- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Cell Counting and Analysis Market Size, Share | CAGR 8.2%

Global Cell Counting and Analysis Market Size, Share Analysis By Product (Instruments, Consumables, Software, Services), By Technology (Flow Cytometry, Image-Based, Electrical Impedance, Fluorescence, High-Content Screening, Single-Cell, AI-Enabled), By End-User (Hospitals, Academics, Pharma & Biotech, CROs), By Application (Oncology, Drug Discovery, Diagnostics, Stem Cell, Cell & Gene Therapy) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

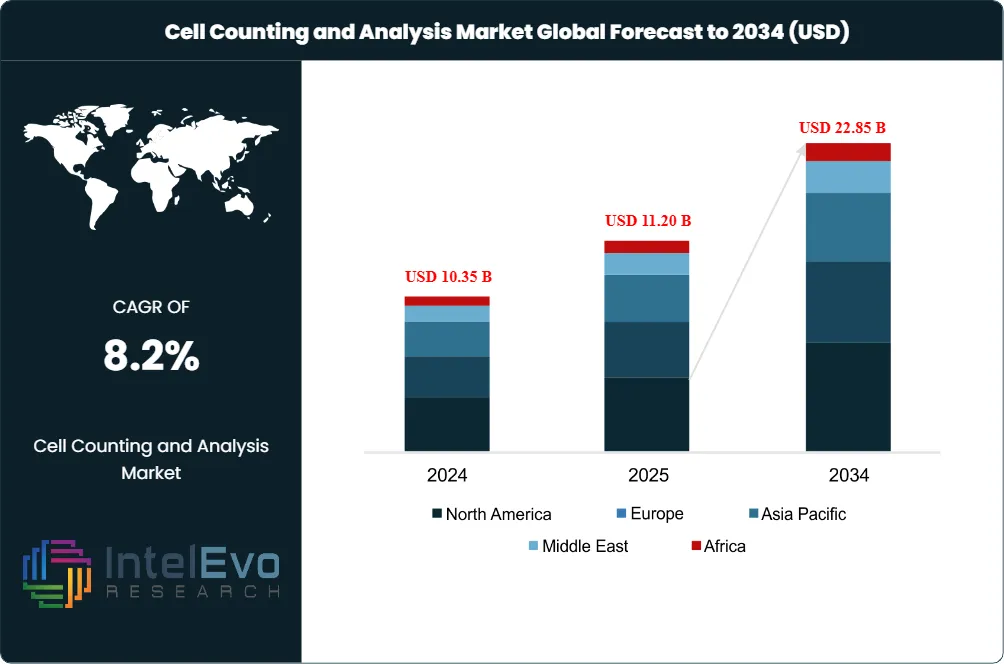

| USD 11.20 Billion | USD 22.85 Billion | 8.2% | North America, 39.7% |

The Cell Counting and Analysis Market was valued at USD 10.35 Billion in 2024 and USD 11.20 Billion in 2025. The market is projected to reach USD 22.85 Billion by 2034, expanding at a CAGR of 8.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 11.65 Billion over the analysis period. Demand expansion is anchored in the structural shift from manual hemocytometer methods to automated, image-based, and flow cytometry platforms across pharmaceutical manufacturing, clinical diagnostics, and academic research.

Get More Information about this report -

Request Free Sample ReportThe cell counting and analysis market is being shaped by the rapid scale-up of cell and gene therapy manufacturing. The U.S. FDA has issued release-criteria guidance requiring viability above 70% for autologous cell products such as Kymriah, with total nucleated cell viability above 85% for cord blood-derived HPC products. These thresholds make accurate, reproducible counting a regulatory-grade requirement rather than a research preference. ISO 20391-1:2018 and ISO 20391-2:2019, developed in collaboration with NIST and FDA, codify cell counting performance and statistical analysis. Vendors validating against ISO 20391-2 enjoy faster procurement cycles inside GMP environments.

