- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Carbon Fiber Reinforced Polymer Market Forecast 2034 | CAGR 8.0%

Global Carbon Fiber Reinforced Polymer Market Size, Share, Growth & Industry Analysis By Fiber Type (PAN-Based Carbon Fiber Composites, Pitch-Based Carbon Fiber Composites, Rayon-Based & Others), By Resin Type (Thermoset Including Epoxy, Vinyl Ester, Polyester, BMI and Thermoplastic Including PEEK, PA6, PPS, PEI), By Manufacturing Process (Prepreg Lay-Up, RTM, Filament Winding, Pultrusion, Compression Molding), By End-Use Industry (Aerospace & Defense, Wind Energy, Automotive, Construction) Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

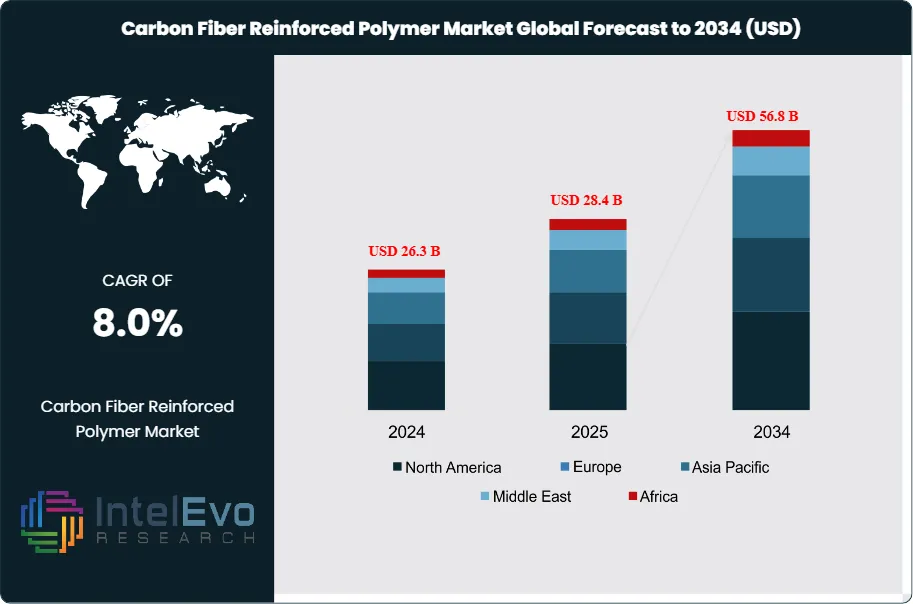

| USD 28.4 Billion | USD 56.8 Billion | 8.0% | North America, 38.6% |

The Carbon Fiber Reinforced Polymer Market was valued at approximately USD 26.3 Billion in 2024 and reached USD 28.4 Billion in 2025. The market is projected to grow to USD 56.8 Billion by 2034, expanding at a CAGR of 8.0% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 28.4 Billion over the analysis period. Carbon fiber reinforced polymer (CFRP) composites combine high tensile strength (typically 3,500–7,000 MPa), low density (approximately 1.55 g/cm³), and corrosion resistance, making them indispensable across aerospace, automotive, wind energy, and sporting goods applications. Global production capacity for polyacrylonitrile (PAN)-based carbon fiber reached approximately 215,000 tonnes in 2025, with Toray Industries, Hexcel, Teijin, and SGL Carbon controlling roughly 52% of upstream fiber output.

Get More Information about this report -

Request Free Sample ReportDemand from commercial aerospace continues to anchor the market. Single-aisle aircraft programs such as the Airbus A320neo and Boeing 737 MAX consume 15–20% CFRP by structural weight, while wide-body platforms like the A350 XWB and Boeing 787 incorporate over 50% composite content. Automotive lightweighting regulations, including the EU’s CO2 emission target of 93.6 g/km by 2025 under Euro 7 and CAFE standards in the United States, are accelerating CFRP adoption in structural battery enclosures, body-in-white panels, and crash structures for electric vehicles. Wind energy is the fastest-growing application segment; turbine blades exceeding 100 meters now require carbon fiber spar caps to maintain structural rigidity at reduced weight. The carbon fiber reinforced polymer market also benefits from expanding defense procurement budgets. The U.S. Department of Defense allocated over USD 19 Billion toward advanced material programs in fiscal year 2025.

