- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Carbon Black Market Size Growth Outlook & Forecast | CAGR of 6.7%

Global Carbon Black Market Size, Share & Analysis By Type (Furnace Black, Channel Black, Thermal Black, Acetylene Black, Others), By Grade (Standard Grade, Specialty Grade), By Application (Tire Rubber, Non-Tire Rubber, Inks and Coatings, Plastics, Others), By End-Use Industry, Price Volatility, Capacity Expansion & Forecast 2025–2034

Report Overview

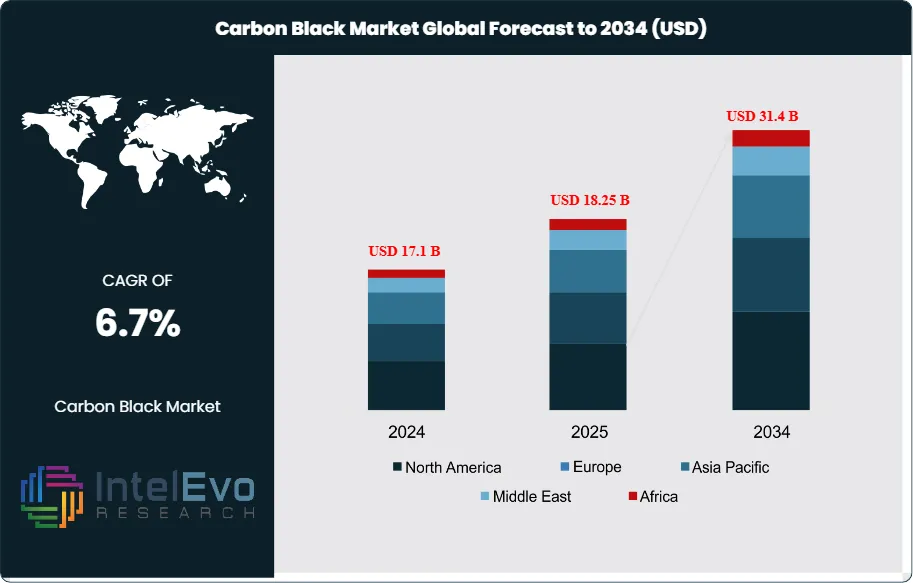

The Carbon Black Market is valued at approximately USD 17.1 billion in 2024 and is projected to reach nearly USD 31.4 billion by 2034, expanding at a CAGR of around 6.7% during 2025–2034. Growing consumption in automotive tires, conductive plastics, industrial rubber goods, and lithium-ion battery applications is reinforcing long-term demand worldwide. The shift toward high-performance and sustainable grades, along with capacity expansions across Asia Pacific, continues to reshape competitive dynamics.

Get More Information about this report -

Request Free Sample ReportThis steady expansion reflects the market’s critical role in diverse industrial applications, underpinned by both demand-side growth from key end-use sectors and advances in processing technologies. Historically, the market has demonstrated resilience, with incremental adoption driven by the tire and rubber industries, which account for over 70% of total consumption, alongside increasing penetration in plastics, coatings, and specialty applications. The recent acceleration in global mobility trends, construction activity, and infrastructure investment has further lifted demand, while environmental regulations and supply chain realignments have added complexity to the market outlook.

Carbon black’s functionality as a reinforcing filler and pigment remains at the heart of its growth. Its ability to enhance mechanical strength, abrasion resistance, and UV protection continues to drive adoption in automotive tires, rubber products, and polymer-based applications. On the demand side, rising global vehicle production—expected to surpass 95 million units by 2030—represents a significant volume driver. Simultaneously, the plastics industry, valued at over USD 700 billion, is increasingly incorporating carbon black for insulation, color stabilization, and performance improvements. However, supply-side challenges such as reliance on petroleum-based feedstocks, energy-intensive production, and tightening emissions regulations in regions like Europe and North America pose headwinds, compelling producers to innovate toward cleaner and more efficient processes.

Technological innovation is reshaping the industry, particularly through the development of sustainable manufacturing pathways. Emerging solutions such as recovered carbon black (rCB) from end-of-life tires, coupled with process automation, AI-driven quality monitoring, and digitalized supply chain management, are enhancing cost efficiency and environmental compliance. These advancements are expected to account for a growing share of market revenues over the coming decade, with sustainability considerations shaping investment priorities.