Flow cytometry held a 44.6% technology share in 2024 and remains the analytical backbone for immunophenotyping, hematology, and rare-cell detection. New spectral platforms such as Beckman Coulter's CytoFLEX mosaic deliver up to 88 detection channels and nanoparticle resolution down to 80 nm, expanding panel design beyond traditional 10-color systems. Image-based cytometry is forecast to grow at an 8.3% CAGR through 2030, propelled by AI-driven cell segmentation that achieves throughput up to 180 times faster than manual counts per NIH-cited methodology.

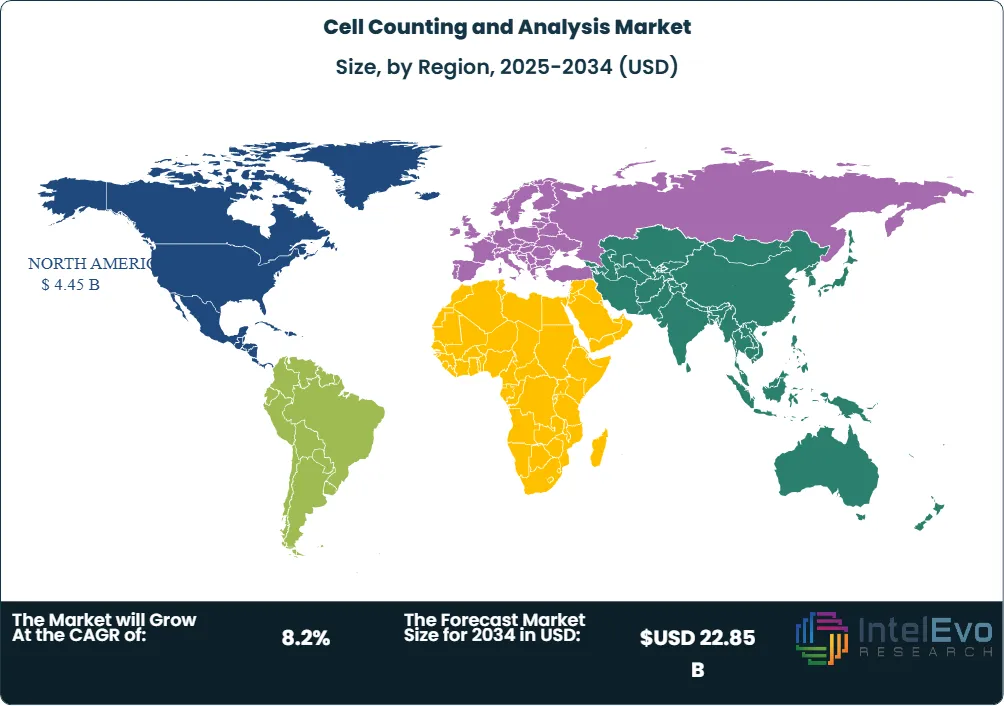

North America led the cell counting and analysis market with 39.7% share in 2025, equivalent to approximately USD 4.45 Billion in regional revenue. The region benefits from concentrated biopharma capacity, federal research funding through NIH, and rapid CAR-T commercialization. Asia Pacific is forecast to expand at the strongest 7.93% CAGR through 2030, driven by China's bioprocessing investments and India's expanding contract manufacturing footprint. Sartorius launched the Eveo Cell Therapy Platform in March 2026, modeled to enable approximately 350 autologous doses per year in cleanroom space that today yields 100, with manufacturing cost reductions approaching 90% in CAR-T workflows. Through 2034, vendors integrating AI image analysis, microfluidic chip cytometry, and single-use bioprocess sensors are positioned to capture the highest forecast-period growth.

Market Definition & Scope

The cell counting and analysis market is defined as the global commercial activity covering instruments, consumables, software, and services used to enumerate, characterize, and assess viability of biological cells in suspension or culture. The market includes automated cell counters, flow cytometers, hematology analyzers, image-based cytometers, spectrophotometers, microfluidic chip platforms, and the reagents, dyes, slides, and assay kits required to operate them.

