in December 2025, narrowing CSRD scope to companies with 1,000+ employees and EUR 450 million turnover, and postponing Wave 2 reporting from 2026 to 2028 under the Stop-the-Clock directive of April 2025.

- California Air Resources Board (CARB) released a preliminary list of approximately 4,000 businesses on 24 September 2025 covered by SB 253 and SB 261, with SB 261 first reports due 1 January 2026 and SB 253 first reports expected 30 June 2026.

- Persefoni AI raised USD 23 million in Series C funding in March 2025, bringing total capital to USD 179 million, with CEO Kentaro Kawamori projecting profitability by the second half of 2025.

- Sweep, headquartered in Paris, has raised approximately USD 100 million from Coatue-led rounds through 2025, anchoring Europe-focused CSRD and ISSB-aligned platform deployment.

- South Pole raised USD 120 million in a Series D funding round in May 2024 to expand the Carbon Action Platform, illustrating the scale of climate tech venture activity preceding the 2025 regulatory environment.

- AI-powered carbon platforms extract activity data from unstructured PDF invoices with 95% accuracy in emissions factor mapping, reducing manual data entry by 80% per vendor disclosures through 2025.

- Over 90% of S&P 500 companies disclose climate-related information in annual reports, with approximately 60% providing quantitative emissions data per 2025 disclosure tracking data.

Competitive Landscape Overview

The Carbon Accounting Software Market is moderately fragmented, with the top four companies including Microsoft, IBM, SAP, and Salesforce together holding an estimated 38 to 42% of global enterprise revenue in 2025. The next tier includes pure-play vendors Persefoni AI, Watershed, Sweep, Normative, and Sphera Solutions, which collectively hold approximately 22 to 26% of revenue. Competition is structured around ERP integration depth, Scope 3 supplier engagement tooling, AI-powered emission factor matching, and regulatory content coverage (CSRD, SB 253, SEC, ISSB).

The competitive environment is in active consolidation per Persefoni CEO Kentaro Kawamori, who publicly described the market as 'in consolidation phase, big time' in July 2025, citing weekly inbound buyout inquiries. Watershed serves an enterprise client base including Walmart, Airbnb, Stripe, DoorDash, BlackRock, and Klarna with emphasis on rapid disclosure preparation. Persefoni serves financial institutions including Citi, Bain and Company, Dropbox, and Evergy. Workiva positions as the disclosure-and-controls layer often deployed alongside purpose-built carbon engines rather than as a standalone emissions platform. Greenly targets small and mid-size enterprises with a self-serve model, while SINAI Technologies, CarbonChain, and CarbonCloud serve resource-intensive industries including transportation, mining, and commodity trading.

Competitive Landscape Matrix

| Company | HQ | Position | Key Platform | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Microsoft Corporation | Redmond, WA, USA | Leader | Microsoft Cloud for Sustainability; Sustainability Manager | Global | Continued expansion of Sustainability Manager with AI integration through 2025 |

| International Business Machines Corp. | Armonk, NY, USA | Leader | IBM Envizi ESG Suite; Carbon Performance Engine | Global | Continued Envizi platform expansion with AI-assisted Scope 3 tooling 2025 |

| SAP SE | Walldorf, Germany | Leader | SAP Sustainability Control Tower; Green Ledger | Global (EU-led) | Continued SAP Green Ledger rollout for CSRD-aligned sustainability reporting 2025 |

| Salesforce, Inc. | San Francisco, CA, USA | Leader | Net Zero Cloud | Global | Continued Net Zero Cloud feature expansion for CSRD disclosure workflows 2025 |

| Persefoni AI, Inc. | Tempe, AZ, USA | Leader (Pure-play) | Climate Management & Accounting Platform (CMAP); PersefoniGPT | North America | Raised USD 23M Series C in March 2025 bringing total funding to USD 179M |

| Watershed Technology, Inc. | San Francisco, CA, USA | Leader (Pure-play) | Watershed carbon accounting and disclosure platform | North America, EU | Continued expansion with Walmart, Airbnb, Stripe, BlackRock, Klarna client base 2025 |

