- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Cell-Cultured Seafood Market Size & Forecast 2034 | CAGR 32.6%

Global Cell-Cultured Seafood Market Size, Share, Growth & Industry Analysis By Species Type (Finfish—Salmon, Tuna, Grouper, Mahi-Mahi, Seabream; Crustaceans—Shrimp, Crab, Lobster; Mollusks—Oysters, Mussels, Clams), By Distribution Channel (Foodservice, Specialty Retail, E-Commerce, Institutional), By Production Technology (Bioreactors, Scaffold-Based, Adherent Systems) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

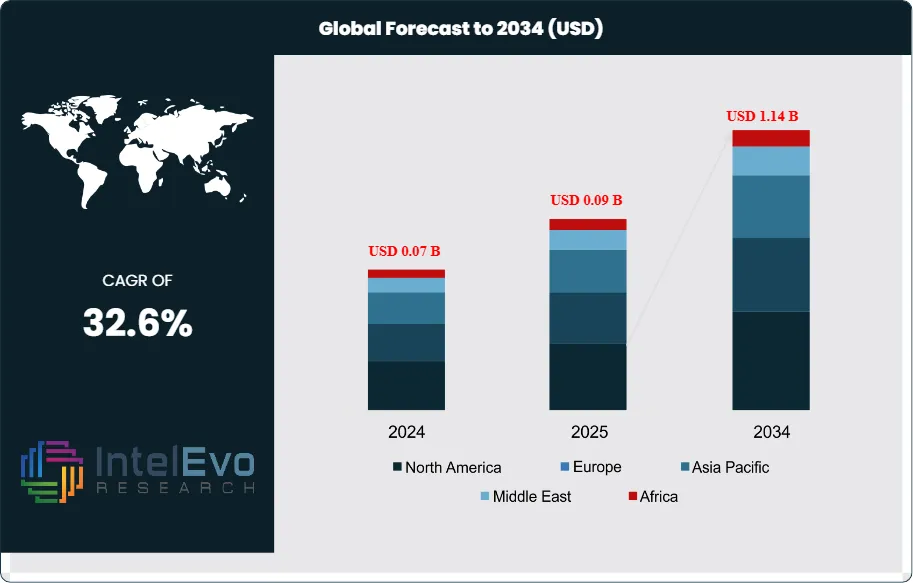

| USD 0.09 Billion | USD 1.14 Billion | 32.6% | North America, 44.4% |

The Cell-Cultured Seafood Market was valued at approximately USD 0.07 Billion in 2024 and reached USD 0.09 Billion in 2025. The market is projected to grow to USD 1.14 Billion by 2034, expanding at a CAGR of 32.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 1.05 Billion over the analysis period, driven by mounting regulatory approvals in key markets, accelerating bioprocess scale-up, declining cell culture media costs, and intensifying investor conviction in alternative protein supply chain development.

Get More Information about this report -

Request Free Sample ReportCell-cultured seafood, also referred to as cultivated seafood or cell-based seafood, is produced by isolating living cells from marine organisms, proliferating those cells in bioreactors using nutrient-rich culture media, and structuring the resulting cell mass into consumer-ready seafood products. The technology eliminates the need for ocean harvesting or aquaculture grow-out, offering a production pathway that is independent of wild fish population health, ocean temperature variability, and disease risk in conventional aquaculture systems. The cell-cultured seafood market spans finfish products including salmon, tuna, and grouper; crustaceans including shrimp, crab, and lobster; and mollusks and other marine species targeted for premium food service and retail applications.

Several macro forces are converging to accelerate commercial development of the cell-cultured seafood market. The FAO estimates that global wild-capture fisheries have been at or near their maximum sustainable yield since the mid-1990s, and approximately 35% of global fish stocks are now classified as overfished, creating structural supply pressure that cell-cultured alternatives can address. The FDA and USDA finalized their joint oversight framework for cell-cultured meat and seafood products in 2023, and the Singapore Food Agency (SFA) granted the world's first novel food approval for a cell-cultured meat product, establishing the regulatory precedent that the cell-cultured seafood market needed to attract institutional capital. Consumer concern over microplastic contamination in wild-caught seafood, detected in commercial fish tissue at concentrations exceeding 1-2 particles per gram in multiple independent studies, is also creating a demand-side pull toward controlled-environment cell-cultured production.