This analysis includes products used for research, clinical diagnostics, bioprocessing, cell therapy quality control, and food and water testing. Excluded are upstream cell isolation systems, downstream cell sorting equipment dedicated to therapeutic manufacturing, mass cytometry consumables, and standalone microscopy products without cell-counting analytics. The cell counting and analysis market sits within the broader cell analysis instruments parent market, which industry analysis indicates approached USD 22.2 Billion in 2024, meaning cell counting represents approximately half of parent-market revenue. Adjacent markets including DNA/RNA quantification, single-cell sequencing library preparation, and high-content screening are tracked separately and excluded.

, By Technology (Flow Cytometry, Image-Based, Electrical Impedance, Fluorescence, High-Content Screening, Single-Cell, AI-Enabled), By End-User (Hospitals, Academics, Pharma & Biotech, CROs), By Application (Oncology, Drug Discovery, Diagnostics, Stem Cell, Cell & Gene Therapy) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The cell counting and analysis market grew from USD 11.20 Billion in 2025 toward a forecast value of USD 22.85 Billion by 2034 at an 8.2% CAGR.

- Segment Dominance: Consumables and accessories captured 55.4% revenue share in 2025, anchored by recurring reagent and assay-kit consumption.

- Segment Dominance: Research applications accounted for 40.6% of revenue in 2025, led by oncology, immunology, and stem-cell programs.

- Driver: Cell and gene therapy commercialization is the primary driver, with FDA-mandated viability thresholds above 70% for autologous products elevating counting from research to QC-grade.

- Restraint: Capital cost is the principal constraint; spectral flow cytometers can exceed USD 500,000, with annual service contracts adding 10 to 15% of purchase price.

- Opportunity: Image-based cytometry represents the largest forecast-period opportunity at an 8.3% CAGR through 2030, contributing meaningfully to the USD 11.65 Billion absolute dollar gain.

- Trend: AI-enabled image analysis is now standard in new instrument launches, delivering enumeration speedups up to 180 times faster than manual hemocytometers per NIH-published benchmarks.

- Regional: North America led with 39.7% share in 2025 equivalent to approximately USD 4.45 Billion, while Asia Pacific is the fastest-growing region at 7.93% forecast CAGR.

Key Insights Summary

- More than 210,000 automated cell counters were deployed across research labs, hospitals, and biopharma facilities by year-end 2024, per industry installed-base estimates compiled from vendor disclosures.

- The U.S. FDA mandates a minimum 70% viability for tisagenlecleucel (Kymriah) cell therapy products, with dose specifications of 0.2 to 5.0 x 10^6 transduced viable T cells per kg in patients weighing 50 kg or less.

- Beckman Coulter's CytoFLEX mosaic Spectral Detection Module, released in March 2025, delivers up to 88 detection channels and detects nanoparticles down to 80 nm.

- ISO 20391-1:2018 and ISO 20391-2:2019, developed by NIST in collaboration with FDA, are the recognized international standards for cell counting performance and statistical validation.

- Sartorius Stedim's ambr miniature bioreactors achieved viable cell density of 125 x 10^6 cells/mL while reducing media consumption by 87%, intensifying demand for in-situ viable cell density monitoring.

- Sartorius launched the Eveo Cell Therapy Platform on March 16, 2026, modeled to enable approximately 350 autologous doses per year in cleanroom footprint that currently yields 100 doses.

- Flow cytometry held 44.6% technology revenue share in 2024 and remains the backbone of clinical immunophenotyping per industry-wide installed-base data.

Competitive Landscape Overview

The cell counting and analysis market is moderately consolidated, with the top four suppliers controlling an estimated 42 to 48% of 2025 global revenue and the top ten accounting for approximately 65%. Danaher (Beckman Coulter), Thermo Fisher Scientific, Becton Dickinson, and Merck KGaA dominate across multiparametric flow cytometry and automated counting, supported by global service networks, broad reagent catalogs, and validated GMP-compliant workflows. Sartorius and Corning hold strong positions in single-use bioprocess monitoring, while Sysmex Corporation leads in clinical hematology analyzers. Compact image-based counters from NanoEnTek, Logos Biosystems, ChemoMetec, and DeNovix carve sustainable niches in academic and biotech laboratories.

