- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global CBD Beverages Market Size & Forecast 2024–2034 | 22.5% CAGR

Global CBD Beverages Market Size, Share & Industry Analysis By Type (Hemp-Derived, Marijuana-Derived, Other Types), By Product Type (CBD Water, CBD Tea, CBD Coffee, CBD Energy Drinks, CBD Mocktails, CBD Alcoholic Drinks), By Grade (Pharmaceutical Grade, Food Grade), By Distribution Channel (Pharmaceutical Stores, Specialty Stores, Online Platforms), Regional Outlook, Competitive Landscape, Market Trends & Forecast 2025–2034

Report Overview

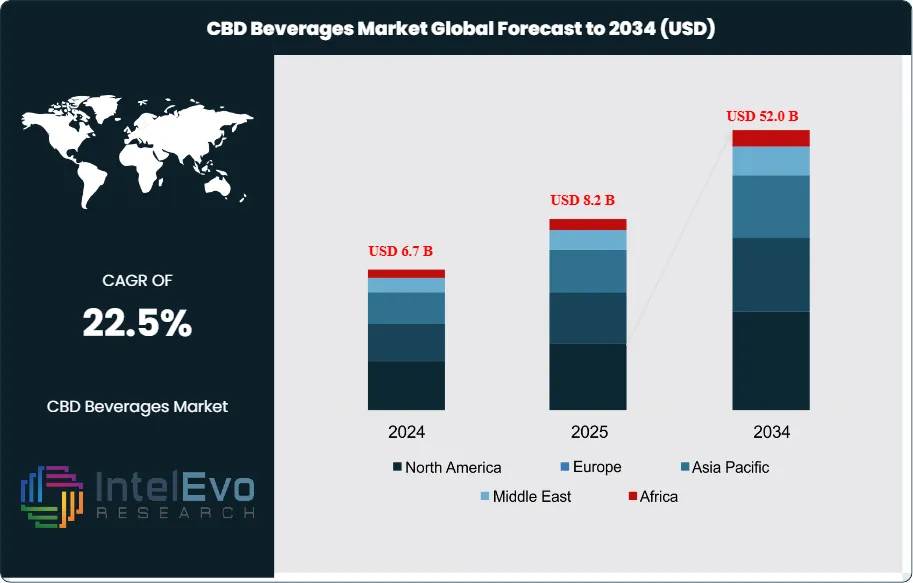

The CBD Beverages Market was valued at USD 6.7 Billion in 2024 and is projected to reach approximately USD 52.0 Billion by 2034. The market is estimated to grow to around USD 8.2 Billion in 2025. Based on projected expansion from 2026 onward, the industry is expected to register a compound annual growth rate (CAGR) of approximately 22.5% during 2026–2034.

Get More Information about this report -

Request Free Sample ReportCBD (cannabidiol) beverages use CBD oils or extracts to deliver measured intake in familiar formats such as sparkling waters, flavored teas, functional drinks, and select alcoholic offerings. Demand rises as consumers link CBD with wellness routines and everyday stress management. Product positioning increasingly centers on immunity support, weight management, and digestive comfort, even as claims remain constrained by local rules. This dynamic keeps brand messaging focused on “calm,” “balance,” and ingredient transparency, while innovation concentrates on taste masking and consistent dosing.

Growth reflects both demand pull and supply push. On the demand side, premiumization and convenience support higher price points, and ready-to-drink formats expand usage occasions beyond tinctures and gummies. On the supply side, wider hemp cultivation and improving extraction yields lower unit costs, supporting broader distribution. Water-soluble CBD, nanoemulsions, and microencapsulation improve bioavailability and stability, reducing separation and enabling clear beverages. Producers also use AI to optimize flavor systems, predict regional demand, and flag quality deviations, while automation tightens batch-to-batch dosage control and improves throughput in bottling and canning. Digital-first go-to-market models account for an estimated 35% of global sales in 2024, led by direct-to-consumer and marketplace channels, with rapid repeat purchasing in subscription programs.

Regulation remains the primary swing factor. Most markets enforce strict THC thresholds, labeling rules, and limits on health claims, while enforcement intensity varies by jurisdiction. Compliance costs rise as brands invest in third-party testing, traceability, and standardized certificates of analysis. Key risks include shifting guidance on CBD as a food ingredient, inconsistent product quality among smaller entrants, and reputational exposure from mislabeling. Regionally, North America leads with about 45% of 2024 revenue, supported by broad retail penetration and mature wellness purchasing. Europe holds roughly 28%, shaped by novel-food style approvals and conservative claims frameworks. Asia-Pacific represents near 20% but posts the fastest growth, with emerging investment hotspots in Australia, Japan, and Thailand as regulated wellness channels expand and local bottlers partner with ingredient specialists.