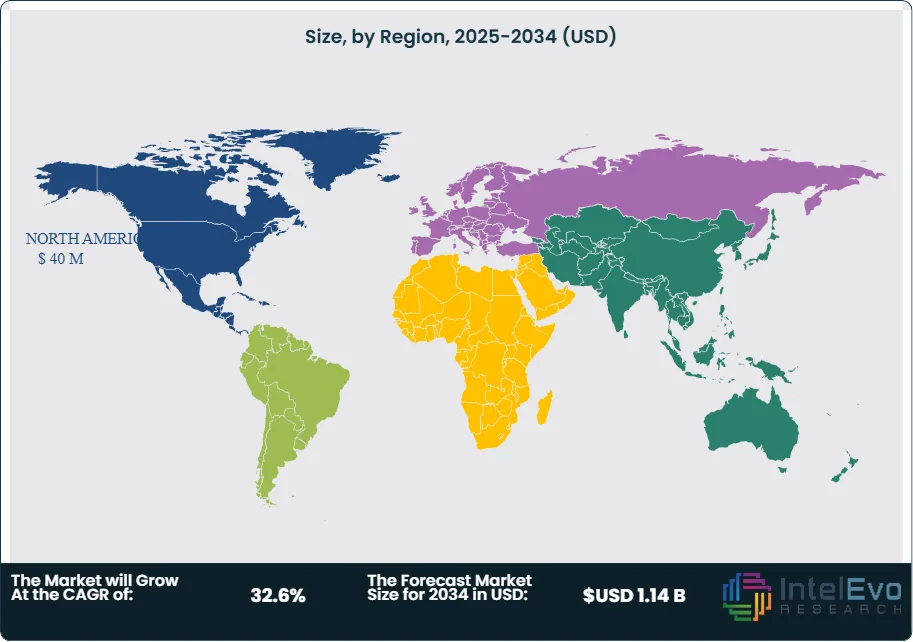

The cell-cultured seafood market remains in an early commercial stage, with most producers operating at pilot or demonstration scale in 2025. Bioprocess cost reduction, particularly the development of food-grade serum-free cell culture media that do not rely on fetal bovine serum, is the central technical challenge gating cost-competitive commercial production. North America leads the cell-cultured seafood market with a 44.4% share in 2025, equivalent to USD 40 Million, driven by concentrated startup activity in San Francisco and Boston, regulatory clarity from the FDA-USDA framework, and strong institutional investor funding. Asia Pacific is the second-largest region and growing fastest, reflecting Singapore's regulatory leadership and Japan's strategic interest in seafood security.

, By Distribution Channel (Foodservice, Specialty Retail, E-Commerce, Institutional), By Production Technology (Bioreactors, Scaffold-Based, Adherent Systems) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global cell-cultured seafood market was valued at USD 0.09 Billion in 2025 and is forecast to reach USD 1.14 Billion by 2034, registering a CAGR of 32.6% during the 2026-2034 forecast period.

- Segment Dominance: By species type, cell-cultured finfish held the largest share at 52.3% of the cell-cultured seafood market in 2025, with salmon and tuna representing the highest-value target species due to their premium consumer price positioning and strong brand recognition in foodservice.

- Segment Dominance: By distribution channel, foodservice and restaurant applications accounted for 68.4% of cell-cultured seafood market revenues in 2025, as premium restaurants and controlled-environment dining venues serve as the primary commercial launch channel for early cell-cultured seafood products.

- Driver: Global wild fish stock depletion, with approximately 35% of global fisheries classified as overfished by the FAO as of 2025, is creating structural seafood supply pressure that cell-cultured production directly addresses, compelling food security-focused governments and institutional investors to accelerate funding.