Competitive differentiation centers on workflow integration. Vendors are pairing instruments with informatics platforms so users can archive raw FCS files, AI-generated morphometric features, and batch metadata in a single cloud environment. The competitive evolution is shifting from hardware specification toward software orchestration and consumables continuity. Strategic partnerships such as Becton Dickinson's collaboration with Biosero for robotic flow cytometry integration, and Merck's September 2025 MoU with Siemens to digitize life-sciences manufacturing, are expanding share-of-wallet by reducing operator labor and standardizing run-to-run variability. New entrants are concentrated in microfluidic and AI software segments rather than benchtop hardware.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product / Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Thermo Fisher Scientific | USA | Leader | Invitrogen Countess 3, Attune NxT | North America, Europe | Apr 2026 launched integrated cell line development platform |

| Danaher (Beckman Coulter) | USA | Leader | CytoFLEX mosaic, Vi-CELL BLU | North America, Asia Pacific | Mar 2025 launched CytoFLEX mosaic Spectral Detection Module |

| Becton, Dickinson and Company | USA | Leader | FACSDiscover S8, FACSLyric | North America, Europe | Oct 2025 acquired imaging-technology biotech firm |

| Merck KGaA | Germany | Leader | Scepter, Muse Cell Analyzer | Europe, North America | Sep 2025 signed digitization MoU with Siemens AG |

| Sartorius AG | Germany | Challenger | ambr, Eveo Cell Therapy Platform | Europe, North America | Mar 2026 launched Eveo Cell Therapy Platform |

| Sysmex Corporation | Japan | Challenger | XN-1000 Hematology Analyzer | Asia Pacific, Europe | Q4 2024 received FDA 510(k) for XN-1000 |

| Bio-Rad Laboratories | USA | Challenger | TC20 Plus, ddSEQ Single-Cell | North America, Europe | Q4 2024 launched TC20 Plus Automated Cell Counter |

| Agilent Technologies | USA | Challenger | BioTek Cytation, Lionheart | North America, Asia Pacific | Continued BioTek portfolio integration through 2025 |

| ChemoMetec A/S | Denmark | Niche Player | NucleoCounter NC-202 | Europe, Asia Pacific | Q1 2025 appointed new CEO for global expansion |

| DeNovix Inc. | USA | Niche Player | CellDrop FLi, CellDrop BF | North America, Europe | Aug 2024 launched CellDrop FLi Automated Cell Counter |

Segmentation Analysis

The cell counting and analysis market is segmented by product, technology, application, and end-user, each producing distinct competitive and growth dynamics across the forecast period.

By Product

The cell counting and analysis market by product is split into consumables and accessories versus instruments, with consumables and accessories holding 55.4% revenue share in 2025 driven by routine, high-volume reorder cycles for reagents, microplates, sera, and assay kits. Single-use bioreactor adoption reinforces this pattern because every batch requires fresh sterile bags, tubing, and media supplements; Sartorius and Corning have built consumables-anchored revenue around their bioprocessing platforms. Reagent procurement also benefits from validated workflows because pharmaceutical buyers tend to lock in trypan-blue or fluorescent-dye SKUs once they pass qualification rather than re-validate alternatives.

The instruments segment, while smaller, is forecast to expand at a 7.7% CAGR to 2030, the strongest within the product taxonomy. Image-based cytometers and microfluidic chip platforms are displacing legacy benchtop counters as labs prioritize speed, reproducibility, and integration with electronic lab notebooks. Beckman Coulter's Vi-CELL BLU integrated with Sartorius Ambr 250 systems has become a reference workflow at major biopharma sites including Boehringer Ingelheim's Biberach facility, supporting cell-line development at viable densities exceeding 20 x 10^6 cells/mL. Decision criteria for instrument procurement now extend to ROI calculation and implementation timeline, with most labs expecting 18 to 30-month payback through reagent savings, throughput gains, and reduced operator-error rework.

By Technology

Flow cytometry held 44.6% revenue share in 2024 and continues to anchor multi-parameter cell analysis across immunophenotyping, hematology, and rare-cell detection. Spectral instruments such as Beckman Coulter's CytoFLEX mosaic and Cytek's Aurora extend traditional 10-color panels to 30 to 40 color designs, enabling deep immunophenotyping of T-cell subsets in murine tumor models per OMIP-105 panel publications in 2024. Image-based cytometry is the fastest-growing technology at an 8.3% CAGR through 2030, with AI-driven cell segmentation performing counts up to 180 times faster than manual hemocytometers per NIH-cited benchmarks.