Asia Pacific accounted for 38.6% of global CFRP revenue in 2025, driven by aerospace supply chain growth in Japan, EV manufacturing in China, and wind turbine production across the region. North America held 29.3%, supported by defense spending and the Boeing commercial backlog. Europe contributed 24.1%, led by Airbus programs and German automotive OEM lightweighting. Recycling and sustainability mandates under EU REACH regulation and the TSCA framework in the U.S. are pushing manufacturers toward thermoplastic CFRP matrices and pyrolysis-based fiber reclamation. ASTM D3039 and ISO 14125 testing standards govern mechanical qualification, ensuring consistent material performance across applications.

, By Resin Type (Thermoset Including Epoxy, Vinyl Ester, Polyester, BMI and Thermoplastic Including PEEK, PA6, PPS, PEI), By Manufacturing Process (Prepreg Lay-Up, RTM, Filament Winding, Pultrusion, Compression Molding), By End-Use Industry (Aerospace & Defense, Wind Energy, Automotive, Construction) Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The carbon fiber reinforced polymer market was valued at USD 28.4 Billion in 2025 and is projected to reach USD 56.8 Billion by 2034, expanding at a CAGR of 8.0% over the 2025–2034 forecast period.

- Segment Dominance (By Fiber Type): PAN-based carbon fiber composites held 92.1% of total market revenue in 2025, valued at USD 26.2 Billion, due to superior tensile strength and established aerospace qualification.

- Segment Dominance (By End-Use Industry): Aerospace and defense represented the largest application at 35.8% share in 2025, driven by composite-intensive aircraft platforms and military procurement.

- Driver: Aircraft production ramp-ups contributed an estimated USD 2.1 Billion in incremental CFRP demand in 2025, with Airbus and Boeing targeting combined deliveries exceeding 1,500 aircraft annually by 2026.

- Restraint: High raw material cost, with aerospace-grade carbon fiber priced at USD 22–35/kg in 2025, limits adoption in price-sensitive automotive and construction applications, constraining approximately 12–15% of addressable demand.

- Opportunity: Electric vehicle structural components represent a USD 8.5 Billion addressable CFRP market by 2034, enabled by declining fiber costs and automated tape laying processes that cut cycle times below 3 minutes per part.

- Trend: Thermoplastic CFRP adoption reached 14.7% of total composite shipments in 2025, up from 8.2% in 2022, driven by recyclability, weldability, and sub-60-second forming cycles.

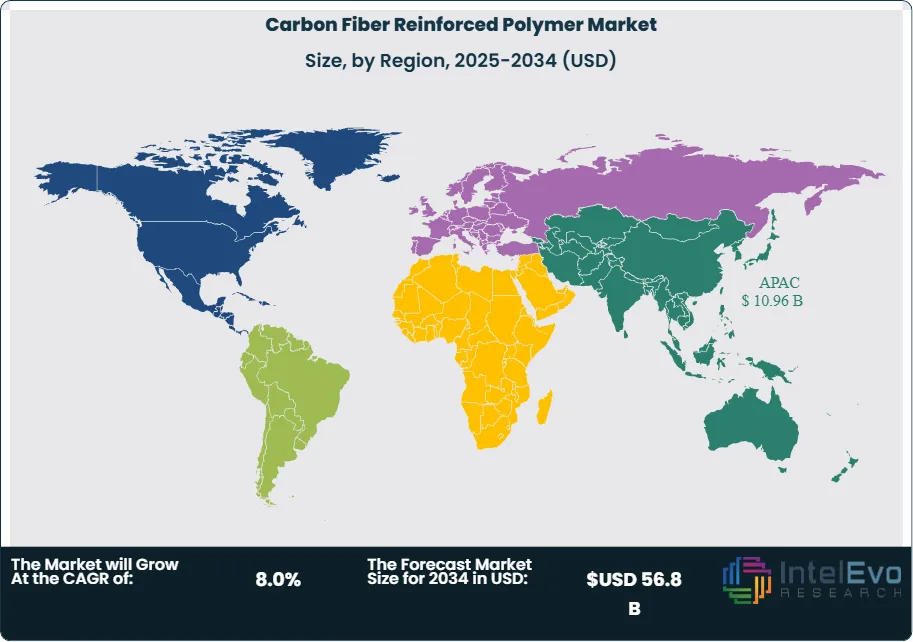

- Regional Analysis: Asia Pacific led with 38.6% market share and USD 10.96 Billion in revenue in 2025, anchored by Japanese fiber production, Chinese wind energy installations, and South Korean aerospace supply chains.

