- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Cell Line Development Services Market Size & Forecast | CAGR 12.2%

Global Cell Line Development Services Market Size, Share, Analysis By Service Type, (CHO Cell Line Development, HEK293 & Human Cell Line Development, Microbial (E. coli / Pichia) Cell Line Development, Viral Vector Producer Cell Line Development), By Application, (Monoclonal Antibody Development, Biosimilar Development, Recombinant Protein & Enzyme Development, Cell & Gene Therapy Cell Line Development, Other Applications (Vaccines, Diagnostics)), By End-User, (Biopharmaceutical Companies, Contract Development & Manufacturing Organizations (CDMOs), Academic & Research Institutions, Contract Research Organizations (CROs)) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

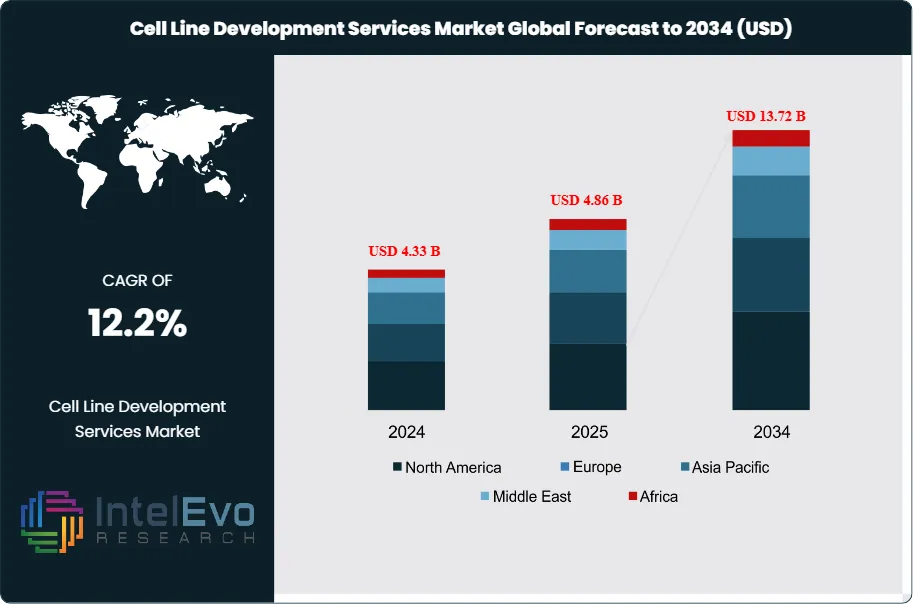

| USD 4.86 Billion | USD 13.72 Billion | 12.2% | North America, 44.8% |

The Cell Line Development Services Market was valued at approximately USD 4.33 Billion in 2024 and reached USD 4.86 Billion in 2025. The market is projected to grow to USD 13.72 Billion by 2034, expanding at a CAGR of 12.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 8.86 Billion over the analysis period, driven by the rapid expansion of the biologics drug pipeline, the accelerating adoption of Chinese hamster ovary (CHO) expression platforms, and the growing demand for specialized cell line development services from CDMOs, emerging biotechs, and biosimilar developers worldwide.

Get More Information about this report -

Request Free Sample ReportCell line development (CLD) services encompass the full workflow of generating a stable, high-expressing, well-characterized mammalian or microbial production cell line suitable for GMP biopharmaceutical manufacturing. The process includes host cell selection, gene construct design, transfection, single-cell cloning, clone screening and selection using high-throughput methods, characterization of the master cell bank (MCB), and preparation of regulatory documentation supporting IND, BLA, and MAA filings. CLD is the foundational upstream step of biologic drug manufacturing — the quality and productivity of the production cell line directly determines the efficiency, yield, and cost structure of all subsequent manufacturing campaigns. A high-expressing, genetically stable CHO cell line producing 5–10 g/L of monoclonal antibody can reduce upstream manufacturing costs by 40–60% versus a lower-expressing clone.