Hematology analyzers from Sysmex, Abbott, and Siemens Healthineers serve standardized clinical workflows with integrated coagulation and immunology modules. Microfluidic chip counters offer reagent-volume reductions of multiple orders of magnitude, attractive for high-cost cell-therapy batches that cannot afford large sample volumes. Spectrophotometric methods retain a niche in nucleic acid concentration and microbial counts, with DeNovix and Thermo Fisher anchoring this sub-segment. Cost-per-sample comparison favors image-based platforms over flow cytometry by approximately 40% for routine viability checks.

By Application

Research applications captured 40.6% of cell counting and analysis market revenue in 2025, sustained by tumor organoid screening, CRISPR editing-efficiency normalization, and stem-cell differentiation tracking. Clinical and diagnostic applications are the fastest-growing segment at a 7.8% CAGR through 2030 because complete blood count and lymphocyte subset analysis remain core hospital workflows, and CD4/CD8 enumeration is now embedded in HIV monitoring per WHO reference protocols established by NIST.

Bioprocessing, including viable cell density monitoring in single-use perfusion systems, is the third-largest application, with Sartorius ambr platforms achieving 125 x 10^6 cells/mL densities. Toxicity testing and cell-based therapeutic QC complete the application taxonomy, the latter directly tied to FDA-mandated 70 to 85% viability release criteria for products such as Kymriah, Yescarta, and cord-blood HPC. Cultivated meat manufacturing has emerged as a nascent industrial application, requiring continuous viable-density monitoring at scales exceeding 1,000-liter bioreactors.

By End-User

Pharmaceutical and biotechnology companies controlled 38.3% of cell counting and analysis demand in 2025, anchored by upstream and downstream bioprocessing of biologics and advanced therapies. Hospitals and clinical laboratories are forecast to grow fastest at an 8.1% CAGR, driven by routine hematology and the integration of automated counters into emergency departments and oncology wards.

Academic and research institutes account for the third-largest end-user share at approximately 27%, supported by NIH and Horizon Europe grant funding into single-cell biology. Contract research organizations and CDMOs represent the fastest-emerging end-user segment given the outsourced nature of CAR-T and TIL therapy manufacturing for sponsors such as Bristol Myers Squibb, Novartis, and Vertex Pharmaceuticals. End-user procurement checklists now extend beyond price to include data integrity, 21 CFR Part 11 compliance, and remote service uptime guarantees.

Regional Analysis

The global cell counting and analysis market displays distinct regional revenue and growth profiles across North America, Europe, Asia Pacific, Latin America, and Middle East and Africa, with U.S. installed-base density and Chinese bioprocessing investment driving the geographic mix.

North America

North America led the cell counting and analysis market with 39.7% share in 2025, equivalent to approximately USD 4.45 Billion in regional revenue. The United States accounted for the bulk of regional demand, supported by NIH funding exceeding USD 47 Billion in fiscal year 2025 and FDA approvals of multiple CAR-T therapies including Carvykti, Kymriah, and Yescarta. Canada's market is concentrated in Toronto and Montreal biopharma clusters, with Sanofi and STEMCELL Technologies anchoring local instrument demand. The U.S. holds roughly 84% of North American regional revenue. Federal Cures 2.0 reauthorization activity in early 2026 is expected to maintain biomedical research-grant volume.

Europe

Europe held approximately 27.5% of cell counting and analysis market revenue in 2025, valued near USD 3.08 Billion. Germany leads regional demand with strong Merck KGaA, Sartorius, and Miltenyi Biotec headquarters presence, while the United Kingdom and France contribute through GSK, AstraZeneca, and Sanofi pipelines. The EU In Vitro Diagnostic Regulation (IVDR 2017/746), now fully enforced, has tightened conformity assessment requirements for clinical cytometry and accelerated procurement of CE-IVD compliant systems. Horizon Europe research funding allocated EUR 95.5 Billion through 2027, with substantial flows into single-cell genomics and ATMP characterization. Germany alone is projected near USD 0.78 Billion in 2026.