Competitive Landscape Overview

The carbon fiber reinforced polymer market is moderately consolidated, with the top four players; Toray Industries, Hexcel, Teijin, and SGL Carbon; collectively holding approximately 52% of global revenue in 2025. Competition centers on fiber grade qualification, resin chemistry, and supply chain proximity to OEM assembly lines. Toray alone commands roughly 28% of global PAN-based carbon fiber capacity. Between December 2024 and early 2026, at least eight capacity expansion projects were announced, representing over 35,000 tonnes of new annual fiber output. Strategic partnerships with aerospace OEMs and automotive platform agreements serve as critical competitive moats.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Toray Industries | Japan | Leader | Torayca T800/T1100 prepreg systems | Asia Pacific, North America | Expanded Moses Lake PAN capacity by 6,000 tonnes/yr (Mar 2025) |

| Hexcel Corporation | US | Leader | HexPly M56 prepreg | North America, Europe | Opened USD 250M composite center in Morocco (Jun 2025) |

| Teijin Limited | Japan | Leader | Tenax carbon fiber; Sereebo CFRP | Asia Pacific, Europe | Acquired carbon recycling firm CFK Valley (Jan 2025) |

| SGL Carbon | Germany | Leader | SIGRAFIL continuous fiber | Europe | Partnered with BMW for next-gen EV structural parts (Sep 2025) |

| Mitsubishi Chemical | Japan | Challenger | PYROFIL carbon fiber | Asia Pacific | Commissioned 4,500 t/yr PAN line in Otake (Dec 2024) |

| Solvay | Belgium | Challenger | APC-2 PEEK/carbon tape | Europe, North America | Launched fast-cure resin for automotive CFRP (Apr 2025) |

| SABIC | Saudi Arabia | Challenger | UDMAX GPP tapes | Middle East, Europe | Signed 10-yr supply deal with Airbus for thermoplastic CFRP (Feb 2025) |

| DowAksa | Turkey/US | Challenger | A-42 large-tow carbon fiber | Europe, North America | Broke ground on 12,000 t/yr plant in Yalova, Turkey (May 2025) |

| Hyosung Advanced Materials | South Korea | Challenger | TANSOME carbon fiber | Asia Pacific | Secured USD 180M Korean gov. subsidy for aerospace-grade line (Nov 2024) |

| Cytec/Solvay Composite Materials | US/Belgium | Niche Player | MTM 45-1 prepreg | North America | Qualified MTM 49 resin for Lockheed Martin F-35 repairs (Mar 2025) |

By Fiber Type

PAN-based carbon fiber composites dominated with 92.1% market share in 2025, generating USD 26.2 Billion. Polyacrylonitrile precursor provides the highest tensile modulus (230–600 GPa) and strength characteristics required for aerospace primary structures, pressure vessels, and high-performance automotive parts. Toray’s T800 and T1100 grades set industry benchmarks for intermediate-modulus fiber, achieving tensile strengths exceeding 6,500 MPa. The PAN segment benefits from decades of aerospace qualification data and established supply agreements with Airbus, Boeing, Lockheed Martin, and Northrop Grumman. Production economics continue to improve; large-tow PAN fiber (48K–50K filament count) costs fell to approximately USD 11–14/kg in 2025 for industrial applications, compared with USD 15–18/kg in 2020.

Pitch-based carbon fiber composites accounted for 5.4% of the market in 2025, valued at USD 1.53 Billion. Pitch precursor yields ultra-high-modulus fibers (modulus exceeding 900 GPa) with excellent thermal conductivity (400–900 W/mK), making them essential for satellite structures, thermal management systems, and semiconductor manufacturing equipment. Mitsubishi Chemical’s DIALEAD fiber leads this niche. Rayon-based and other precursor types composed the remaining 2.5%, serving specialized ablative and friction applications.