| Sweep SAS | Paris, France | Challenger | Sweep carbon and sustainability data platform | EMEA | Raised approximately USD 100M from Coatue; continued EMEA expansion under CSRD 2025 |

| Normative Earth AB | Stockholm, Sweden | Challenger | Normative Carbon Accounting; Carbon Network | EU, UK | Continued Scope 3 visibility tooling expansion through 2025 |

| Sphera Solutions, Inc. | Chicago, IL, USA | Challenger | SpheraCloud Sustainability | Global | Continued enterprise sustainability operations platform expansion 2025 |

| Workiva Inc. | Ames, IA, USA | Challenger (Reporting) | Workiva ESG Reporting Platform | North America, EU | Continued expansion of CSRD and SEC disclosure reporting workflows 2025 |

Segmentation Analysis

The Carbon Accounting Software Market segments across deployment mode, component, enterprise size, and industry vertical. Procurement leaders building a carbon accounting software procurement checklist should benchmark vendors on Scope 3 coverage depth, regulatory framework alignment (CSRD, ESRS, ISSB, GHG Protocol, SB 253), data transparency, SOC 2 and ISO 27001 certifications, and audit-trail integrity across each segmentation dimension.

By Deployment Mode

Cloud-based deployment led the Carbon Accounting Software Market with 72.4% revenue share in 2025, equivalent to approximately USD 16.30 Billion. The cloud deployment model offers flexibility, scalability, subscription-based pricing, real-time data updates, and integration with adjacent cloud ERP systems from SAP, Oracle, Microsoft Dynamics, and Workday. Persefoni, Watershed, Sweep, Normative, and Greenly operate exclusively on cloud architecture, while legacy on-premise deployments persist mainly in resource-intensive industries with data-residency constraints.

On-premise deployment captured 27.6% revenue share in 2025 and is declining through the forecast period, with migration economics favoring cloud for new purchases. Hybrid deployments remain common among Fortune 500 buyers integrating carbon accounting with legacy EHS platforms. Carbon accounting software implementation timelines for cloud deployments typically range from 8 to 16 weeks for mid-market companies and 4 to 9 months for Fortune 1000 enterprises with global Scope 3 footprint.

By Component

Software licenses held 68% revenue share in 2025, equivalent to approximately USD 15.31 Billion, comprising platform subscriptions, module add-ons, and enterprise tier pricing. Services held 32% share, including implementation, data migration, supplier engagement, regulatory advisory, and audit preparation services. Services revenue is growing faster than software in 2025 as Wave 4 CSRD preparation and California SB 253 compliance drive advisory engagements. Large enterprise buyer contracts regularly exceed USD 500,000 in annual software plus services spend, with Fortune 100 deployments approaching USD 5 million annual run-rate.

By Enterprise Size

Large enterprises held 71% revenue share in 2025, reflecting the concentration of mandatory disclosure obligations under CSRD Omnibus I (1,000+ employees threshold), SB 253 (USD 1 Billion revenue threshold), and SEC large accelerated filer criteria. Small and medium enterprises (SMEs) captured 29% share and are growing fastest as value-chain supplier engagement from large-enterprise customers drives SME platform adoption. Persefoni Pro, a free self-guided SMB tier launched in March 2024, reached more than 6,000 organic sign-ups through 2025 per Persefoni disclosure. Normative, Sweep, and Greenly each operate free or freemium SME tiers to lock in supply-chain data capture.

By Industry Vertical

Energy and utilities led the Carbon Accounting Software Market with approximately 23% revenue share in 2025, equivalent to approximately USD 5.18 Billion, reflecting Scope 1 emissions exposure under EPA Greenhouse Gas Reporting Program and EU ETS. Manufacturing held 18% share, driven by automotive, steel, and chemicals companies tracking product-level embedded carbon. Financial services captured 16% share, with the Partnership for Carbon Accounting Financials (PCAF) framework driving bank and asset manager adoption of platforms including Persefoni, Watershed, and Normative. Technology and telecommunications held 12%, consumer products 10%, healthcare 8%, and remaining verticals including retail, transport, construction, and agriculture collectively 13%. Energy and utilities is projected to grow fastest at approximately 25% CAGR through 2034 under tightening Scope 1 disclosure rules.

