- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Casing and Tubing Market Size | OCTG Industry Trends & Forecast | 5.8% CAGR

Global Casing and Tubing Market Size, Share & Industry Analysis By Product Type (Casing, Tubing), By Material Grade (Carbon Steel – API and Proprietary High-Strength Grades, Corrosion-Resistant Alloy – Chrome, Duplex Stainless & Nickel Alloy, High-Strength Specialty Alloy Grades), By Connection Type (API Round Thread & Buttress Thread, Premium Threaded Connections), By Application (Onshore Drilling, Offshore Drilling – Deepwater & Ultra-Deepwater) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Trends & Forecast 2025–2034

Report Overview

| Market Size (2025) | Forecast (2034) | CAGR | Lead Region (2025) |

| USD 18.6 Billion | USD 30.8 Billion | 5.8% | Middle East |

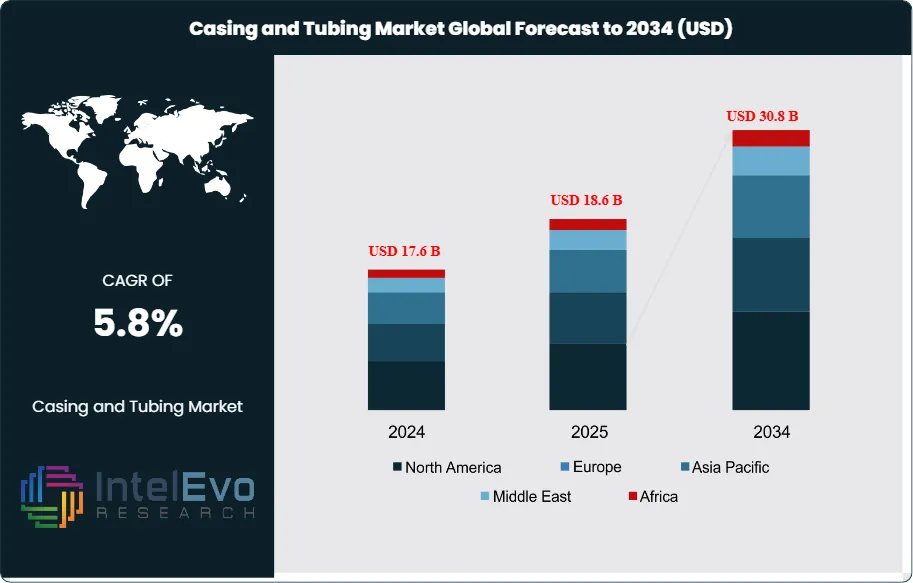

The Global Casing and Tubing Market was valued at USD 18.6 Billion in 2025 and is expected to reach USD 30.8 Billion by 2034, growing at a CAGR of 5.8% during the forecast period 2025–2034. The casing and tubing market sits at the intersection of oil and gas upstream capital expenditure cycles, steel manufacturing capacity, and advances in metallurgical and connection technology, supplying the tubular products that provide structural integrity to wellbores drilled in increasingly challenging pressure, temperature, and corrosive environments worldwide. Casing strings isolate productive formations from groundwater aquifers, provide mechanical support to the wellbore, and enable the controlled management of wellbore pressure during drilling and completion operations. Tubing strings transport produced hydrocarbons to surface, deliver injection fluids to reservoir intervals, and serve as the conduit for well intervention and workover operations throughout the productive life of oil and gas wells.

Get More Information about this report -

Request Free Sample ReportDemand forces driving the casing and tubing market in 2025 include sustained global upstream capital expenditure recovery following the trough of the 2020–2021 downturn, with international oil company upstream spending estimated at USD 420 Billion in 2025 and growing at approximately 6.2% annually. The structural shift toward deeper, longer, and more technically demanding wells in offshore deepwater, ultra-deepwater, and onshore tight oil and gas reservoirs is increasing tubular tonnage per well and intensifying demand for premium threaded connections that deliver seal integrity and mechanical performance in high-pressure high-temperature and sour service environments. Horizontal well programs in North American unconventional plays require casing and tubing volumes significantly greater than vertical well equivalents, with average horizontal tight oil well casing consumption exceeding 350 metric tons of tubular product per well in 2025. Supply-side dynamics reflect competitive production from Russian, European, Japanese, and Chinese tubular manufacturers whose combined capacity significantly exceeds global demand, creating structural pricing pressure that constrains market revenue growth relative to volume growth.

