- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Carbon Sequestration Technology Market Size, Trends | 12.3% CAGR

Global Carbon Sequestration Technology Market Size, Share, Analysis Report By Technology (Direct Air Capture, Carbon Capture & Storage, Ocean-based Sequestration, Terrestrial Sequestration), Application (Industrial, Agricultural, Energy, Transportation), End User (Oil & Gas, Power Generation, Manufacturing, Agriculture, Others), Capture Source (Power Plants, Industrial Processes, Transportation, Others), Storage Type (Geological, Ocean, Terrestrial), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

Report Overview

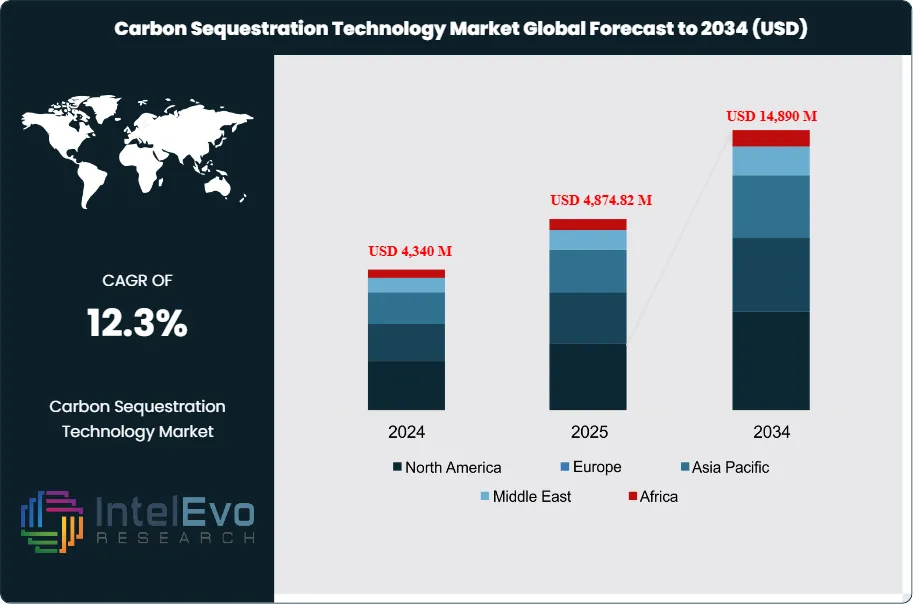

The Carbon Sequestration Technology Market size is projected to reach approximately USD 14,890 Million by 2034, up from USD 4,340 Million in 2024, growing at a CAGR of 12.3% during the forecast period from 2025 to 2034. This market growth is driven by the rising urgency to mitigate greenhouse gas emissions, the increasing adoption of carbon capture, utilization, and storage (CCUS) systems, and supportive climate-focused government policies worldwide. The transition toward net-zero targets, combined with innovations in direct air capture (DAC) and bioenergy carbon capture (BECCS), is redefining industrial sustainability. As industries intensify their decarbonization efforts, carbon sequestration technologies are set to become a cornerstone of global climate strategy, creating vast opportunities for energy, manufacturing, and environmental tech companies.

Get More Information about this report -

Request Free Sample ReportThis growth is driven by increasing global initiatives to reduce carbon emissions and meet climate change targets. Rising investments in advanced carbon capture and storage technologies, along with supportive government policies and environmental regulations, are accelerating the adoption of carbon sequestration solutions across industrial and energy sectors.

The global carbon sequestration technology market involves methods and technologies that capture and store atmospheric carbon dioxide (CO2) to mitigate the effects of climate change. Carbon sequestration can be achieved through biological processes (e.g., afforestation) or engineered methods, such as carbon capture and storage (CCS) in geological formations. The current market is driven by the urgent need to reduce greenhouse gas emissions and combat global warming, along with governmental policies and regulations. As of 2024, the market is valued at around USD 4,100 million, reflecting increasing adoption by industries like energy, manufacturing, and transportation that seek sustainable solutions to offset their carbon footprints.

The growth of the carbon sequestration technology market is primarily driven by the escalating global focus on achieving net-zero emissions. Governments and corporations are setting ambitious carbon reduction targets, stimulating investments in carbon capture and storage (CCS) technologies. Technological advancements in direct air capture and CCS systems, along with increasing funding for research and development, further bolster the market. The rise in carbon pricing mechanisms and the expansion of carbon trading markets also incentivize companies to adopt these technologies. Additionally, sectors like oil and gas, which are under intense scrutiny for emissions, are increasingly integrating carbon sequestration to improve sustainability.