Regional Analysis

The Carbon Accounting Software Market divides across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, with North America leading in 2025 and Asia Pacific growing fastest through 2034.

North America

North America held 39.0% of global Carbon Accounting Software Market revenue in 2025, equivalent to USD 8.78 Billion. The United States accounted for approximately 80% of regional revenue. The SEC climate disclosure rule adopted in March 2024 mandates large accelerated filers to report Scope 1 and 2 emissions for fiscal year 2025. California's SB 261 first reports were due 1 January 2026 and SB 253 first reports are expected 30 June 2026, with CARB's 24 September 2025 preliminary list covering approximately 4,000 businesses. Canada's Office of the Superintendent of Financial Institutions (OSFI) Guideline B-15 requires federally regulated financial institutions to disclose climate-related risks aligned with the ISSB framework. Mexico's CONBIVE sustainability reporting draft continues consultation.

Europe

Europe held 30.0% share in 2025 at approximately USD 6.75 Billion, with Germany, France, the Netherlands, Spain, and the Nordic countries leading adoption. The CSRD entered Wave 1 reporting in 2025 for fiscal year 2024 disclosures, covering approximately 11,700 EU entities under the original scope. The Omnibus I package approved by the European Parliament in December 2025 narrowed scope to 1,000+ employee companies with EUR 450 million turnover. The European Sustainability Reporting Standards (ESRS) mandate double materiality assessment, Scope 1 through 3 emissions disclosure, and Paris Agreement-aligned transition plans. EFRAG submitted simplified ESRS to the European Commission in Q4 2025, reducing mandatory datapoints by 61% from approximately 1,100 to 430.

Asia Pacific

Asia Pacific captured approximately 22.0% share in 2025 at USD 4.95 Billion and is growing fastest at approximately 27% CAGR through 2034. China held approximately 28.07% of the Asia Pacific subtotal in 2023, driven by Ministry of Ecology and Environment carbon reporting rules for listed companies and expansion of the national Emissions Trading System (ETS). Japan's Financial Services Agency mandates TCFD-aligned disclosure for Prime Market listed companies, while Japan Sustainability Standards Board (SSBJ) finalized JSSB Standards No. 1 and No. 2 in March 2025 aligned with ISSB. Singapore's SGX climate disclosure rules apply phased by sector through 2025-2027. Australia's mandatory climate reporting under the Australian Accounting Standards Board AASB S2 began 1 January 2025 for Group 1 entities.

Latin America

Latin America held 4.5% share in 2025 at approximately USD 1.01 Billion, led by Brazil, Chile, Mexico, and Colombia. Brazil's Resolution CVM 193, effective 1 January 2026, requires listed companies to disclose ISSB-aligned sustainability and climate information. The Brazilian Federation of Banks FEBRABAN, a framework for voluntary GHG reporting, continues expansion through 2025. Chile's Comision para el Mercado Financiero (CMF) NCG 461 requires sustainability reporting for listed companies. Regional growth is constrained by currency volatility and mid-market SaaS purchasing capacity, though multinational subsidiaries in Sao Paulo, Santiago, and Mexico City deploy corporate-standard platforms tracking global headquarters decisions.

Middle East & Africa

The Middle East & Africa region held 4.5% share in 2025 at approximately USD 1.01 Billion. The United Arab Emirates' Federal Decree-Law No. 11 of 2024 on Climate Change requires large emitters to report GHG emissions starting in 2026. Saudi Arabia's Saudi Exchange (Tadawul) ESG Disclosure Guidelines apply voluntary reporting aligned with ISSB. South Africa's Johannesburg Stock Exchange requires sustainability reporting for listed issuers. Qatar's Financial Centre Regulatory Authority and Egypt's Financial Regulatory Authority continue framework development through 2025. Regional growth is driven by COP-cycle commitments including COP28 UAE Consensus of December 2023 and follow-through at COP29 Baku and COP30 Belem.