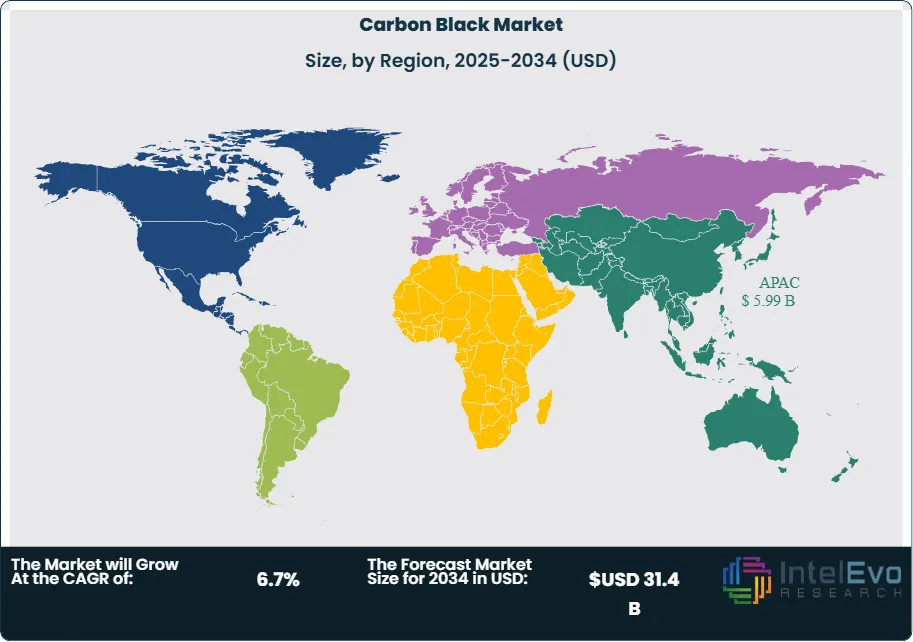

Regionally, Asia-Pacific dominates the market, accounting for nearly 50% of global consumption, fueled by robust automotive and industrial output in China, India, and Southeast Asia. North America and Europe remain mature yet innovation-driven markets, with investments focused on sustainable production and specialty-grade carbon black. Meanwhile, emerging economies in Latin America and Africa represent nascent growth hotspots, supported by rising urbanization and infrastructure spending. For investors, opportunities lie in scaling sustainable technologies, expanding specialty applications, and tapping underpenetrated markets where industrial demand is expected to accelerate sharply through 2034.

, By Grade (Standard Grade, Specialty Grade), By Application (Tire Rubber, Non-Tire Rubber, Inks and Coatings, Plastics, Others), By End-Use Industry, Price Volatility, Capacity Expansion & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global carbon black market was valued at USD 17.1 billion in 2024 and is projected to reach USD 31.4 billion by 2034, expanding at a CAGR of 6.7% over 2025–2034, driven by sustained demand from automotive, plastics, and industrial manufacturing sectors.

- Product Type: Furnace black remains the leading product type, accounting for over 75% of global output, due to its cost-efficiency and superior reinforcement properties for rubber and tire applications.

- Application: Tire manufacturing dominates with nearly 70% of total consumption, underpinned by rising global vehicle production and replacement tire demand, which together generate consistent revenue streams for producers.

- Driver: Expanding automotive production—forecasted to surpass 95 million vehicles by 2030—continues to boost tire consumption, reinforcing carbon black’s role as a critical raw material for performance durability and safety.

- Restraint: Stringent environmental regulations, particularly in North America and Europe, along with volatility in petroleum-derived feedstock prices, are exerting pressure on margins and prompting costly compliance investments.

- Opportunity: Recovered carbon black (rCB) from end-of-life tires presents a fast-growing segment, projected to grow at over 10% CAGR through 2030, offering both cost savings and alignment with sustainability mandates.

- Trend: Leading producers such as Cabot Corporation and Birla Carbon are investing in AI-driven process optimization and circular economy models, including carbon black recycling and cleaner production technologies, to meet regulatory and customer sustainability goals.

- Regional Analysis: Asia-Pacific leads with a 33.9% share and is expected to register a robust CAGR of 8.1% through 2034, driven by automotive and industrial expansion in China and India. Europe and North America, though mature, are innovation hubs emphasizing sustainable production and specialty-grade carbon black, while Latin America and Africa represent emerging high-growth regions.

Type Analysis

The carbon black market is segmented into furnace black, channel black, acetylene black, thermal black, and other niche variants, with furnace black commanding the largest share. As of 2025, furnace black accounts for more than 70% of total production, supported by its cost efficiency and superior reinforcing properties for rubber, particularly in the tire industry. Its role extends beyond automotive, with growing use as a pigment in plastics, coatings, and even cosmetics, reinforcing its dominance across industries.