North America is expected to dominate the carbon sequestration technology market, with the U.S. leading due to strong governmental support, regulatory frameworks, and significant investments in carbon capture projects. Europe follows closely, driven by strict environmental regulations and the European Union's climate policies promoting carbon neutrality by 2050. Asia-Pacific is witnessing rapid growth due to the industrial expansion in China and India, where efforts are being made to integrate carbon sequestration technologies into energy-intensive industries. Middle Eastern and African regions are gradually adopting carbon capture techniques, primarily due to the rising awareness of the economic benefits associated with reducing emissions.

The COVID-19 pandemic initially slowed the development of carbon sequestration projects due to disruptions in global supply chains, labor shortages, and reduced investments in large-scale infrastructure projects. However, the post-pandemic economic recovery has led to a resurgence of investments in green technologies. Governments worldwide are focusing on integrating climate policies into their recovery plans, emphasizing sustainable development, and accelerating the adoption of carbon sequestration technology. This renewed focus is expected to drive significant market growth in the coming years, as carbon reduction goals become more critical to future economic and environmental resilience.

, Application (Industrial, Agricultural, Energy, Transportation), End User (Oil & Gas, Power Generation, Manufacturing, Agriculture, Others), Capture Source (Power Plants, Industrial Processes, Transportation, Others), Storage Type (Geological, Ocean, Terrestrial), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Key Takeaways

- Market Growth: The global carbon sequestration technology market is projected to reach USD 14,890 million by 2034, growing at a robust CAGR of 12.3%, highlighting the increasing adoption of these technologies worldwide.

- Technology Dominance: Direct Air Capture (DAC) is expected to dominate the technology segment, driven by advancements in capturing atmospheric CO2 directly, making it a crucial tool for reducing global emissions across various industries.

- Application Dominance: The industrial sector is anticipated to hold the largest market share, as energy-intensive industries such as oil and gas, manufacturing, and power generation increasingly adopt carbon capture solutions to meet emission reduction targets.

- Driver: The growing global focus on achieving net-zero emissions by 2050 and stringent government regulations aimed at reducing carbon emissions are the primary drivers of growth in the carbon sequestration technology market.

- Restraint: High initial costs associated with the development and deployment of carbon sequestration technologies, coupled with technical challenges, pose significant barriers to widespread adoption in developing regions.

- Opportunity: Expanding carbon trading markets and increasing government subsidies for green technology projects present significant opportunities for carbon sequestration technologies to grow, especially in regions prioritizing climate goals.

- Trend: Technological innovations in direct air capture and carbon storage methods are shaping the market’s future, enhancing efficiency and scalability.

- Regional Analysis: North America is expected to dominate the market due to substantial investments in carbon capture projects and supportive government policies.

Technology

The carbon sequestration technology market is segmented into Direct Air Capture (DAC), Carbon Capture & Storage (CCS), ocean-based sequestration, and terrestrial sequestration. Direct Air Capture is gaining momentum due to its ability to directly capture CO2 from the atmosphere, playing a vital role in offsetting emissions from hard-to-decarbonize sectors. CCS, used primarily in industrial processes and power plants, captures CO2 before it is emitted into the atmosphere and stores it underground. Ocean-based sequestration focuses on enhancing natural ocean processes to store carbon, while terrestrial sequestration leverages forests and soil to absorb CO2. Each technology caters to different industries and applications, making the overall market highly diversified with tailored solutions for carbon reduction.

Application

The application segment of the carbon sequestration technology market includes industrial, agricultural, energy, and transportation sectors. Industrial applications are the largest contributors to market growth, with industries like oil & gas, cement, and steel implementing carbon capture to meet emission targets. In the energy sector, power plants are adopting CCS technology to curb emissions from fossil fuel combustion. Agriculture benefits from terrestrial sequestration, where soil management and afforestation help in carbon absorption. Transportation is gradually integrating sequestration through biofuels and electric vehicles, although it remains a smaller share. The diversity of applications indicates that carbon sequestration technology is essential across multiple industries striving to minimize their environmental footprint.