Country Analysis

The Carbon Accounting Software Market concentrates in four national markets that together contribute more than 60% of 2025 global revenue: the United States, Germany, China, and the United Kingdom.

United States

The United States generated approximately USD 7.02 Billion in Carbon Accounting Software Market revenue in 2025 and is projected to reach approximately USD 16.5 Billion by 2032 per Fortune Business Insights disclosure. The country CAGR is approximately 22.5% through 2034. California SB 253 (Climate Corporate Data Accountability Act) applies to companies with USD 1 billion or more in annual revenue, with first Scope 1 and 2 reports due 30 June 2026. SB 261 (Climate-Related Financial Risk Act) applies to companies with USD 500 million or more in revenue, with first reports due 1 January 2026. CARB released a preliminary list on 24 September 2025 of approximately 4,000 covered businesses. The SEC climate disclosure rule of March 2024 remains under court review, though large accelerated filer reporting for fiscal year 2025 proceeded under state-level pressure.

Germany

Germany contributed approximately USD 1.62 Billion in Carbon Accounting Software Market revenue in 2025, growing at a country CAGR of approximately 22.8% through 2034. Germany leads European CSRD implementation, with the Federal Office of Economics and Export Control (BAFA) and the Bundesanstalt fur Finanzdienstleistungsaufsicht (BaFin) supervising covered entities. The German Supply Chain Due Diligence Act (Lieferkettensorgfaltspflichtengesetz, or LkSG) applies to companies with 1,000+ employees effective January 2024, creating a parallel regulatory driver for supplier emissions data. Bayer AG, Siemens AG, SAP SE, BASF SE, and Mercedes-Benz Group AG are leading carbon accounting software buyers, frequently deploying SAP Sustainability Control Tower alongside specialist platforms.

China

China generated approximately USD 2.35 Billion in Carbon Accounting Software Market revenue in 2025, with a country CAGR of approximately 25.5% through 2034. The Ministry of Ecology and Environment (MEE) operates the national Emissions Trading System covering power generation and expanded to cement, steel, and aluminum sectors in 2024-2025. The Shanghai Stock Exchange, Shenzhen Stock Exchange, and Beijing Stock Exchange issued sustainability reporting guidelines effective 1 May 2024, with mandatory reporting for index constituents beginning with fiscal year 2025 disclosures published in 2026. China Securities Regulatory Commission (CSRC) supports harmonization with ISSB standards. Domestic vendors including MioTech, Zhonglun, and local SAP/Oracle integration partners compete alongside global platforms.

United Kingdom

The United Kingdom accounted for approximately USD 1.24 Billion in Carbon Accounting Software Market revenue in 2025, with a projected country CAGR of 21.5% through 2034. The Streamlined Energy and Carbon Reporting (SECR) framework applies to large UK companies, and the Financial Conduct Authority (FCA) TCFD-aligned disclosure rules cover listed companies and large asset managers. The UK Sustainability Reporting Standards (UK SRS), based on ISSB IFRS S1 and S2, are progressing through government endorsement in 2025-2026. Companies House reforms and the UK Transition Plan Taskforce framework provide additional regulatory tailwinds. Major UK buyers include HSBC, Unilever, BP, Shell, Diageo, and GlaxoSmithKline, frequently deploying Persefoni, Watershed, Sweep, or IBM Envizi alongside Workiva disclosure orchestration.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Deployment Mode

- Cloud-Based

- On-Premise

- Hybrid

By Component

- Software Platforms

- Services

- Consulting Services

- Implementation & Integration Services

- Managed Services

- Support & Maintenance Services

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By Industry Vertical

- BFSI

- Manufacturing

- Energy & Utilities

- IT & Telecommunications

- Retail & E-Commerce

- Healthcare & Life Sciences

- Transportation & Logistics

- Government & Public Sector

- Food & Beverage

- Others (Education, Real Estate, Chemicals, Agriculture)