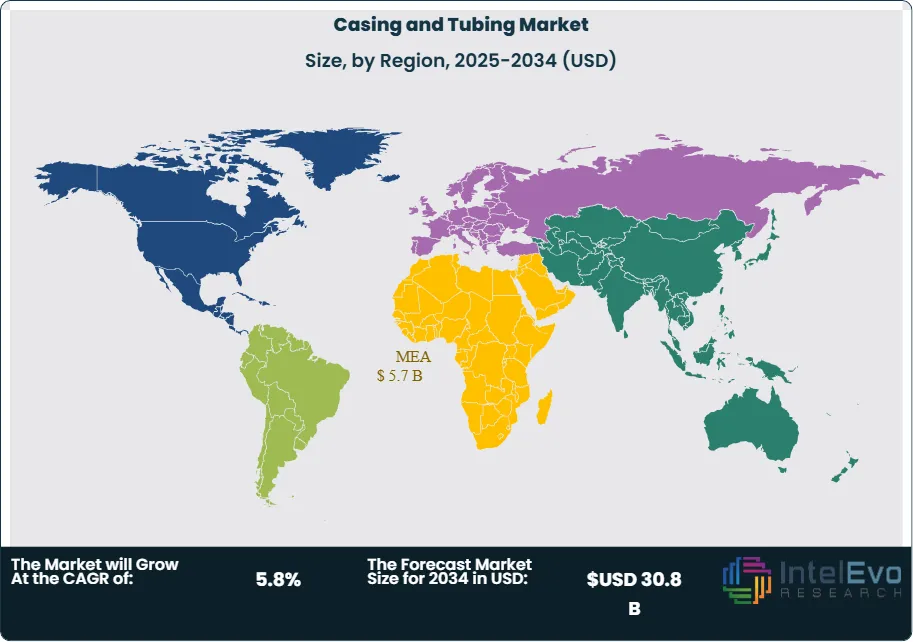

Regulatory influences on the casing and tubing market include evolving wellbore integrity standards, API Spec 5CT and ISO 11960 product specifications that govern base material properties and dimensional tolerances, and premium connection qualification requirements under ISO 13679 that establish the testing protocols manufacturers must satisfy to supply premium thread products to technically demanding well programs. Environmental regulations addressing wellbore integrity and casing leakage are tightening in North America, Europe, and Australia, requiring operators to use casing and tubing products certified to higher integrity standards for wells near groundwater resources and in areas with elevated regulatory scrutiny. Risk factors include steel input cost volatility driven by iron ore and coking coal price cycles, the concentration of tubular manufacturing capacity in Russia and China creating geopolitical supply chain risk for Western operators, and the potential long-term displacement of hydrocarbon well drilling by energy transition investment that could dampen casing and tubing market growth in the outer years of the forecast period. The Middle East leads the casing and tubing market with a 30.6% share at USD 5.7 Billion in 2025, reflecting intensive drilling programs across Saudi Arabia, Iraq, UAE, and Kuwait.

, By Material Grade (Carbon Steel – API and Proprietary High-Strength Grades, Corrosion-Resistant Alloy – Chrome, Duplex Stainless & Nickel Alloy, High-Strength Specialty Alloy Grades), By Connection Type (API Round Thread & Buttress Thread, Premium Threaded Connections), By Application (Onshore Drilling, Offshore Drilling – Deepwater & Ultra-Deepwater) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global casing and tubing market was valued at USD 18.6 Billion in 2025 and is projected to reach USD 30.8 Billion by 2034, registering a CAGR of 5.8% during the forecast period 2025–2034, driven by deepwater drilling expansion, rising Middle East national oil company drilling programs, and growing horizontal well tubular consumption in North American unconventional plays.

- Segment Dominance (By Product Type): Casing is the dominant product type in the casing and tubing market with a 62.4% share in 2025 at USD 11.6 Billion, reflecting the multi-string well architecture of modern oil and gas wells that requires conductor, surface, intermediate, and production casing strings of varying diameter and grade for every well drilled.