End User

The market is segmented by end users such as oil & gas, power generation, manufacturing, agriculture, and others. The oil & gas sector is a key end user, utilizing carbon capture technologies to reduce the significant emissions associated with fossil fuel extraction and refining. Power generation also plays a crucial role, particularly in coal and natural gas power plants, where CCS is applied to minimize emissions. Manufacturing industries, including cement and steel production, are increasingly adopting these technologies to meet stringent regulations. The agricultural sector relies on terrestrial sequestration to reduce its carbon impact, primarily through afforestation and soil management practices.

Capture Source

The market is divided into capture sources, including power plants, industrial processes, transportation, and others. Power plants, particularly those relying on fossil fuels, are the largest source of CO2 emissions and a primary focus for carbon capture technologies. Industrial processes, such as cement, steel, and chemical production, are also significant contributors to emissions and increasingly adopting CCS solutions. Transportation, while a smaller segment, is beginning to explore biofuel usage and direct capture technologies to offset carbon emissions from vehicles. Other sources include waste management and non-energy industries, showing the versatility of carbon capture technologies in addressing emissions from multiple sectors.

Storage Type

Carbon sequestration technologies use various storage types, including geological, ocean, and terrestrial storage. Geological storage, the most widely used method, involves injecting captured CO2 into underground reservoirs, including depleted oil and gas fields and saline aquifers. This method is favored for its long-term storage potential and minimal environmental impact. Ocean storage seeks to enhance the ocean’s natural carbon absorption processes by capturing and storing CO2 in deep-sea ecosystems, although it is still in experimental stages. Terrestrial storage focuses on afforestation, reforestation, and soil management techniques to increase the capacity of land-based ecosystems to absorb and retain carbon.

Region Analysis:

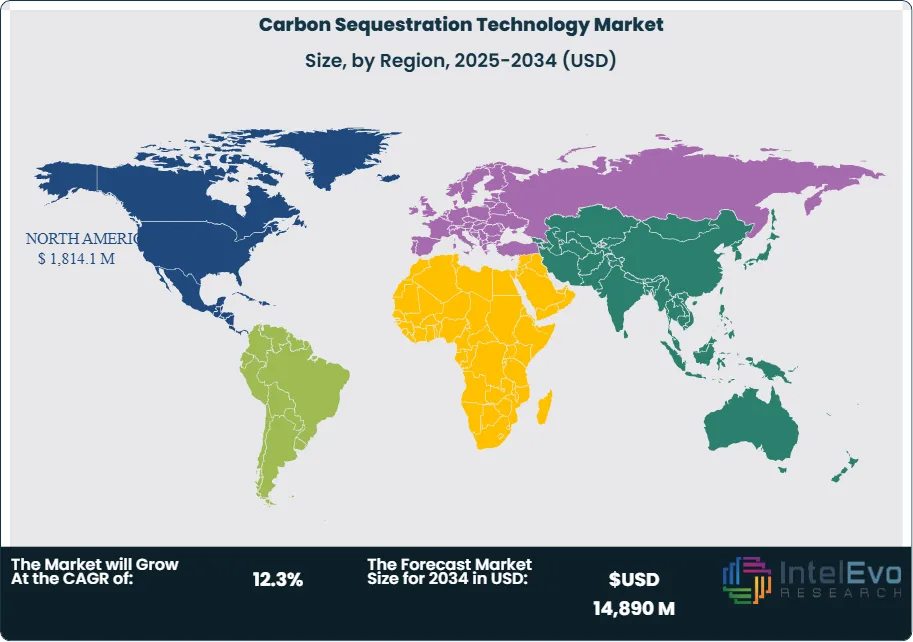

North America Leads With the Largest Market Share in the Carbon Sequestration Technology Market: North America holds the largest market share in the global carbon sequestration technology market, driven by strong governmental policies, substantial investments, and the presence of leading carbon capture and storage (CCS) projects, particularly in the United States and Canada. The U.S. government’s commitment to achieving net-zero emissions by 2050, combined with regulatory frameworks like the 45Q tax credit, has incentivized industries to adopt carbon sequestration technologies. Major oil and gas companies in North America are also heavily investing in CCS technologies to offset their emissions, particularly in regions with significant fossil fuel extraction. Additionally, advancements in direct air capture (DAC) technologies and increased funding for research and development contribute to North America's dominant position in the market.