- Restraint: Cell culture media costs, which currently represent 55-70% of total cell-cultured seafood production costs, constrain commercial viability; food-grade serum-free media for marine cell lines are priced at USD 300-800 per liter, making cost-competitive production at retail price points technically infeasible at current scale.

- Opportunity: Japan's strategic seafood security concerns, combined with the Ministry of Agriculture Forestry and Fisheries' active support for cultivated seafood development, represent an addressable cell-cultured seafood market opportunity estimated at USD 180 Million annually by 2034 within the world's largest per-capita seafood consuming nation.

- Trend: Adoption of suspension bioreactor production systems for cell-cultured seafood, which offer 10-50 times higher volumetric productivity versus static culture formats, grew at approximately 28.4% annually in 2025 as producers transitioned from research-scale to pilot-scale manufacturing infrastructure.

- Regional Analysis: North America led the cell-cultured seafood market with a 44.4% share, equivalent to USD 40 Million in 2025, supported by FDA-USDA joint regulatory clarity, dense startup activity in California and Massachusetts, and venture capital investment from alternative protein-focused funds.

Competitive Landscape Overview

The cell-cultured seafood market is highly fragmented, with the top four companies — Wildtype Inc., Shiok Meats, BlueNalu Inc., and Umami Meats — collectively accounting for approximately 58% of global market revenues in 2025. Competition centers on species specialization, bioprocess technology differentiation, regulatory approval status, and speed of foodservice channel penetration. Most competitors are pre-revenue or in early revenue stages, with competition currently defined more by technical milestone achievement and regulatory progress than by commercial sales volume. M&A activity remains limited, with the dominant competitive dynamic being venture capital fundraising and strategic corporate partnerships with food ingredient companies and seafood distributors. The sector received over USD 190 Million in disclosed investment between 2023 and 2025.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Wildtype Inc. | USA | Leader | Cell-Cultured Atlantic Salmon | North America | Expanded pilot production facility in San Francisco; targeting US restaurant channel launch in 2025. |

| Shiok Meats | Singapore | Leader | Cell-Cultured Shrimp & Crustaceans | Asia Pacific | Received Singapore SFA novel food approval for cell-cultured shrimp; commenced limited commercial supply Q1 2025. |

| BlueNalu Inc. | USA | Leader | Cell-Cultured Mahi-Mahi & Yellowtail | North America | Secured USD 60M in Series B funding; began construction of first commercial-scale cell-cultured seafood production facility; 2025. |

| Umami Meats | Singapore | Leader | Cell-Cultured Grouper & Seabream | Asia Pacific | Partnered with major Singapore food service operator for pilot restaurant supply of cell-cultured grouper; Q2 2025. |

| Finless Foods | USA | Challenger | Cell-Cultured Bluefin Tuna | North America | Announced technology partnership with Japanese sushi chain for pilot menu introduction of cell-cultured tuna; 2025. |

| CellarDoor Bio (Avant Meats) | Hong Kong | Challenger | Cell-Cultured Fish Maw & Marine Products | Asia Pacific | Signed co-development agreement with a Hong Kong seafood distributor for cell-cultured fish maw; early 2025. |

| Cell-Ag Tech (Protein Brewery) | Netherlands | Niche Player | Cell-Cultured Marine Protein Ingredients | Europe | Received EU novel food dossier pre-submission feedback; advancing regulatory approval process; Q3 2025. |

| Aqua-Spark Portfolio Companies | Netherlands | Niche Player | Cell-Cultured Seafood Investment Portfolio | Europe | Expanded portfolio to include two additional cell-cultured seafood biotech startups; January 2026. |

| Good Food Institute Partners | USA | Niche Player | Open-Source Cell-Cultured Seafood R&D | Global | Published open-access research on serum-free media for marine cell culture; accelerating industry progress; 2025. |

| Tao Foods | USA | Niche Player | Cell-Cultured Shrimp & Shellfish | North America | Raised USD 12M seed round to advance cell-cultured shrimp bioprocess development; Q3 2025. |