- Segment Dominance (By Grade): Carbon steel grades dominate the casing and tubing market by material with a 74.8% share in 2025 at USD 13.9 Billion, as the standard API grades H-40 through P-110 and proprietary high-strength grades serve the large-volume conventional and unconventional drilling programs that account for the majority of global well count.

- Driver: Global upstream oil and gas capital expenditure reached USD 420 Billion in 2025 and is growing at 6.2% annually, with horizontal tight oil and gas well programs consuming an average of 350 metric tons of casing and tubing per well and deepwater programs consuming 600–1,200 metric tons per well, sustaining above-average tubular demand intensity per drilling dollar spent.

- Restraint: Structural manufacturing overcapacity in the global casing and tubing market, where combined global production capacity exceeds demand by an estimated 18–22% in 2025, creates persistent pricing pressure that suppresses market revenue growth to below volumetric growth rates, particularly in the commodity API-grade casing segment where Chinese and Russian producers compete aggressively on price.

- Opportunity: Corrosion-resistant alloy and premium connection casing and tubing products for high-pressure high-temperature and sour service wells represent a USD 6.4 Billion addressable opportunity within the casing and tubing market by 2034. CRA tubular penetration covers less than 12% of technically eligible high-pressure high-temperature and sour service well candidates globally as of 2025, indicating significant room for premium product adoption expansion.

- Trend: Digital thread inspection and tubular tracking technologies, incorporating AI-powered surface defect detection, RFID-tagged tubular asset management, and cloud-based thread condition monitoring, are being adopted by approximately 28% of major offshore drilling programs in 2025, reducing tubular failure rates by 35–45% and creating a new premium service revenue stream for tubular suppliers with integrated digital inspection capabilities.

- Regional Analysis: The Middle East leads the global casing and tubing market with a 30.6% share in 2025, equivalent to USD 5.7 Billion, driven by Saudi Aramco, ADNOC, Kuwait Oil Company, and Iraq's state operator drilling programs that collectively account for one of the world's highest concentrations of active drilling rigs and annual well counts.

Casing And Tubing Market — Competitive Landscape

The global casing and tubing market is moderately consolidated, with the top four producers, Tenaris, Vallourec, TMK, and U.S. Steel Tubular Products, collectively accounting for approximately 46–50% of global market revenue in 2025. Competition is primarily driven by a combination of product technology, premium connection performance credentials, and geographic supply presence, with pricing as a secondary driver in the commodity API-grade segment. The competitive landscape experienced material shifts between 2024 and 2026 as Tenaris expanded North American capacity, Vallourec reinforced long-term supply commitments with major European and African operators, and Chinese producers accelerated market share gains in Middle East and Asian commodity tubular segments. Premium connection technology, measured by ISO 13679 CAL IV certification status, increasingly determines vendor selection for high-value deepwater and HPHT well programs.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

|---|---|---|---|---|---|

| Tenaris S.A. | Luxembourg | Leader | TenarisHydril Premium Connections | Global | Acquired IPSCO Tubulars capacity expansion, Jan 2025 |

| Vallourec S.A. | France | Leader | VAM Premium Connections | Europe / MEA / LatAm | Long-term supply agreement with TotalEnergies, Feb 2025 |

| TMK Group | Russia | Leader | TMK UP Series Threads | Europe / MEA / CIS | Expanded Seversky pipe capacity by 18%, Mar 2025 |

| U.S. Steel (Tubular Products) | USA | Leader | API Casing & Tubing Strings | North America | Acquired Wheeling-Nippon Steel assets, Dec 2024 |

| Nippon Steel Corp. | Japan | Challenger | NS-CC Premium Connections | Asia Pacific / Global | New premium thread facility, Kyushu, Apr 2025 |

| ArcelorMittal Tubular Products | Luxembourg | Challenger | ArcelorMittal OCTG Range | Europe / North America | Expanded Mexican mill output, Jun 2025 |

| NOV Inc. (Grant Prideco) | USA | Challenger | XT-M Drill Pipe & Casing | North America / Global | Launched AI thread inspection system, Aug 2025 |

| Evraz Group | UK | Challenger | EVRAZ OCTG Casing Line | North America / CIS | Commissioning new Rocky Mountain mill, Oct 2025 |

| SeAH Steel Holdings | South Korea | Niche Player | OCTG Premium Tubing | Asia Pacific | Supply contract with Saudi Aramco, Nov 2025 |

| Sandvik AB (Tube Division) | Sweden | Niche Player | Sanduvik Corrosion-Resistant Tubes | Europe / Global | New CRA alloy tubing plant, Jan 2026 |