Demand within the cell line development services market is fundamentally driven by the biologics pipeline. The global biologic drug pipeline encompasses over 600 monoclonal antibody programs in clinical development, an expanding portfolio of bispecific antibodies, ADCs, fusion proteins, and recombinant enzymes, and a rapidly growing biosimilar development pipeline targeting originator biologics facing patent expiration. Each novel biologic program requires a dedicated production cell line developed from scratch, making CLD a mandatory early-phase investment for every biologic drug developer. Biosimilar development programs add substantial incremental CLD demand, as biosimilar developers require a cell line that produces a protein sufficiently similar to the reference product to satisfy EMA and FDA analytical similarity requirements.

Technology is transforming the cell line development services market. High-throughput clone screening platforms using fluorescence-activated cell sorting (FACS), automated imaging, and ambr15/250 scale-down bioreactor systems have compressed typical CLD timelines from 18–24 months to 6–9 months, reducing time-to-IND and creating competitive pressure on service providers to deliver accelerated timelines. AI-powered clone selection algorithms, which analyze large imaging and productivity datasets to predict clone stability and expression levels earlier in the screening funnel, are being adopted by leading CLD service providers and are shortening clone selection timelines by an additional 20–30%. FDA's Guidance for Industry on Biosimilars, ICH Q5D guidelines on cell substrate characterization, and EMA's CHMP Guidelines on the derivation of cell lines all govern CLD documentation and testing requirements, creating a regulated service environment that rewards providers with deep regulatory expertise.

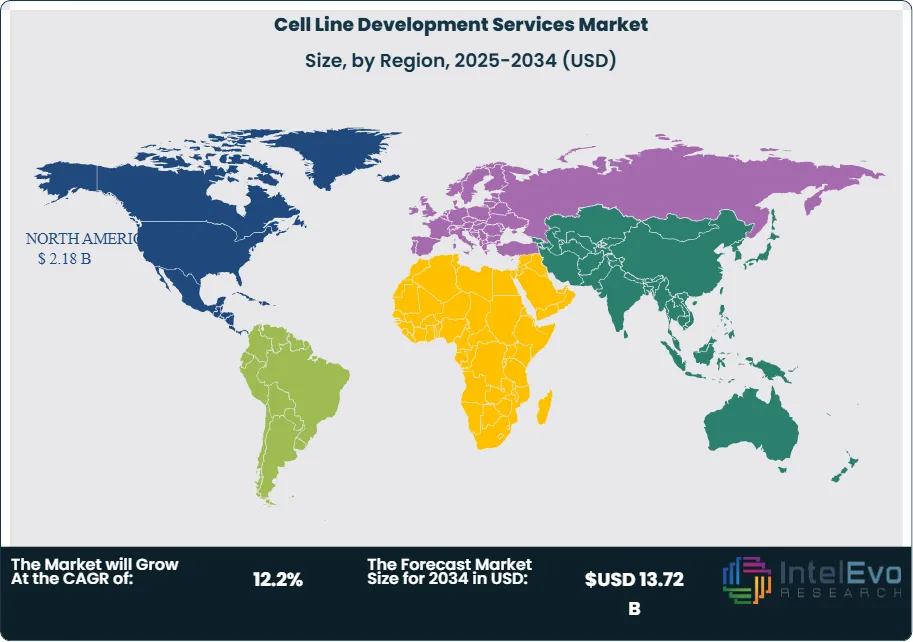

North America leads the cell line development services market with a 44.8% share in 2025, generating approximately USD 2.18 Billion, driven by the United States' dense concentration of biopharmaceutical companies and CLD-specialist CROs. Europe holds 28.4% of the market. Asia Pacific is the fastest-growing region at a projected CAGR of 15.4% through 2034, with China, South Korea, and India building CLD service capability to support domestic biologic development programs and capture global outsourcing mandates.

Cell Line Development, Viral Vector Producer Cell Line Development), By Application, (Monoclonal Antibody Development, Biosimilar Development, Recombinant Protein & Enzyme Development, Cell & Gene Therapy Cell Line Development, Other Applications (Vaccines, Diagnostics)), By End-User, (Biopharmaceutical Companies, Contract Development & Manufacturing Organizations (CDMOs), Academic & Research Institutions, Contract Research Organizations (CROs)) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global cell line development services market was valued at USD 4.86 Billion in 2025 and is projected to reach USD 13.72 Billion by 2034, growing at a CAGR of 12.2% over the forecast period 2026–2034.