By Species Type

The cell-cultured seafood market by species type spans finfish, crustaceans, mollusks, and other marine species. Cell-cultured finfish held the dominant share at 52.3% of the market in 2025, equivalent to approximately USD 47 Million. Salmon, tuna, mahi-mahi, grouper, and seabream are the primary target finfish species, selected for their high retail price points, strong consumer demand, and cultural significance in key target markets including the United States, Japan, Singapore, and Europe. Wildtype Inc. has focused exclusively on Atlantic salmon, leveraging its position as a premium seafood species commanding retail prices of USD 15-30 per pound that can accommodate the higher production costs of early cell-cultured manufacturing. Finless Foods has targeted bluefin tuna, the highest-value wild-caught seafood species with Japanese retail prices exceeding USD 80 per pound for premium cuts, creating the largest margin buffer for early cell-cultured production costs.

Cell-cultured crustaceans represented 31.4% of the cell-cultured seafood market in 2025. Shrimp is the primary target crustacean species, as it is the most consumed seafood product globally by volume, with annual global consumption exceeding 6 million metric tons. Shiok Meats and Tao Foods have each developed cell culture protocols for shrimp cell expansion, with Shiok Meats achieving the world's first regulatory approval for a cell-cultured crustacean product in Singapore. Crab and lobster represent smaller but higher-margin crustacean targets. Mollusks including oysters, mussels, and clams held an 11.2% share of the cell-cultured seafood market in 2025, with appeal driven by their high omega-3 fatty acid content and premium positioning. Other marine species including sea urchin, sea cucumber, and specialty marine organisms represented the remaining 5.1% of the cell-cultured seafood market by species type in 2025.

By Distribution Channel

The cell-cultured seafood market by distribution channel covers foodservice and restaurants, specialty retail, e-commerce direct-to-consumer, and institutional food service. Foodservice and restaurant channels accounted for the dominant share at 68.4% of the cell-cultured seafood market in 2025, equivalent to approximately USD 62 Million. Premium restaurants, fine-dining establishments, and technology-focused dining concepts serve as the optimal launch channel for early cell-cultured seafood products, enabling controlled consumer education experiences and supporting price premiums of 50-200% above conventional seafood equivalents. Wildtype has pursued this channel strategy explicitly, partnering with San Francisco and New York restaurant groups to introduce cell-cultured salmon in curated tasting menus. Singapore's Shiok Meats has similarly prioritized high-end Asian restaurant partnerships as its initial market entry pathway following SFA novel food approval.

Specialty retail, including natural food stores, specialty seafood retailers, and premium grocery chains, held 18.7% of the cell-cultured seafood market in 2025 and represents the next commercialization phase as production scales and per-unit costs decline. E-commerce direct-to-consumer channels accounted for 8.4% of the market in 2025, primarily through subscription models and limited-availability product launches that build brand awareness and gather consumer feedback ahead of broader retail distribution. Institutional food service, including hotel groups, airline catering, and corporate dining, held the remaining 4.5% of the cell-cultured seafood market by distribution channel in 2025. Institutional channels are expected to grow rapidly once production volumes can sustain the consistent supply volumes that institutional buyers require.

By Production Technology

The cell-cultured seafood market by production technology segments into suspension bioreactor systems, adherent cell culture systems, scaffold-based 3D culture, and hybrid bioprocess approaches. Suspension bioreactor production held the largest share at 44.6% of the cell-cultured seafood market by production technology in 2025. Suspension systems, where marine cells are adapted to grow freely in agitated liquid culture without an attachment surface, offer the most straightforward pathway to large-scale production because existing fermentation infrastructure can be repurposed and batch sizes are limited primarily by bioreactor vessel volume rather than surface area. Producers including BlueNalu and Wildtype are pursuing suspension culture as their primary scale-up pathway. The transition from research-scale suspension culture to pilot-scale 1,000-10,000 liter bioreactors represents the primary engineering challenge in 2025.