By Resin Type

Thermoset CFRP held 73.8% of market revenue in 2025, valued at USD 20.96 Billion. Epoxy-based thermoset systems remain the standard matrix for aerospace prepregs, offering excellent fiber-matrix adhesion, high glass transition temperatures (Tg of 180–220°C), and validated fatigue performance under cyclic loading. Hexcel’s HexPly and Toray’s Torayca prepreg families dominate the aerospace thermoset supply chain. Autoclave curing at 180°C and 6–7 bar pressure remains the primary consolidation method for structural parts, although out-of-autoclave (OoA) systems are gaining ground for secondary structures. The chief limitation of thermoset CFRP is its inability to be reformed or welded after curing, which complicates recycling.

Thermoplastic CFRP captured 26.2% of market share in 2025, valued at USD 7.44 Billion, and is growing at an estimated 11.3% CAGR through 2034. Polyether ether ketone (PEEK), polyamide 6 (PA6), and polyphenylene sulfide (PPS) matrices offer rapid forming cycles (under 60 seconds for stamp forming), inherent recyclability through remelting, and the ability to join parts via resistance or induction welding. Solvay’s APC-2 PEEK/carbon tape and SABIC’s UDMAX glass-carbon hybrid tapes are leading products. Automotive and wind energy OEMs are shifting toward thermoplastic matrices to meet EU REACH end-of-life recycling mandates.

By Manufacturing Process

Prepreg lay-up accounted for 38.2% of the CFRP market in 2025, generating USD 10.85 Billion. This process, involving pre-impregnated fiber sheets placed in molds and cured under heat and pressure, delivers the highest fiber volume fractions (55–65%) and the most consistent mechanical properties. It is the default process for aerospace primary structures. Automated tape laying (ATL) and automated fiber placement (AFP) machines from suppliers such as Electroimpact and Coriolis Composites have reduced lay-up cycle times by 30–40% compared with manual processes. Resin transfer molding (RTM) held 22.4% share (USD 6.36 Billion), favored for complex geometries in automotive and industrial applications. Filament winding contributed 16.8% (USD 4.77 Billion), primarily for pressure vessels, hydrogen storage tanks, and wind turbine components. Pultrusion accounted for 11.3% (USD 3.21 Billion), serving construction rebar, structural profiles, and transmission line conductors. Compression molding and other processes represented 11.3%.

By End-Use Industry

Aerospace and defense led with 35.8% share in 2025, valued at USD 10.17 Billion. Commercial aircraft platforms consume the largest volume; the Boeing 787 uses approximately 23 tonnes of CFRP per airframe, while the Airbus A350 XWB uses about 32 tonnes. Defense programs including the F-35 Lightning II, B-21 Raider, and various UAV platforms sustain high-value, long-term demand. Wind energy ranked second at 21.2% (USD 6.02 Billion), as blade lengths exceeding 100 meters increasingly require carbon fiber spar caps to prevent tip deflection. Automotive held 18.4% (USD 5.23 Billion), with BMW, Mercedes-Benz, and several EV startups integrating CFRP battery enclosures and structural floor assemblies. Sporting goods contributed 8.9% (USD 2.53 Billion), covering golf shafts, bicycle frames, and tennis rackets. Construction and infrastructure accounted for 6.8% (USD 1.93 Billion), driven by seismic retrofit wraps and bridge deck panels. Other industries, including marine, medical, and oil and gas, comprised the remaining 8.9%.

Regional Analysis

North America Carbon Fiber Reinforced Polymer Market

North America held 29.3% of the global carbon fiber reinforced polymer market in 2025, generating USD 8.32 Billion. The United States accounted for approximately 84% of regional revenue, driven by Boeing’s commercial aircraft backlog, Lockheed Martin and Northrop Grumman defense programs, and Vestas wind turbine blade manufacturing in Colorado. Hexcel and Toray Composite Materials America operate large-scale prepreg facilities in Salt Lake City and Tacoma, respectively. Toray’s Moses Lake, Washington plant is the largest single-site PAN-based carbon fiber facility in the Western Hemisphere, with annual capacity exceeding 24,000 tonnes. Canada contributed USD 0.68 Billion, supported by Bombardier’s aerospace composites division and growing hydrogen storage vessel production. Mexico added USD 0.36 Billion through its expanding aerospace manufacturing corridor in Queretaro and Chihuahua. U.S. Department of Commerce tariffs on Chinese carbon fiber imports, combined with Buy American provisions in defense procurement, protect domestic producers and incentivize nearshoring.