Segmentation Analysis

The casing and tubing market segmentation analysis covers four key dimensions: By Product Type, By Material Grade, By Connection Type, and By Application. Each dimension reveals distinct specification requirements, pricing dynamics, and competitive positioning patterns that define the global casing and tubing market through 2034.

By Product Type

Casing is the dominant product type in the casing and tubing market, accounting for 62.4% of product type segment revenue in 2025 at USD 11.6 Billion. Casing strings are deployed in multiple concentric configurations within every oil and gas well, beginning with the large-diameter conductor casing that provides structural support at the wellhead, through surface casing that protects freshwater aquifers, intermediate casing strings that isolate abnormal pressure zones, and production casing that provides the pressure-containing conduit from the producing reservoir to surface. The casing market is further differentiated by outer diameter range, with large-diameter casing above 9.625 inches used for conductor and surface strings and smaller diameters from 4.5 to 9.625 inches used for intermediate and production applications. The volume and grade specifications of casing programs vary substantially by well type: a standard vertical onshore well in the Middle East may require 200–350 metric tons of casing across all strings, while a Gulf of Mexico deepwater well with multiple intermediate strings and an extended-reach horizontal completion can require 800–1,400 metric tons of casing product. Casing demand growth is closely correlated with global rig count and wells-drilled metrics, which are projected to grow at 4.8% annually through 2034.

Tubing accounts for 37.6% of product type segment revenue in 2025 at USD 7.0 Billion. Production tubing is run inside the production casing string and provides the flow conduit from the producing reservoir interval to the surface production facilities, operating under the combined mechanical loads of hydrostatic pressure, reservoir fluid pressure, and thermal expansion through the full depth of the well. Tubing sizes typically range from 2.375 inches to 4.5 inches outer diameter in standard configurations, with larger diameter tubing used in high-rate gas producers and horizontal well completions. The tubing market includes both new completions strings for newly drilled wells and workover tubing replacements for existing wells whose original tubing strings have corroded, worn, or suffered mechanical damage, providing a demand base that is somewhat less correlated with the new well drilling cycle than the casing segment. Premium corrosion-resistant tubing for sour service and high-CO2 wells, coiled tubing for well intervention, and expandable tubulars for contingency casing programs represent the higher-margin sub-segments within the tubing product category.

By Material Grade

Carbon steel grades dominate the casing and tubing market material segment with a 74.8% share in 2025 at USD 13.9 Billion. The American Petroleum Institute's Specification 5CT establishes the standard carbon steel grades used in oil country tubular goods, ranging from H-40 and J-55 grades used in shallow low-pressure wells through N-80, L-80, C-90, T-95, P-110, and Q-125 grades for progressively higher-strength and sour service applications. Carbon steel API and proprietary high-strength grades are the workhorses of the global casing and tubing market, supplying the volume demand from onshore conventional drilling programs in the Middle East, Russia, and North America where formation fluids are generally non-corrosive and reservoir pressures do not exceed the mechanical ratings of standard API grades. Premium proprietary carbon steel grades developed by Tenaris, Vallourec, and Nippon Steel for ultra-deep high-pressure well programs offer yield strengths above 125,000 pounds per square inch that exceed the standard API grade range, addressing technically demanding well programs without the cost premium of corrosion-resistant alloy materials.