Scaffold-based 3D culture, where marine cells are seeded onto edible scaffolding materials including plant-derived proteins, alginate, or chitosan to form structured tissue resembling whole fish muscle cuts, held a 28.3% share of the production technology segment in 2025 and is the most technically ambitious approach. This technology produces cell-cultured seafood products with authentic fibrous texture that resembles conventional fish fillets, commanding the highest consumer price premiums. Adherent cell culture systems, using flat culture vessels or microcarrier bead systems where cells attach to a surface for growth, represented 18.6% of the production technology market in 2025 and are most commonly used in early R&D and pilot production stages. Hybrid approaches combining suspension proliferation with downstream scaffolding for texturization held the remaining 8.5% of the cell-cultured seafood market by production technology in 2025.

By End-Use

The cell-cultured seafood market by end-use covers whole-muscle analogs, minced or processed seafood products, ingredient-form marine proteins, and cosmetic and nutraceutical applications. Whole-muscle analog products, which aim to replicate the appearance, texture, and eating experience of conventional fish fillets, steaks, or shellfish, held the dominant end-use share at 48.2% of the cell-cultured seafood market in 2025. These products command the highest retail price premiums and represent the most aspirational commercial target for leading producers. Minced or processed seafood products, including cell-cultured fish cakes, sushi fillings, surimi analogs, and processed shrimp, represented 32.6% of the market in 2025 and represent a technically more accessible near-term commercial pathway because texture engineering requirements are less demanding than for whole-muscle formats. Ingredient-form marine proteins, where cell-cultured biomass is processed into protein powders, extracts, or flavor compounds for use as food ingredients, held 14.7% of the end-use market in 2025. Cosmetic, nutraceutical, and specialty applications represented the remaining 4.5%.

Regional Analysis

North America

North America cell-cultured seafood market held a 44.4% share in 2025, generating approximately USD 40 Million in revenue. The United States is the dominant national market, home to the largest concentration of cell-cultured seafood startups globally, with companies including Wildtype, BlueNalu, Finless Foods, and Tao Foods all based in California. The FDA-USDA joint regulatory framework finalized in 2023 provides the clearest regulatory pathway for cell-cultured seafood commercialization of any major market globally, requiring pre-market consultation and cell line safety evaluation before commercial sale. USDA's Food Safety and Inspection Service oversees cell-cultured seafood production under the Poultry Products Inspection Act framework, while FDA's Center for Food Safety and Applied Nutrition handles cell line and ingredient safety. The National Oceanic and Atmospheric Administration (NOAA) has engaged with cell-cultured seafood development through its aquaculture research programs, recognizing cultivated seafood as a potential tool for reducing pressure on wild-capture fisheries. US venture capital investment in cell-cultured seafood companies exceeded USD 120 Million between 2022 and 2025, sustaining a pipeline of well-funded development-stage companies. Canada contributes through emerging cell-cultured salmon research programs at British Columbia academic institutions aligned with the country's significant wild salmon fishery sector.

Europe

Europe held approximately 18.6% of the cell-cultured seafood market in 2025, generating approximately USD 17 Million. The Netherlands leads European market activity through its concentration of alternative protein research institutions, Wageningen University's food technology programs, and portfolio investment activity through Aqua-Spark's alternative seafood fund. The European Union's Novel Food Regulation (EU) 2015/2283 governs the regulatory approval pathway for cell-cultured seafood products, requiring submission of detailed safety dossiers to EFSA before commercial sale across EU member states. As of 2025, no cell-cultured seafood product had achieved full EU novel food authorization, but pre-submission scientific consultations with EFSA were underway for several European and US-based producers. The UK's Food Standards Agency is assessing cell-cultured food safety under its post-Brexit novel food framework, with the FSA's positive engagement signaling a receptive regulatory environment. Germany represents the largest potential consumer market within Europe, where premium seafood consumption and strong consumer interest in sustainability-labeled food products create favorable demand conditions. France and the Netherlands each contribute through food technology innovation programs and sustainable food investment funds.