- Segment Dominance: By service type, CHO cell line development services account for approximately 58.4% of cell line development services market revenue in 2025, reflecting CHO's established status as the preferred mammalian expression host for monoclonal antibodies and recombinant protein biologics.

- Segment Dominance: By application, monoclonal antibody development accounts for the largest application share at 46.2% of cell line development services market revenue in 2025, driven by the expansive global mAb clinical pipeline and the structural requirement for a new production cell line for each novel mAb program.

- Driver: The global biologic drug pipeline included over 600 active mAb development programs in clinical stages as of 2025, each requiring a new production cell line — generating a sustained pipeline of CLD mandates that is growing at approximately 8.4% annually as new biologic modalities expand the addressable project base.

- Restraint: Cell line development timelines of 6–18 months, even with accelerated high-throughput screening platforms, remain a structural bottleneck in biologic drug development, constraining the rate at which biopharmaceutical companies can advance programs from gene construct to IND-enabling studies and limiting the number of CLD programs a single service provider can manage simultaneously.

- Opportunity: The biosimilar cell line development segment represents an incremental addressable revenue opportunity exceeding USD 2.4 Billion through 2034, as more than 30 major originator biologic products face patent expiration before 2030, each requiring a dedicated biosimilar production cell line developed with rigorous analytical similarity characterization.

- Trend: AI-assisted clone selection and automated high-throughput screening platforms are present in approximately 38.6% of commercial CLD service workflows in 2025, up from 14.2% in 2020, as service providers invest in productivity-enhancing technologies to compress timelines and improve clone selection accuracy.

- Regional Analysis: North America leads the global cell line development services market with a 44.8% share in 2025, generating approximately USD 2.18 Billion in revenue, anchored by the United States' dominant biopharmaceutical R&D base and its dense concentration of specialist CLD CROs and biologic CDMOs.

Competitive Landscape Overview

The cell line development services market is moderately fragmented, with the top four providers — Lonza Group, Thermo Fisher Scientific (Patheon), WuXi Biologics, and Sartorius AG (Cellca) — collectively accounting for approximately 38.4% of global market revenue in 2025. Competition is technology- and timeline-driven, with providers differentiating on clone selection platform speed, expression system proprietary technology, CHO cell line IP licensing terms, and regulatory documentation quality. M&A activity has increased as large CDMOs and CROs acquire specialist CLD firms to build integrated upstream development capabilities that convert CLD projects into manufacturing mandates.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product/Service | Geo Strength | Recent Strategic Move (2024–2026) |

| Lonza Group | Switzerland | Leader | Lonza GS Xceed CHO Expression System | Europe / Global | Mar 2025: Launched an enhanced GS Xceed 2.0 platform with AI-assisted clone ranking tools, reducing median CLD timelines to 6 months for standard mAb programs. |

| Thermo Fisher Scientific (Patheon) | USA | Leader | Thermo Fisher CHO-S Expression System | North America / Global | Jan 2025: Expanded CLD service capacity at its Brisbane biologics development center, adding ambr250 high-throughput bioreactor screening capability for mAb and bispecific programs. |

| WuXi Biologics | China | Leader | WuXi WHOA CHO Expression Platform | Asia Pacific / Global | May 2025: Secured a multi-program CLD partnership with a top-10 global pharmaceutical company, covering 12 biologic programs across mAb, bispecific, and ADC modalities. |

| Sartorius AG (Cellca) | Germany | Leader | Cellca CHO Cell Line Development Platform | Europe / Global | Feb 2026: Integrated Cellca's proprietary CHO platform with Sartorius ambr bioreactor systems, enabling seamless CLD-to-bioprocess development workflow for CDMO clients. |