Corrosion-resistant alloy grades, including chrome alloys from 9% to 13% Cr, duplex and super-duplex stainless steels, and nickel-based alloys such as Inconel and Hastelloy variants, represent 16.4% of material grade revenue in 2025 at USD 3.1 Billion. CRA casing and tubing products are deployed in wells containing significant concentrations of hydrogen sulfide, carbon dioxide, or chloride ions that would rapidly corrode carbon steel tubulars and cause well integrity failures. Deepwater gas wells with high CO2 partial pressures, sour gas production in the Middle East and North Africa, and geothermal wells are the primary CRA consumption markets. The CRA segment commands significant price premiums over carbon steel, with 13% Cr tubing priced at 3–4 times the equivalent carbon steel product and duplex stainless steel tubing at 6–8 times the carbon steel equivalent. High-strength specialty alloy grades for extreme pressure and temperature applications represent the remaining 8.8% of material grade revenue at USD 1.6 Billion in 2025.

By Connection Type

API round thread and buttress thread connections are the dominant connection type category in the casing and tubing market, accounting for 52.6% of connection type segment revenue in 2025 at USD 9.8 Billion. API connections are defined by American Petroleum Institute Specification 5B and provide standardized thread forms, tolerances, and makeup parameters that enable interchangeability between manufacturers and are universally accepted for conventional well programs in non-critical pressure and temperature environments. The API connection segment is the most price-competitive segment of the casing and tubing market, with manufacturers from China, Russia, South Korea, and Brazil producing API-specification products that compete primarily on delivered price. API connections remain the standard specification for the majority of onshore well programs globally, including the large-volume conventional drilling programs in the Middle East, Russia, and Africa that account for the majority of global well count.

Premium threaded connections represent 47.4% of connection type segment revenue in 2025 at USD 8.8 Billion. Premium connections use proprietary thread profiles, metal-to-metal sealing systems, and torque shoulder geometries developed by manufacturers such as Tenaris (Hydril series), Vallourec (VAM series), and Nippon Steel (NS-CC series) to deliver seal integrity and mechanical performance under gas-tight conditions, high tensile loads, and elevated temperature that API connections cannot reliably achieve. The premium connection segment is growing faster than the overall casing and tubing market, driven by the increasing proportion of deepwater, high-pressure high-temperature, and sour service wells in the global drilling mix that technically mandate premium connection performance credentials. ISO 13679 CAL IV certification, the highest level of premium connection qualification testing, is required by most major international and national oil companies for wells meeting specified pressure and temperature threshold criteria, effectively mandating premium connections for a growing share of global well programs.

By Application

Onshore drilling applications represent the largest segment of the casing and tubing market by application, accounting for 58.4% of application segment revenue in 2025 at USD 10.9 Billion. The onshore segment encompasses the massive conventional drilling programs of Saudi Arabia, Iraq, Kuwait, UAE, Russia, and Iran, the horizontal unconventional tight oil and gas programs of North America's Permian Basin, Eagle Ford, Bakken, and Marcellus plays, and the growing onshore drilling activity across Africa, Southeast Asia, and Latin America. North American unconventional drilling programs represent the most tubular-intensive sub-segment of onshore applications, as horizontal wells with lateral lengths averaging 10,000–14,000 feet require substantially greater casing and liner tonnage per well than comparable vertical well programs. Middle East conventional onshore programs are characterized by high-volume standardized API-grade tubular procurement on long-term supply frameworks that make them the primary volume demand source for commodity casing products globally.

Offshore drilling applications account for 41.6% of casing and tubing market revenue in 2025 at USD 7.7 Billion. The offshore segment, while smaller by volume than onshore, generates disproportionate revenue due to the premium connection, high-strength grade, and CRA material requirements of deepwater and HPHT offshore well programs. Gulf of Mexico deepwater, Brazilian pre-salt Santos Basin, Norwegian Continental Shelf, and West African deepwater blocks drive the premium offshore tubular demand that commands the highest per-ton pricing in the casing and tubing market. Deepwater wells typically require 5–8 distinct casing strings of varying diameter and specification, with premium connections mandatory on all strings below the mudline, CRA tubing mandatory for CO2-rich gas producers, and ultra-high-strength casing grades required for pressure containment in formations exceeding 15,000 pounds per square inch shut-in wellhead pressure. The offshore segment is projected to grow at a CAGR of 7.2% through 2034, outpacing the overall market rate.