Asia Pacific

Asia Pacific held approximately 28.4% of the global cell-cultured seafood market in 2025, generating approximately USD 26 Million, and is the second-largest regional market and a global regulatory leader. Singapore occupies a uniquely important position in the cell-cultured seafood market globally, having granted the world's first approval for a commercial cell-cultured food product in 2020 under the Singapore Food Agency's novel food regulatory framework. This approval created the legal and commercial foundation for Shiok Meats and Umami Meats to begin limited commercial supply of cell-cultured shrimp and grouper in Singapore's premium foodservice sector in 2025. Japan is the strategically most significant longer-term Asia Pacific market, as the country consumes more seafood per capita than any other nation and faces acute wild fish supply pressures from declining Pacific fisheries. Japan's Ministry of Agriculture, Forestry and Fisheries has actively funded cultivated seafood research and is developing a regulatory approval pathway modeled on the FDA-USDA framework. South Korea's active alternative protein startup sector and government food technology investment programs create a receptive environment for cell-cultured seafood development. China, the world's largest seafood consumer by absolute volume, represents the ultimate high-volume opportunity for cell-cultured seafood producers, with pilot regulatory engagement underway through the National Center for Food Safety Risk Assessment.

Latin America

Latin America represented approximately 5.4% of the cell-cultured seafood market in 2025, generating approximately USD 5 Million. Chile is the most significant national market within the region and globally important for the cell-cultured seafood sector because of its position as the world's second-largest farmed salmon producer after Norway. Conventional farmed salmon in Chile faces persistent sea lice infestation, infectious salmon anemia outbreaks, and growing environmental regulation of net pen aquaculture in Patagonian fjords, creating commercial interest in land-based and cell-culture alternatives. Chilean government biotechnology investment programs and university research collaborations are beginning to explore cell-cultured salmon as a potential complement to the country's existing aquaculture industry. Brazil represents a growing consumer market for premium seafood products and hosts an expanding food technology startup sector, with cell-cultured seafood emerging as a potential application for Brazilian biotech investment. Mexico contributes through aquaculture-adjacent food technology development, particularly for shrimp, which is one of Mexico's primary conventional aquaculture export products. The region's overall cell-cultured seafood market remains in an early awareness and pre-commercial stage, with growth dependent on regulatory framework development and bioprocess cost reduction.

Middle East & Africa

The Middle East and Africa region held approximately 3.2% of the cell-cultured seafood market in 2025, generating approximately USD 3 Million. The UAE is the most active regional market, driven by Dubai's position as a global food innovation hub and the UAE government's food security strategy, which identifies cell-cultured protein as a strategic domestic production priority to reduce dependence on seafood imports. The Dubai Future Foundation and Abu Dhabi's food technology investment programs have both engaged with cell-cultured seafood development, and several international cell-cultured seafood companies have entered discussions for UAE pilot production facilities. Saudi Arabia's Vision 2030 food diversification agenda includes aquaculture expansion and alternative protein development, creating a supportive policy environment for cell-cultured seafood investment. Israel, while geographically positioned within the broader region, contributes disproportionately through its deep-tech food technology sector, with companies developing enabling bioprocessing technologies including serum-free marine cell culture media and scaffold materials that support global cell-cultured seafood development. South Africa is the most active Sub-Saharan African market, with nascent alternative protein research activity at university food science departments. The region's overall market remains small and pre-commercial but is expected to grow as UAE regulatory frameworks for novel food are developed.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Species Type

- Finfish (Salmon, Tuna, Grouper, Mahi-Mahi, Seabream)

- Crustaceans (Shrimp, Crab, Lobster)

- Mollusks (Oysters, Mussels, Clams)