| Samsung Biologics | South Korea | Challenger | Samsung CLD Services for Biosimilars | Asia Pacific / Global | Apr 2025: Launched a dedicated biosimilar CLD service targeting originator biologics facing patent expiry, integrating cell line generation with analytical similarity studies. |

| Boehringer Ingelheim BioXcellence | Germany | Challenger | BI HEX CHO Expression System | Europe / North America | Nov 2024: Expanded CLD service offering to include bispecific antibody cell line development, leveraging its BI HEX platform with dedicated bispecific clone selection workflows. |

| FUJIFILM Diosynth Biotechnologies | UK | Challenger | FUJIFILM CHO Cell Line Development | Europe / North America | Jul 2025: Opened a new biologics development center in Research Triangle Park, NC, with dedicated CLD laboratories targeting North American biopharmaceutical clients. |

| Creative Biolabs | USA | Niche Player | CHO-based Custom Cell Line Services | North America | Jun 2025: Launched an AI-powered clone selection portal enabling clients to monitor real-time clone productivity and stability predictions during CLD campaigns. |

| ProBioGen AG | Germany | Niche Player | AGE1.HN CHO Expression System | Europe | Sep 2025: Entered a licensing agreement with a mid-sized European biopharmaceutical company for its AGE1.HN platform, targeting difficult-to-express protein production. |

| Batavia Biosciences | Netherlands | Niche Player | Viral Vector Cell Line Development | Europe / North America | Jan 2026: Expanded viral vector producer cell line development services to include AAV and lentiviral systems for gene therapy CDMO clients. |

By Service Type

The cell line development services market by service type is led by CHO (Chinese hamster ovary) cell line development services, which account for approximately 58.4% of total market revenue in 2025 at USD 2.84 Billion. CHO cells are the dominant mammalian expression host for commercial biologic drug manufacturing, owing to their high transfection efficiency, capacity for human-like glycosylation of recombinant proteins, adaptability to suspension culture in serum-free media, and an extensive regulatory track record spanning over four decades of approved biopharmaceutical products. CHO-based CLD services encompass host cell acquisition, vector design and optimization, stable transfection, single-cell cloning via limiting dilution or FACS, automated clone screening in ambr15 or 96-well miniature bioreactor formats, fed-batch optimization to maximize viable cell density and titer, and preparation of ICH Q5D-compliant master and working cell bank documentation. Leading CHO expression systems include Lonza's GS Xceed, Sartorius Cellca's CHO platform, Boehringer Ingelheim's BI HEX, and FUJIFILM Diosynth's proprietary CHO line. The CHO CLD segment is growing at a 12.0% CAGR through 2034, tracking the broader biologics market expansion.

HEK293 and other human cell line development services account for 14.8% of market revenue in 2025 at USD 0.72 Billion. HEK293 systems are preferred for complex proteins requiring human post-translational modifications that CHO cells cannot fully recapitulate, for transient expression campaigns producing clinical Phase I material, and for certain viral vector production applications in gene therapy. The gene therapy sector is driving HEK293 CLD growth, as adeno-associated virus (AAV) and lentiviral vector production for cell and gene therapy programs increasingly utilizes HEK293-based stable producer cell lines. Microbial (E. coli and Pichia) CLD services represent 14.4% of revenue at USD 0.70 Billion, primarily serving biosimilar insulin, growth hormone, and antibody fragment programs where the glycosylation profile of mammalian systems is not required. Viral vector producer cell line development — generating stable HEK293, SF9 (insect), or BHK-based producer lines for AAV, lentiviral, and adenoviral vectors — accounts for 12.4% of market revenue at USD 0.60 Billion and is the fastest-growing service category at an estimated 22.6% CAGR through 2034.