Asia Pacific

Asia Pacific captured 23% of cell counting and analysis market revenue in 2025 and is forecast to grow fastest at a 7.93% CAGR through 2030. China leads regional demand on the back of biopharmaceutical capacity expansion and government-backed cell-therapy approvals through the National Medical Products Administration. India is rapidly scaling contract manufacturing through CDMOs such as Syngene and Biocon, with the Department of Biotechnology funding cell-therapy infrastructure. Japan's Pharmaceuticals and Medical Devices Agency continues to lead globally in regenerative-medicine conditional approvals, sustaining instrument demand at Takeda, Astellas, and Daiichi Sankyo. South Korea's bio-cluster in Songdo anchors Samsung Biologics and Celltrion procurement.

Latin America

Latin America accounted for approximately 5.8% of cell counting and analysis market revenue in 2025. Brazil and Mexico together represent more than 60% of regional adoption, driven by ANVISA-regulated public hospital networks and growing contract research at Eurofins-affiliated sites. Argentina and Colombia contribute through clinical-trial infrastructure expansion. Regional growth is constrained by USD-denominated instrument pricing and capital-cost barriers in mid-tier hospitals, with most laboratories prioritizing manual or semi-automated counters until reagent supply stabilizes.

Middle East & Africa

Middle East and Africa held approximately 4% of cell counting and analysis market revenue in 2025. The UAE, Saudi Arabia, and Israel anchor instrument demand through Vision 2030 healthcare investments and growing precision-medicine programs at institutions such as King Faisal Specialist Hospital. South Africa leads the African market through National Health Laboratory Service procurement. February 2025's USD 2.5 Million National Cancer Institute grant supporting Beckman Coulter and Indiana University leukemia diagnostics in Western Kenya signals expanding philanthropic and government co-investment in African cell-analysis capacity.

Country Analysis

United States

The United States cell counting and analysis market reached approximately USD 3.74 Billion in 2025, with country-specific growth tracking near 8.4% CAGR through 2034, slightly above global average. Demand is concentrated in Massachusetts, California, and North Carolina biopharma corridors, with major procurement at Pfizer, Moderna, Bristol Myers Squibb, and Genentech. NIH allocated USD 47.7 Billion to medical research in fiscal 2025, of which roughly USD 5 Billion supports cell-biology programs requiring high-throughput counting. The FDA's Office of Tissues and Advanced Therapies has approved 12 cell and gene therapy products through April 2026, each with viability and dose-count release specifications enforced through GMP-compliant counting platforms. State-level investment includes the California Institute for Regenerative Medicine's USD 5.5 Billion bond funding stem-cell research infrastructure across the state's universities.

Germany

Germany's cell counting and analysis market reached approximately USD 0.78 Billion in 2026, growing at a country CAGR near 7.5%. Merck KGaA, Sartorius AG, and Miltenyi Biotec headquartered in Darmstadt, Goettingen, and Bergisch Gladbach respectively anchor domestic instrument supply and cluster academic-industrial procurement. The Federal Ministry of Education and Research (BMBF) funds the National Decade Against Cancer with EUR 1 Billion through 2029, embedding cell counting in oncology research workflows. Q3 2024's Merck cell-analysis facility opening in Darmstadt added local manufacturing capacity for advanced counting instruments.

China

China's cell counting and analysis market reached approximately USD 1.08 Billion in 2026, growing at country CAGR exceeding 9.0%, the highest among major economies. The 14th Five-Year Plan prioritizes biotech as a strategic emerging industry, with the National Medical Products Administration approving multiple domestic CAR-T therapies including Carteyva and CT103A. WuXi Biologics, BeiGene, and Innovent Biologics anchor commercial demand. Local instrument competitors such as Countstar (Aligned Genetics) are gaining domestic share through cost-competitive image-based counters, while Beckman Coulter and Thermo Fisher retain leadership in high-end flow cytometry.