Asia-Pacific is expected to be the fastest-growing region in the carbon sequestration technology market due to rapid industrialization, increasing energy demand, and growing government initiatives aimed at reducing emissions. China and India are at the forefront of this growth, with both countries investing heavily in carbon capture projects, especially in the power generation and industrial sectors. In China, carbon reduction goals tied to the country’s carbon neutrality target by 2060 are spurring the adoption of CCS technologies. Europe also exhibits strong growth potential, backed by the European Green Deal and stringent climate regulations, while Latin America and the Middle East & Africa are gradually integrating carbon capture solutions as they seek to reduce industrial emissions and participate in global climate initiatives.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Technology:

- Biological Carbon Sequestration

- Geological Carbon Sequestration

- Ocean-Based Carbon Sequestration

- Chemical/Industrial Sequestration

- Others

By Capture Source:

- Power Plants

- Industrial Processes

- Transportation

- Others

By Storage Type:

- Geological

- Ocean

- Terrestrial

By End User:

- Power Generation

- Oil & Gas

- Cement & Construction

- Agriculture

- Others

By Application:

- Industrial

- Agricultural

- Energy

- Transportation

By Region:

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4,874.82 M |

| Forecast Revenue (2034) | USD 14,890 M |

| CAGR (2025-2034) | 12.3% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Technology:(Biological Carbon Sequestration, Geological Carbon Sequestration, Ocean-Based Carbon Sequestration, Chemical/Industrial Sequestration, Others), Capture Source: (Power Plants, Industrial Processes, Transportation, Others), Storage Type: (Geological, Ocean, Terrestrial), End User: (Power Generation, Oil & Gas, Cement & Construction, Agriculture, Others), Application: (Industrial, Agricultural, Energy, Transportation) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ExxonMobil Corporation, Shell PLC, Chevron Corporation, Schlumberger Limited, TotalEnergies SE, Equinor ASA, BP PLC, Linde PLC, Siemens Energy AG, Fluor Corporation, Mitsubishi Heavy Industries Ltd., Aker Solutions ASA, Honeywell International Inc., General Electric Company, Halliburton Company, Air Products and Chemicals, Inc., Baker Hughes Company, Carbon Clean Solutions Limited, Climeworks AG, Global Thermostat |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Application (Industrial, Agricultural, Energy, Transportation), End User (Oil & Gas, Power Generation, Manufacturing, Agriculture, Others), Capture Source (Power Plants, Industrial Processes, Transportation, Others), Storage Type (Geological, Ocean, Terrestrial), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Application (Industrial, Agricultural, Energy, Transportation), End User (Oil & Gas, Power Generation, Manufacturing, Agriculture, Others), Capture Source (Power Plants, Industrial Processes, Transportation, Others), Storage Type (Geological, Ocean, Terrestrial), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Application (Industrial, Agricultural, Energy, Transportation), End User (Oil & Gas, Power Generation, Manufacturing, Agriculture, Others), Capture Source (Power Plants, Industrial Processes, Transportation, Others), Storage Type (Geological, Ocean, Terrestrial), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Frequently Asked Questions

How big is the Carbon Sequestration Technology Market?

Explore the Carbon Sequestration Technology Market, set to reach USD 14.9 Bn by 2034, growing at 12.3% CAGR, driven by CCUS and net-zero innovations.

Who are the major players in the Carbon Sequestration Technology Market?

ExxonMobil Corporation, Shell PLC, Chevron Corporation, Schlumberger Limited, TotalEnergies SE, Equinor ASA, BP PLC, Linde PLC, Siemens Energy AG, Fluor Corporation, Mitsubishi Heavy Industries Ltd., Aker Solutions ASA, Honeywell International Inc., General Electric Company, Halliburton Company, Air Products and Chemicals, Inc., Baker Hughes Company, Carbon Clean Solutions Limited, Climeworks AG, Global Thermostat

Which segments covered the Carbon Sequestration Technology Market?

Technology:(Biological Carbon Sequestration, Geological Carbon Sequestration, Ocean-Based Carbon Sequestration, Chemical/Industrial Sequestration, Others), Capture Source: (Power Plants, Industrial Processes, Transportation, Others), Storage Type: (Geological, Ocean, Terrestrial), End User: (Power Generation, Oil & Gas, Cement & Construction, Agriculture, Others), Application: (Industrial, Agricultural, Energy, Transportation)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Carbon Sequestration Technology Market

Published Date : 04 Dec 2024 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date