By Application

By application, monoclonal antibody development accounts for the largest share of the cell line development services market at 46.2% of revenue in 2025 at USD 2.25 Billion. Every approved or pipeline mAb product requires a unique production cell line, and the global mAb clinical pipeline — with over 600 active programs in clinical development as of 2025 — generates a sustained and growing pipeline of CLD mandates. IgG1, IgG2, IgG4, and bispecific antibody formats are the dominant mAb species requiring CLD, with bispecific antibodies presenting additional complexity due to their asymmetric heavy chain structure and the additional vector engineering required. Biosimilar development represents 21.6% of market revenue at USD 1.05 Billion, reflecting the substantial wave of originator biologic patent expirations in the 2022–2030 period. Biosimilar CLD programs require a production cell line that generates a protein with demonstrated analytical similarity to the reference product, necessitating iterative clone selection and glycoengineering to match originator glycosylation profiles within acceptable ranges. Recombinant protein and enzyme development accounts for 16.8% of revenue. Cell and gene therapy cell line development constitutes 11.6% of revenue and is the fastest-growing application category, as the commercial expansion of CGT programs requiring stable viral vector producer cell lines generates new CLD demand. Other applications including vaccine development contribute 3.8%.

By End-User

By end-user, biopharmaceutical companies represent the primary customer segment in the cell line development services market at 52.8% of market revenue in 2025 at USD 2.57 Billion. Large integrated biopharma companies outsource CLD for pipeline programs where proprietary internal expression systems are not available, or where timeline compression achievable with specialized CLD service providers is strategically valuable. Emerging and mid-sized biotechs — which typically lack internal CLD infrastructure — account for a disproportionate share of outsourced CLD mandates. CDMOs represent 28.4% of market revenue at USD 1.38 Billion, as integrated biologic CDMOs increasingly offer CLD as a gateway service that converts development relationships into long-term upstream manufacturing contracts. Academic and research institutions account for 12.6% of revenue, procuring CLD services for translational research programs and academic spin-out biologic development. Contract research organizations (CROs) contributing cell line development as part of broader biologic research programs account for the remaining 6.2%.

Regional Analysis

North America Cell Line Development Services Market

North America holds the leading position in the global cell line development services market with a 44.8% share in 2025, generating approximately USD 2.18 Billion in revenue. The United States dominates the regional market, hosting the world's highest concentration of biopharmaceutical companies, biologic CDMOs, and specialist CLD CROs. US-based biotech companies — including emerging biotechs in the San Francisco Bay Area, Boston/Cambridge, San Diego, and Research Triangle Park clusters — generate a substantial share of global CLD outsourcing mandates as they advance novel biologic programs from discovery through IND-enabling studies. The FDA's regulatory framework for biologics, including IND requirements for production cell line characterization under 21 CFR Part 610 and ICH Q5D documentation standards, defines the quality and technical requirements that CLD service providers must meet for US-market submissions. The US CDMO sector, which outsources CLD for client programs, is a growing buyer of cell line development services, as integrated biologics CDMOs add CLD to their upstream development service offerings. Canada contributes to regional demand through academic biologic research programs and growing biotechnology clusters in Toronto, Montreal, and Vancouver. North America's cell line development services market is projected to grow at a 11.6% CAGR through 2034, reaching approximately USD 5.72 Billion.

Europe Cell Line Development Services Market

Europe represents 28.4% of the global cell line development services market in 2025 at approximately USD 1.38 Billion. Germany, the United Kingdom, and Switzerland are the primary national markets, collectively hosting major biopharmaceutical companies, specialist CLD technology developers, and integrated CDMO operators offering upstream biologic development services. Germany is home to Sartorius Cellca — one of the leading specialist CHO CLD service providers globally — and to Boehringer Ingelheim BioXcellence, which offers its proprietary BI HEX CHO expression system through its CDMO division. The United Kingdom hosts FUJIFILM Diosynth Biotechnologies, Oxford Biomedica, and numerous academic-commercial partnerships contributing to CLD technology development and services. Switzerland's biopharma cluster generates significant CLD demand through Novartis and Roche biologic development programs, and through the operations of Lonza, whose proprietary GS Xceed CHO expression system is one of the most widely licensed CLD platforms globally. The EMA's guidelines on cell substrate characterization and the European Pharmacopoeia standards for cell banks are key regulatory frameworks governing European CLD service quality. Europe's cell line development services market is projected to grow at a 11.8% CAGR through 2034.