Japan

Japan's cell counting and analysis market reached approximately USD 0.57 Billion in 2026 and is forecast as one of the fastest-growing country markets at country CAGR near 9.5% through 2030. The Pharmaceuticals and Medical Devices Agency operates a unique conditional-approval pathway for regenerative-medicine products, accelerating procurement of GMP-grade counters at Takeda's T-CiRA cell-therapy facility and CellSeed Inc. Sysmex Corporation, headquartered in Kobe, dominates Japanese clinical hematology and received FDA 510(k) clearance for the XN-1000 cell counter in Q4 2024, expanding U.S. market access.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Product

- Instruments

- Automated Cell Counters

- Flow Cytometers

- Hematology Analyzers

- High-Content Screening Systems

- Microscopes and Imaging Systems

- Spectrophotometers

- Cell Analysis Platforms

- Others

- Consumables and Reagents

- Assay Kits

- Stains and Dyes

- Microplates

- Counting Chambers and Slides

- Buffers and Media

- Antibodies and Probes

- Others

- Software and Analytics Solutions

- Services

- Others

By Technology

- Flow Cytometry

- Image-Based Cell Counting

- Electrical Impedance (Coulter Principle)

- Fluorescence-Based Detection

- Spectrophotometry

- Microscopy-Based Cell Analysis

- Microfluidics-Based Cell Analysis

- Automated Cell Counting Technologies

- High-Content Screening and Analysis

- Single-Cell Analysis Technologies

- Artificial Intelligence (AI)-Enabled Cell Analysis

- Others

By End-User

- Hospitals and Diagnostic Laboratories

- Academic and Research Institutes

- Pharmaceutical and Biotechnology Companies

- Contract Research Organizations (CROs)

- Clinical Testing Laboratories

- Cell Therapy and Regenerative Medicine Centers

- Blood Banks

- Forensic Laboratories

- Food and Beverage Testing Laboratories

- Environmental Testing Laboratories

- Others

By Application

- Cancer Research

- Drug Discovery and Development

- Clinical Diagnostics

- Stem Cell Research

- Immunology Research

- Cell and Gene Therapy

- Regenerative Medicine

- Toxicity Testing

- Biopharmaceutical Production

- Microbiology and Infectious Disease Research

- Hematology Studies

- Personalized Medicine

- Food Safety and Environmental Monitoring

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 11.20 B |

| Forecast Revenue (2034) | USD 22.85 B |

| CAGR (2025-2034) | 8.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product, (Instruments, Consumables and Reagents, Software and Analytics Solutions, Services, Others), By Technology, (Flow Cytometry, Image-Based Cell Counting, Electrical Impedance (Coulter Principle), Fluorescence-Based Detection, Spectrophotometry, Microscopy-Based Cell Analysis, Microfluidics-Based Cell Analysis, Automated Cell Counting Technologies, High-Content Screening and Analysis, Single-Cell Analysis Technologies, Artificial Intelligence (AI)-Enabled Cell Analysis, Others), By End-User, (Hospitals and Diagnostic Laboratories, Academic and Research Institutes, Pharmaceutical and Biotechnology Companies, Contract Research Organizations (CROs), Clinical Testing Laboratories, Cell Therapy and Regenerative Medicine Centers, Blood Banks, Forensic Laboratories, Food and Beverage Testing Laboratories, Environmental Testing Laboratories, Others), By Application, (Cancer Research, Drug Discovery and Development, Clinical Diagnostics, Stem Cell Research, Immunology Research, Cell and Gene Therapy, Regenerative Medicine, Toxicity Testing, Biopharmaceutical Production, Microbiology and Infectious Disease Research, Hematology Studies, Personalized Medicine, Food Safety and Environmental Monitoring, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | THERMO FISHER SCIENTIFIC INC., DANAHER CORPORATION (BECKMAN COULTER LIFE SCIENCES), BECTON, DICKINSON AND COMPANY (BD), MERCK KGAA, SARTORIUS AG, AGILENT TECHNOLOGIES INC., BIO-RAD LABORATORIES INC., SYSMEX CORPORATION, ABBOTT LABORATORIES, F. HOFFMANN-LA ROCHE LTD., SIEMENS HEALTHINEERS AG, REVVITY INC. (FORMERLY PERKINELMER), OLYMPUS CORPORATION, MILTENYI BIOTEC GMBH, DENOVIX INC., CHEMOMETEC A/S, LOGOS BIOSYSTEMS INC., NANOENTEK INC., HORIBA LTD., CYTEK BIOSCIENCES INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Flow Cytometry, Image-Based, Electrical Impedance, Fluorescence, High-Content Screening, Single-Cell, AI-Enabled), By End-User (Hospitals, Academics, Pharma & Biotech, CROs), By Application (Oncology, Drug Discovery, Diagnostics, Stem Cell, Cell & Gene Therapy) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Technology (Flow Cytometry, Image-Based, Electrical Impedance, Fluorescence, High-Content Screening, Single-Cell, AI-Enabled), By End-User (Hospitals, Academics, Pharma & Biotech, CROs), By Application (Oncology, Drug Discovery, Diagnostics, Stem Cell, Cell & Gene Therapy) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Technology (Flow Cytometry, Image-Based, Electrical Impedance, Fluorescence, High-Content Screening, Single-Cell, AI-Enabled), By End-User (Hospitals, Academics, Pharma & Biotech, CROs), By Application (Oncology, Drug Discovery, Diagnostics, Stem Cell, Cell & Gene Therapy) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Cell Counting and Analysis Market?