Europe Carbon Fiber Reinforced Polymer Market

Europe accounted for 24.1% of the market in 2025, valued at USD 6.84 Billion. Germany led at USD 2.18 Billion, anchored by BMW’s CFRP programs (Leipzig i-series production), SGL Carbon’s fiber and textile operations, and a dense automotive Tier 1 supply chain. The United Kingdom generated USD 1.32 Billion, with significant aerospace composite demand from Airbus’ Broughton wing facility, Rolls-Royce fan blade programs, and defense contractor BAE Systems. France contributed USD 1.08 Billion, supported by Airbus’ Nantes and Toulouse composite assembly lines and Safran’s aero-engine fan cases. Italy added USD 0.72 Billion through Lamborghini’s CFRP monocoque production and Leonardo Helicopters. EU REACH regulation mandates end-of-life management for thermoset composites, accelerating thermoplastic matrix adoption and investment in pyrolysis-based fiber recycling. The Clean Aviation Joint Undertaking has allocated over EUR 1.7 Billion equivalent for composite-intensive sustainable aviation research through 2030.

Asia Pacific Carbon Fiber Reinforced Polymer Market

Asia Pacific commanded 38.6% of the global carbon fiber reinforced polymer market in 2025, with revenue of USD 10.96 Billion. Japan led the region at USD 4.12 Billion, home to Toray, Teijin, and Mitsubishi Chemical; the three producers that collectively supply over 55% of global PAN-based carbon fiber. China generated USD 3.41 Billion, driven by the world’s largest wind energy installation base (over 450 GW cumulative capacity) and rapid growth in EV manufacturing, where BYD and NIO are integrating CFRP structural parts. South Korea contributed USD 1.54 Billion, with Hyosung Advanced Materials expanding aerospace-grade carbon fiber production and Hyundai Motor Group investing in composite body structures. India added USD 0.98 Billion, with DRDO defense programs, HAL aircraft manufacturing, and an expanding wind energy sector. Regional governments actively subsidize carbon fiber production; Japan’s METI allocated JPY 28 Billion for advanced material R&D in fiscal 2025, and China’s MIIT designated carbon fiber as a strategic material in its 14th Five-Year Plan.

Latin America Carbon Fiber Reinforced Polymer Market

Latin America represented 4.6% of the global market in 2025, valued at USD 1.31 Billion. Brazil led at USD 0.72 Billion, with Embraer’s commercial and defense aircraft programs consuming significant CFRP volumes; the E2 regional jet family uses approximately 12% composite content by structural weight. Mexico contributed USD 0.36 Billion through its growing aerospace manufacturing zone, where Safran and GE Aviation operate composite component plants. Argentina added approximately USD 0.12 Billion, concentrated in wind energy installations in Patagonia. The region’s growth is constrained by limited domestic fiber production, requiring imports primarily from Japan and the United States.

Middle East and Africa Carbon Fiber Reinforced Polymer Market

The Middle East and Africa held 3.4% of the global carbon fiber reinforced polymer market in 2025, generating USD 0.97 Billion. The UAE led at USD 0.34 Billion, supported by Strata Manufacturing’s composite aerostructure production for Airbus A350 and Boeing 787 programs in Al Ain. Saudi Arabia contributed USD 0.28 Billion, aligned with Vision 2030 defense localization targets and Saudi Arabian Airlines’ fleet expansion. South Africa generated USD 0.18 Billion through defense composites and wind energy projects. SABIC’s thermoplastic CFRP tape production in Riyadh and its 10-year supply agreement with Airbus position the Middle East as an emerging hub for composite materials.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Fiber Type

- PAN-Based Carbon Fiber Composites

- Pitch-Based Carbon Fiber Composites

- Rayon-Based and Others

By Resin Type

- Thermoset (Epoxy, Vinyl Ester, Polyester, BMI)

- Thermoplastic (PEEK, PA6, PPS, PEI)

By Manufacturing Process

- Prepreg Lay-Up (ATL/AFP)

- Resin Transfer Molding (RTM)