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 22.51 B |

| Forecast Revenue (2034) | USD 136.44 B |

| CAGR (2025-2034) | 22.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Deployment Mode, (Cloud-Based, On-Premise, Hybrid), By Component, (Software Platforms, Services), By Enterprise Size, (Large Enterprises, Small & Medium Enterprises (SMEs)), By Industry Vertical, (BFSI, Manufacturing, Energy & Utilities, IT & Telecommunications, Retail & E-Commerce, Healthcare & Life Sciences, Transportation & Logistics, Government & Public Sector, Food & Beverage, Others (Education, Real Estate, Chemicals, Agriculture)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MICROSOFT CORPORATION, INTERNATIONAL BUSINESS MACHINES CORP., SAP SE, SALESFORCE, INC., PERSEFONI AI, INC., WATERSHED TECHNOLOGY, INC., SWEEP SAS, NORMATIVE EARTH AB, SPHERA SOLUTIONS, INC., WORKIVA INC., GREENLY SAS, DILIGENT CORPORATION, SINAI TECHNOLOGIES, INC., CARBONCHAIN LIMITED, CARBONCLOUD AB, ENABLON (WOLTERS KLUWER N.V.), ORACLE CORPORATION, INTELEX TECHNOLOGIES, GREENPLACES, INC., PATCH TECHNOLOGIES, INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Component (Software Platforms, Consulting Services, Implementation & Integration Services, Managed Services, Support & Maintenance), By Enterprise Size (Large Enterprises, SMEs), By Industry Vertical (BFSI, Manufacturing, Energy & Utilities, IT & Telecommunications, Retail & E-Commerce, Healthcare) Industry Trends, ESG Reporting Solutions & Forecast 2026-2034")

, By Component (Software Platforms, Consulting Services, Implementation & Integration Services, Managed Services, Support & Maintenance), By Enterprise Size (Large Enterprises, SMEs), By Industry Vertical (BFSI, Manufacturing, Energy & Utilities, IT & Telecommunications, Retail & E-Commerce, Healthcare) Industry Trends, ESG Reporting Solutions & Forecast 2026-2034")

, By Component (Software Platforms, Consulting Services, Implementation & Integration Services, Managed Services, Support & Maintenance), By Enterprise Size (Large Enterprises, SMEs), By Industry Vertical (BFSI, Manufacturing, Energy & Utilities, IT & Telecommunications, Retail & E-Commerce, Healthcare) Industry Trends, ESG Reporting Solutions & Forecast 2026-2034")

Frequently Asked Questions

How big is the ?

The Global Carbon Accounting Software Market was valued at USD 18.42 Billion in 2024 and is projected to reach USD 136.44 Billion by 2034, growing at a CAGR of 22.2% from 2026 to 2034. Growth is driven by increasing ESG reporting requirements, corporate net-zero commitments, carbon emissions tracking initiatives, sustainability management programs, regulatory compliance mandates, and the rising adoption of AI-powered carbon accounting and environmental reporting solutions across industries worldwide.

Who are the major players in the ?

MICROSOFT CORPORATION, INTERNATIONAL BUSINESS MACHINES CORP., SAP SE, SALESFORCE, INC., PERSEFONI AI, INC., WATERSHED TECHNOLOGY, INC., SWEEP SAS, NORMATIVE EARTH AB, SPHERA SOLUTIONS, INC., WORKIVA INC., GREENLY SAS, DILIGENT CORPORATION, SINAI TECHNOLOGIES, INC., CARBONCHAIN LIMITED, CARBONCLOUD AB, ENABLON (WOLTERS KLUWER N.V.), ORACLE CORPORATION, INTELEX TECHNOLOGIES, GREENPLACES, INC., PATCH TECHNOLOGIES, INC., Others

Which segments covered the ?

By Deployment Mode, (Cloud-Based, On-Premise, Hybrid), By Component, (Software Platforms, Services), By Enterprise Size, (Large Enterprises, Small & Medium Enterprises (SMEs)), By Industry Vertical, (BFSI, Manufacturing, Energy & Utilities, IT & Telecommunications, Retail & E-Commerce, Healthcare & Life Sciences, Transportation & Logistics, Government & Public Sector, Food & Beverage, Others (Education, Real Estate, Chemicals, Agriculture))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Carbon Accounting Software Market

Published Date : 05 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date