The Global Cell Counting and Analysis Market was valued at USD 10.35 Billion in 2024 and USD 11.20 Billion in 2025, and is projected to reach USD 22.85 Billion by 2034, growing at a CAGR of 8.2% from 2026 to 2034. Market growth is driven by increasing life science research activities, rising demand for cell-based assays, and expanding applications in clinical diagnostics and biopharmaceutical development.

Who are the major players in the Cell Counting and Analysis Market?

THERMO FISHER SCIENTIFIC INC., DANAHER CORPORATION (BECKMAN COULTER LIFE SCIENCES), BECTON, DICKINSON AND COMPANY (BD), MERCK KGAA, SARTORIUS AG, AGILENT TECHNOLOGIES INC., BIO-RAD LABORATORIES INC., SYSMEX CORPORATION, ABBOTT LABORATORIES, F. HOFFMANN-LA ROCHE LTD., SIEMENS HEALTHINEERS AG, REVVITY INC. (FORMERLY PERKINELMER), OLYMPUS CORPORATION, MILTENYI BIOTEC GMBH, DENOVIX INC., CHEMOMETEC A/S, LOGOS BIOSYSTEMS INC., NANOENTEK INC., HORIBA LTD., CYTEK BIOSCIENCES INC., Others

Which segments covered the Cell Counting and Analysis Market?

By Product, (Instruments, Consumables and Reagents, Software and Analytics Solutions, Services, Others), By Technology, (Flow Cytometry, Image-Based Cell Counting, Electrical Impedance (Coulter Principle), Fluorescence-Based Detection, Spectrophotometry, Microscopy-Based Cell Analysis, Microfluidics-Based Cell Analysis, Automated Cell Counting Technologies, High-Content Screening and Analysis, Single-Cell Analysis Technologies, Artificial Intelligence (AI)-Enabled Cell Analysis, Others), By End-User, (Hospitals and Diagnostic Laboratories, Academic and Research Institutes, Pharmaceutical and Biotechnology Companies, Contract Research Organizations (CROs), Clinical Testing Laboratories, Cell Therapy and Regenerative Medicine Centers, Blood Banks, Forensic Laboratories, Food and Beverage Testing Laboratories, Environmental Testing Laboratories, Others), By Application, (Cancer Research, Drug Discovery and Development, Clinical Diagnostics, Stem Cell Research, Immunology Research, Cell and Gene Therapy, Regenerative Medicine, Toxicity Testing, Biopharmaceutical Production, Microbiology and Infectious Disease Research, Hematology Studies, Personalized Medicine, Food Safety and Environmental Monitoring, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Cell Counting and Analysis Market

Published Date : 16 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date