- Filament Winding

- Pultrusion

- Compression Molding and Others

By End-Use Industry

- Aerospace and Defense

- Wind Energy

- Automotive

- Sporting Goods

- Construction and Infrastructure

- Others (Marine, Medical, Oil and Gas)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 28.4 B |

| Forecast Revenue (2034) | USD 56.8 B |

| CAGR (2025-2034) | 8.0% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Fiber Type, (PAN-Based Carbon Fiber Composites, Pitch-Based Carbon Fiber Composites, Rayon-Based and Others), By Resin Type, (Thermoset (Epoxy, Vinyl Ester, Polyester, BMI), Thermoplastic (PEEK, PA6, PPS, PEI)), By Manufacturing Process, (Prepreg Lay-Up (ATL/AFP), Resin Transfer Molding (RTM), Filament Winding, Pultrusion, Compression Molding and Others), By End-Use Industry, (Aerospace and Defense, Wind Energy, Automotive, Sporting Goods, Construction and Infrastructure, Others (Marine, Medical, Oil and Gas)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | TORAY INDUSTRIES, HEXCEL CORPORATION, TEIJIN LIMITED, SGL CARBON, MITSUBISHI CHEMICAL GROUP, SOLVAY, SABIC, DOWAKSA, HYOSUNG ADVANCED MATERIALS, CYTEC (SOLVAY COMPOSITE MATERIALS), GURIT HOLDING, ZOLTEK (TORAY GROUP), NIPPON GRAPHITE FIBER, FORMOSA PLASTICS, HENGSHEN CO., LTD., ZHONGFU SHENYING CARBON FIBER, GKN AEROSPACE, SPIRIT AEROSYSTEMS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Resin Type (Thermoset Including Epoxy, Vinyl Ester, Polyester, BMI and Thermoplastic Including PEEK, PA6, PPS, PEI), By Manufacturing Process (Prepreg Lay-Up, RTM, Filament Winding, Pultrusion, Compression Molding), By End-Use Industry (Aerospace & Defense, Wind Energy, Automotive, Construction) Trends & Forecast 2026–2034")

, By Resin Type (Thermoset Including Epoxy, Vinyl Ester, Polyester, BMI and Thermoplastic Including PEEK, PA6, PPS, PEI), By Manufacturing Process (Prepreg Lay-Up, RTM, Filament Winding, Pultrusion, Compression Molding), By End-Use Industry (Aerospace & Defense, Wind Energy, Automotive, Construction) Trends & Forecast 2026–2034")

, By Resin Type (Thermoset Including Epoxy, Vinyl Ester, Polyester, BMI and Thermoplastic Including PEEK, PA6, PPS, PEI), By Manufacturing Process (Prepreg Lay-Up, RTM, Filament Winding, Pultrusion, Compression Molding), By End-Use Industry (Aerospace & Defense, Wind Energy, Automotive, Construction) Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Carbon Fiber Reinforced Polymer Market?

Global CFRP market valued at USD 26.3B in 2024, reaching USD 56.8B by 2034, growing at a CAGR of 8.0% from 2026–2034.

Who are the major players in the Carbon Fiber Reinforced Polymer Market?

TORAY INDUSTRIES, HEXCEL CORPORATION, TEIJIN LIMITED, SGL CARBON, MITSUBISHI CHEMICAL GROUP, SOLVAY, SABIC, DOWAKSA, HYOSUNG ADVANCED MATERIALS, CYTEC (SOLVAY COMPOSITE MATERIALS), GURIT HOLDING, ZOLTEK (TORAY GROUP), NIPPON GRAPHITE FIBER, FORMOSA PLASTICS, HENGSHEN CO., LTD., ZHONGFU SHENYING CARBON FIBER, GKN AEROSPACE, SPIRIT AEROSYSTEMS, Others

Which segments covered the Carbon Fiber Reinforced Polymer Market?

By Fiber Type, (PAN-Based Carbon Fiber Composites, Pitch-Based Carbon Fiber Composites, Rayon-Based and Others), By Resin Type, (Thermoset (Epoxy, Vinyl Ester, Polyester, BMI), Thermoplastic (PEEK, PA6, PPS, PEI)), By Manufacturing Process, (Prepreg Lay-Up (ATL/AFP), Resin Transfer Molding (RTM), Filament Winding, Pultrusion, Compression Molding and Others), By End-Use Industry, (Aerospace and Defense, Wind Energy, Automotive, Sporting Goods, Construction and Infrastructure, Others (Marine, Medical, Oil and Gas))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Carbon Fiber Reinforced Polymer Market

Published Date : 28 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date