Asia Pacific Cell Line Development Services Market

Asia Pacific accounts for 18.6% of the global cell line development services market in 2025 at USD 0.90 Billion and is the fastest-growing region with a projected CAGR of 15.4% through 2034. China is the largest and fastest-growing national market, driven by the NMPA's progressive alignment with ICH standards and the extraordinary growth of domestic Chinese biopharmaceutical development. Chinese biologic developers are generating large volumes of CLD outsourcing demand for domestic CLD service providers including WuXi Biologics, as well as sourcing CLD services from international providers for programs targeting FDA and EMA regulatory pathways. WuXi Biologics operates one of the world's most scaled CLD service platforms, with the WHOA proprietary CHO expression system and automated high-throughput clone screening supporting hundreds of client programs simultaneously. South Korea's biopharmaceutical sector, anchored by Samsung Biologics and Celltrion, generates significant CLD demand through biosimilar and innovative biologic development programs; Samsung Biologics offers CLD services as part of its integrated CDMO platform. India's emerging biopharmaceutical sector, growing through domestic biologic development and CDMO expansion, is a nascent but growing source of CLD demand. Japan's established biopharma sector contributes steady CLD revenue through domestic development programs aligned with PMDA regulatory standards.

Latin America Cell Line Development Services Market

Latin America holds a 5.2% share of the cell line development services market in 2025 at approximately USD 0.25 Billion. Brazil is the dominant regional market, where domestic biopharmaceutical development programs at Fiocruz, Instituto Butantan, and private biologic developers generate CLD demand primarily addressed through outsourcing to international service providers. The Brazilian regulatory authority ANVISA's alignment with ICH standards supports the use of internationally-developed cell lines in Brazilian marketing authorization submissions. Mexico and Argentina contribute to regional demand through academic biologic research programs and emerging biosimilar development initiatives targeting domestic and regional markets. The Latin American cell line development services market remains largely dependent on North American and European service providers, as the region hosts no major proprietary CHO expression system developers. Brazil's active discussions with international biopharmaceutical companies regarding technology transfer agreements for biosimilar manufacturing have included CLD components, creating opportunities for regional capability buildout. Latin America's CLD market is projected to grow at a 10.2% CAGR through 2034.

Middle East & Africa Cell Line Development Services Market

The Middle East and Africa region accounts for 3.0% of global cell line development services market revenue in 2025 at approximately USD 0.15 Billion. The region's cell line development services market is primarily demand-side — pharmaceutical companies in the GCC and South Africa procuring CLD services from international providers for biosimilar and biologic development programs targeting domestic or export markets. Saudi Arabia's Vision 2030 pharmaceutical manufacturing strategy includes building domestic biopharmaceutical development capability, with several government-sponsored programs exploring CLD capacity building through international partnerships. The UAE's pharmaceutical free zones have attracted biotech company formation, some of which generate CLD outsourcing demand. South Africa's pharmaceutical sector, while primarily focused on small-molecule generic manufacturing, includes some biopharmaceutical development activity generating CLD demand. The MEA region's cell line development services market is expected to benefit over the forecast period from growing government investment in domestic biopharmaceutical capability, academic biologic research programs, and biosimilar development initiatives. MEA's CLD market is projected to grow at a 11.8% CAGR through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Service Type

- CHO Cell Line Development

- HEK293 & Human Cell Line Development

- Microbial (E. coli / Pichia) Cell Line Development

- Viral Vector Producer Cell Line Development

By Application

- Monoclonal Antibody Development

- Biosimilar Development

- Recombinant Protein & Enzyme Development

- Cell & Gene Therapy Cell Line Development

- Other Applications (Vaccines, Diagnostics)

By End-User

- Biopharmaceutical Companies

- Contract Development & Manufacturing Organizations (CDMOs)