Regional Analysis

Middle East Casing and Tubing Market

The Middle East leads the global casing and tubing market with a 30.6% share in 2025, equivalent to USD 5.7 Billion. Saudi Arabia is the dominant country market, with Saudi Aramco operating the world's largest single oil company drilling program and consuming estimated annual casing and tubing volumes exceeding 600,000 metric tons across its onshore and offshore well programs. Aramco's sustained capital expenditure program targeting crude oil capacity maintenance and gas expansion in the Jafurah tight gas play creates a structurally large and predictable tubular demand base that the leading global producers compete intensively to supply through long-term framework agreements. The Jafurah gas development program alone represents a multi-decade drilling campaign across thousands of horizontal wells that will consume substantial premium connection casing and CRA tubing volumes for sour gas applications.

Iraq is the second-largest Middle East casing and tubing market, with international oil company operators under technical service agreements including BP, ExxonMobil, and TotalEnergies sustaining active drilling campaigns in the Basra fields that generate significant annual tubular procurement volumes. The UAE is a growing market, with ADNOC's drilling expansion program across its offshore carbonate and onshore gas reservoir developments increasing tubular demand year on year. Kuwait Oil Company and Qatar Energy's LNG expansion drilling programs contribute additional Middle East casing and tubing market volume. The region's demand is characterized by high-volume standardized API-grade casing procurement with selective premium connection requirements for HPHT and sour service wells. The Middle East casing and tubing market is projected to grow at a CAGR of 6.4% through 2034, underpinned by national oil company production capacity maintenance investment.

North America Casing and Tubing Market

North America holds a 26.8% share of the global casing and tubing market in 2025, equivalent to USD 4.99 Billion. The United States is the dominant country market, with casing and tubing demand concentrated in the Permian Basin, Eagle Ford, Bakken, Marcellus, and Haynesville unconventional plays where horizontal well programs drive the world's highest tubular intensity per active rig. The U.S. tight oil sector consumes an estimated 3.8 Million metric tons of OCTG annually in 2025, with average casing and tubing consumption per well of 330–380 metric tons across a horizontal well population that sustains active rig counts of 550–700 units in major unconventional plays. Deepwater Gulf of Mexico operations add a premium-connection and CRA-grade demand layer above the unconventional base, with major operators including Shell, Chevron, and BP specifying premium tubular packages for their deepwater development and exploration programs.

The United States maintains trade protection measures on imported OCTG through antidumping and countervailing duty orders on products from multiple countries including China, South Korea, India, and Turkey, which provide a degree of pricing support for domestic manufacturers including U.S. Steel Tubular Products, Evraz Rocky Mountain Steel, and Ipsco Tubulars. Canada contributes approximately 16% of North American casing and tubing market revenue, with the Alberta oil sands in-situ operations, Deep Basin tight gas development, and Montney unconventional play driving sustained tubular demand. Mexico's Pemex and private sector operators represent a modest but growing casing and tubing market as shallow offshore and onshore conventional drilling activity proceeds. North America is projected to grow at a CAGR of 5.4% through 2034, with tight oil well productivity improvement potentially moderating rig count growth but sustaining tubular intensity per well.

Asia Pacific Casing and Tubing Market

Asia Pacific holds a 22.4% share of the global casing and tubing market in 2025, equivalent to USD 4.2 Billion. China is the dominant country market, with PetroChina and SINOPEC operating extensive onshore conventional and unconventional drilling programs in the Tarim Basin, Sichuan Basin, Ordos Basin, and Xinjiang that generate the world's second-largest national tubular consumption base after the United States. China's domestic tubular manufacturers, including Baosteel, TPCO (Tianjin Pipe), and Hengyang Valin Steel Tube, supply the majority of domestic OCTG demand at competitive prices, with surplus capacity providing the export volume that Chinese producers deploy in Middle East, Latin American, and Southeast Asian markets. China's deep shale gas development programs in the Sichuan Basin require premium connection casing and high-strength grades for horizontal wells at depths exceeding 4,500 meters with complex geological pressure regimes.