- Other Marine Species

By Distribution Channel

- Foodservice & Restaurants

- Specialty Retail

- E-Commerce Direct-to-Consumer

- Institutional Food Service

By Production Technology

- Suspension Bioreactor Systems

- Scaffold-Based 3D Culture

- Adherent Cell Culture Systems

- Hybrid Bioprocess Approaches

By End-Use

- Whole-Muscle Analog Products

- Minced & Processed Seafood Products

- Ingredient-Form Marine Proteins

- Cosmetic, Nutraceutical & Specialty Applications

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 0.09 B |

| Forecast Revenue (2034) | USD 1.14 B |

| CAGR (2025-2034) | 32.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Species Type, (Finfish (Salmon, Tuna, Grouper, Mahi-Mahi, Seabream), Crustaceans (Shrimp, Crab, Lobster), Mollusks (Oysters, Mussels, Clams), Other Marine Species), By Distribution Channel, (Foodservice & Restaurants, Specialty Retail, E-Commerce Direct-to-Consumer, Institutional Food Service), By Production Technology, (Suspension Bioreactor Systems, Scaffold-Based 3D Culture, Adherent Cell Culture Systems, Hybrid Bioprocess Approaches), By End-Use, (Whole-Muscle Analog Products, Minced & Processed Seafood Products, Ingredient-Form Marine Proteins, Cosmetic, Nutraceutical & Specialty Applications) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | WILDTYPE INC., SHIOK MEATS, BLUENALU INC., UMAMI MEATS, FINLESS FOODS, CELLARDOOR BIO (AVANT MEATS), CELL-AG TECH (PROTEIN BREWERY), TAO FOODS, SEAFUTURE (JAPANESE CONSORTIUM), OCEAN ERA, SUSTAINABLE BIOPRODUCTS (SBP), PEARLITA FOODS, AQUA-SPARK PORTFOLIO COMPANIES, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Distribution Channel (Foodservice, Specialty Retail, E-Commerce, Institutional), By Production Technology (Bioreactors, Scaffold-Based, Adherent Systems) Industry Trends & Forecast 2026–2034")

, By Distribution Channel (Foodservice, Specialty Retail, E-Commerce, Institutional), By Production Technology (Bioreactors, Scaffold-Based, Adherent Systems) Industry Trends & Forecast 2026–2034")

, By Distribution Channel (Foodservice, Specialty Retail, E-Commerce, Institutional), By Production Technology (Bioreactors, Scaffold-Based, Adherent Systems) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the ?

Cell-cultured seafood market valued at USD 0.07B in 2024, reaching USD 1.14B by 2034, growing at a CAGR of 32.6% from 2026–2034.

Who are the major players in the ?

WILDTYPE INC., SHIOK MEATS, BLUENALU INC., UMAMI MEATS, FINLESS FOODS, CELLARDOOR BIO (AVANT MEATS), CELL-AG TECH (PROTEIN BREWERY), TAO FOODS, SEAFUTURE (JAPANESE CONSORTIUM), OCEAN ERA, SUSTAINABLE BIOPRODUCTS (SBP), PEARLITA FOODS, AQUA-SPARK PORTFOLIO COMPANIES, OTHERS

Which segments covered the ?

By Species Type, (Finfish (Salmon, Tuna, Grouper, Mahi-Mahi, Seabream), Crustaceans (Shrimp, Crab, Lobster), Mollusks (Oysters, Mussels, Clams), Other Marine Species), By Distribution Channel, (Foodservice & Restaurants, Specialty Retail, E-Commerce Direct-to-Consumer, Institutional Food Service), By Production Technology, (Suspension Bioreactor Systems, Scaffold-Based 3D Culture, Adherent Cell Culture Systems, Hybrid Bioprocess Approaches), By End-Use, (Whole-Muscle Analog Products, Minced & Processed Seafood Products, Ingredient-Form Marine Proteins, Cosmetic, Nutraceutical & Specialty Applications)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Cell-Cultured Seafood Market

Published Date : 20 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date