- Academic & Research Institutions

- Contract Research Organizations (CROs)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.86 B |

| Forecast Revenue (2034) | USD 13.72 B |

| CAGR (2025-2034) | 12.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service Type, (CHO Cell Line Development, HEK293 & Human Cell Line Development, Microbial (E. coli / Pichia) Cell Line Development, Viral Vector Producer Cell Line Development), By Application, (Monoclonal Antibody Development, Biosimilar Development, Recombinant Protein & Enzyme Development, Cell & Gene Therapy Cell Line Development, Other Applications (Vaccines, Diagnostics)), By End-User, (Biopharmaceutical Companies, Contract Development & Manufacturing Organizations (CDMOs), Academic & Research Institutions, Contract Research Organizations (CROs)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | LONZA GROUP, THERMO FISHER SCIENTIFIC (PATHEON), WUXI BIOLOGICS, SARTORIUS AG (CELLCA), SAMSUNG BIOLOGICS, BOEHRINGER INGELHEIM BIOXCELLENCE, FUJIFILM DIOSYNTH BIOTECHNOLOGIES, CREATIVE BIOLABS, PROBIOGREN AG, BATAVIA BIOSCIENCES, MERCK KGAA (MILLIPORESIGMA), GENOPTIX (NOVARTIS SUBSIDIARY), ABZENA, CATALENT BIOLOGICS, RENTSCHLER BIOPHARMA, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Cell Line Development, Viral Vector Producer Cell Line Development), By Application, (Monoclonal Antibody Development, Biosimilar Development, Recombinant Protein & Enzyme Development, Cell & Gene Therapy Cell Line Development, Other Applications (Vaccines, Diagnostics)), By End-User, (Biopharmaceutical Companies, Contract Development & Manufacturing Organizations (CDMOs), Academic & Research Institutions, Contract Research Organizations (CROs)) Industry Trends & Forecast 2026–2034")

Cell Line Development, Viral Vector Producer Cell Line Development), By Application, (Monoclonal Antibody Development, Biosimilar Development, Recombinant Protein & Enzyme Development, Cell & Gene Therapy Cell Line Development, Other Applications (Vaccines, Diagnostics)), By End-User, (Biopharmaceutical Companies, Contract Development & Manufacturing Organizations (CDMOs), Academic & Research Institutions, Contract Research Organizations (CROs)) Industry Trends & Forecast 2026–2034")

Cell Line Development, Viral Vector Producer Cell Line Development), By Application, (Monoclonal Antibody Development, Biosimilar Development, Recombinant Protein & Enzyme Development, Cell & Gene Therapy Cell Line Development, Other Applications (Vaccines, Diagnostics)), By End-User, (Biopharmaceutical Companies, Contract Development & Manufacturing Organizations (CDMOs), Academic & Research Institutions, Contract Research Organizations (CROs)) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Cell Line Development Services Market?

Global Cell line development services market valued at USD 4.33B in 2024, reaching USD 13.72B by 2034, growing at a CAGR of 12.2% from 2026–2034.

Who are the major players in the Cell Line Development Services Market?

LONZA GROUP, THERMO FISHER SCIENTIFIC (PATHEON), WUXI BIOLOGICS, SARTORIUS AG (CELLCA), SAMSUNG BIOLOGICS, BOEHRINGER INGELHEIM BIOXCELLENCE, FUJIFILM DIOSYNTH BIOTECHNOLOGIES, CREATIVE BIOLABS, PROBIOGREN AG, BATAVIA BIOSCIENCES, MERCK KGAA (MILLIPORESIGMA), GENOPTIX (NOVARTIS SUBSIDIARY), ABZENA, CATALENT BIOLOGICS, RENTSCHLER BIOPHARMA, Others

Which segments covered the Cell Line Development Services Market?

By Service Type, (CHO Cell Line Development, HEK293 & Human Cell Line Development, Microbial (E. coli / Pichia) Cell Line Development, Viral Vector Producer Cell Line Development), By Application, (Monoclonal Antibody Development, Biosimilar Development, Recombinant Protein & Enzyme Development, Cell & Gene Therapy Cell Line Development, Other Applications (Vaccines, Diagnostics)), By End-User, (Biopharmaceutical Companies, Contract Development & Manufacturing Organizations (CDMOs), Academic & Research Institutions, Contract Research Organizations (CROs))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Cell Line Development Services Market

Published Date : 05 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date