Australia represents a growing Asia Pacific casing and tubing market, with Woodside Energy, Santos, and Beach Energy conducting offshore and onshore drilling programs across the Carnarvon Basin, Browse Basin, and Cooper Basin that consume premium tubular products. India is a meaningful contributor through ONGC and Oil India's well programs in Rajasthan, Assam, and the Krishna-Godavari deepwater Basin, with the Indian government's push to reduce import dependency driving increased domestic drilling intensity. South Korea's KOGAS and POSCO contribute both as consumers and as tubular manufacturers supplying regional markets through SeAH Steel Holdings. Asia Pacific is projected to grow at a CAGR of 5.6% through 2034, with Chinese unconventional gas development and Australian LNG well programs providing sustained demand growth.

Europe Casing and Tubing Market

Europe accounts for 11.8% of the global casing and tubing market in 2025, equivalent to USD 2.2 Billion. Norway leads the European segment, with Equinor, Aker BP, and Vår Energi conducting sustained exploration, appraisal, and development drilling programs on the Norwegian Continental Shelf that require premium connection casing, CRA tubing for CO2-rich gas condensate wells, and high-strength grades for HPHT formations in the Central North Sea and Barents Sea. The Norwegian market demands the highest technical specification tubular products of any European sub-market, with Norwegian Petroleum Safety Authority regulatory requirements effectively mandating premium connections and CRA materials for specified high-pressure high-temperature well categories. Vallourec's VAM premium connection products maintain a strong commercial position in the Norwegian market, with long-term supply relationships with Equinor and Aker BP providing revenue visibility.

The United Kingdom contributes through North Sea drilling programs operated by Harbour Energy, Repsol Sinopec, and independent operators who maintain reduced but sustained levels of exploration and production drilling activity. Romania and Poland represent smaller but growing European casing and tubing markets as onshore conventional and tight gas drilling programs in the Pannonian Basin and Polish Lowlands proceed with EU energy security investment support. Russia remains a significant tubular producer and consumer, though Western sanctions have redirected TMK Group's export focus toward Middle East, African, and Asian markets rather than Western European customers. Europe is projected to grow at a CAGR of 4.2% through 2034, reflecting a mature North Sea basin with moderate growth from Central and Eastern European onshore programs.

Latin America Casing and Tubing Market

Latin America holds an 8.4% share of the global casing and tubing market in 2025, totaling USD 1.6 Billion. Brazil is the dominant country market, with Petrobras operating the world's technically most demanding deepwater casing and tubing program in the pre-salt Santos Basin where extreme water depth, reservoir pressure, and high CO2 content create requirements for premium connection systems, ultra-high-strength casing grades, and CRA tubing that command premium pricing. Petrobras's annual tubular procurement is estimated at over 200,000 metric tons of casing and tubing in 2025, with a significant proportion specified to premium or CRA standards that generate above-average revenue per ton. Brazil's pre-salt well architecture, incorporating multiple concentric casing strings through the evaporite salt interval, generates among the highest casing tonnage per well of any global deepwater well program.

Colombia contributes through Ecopetrol and international operator partnerships in the Llanos Basin onshore oil program and emerging offshore deepwater exploration. Argentina's Vaca Muerta unconventional play represents a growing casing and tubing demand source as YPF and international operators including Shell and TotalEnergies accelerate horizontal well drilling programs that could generate substantial premium connection and high-strength grade tubular demand. Mexico's drilling program under Pemex and private operators provides conventional tubular demand across shallow offshore and onshore programs in the Burgos Basin, Veracruz, and shallow water Campeche Bay. Latin America is projected to grow at a CAGR of 6.8% through 2034, with Argentina's Vaca Muerta development and Petrobras's sustained pre-salt program providing the primary growth engines.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Casing

- Tubing

By Material Grade

- Carbon Steel (API and Proprietary High-Strength Grades)

- Corrosion-Resistant Alloy (Chrome, Duplex Stainless, Nickel Alloy)