, By Product Type (CBD Water, CBD Tea, CBD Coffee, CBD Energy Drinks, CBD Mocktails, CBD Alcoholic Drinks), By Grade (Pharmaceutical Grade, Food Grade), By Distribution Channel (Pharmaceutical Stores, Specialty Stores, Online Platforms), Regional Outlook, Competitive Landscape, Market Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market expands at 23.5% CAGR, 2024-2034. It sustains scale-up momentum at estimated: 20.0% CAGR, 2024-2034.

- Segment Dominance : CBD mocktails lead product demand at estimated: 35.0% revenue share, 2024. They retain leadership at estimated: 3.5 billion USD, 2024.

- Segment Dominance: Pharmaceutical-grade CBD dominates grade mix at 74.6% revenue share, 2022. It maintains premium positioning at estimated: 60.0% revenue share, 2024.

- Driver: Wellness-led substitution lifts adoption at estimated: 55.0% of buyers citing health positioning, 2024. Regulatory easing accelerates commercialization at estimated: 10.0% increase in compliant SKUs, 2024.

- Restraint: Regulatory uncertainty elevates compliance risk at estimated: 15.0% of launches delayed, 2024. Formulation and potency variability increase quality failures at estimated: 8.0% of batches, 2024.

- Opportunity: Portfolio expansion grows addressable demand at estimated: 25.0% increase in new product introductions, 2024. Partnerships widen reach through pharmacy and retail networks at estimated: 12.0% uplift in distribution points, 2024.

- Trend: CBD beverages gain momentum as wellness routines scale at estimated: 30.0% year-over-year category growth, 2024. Brands improve taste and bioavailability using R&D and process optimization at estimated: 18.0% cost reduction per formulation cycle, 2024.

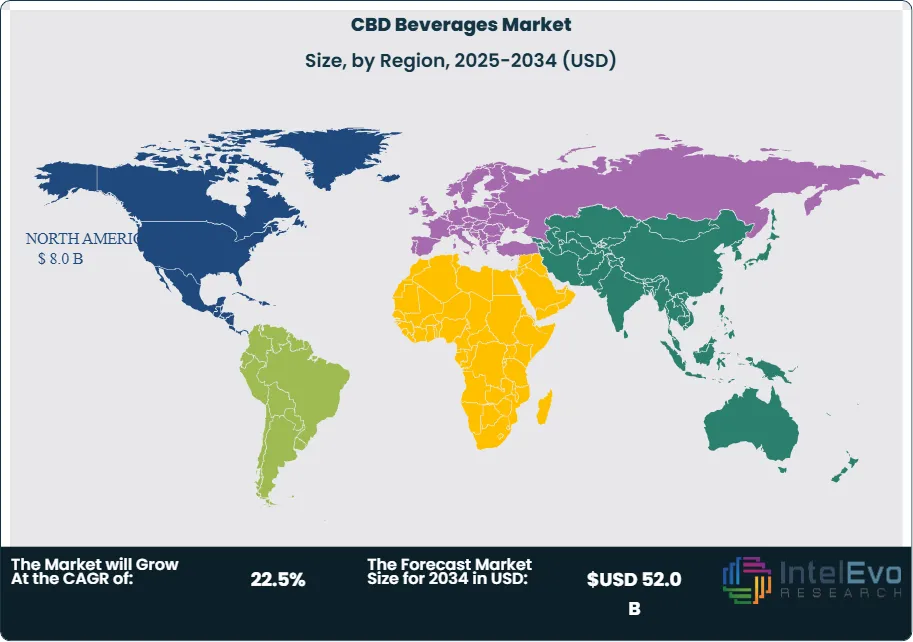

- Regional Analysis: North America leads global cannabis beverage revenue at 79.0% share, 2022. The region sustains growth intensity at estimated: 8.0 billion USD, 2024.

By Type

The global CBD beverages market, segmented by marijuana-derived, hemp-derived, and other sources, continues to show clear preference for hemp-derived CBD heading into 2025. Hemp-derived beverages accounted for approximately 56.5% of total revenue in 2022 and are expected to retain leadership through the forecast period. This dominance reflects favorable regulatory treatment in major economies, particularly following the legalization of industrial hemp with low THC thresholds. By 2025, hemp-derived products represent an estimated 58% to 60% of global CBD beverage revenues, supported by wider retail acceptance and fewer legal barriers.

Consumer demand remains anchored in perceived wellness benefits. Hemp-derived CBD is widely associated with anti-inflammatory, stress-management, and anxiety-relief properties, which aligns with rising demand for functional beverages. Manufacturers favor hemp inputs due to supply stability and compatibility with water-soluble formulations. Availability in oil, powder, and emulsion formats also supports product consistency across beverages such as sparkling water and ready-to-drink teas. These factors collectively sustain volume growth and cost efficiency across global supply chains.