Thermal black is gaining traction due to its high UV absorption capacity, making it increasingly relevant for plastics and rubber-based adhesives where weather resistance is critical. Meanwhile, acetylene black, noted for its ultra-high purity and exceptional conductivity, is witnessing rising adoption in lithium-ion batteries, dry cells, and power cables—sectors poised for rapid growth amid electrification trends. Although channel black accounts for a smaller share, its unique fine-particle properties sustain niche demand, particularly in coatings and inks where high jetness and dispersion are valued. Collectively, these diverse applications highlight a balanced yet furnace-led market structure, with specialty subtypes gradually expanding their influence.

Grade Analysis

The market is bifurcated into standard grade and specialty grade, with specialty carbon black emerging as the dominant segment. Specialty grades are increasingly vital in high-performance applications due to their properties such as enhanced conductivity, UV resistance, and superior dispersion. By 2025, specialty carbon blacks are projected to represent nearly 40% of total market revenues, propelled by demand from polymers, printing inks, coatings, and electronic components.

Rapid expansion in consumer electronics, automotive coatings, and polymer composites has positioned specialty carbon blacks as critical enablers of performance and durability. In contrast, standard grades such as N772 and N660 remain indispensable for general-purpose industrial rubber products, particularly in heavy-duty applications like conveyor belts and hoses. While specialty grades command higher margins, standard grades continue to secure stable volumes, ensuring that the market maintains a dual-growth trajectory catering to both mass industrial demand and advanced material applications.

Application Analysis

Tire manufacturing remains the largest application area, accounting for around 65–70% of total consumption in 2025. Carbon black plays a crucial role in extending tire life by dissipating heat and reinforcing strength, making it indispensable as global vehicle production and replacement tire demand grow steadily. With the automotive industry projected to surpass 100 million units annually by 2030, tire-related applications will remain the backbone of market growth.

Non-tire rubber applications, including conveyor belts, roofing membranes, gaskets, and hoses, are gaining momentum as industries prioritize durability and cost efficiency in materials. Inks, coatings, and plastics together form another high-potential segment, supported by rising consumer preference for black-colored products and expanding use in electronics and packaging. Specialty coatings, conductive polymers, and high-gloss plastics are expected to lift demand further, diversifying carbon black’s application base beyond traditional tire-centric usage.

Regional Analysis

Asia-Pacific leads the global market, accounting for more than 35% of revenues in 2025 and projected to grow at a CAGR above 7% through 2034. This dominance is fueled by rapid industrialization in China and India, where polymer, tire, and automotive manufacturing continue to expand at scale. Southeast Asian nations, including Thailand, Malaysia, and Vietnam, are also emerging as production hubs, driven by investments in construction and manufacturing.

North America maintains a strong position with robust demand from automotive and polymer industries, supported by R&D into sustainable and specialty carbon blacks. Europe, while a mature market, is shifting focus toward high-value specialty grades, particularly for coatings, plastics, and electronics. The Middle East & Africa and Latin America, though smaller in size, present untapped growth opportunities. Rising infrastructure development, urbanization, and industrial investments are expected to accelerate carbon black demand in these regions, positioning them as the next wave of investment hotspots.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Furnace Black

- Channel Black

- Thermal Black

- Acetylene Black

- Others

By Grade

- Standard Grade

- Specialty Grade

By Application

- Tire Rubber

- Non-Tire Rubber

- Inks and Coatings

- Plastics

- Others

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 17.1 B |

| Forecast Revenue (2034) | USD 31.4 B |

| CAGR (2024-2034) | 6.7% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Furnace Black, Channel Black, Thermal Black, Acetylene Black, Others), By Grade (Standard Grade, Specialty Grade), By Application (Tire Rubber, Non-Tire Rubber, Inks and Coatings, Plastics, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Mitsubishi Chemical Corporation, Omsk Carbon Group, Orion Engineered Carbons GmbH, Cabot Corporation, Longxing Chemical Stock Co. Ltd, Atlas Organics Private Limited, Philips Carbon Black Limited, PCBL Limited, Birla Carbon, Jiangxi Black Cat Carbon Black Co. Ltd., Continental Carbon Company, Himadri Speciality Chemical Ltd, Tokai Carbon Co. Ltd., Orion Engineered Carbons S.A., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Grade (Standard Grade, Specialty Grade), By Application (Tire Rubber, Non-Tire Rubber, Inks and Coatings, Plastics, Others), By End-Use Industry, Price Volatility, Capacity Expansion & Forecast 2025–2034")

, By Grade (Standard Grade, Specialty Grade), By Application (Tire Rubber, Non-Tire Rubber, Inks and Coatings, Plastics, Others), By End-Use Industry, Price Volatility, Capacity Expansion & Forecast 2025–2034")

, By Grade (Standard Grade, Specialty Grade), By Application (Tire Rubber, Non-Tire Rubber, Inks and Coatings, Plastics, Others), By End-Use Industry, Price Volatility, Capacity Expansion & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date