- High-Strength Specialty Alloy Grades

By Connection Type

- API Round Thread and Buttress Thread

- Premium Threaded Connections

By Application

- Onshore Drilling

- Offshore Drilling (Deepwater and Ultra-Deepwater)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 18.6 B |

| Forecast Revenue (2034) | USD 30.8 B |

| CAGR (2025-2034) | 5.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Casing, Tubing), By Material Grade (Carbon Steel (API and Proprietary High-Strength Grades), Corrosion-Resistant Alloy (Chrome, Duplex Stainless, Nickel Alloy), High-Strength Specialty Alloy Grades), By Connection Type (API Round Thread and Buttress Thread, Premium Threaded Connections), By Application (Onshore Drilling, Offshore Drilling (Deepwater and Ultra-Deepwater)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | TENARIS S.A., VALLOUREC S.A., TMK GROUP, U.S. STEEL (TUBULAR PRODUCTS DIVISION), NIPPON STEEL CORPORATION, ARCELORMITTAL TUBULAR PRODUCTS, NOV INC. (GRANT PRIDECO), EVRAZ GROUP, SEAH STEEL HOLDINGS, SANDVIK AB (TUBE DIVISION), TPCO (TIANJIN PIPE CORPORATION), BAOSTEEL GROUP (BAOSHAN IRON AND STEEL), HENGYANG VALIN STEEL TUBE CO., LTD., IPSCO TUBULARS INC., JFE STEEL CORPORATION, SUMITOMO CORPORATION (OCTG DIVISION), BENTELER STEEL / TUBE, METALCAM, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Material Grade (Carbon Steel – API and Proprietary High-Strength Grades, Corrosion-Resistant Alloy – Chrome, Duplex Stainless & Nickel Alloy, High-Strength Specialty Alloy Grades), By Connection Type (API Round Thread & Buttress Thread, Premium Threaded Connections), By Application (Onshore Drilling, Offshore Drilling – Deepwater & Ultra-Deepwater) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Trends & Forecast 2025–2034")

, By Material Grade (Carbon Steel – API and Proprietary High-Strength Grades, Corrosion-Resistant Alloy – Chrome, Duplex Stainless & Nickel Alloy, High-Strength Specialty Alloy Grades), By Connection Type (API Round Thread & Buttress Thread, Premium Threaded Connections), By Application (Onshore Drilling, Offshore Drilling – Deepwater & Ultra-Deepwater) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Trends & Forecast 2025–2034")

, By Material Grade (Carbon Steel – API and Proprietary High-Strength Grades, Corrosion-Resistant Alloy – Chrome, Duplex Stainless & Nickel Alloy, High-Strength Specialty Alloy Grades), By Connection Type (API Round Thread & Buttress Thread, Premium Threaded Connections), By Application (Onshore Drilling, Offshore Drilling – Deepwater & Ultra-Deepwater) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Casing and Tubing Market?

The Global Casing and Tubing Market was valued at USD 17.6 Billion in 2024 and is projected to reach USD 30.8 Billion by 2034, growing at a CAGR of 5.8% from 2026–2034. Explore market trends, OCTG demand drivers, upstream drilling activity, steel technology innovations, and competitive landscape.

Who are the major players in the Casing and Tubing Market?

TENARIS S.A., VALLOUREC S.A., TMK GROUP, U.S. STEEL (TUBULAR PRODUCTS DIVISION), NIPPON STEEL CORPORATION, ARCELORMITTAL TUBULAR PRODUCTS, NOV INC. (GRANT PRIDECO), EVRAZ GROUP, SEAH STEEL HOLDINGS, SANDVIK AB (TUBE DIVISION), TPCO (TIANJIN PIPE CORPORATION), BAOSTEEL GROUP (BAOSHAN IRON AND STEEL), HENGYANG VALIN STEEL TUBE CO., LTD., IPSCO TUBULARS INC., JFE STEEL CORPORATION, SUMITOMO CORPORATION (OCTG DIVISION), BENTELER STEEL / TUBE, METALCAM, Others

Which segments covered the Casing and Tubing Market?

By Product Type (Casing, Tubing), By Material Grade (Carbon Steel (API and Proprietary High-Strength Grades), Corrosion-Resistant Alloy (Chrome, Duplex Stainless, Nickel Alloy), High-Strength Specialty Alloy Grades), By Connection Type (API Round Thread and Buttress Thread, Premium Threaded Connections), By Application (Onshore Drilling, Offshore Drilling (Deepwater and Ultra-Deepwater))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date