Marijuana-derived CBD beverages maintain a smaller share, largely restricted to markets with mature recreational cannabis frameworks. Other sources remain niche and are primarily used in experimental or region-specific formulations, limiting their commercial scale.

By Application

Application trends show strong momentum for social and lifestyle consumption formats, particularly non-alcoholic alternatives. CBD mocktails continue to account for the largest application share, capturing more than one-third of total market revenue by 2025. These beverages replicate traditional cocktail experiences while eliminating alcohol-related calories and after-effects. Restaurants, lounges, and hospitality venues increasingly adopt CBD mocktails to meet demand for sober-curious offerings.

Functional daily-use beverages such as CBD water and CBD tea are gaining steady traction. These products support hydration and relaxation use cases and are commonly positioned for routine consumption rather than social occasions. CBD energy drinks and coffee occupy a smaller but growing segment, driven by formulations that balance stimulation with calm effects.

Adoption across foodservice channels accelerates application diversity. On-premise sales now account for an estimated 22% of CBD beverage consumption globally, supported by urban wellness trends and premium pricing strategies.

By End-Use

End-use demand remains concentrated in residential consumption, which represents the largest share of CBD beverage sales in 2025. Home consumption benefits from repeat purchasing behavior and subscription-based online models. Consumers increasingly integrate CBD beverages into daily routines for sleep support and stress reduction.

Commercial buildings, including hospitality and wellness centers, represent the fastest-growing end-use segment with double-digit annual growth. Gyms, spas, and boutique hotels actively incorporate CBD beverages into premium service offerings. Industrial end-use remains limited and primarily linked to workforce wellness programs in regulated markets.

By Region

North America continues to dominate the global CBD beverages market, accounting for approximately 79% of total revenue in 2022 and maintaining leadership in 2025. The United States and Canada benefit from established cannabis regulations and high consumer awareness. Recreational cannabis legalization across multiple U.S. states and federal-level research funding in Canada continue to support market expansion.

Europe represents a secondary growth region, with demand driven by the United Kingdom, Germany, and Switzerland. Asia Pacific shows early-stage momentum, led by Australia and select Southeast Asian markets, although regulatory clarity remains uneven. Latin America and the Middle East and Africa remain nascent, with growth tied closely to future policy developments and import regulations.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Marijuana-derived

- Hemp-derived

- Other Types

By Product Type

- CBD Water

- CBD Tea

- CBD Coffee

- CBD Mocktails

- CBD Energy Drinks

- CBD Alcoholic Drinks

- Other CBD products

By Grade

- Pharmaceutical Grade

- Food Grade

By Distribution Channel

- Pharmaceutical Store

- Specialty Store

- Online Platforms

- Other Distribution Channels

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.2 B |

| Forecast Revenue (2034) | USD 52.0 B |

| CAGR (2025-2034) | 22.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Type, Marijuana-derived, Hemp-derived, Other Types, By Product Type, CBD Water, CBD Tea, CBD Coffee, CBD Mocktails, CBD Energy Drinks, CBD Alcoholic Drinks, Other CBD products, By Grade, Pharmaceutical Grade, Food Grade, By Distribution Channel, Pharmaceutical Store, Specialty Store, Online Platforms, Other Distribution Channels |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Alkaline88, Aurora Cannabis Inc., Cannara, GW Pharmaceuticals plc., Ablis CBD, Canopy Growth Corporation, NewAge Inc., VIVO Cannabis Inc., The Cronos Group, CannTrust, Hexo, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Product Type (CBD Water, CBD Tea, CBD Coffee, CBD Energy Drinks, CBD Mocktails, CBD Alcoholic Drinks), By Grade (Pharmaceutical Grade, Food Grade), By Distribution Channel (Pharmaceutical Stores, Specialty Stores, Online Platforms), Regional Outlook, Competitive Landscape, Market Trends & Forecast 2025–2034")

, By Product Type (CBD Water, CBD Tea, CBD Coffee, CBD Energy Drinks, CBD Mocktails, CBD Alcoholic Drinks), By Grade (Pharmaceutical Grade, Food Grade), By Distribution Channel (Pharmaceutical Stores, Specialty Stores, Online Platforms), Regional Outlook, Competitive Landscape, Market Trends & Forecast 2025–2034")

, By Product Type (CBD Water, CBD Tea, CBD Coffee, CBD Energy Drinks, CBD Mocktails, CBD Alcoholic Drinks), By Grade (Pharmaceutical Grade, Food Grade), By Distribution Channel (Pharmaceutical Stores, Specialty Stores, Online Platforms), Regional Outlook, Competitive Landscape, Market Trends & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date