- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Lab-Grown Meat Market to Reach $48.2 Bn by 2034 | CAGR 22.8%

Global Cellular Agriculture Market Size, Share, Analysis Report By Product Type (Beef, Poultry, Seafood, Pork, Others), Technology (Tissue Engineering, Cell Culture Technology, Bio-printing, Others), Application (Food Products, Nutritional Supplements, Food Service), End-User (Retail, Food and Beverage Industry, Restaurants), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

Report Overview

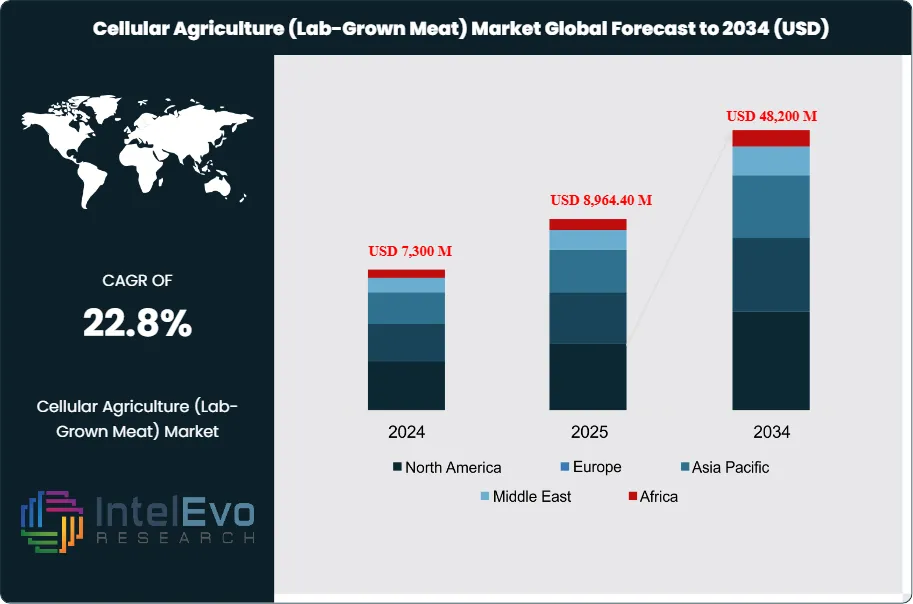

The Global Cellular Agriculture (Lab-Grown Meat) Market size is projected to reach approximately USD 48,200 million by 2034, up from USD 7,300 million in 2024, growing at a CAGR of 22.8% during the forecast period from 2024 to 2034. This growth is fueled by rising consumer demand for sustainable and ethical protein alternatives, coupled with increasing investments in food technology innovations. Supportive government regulations, environmental concerns, and the push for carbon-neutral food production are positioning lab-grown meat as a game-changer in the global protein industry.

Get More Information about this report -

Request Free Sample ReportThe Cellular Agriculture (Lab-Grown Meat) market represents a transformative shift in food production, involving the cultivation of animal cells in controlled environments to produce meat without raising or slaughtering animals. This innovative approach addresses significant environmental and ethical concerns associated with traditional livestock farming, including high greenhouse gas emissions, land use, and water consumption. The current market is rapidly evolving, fueled by advancements in biotechnology and changing consumer preferences. Increasing awareness of animal welfare and sustainability among consumers is driving the demand for lab-grown meat products, positioning them as a viable alternative to conventional meat.

The growth dynamics of the lab-grown meat market are underpinned by several key drivers. First, technological advancements in cellular biology and tissue engineering have led to improvements in the taste, texture, and nutritional profile of lab-grown meat, making it more appealing to consumers. Additionally, heightened concerns about food safety, health, and sustainability are encouraging shifts towards alternative protein sources. The market is further supported by favorable government policies and investments aimed at promoting food innovation.

Regionally, the lab-grown meat market exhibits varying growth patterns. North America currently leads the market, driven by significant investments from key players and a growing acceptance of alternative protein sources among consumers. The United States is at the forefront, with various startups and established companies advancing the commercialization of lab-grown meat. The Asia-Pacific region is also emerging as a critical player, particularly in countries like Singapore, which has become a pioneer in approving the sale of lab-grown meat. As consumer awareness about sustainability and food safety continues to rise, demand in Europe and Latin America is also expected to grow, contributing to the global expansion of the market.

The COVID-19 pandemic has had a notable impact on the lab-grown meat market, amplifying existing trends towards alternative protein sources. The pandemic highlighted vulnerabilities in traditional food supply chains, leading to increased consumer interest in sustainable and resilient food options. As people became more conscious of food safety and health, lab-grown meat gained traction as a reliable and ethically produced alternative. Additionally, disruptions in the livestock industry during the pandemic underscored the need for innovative food production methods, positioning lab-grown meat as a viable solution to ensure food security in future crises.

, Technology (Tissue Engineering, Cell Culture Technology, Bio-printing, Others), Application (Food Products, Nutritional Supplements, Food Service), End-User (Retail, Food and Beverage Industry, Restaurants), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Key Takeaways

- Market Growth: The cellular agriculture market is projected to reach USD $48,200 million by 2034, growing at a robust CAGR of 22.8%, indicating substantial market expansion driven by technological advancements and changing consumer preferences.

- Product Type Dominance: Beef is anticipated to dominate the market share due to its high consumption rates and consumer familiarity. The demand for lab-grown beef is driven by its potential to offer sustainable alternatives to conventional beef production.

- Technology Focus: Tissue engineering is leading the technological segment, enabling the development of lab-grown meat that closely mimics traditional meat in taste and texture. This innovation is crucial for gaining consumer acceptance and regulatory approval.

- Driver: Increasing concerns regarding animal welfare and sustainability are driving the demand for lab-grown meat. Consumers are seeking alternatives that reduce environmental impact while providing ethical food choices.

- Restraint: High production costs associated with lab-grown meat pose a significant challenge, potentially limiting its affordability and widespread adoption. Additionally, regulatory hurdles can delay market entry for new products.

- Opportunity: The growing investment in food technology and innovation offers significant growth opportunities. Partnerships between startups and established food companies can enhance research and development, accelerating market growth.

- Trend: The trend toward sustainable food production is influencing consumer preferences, with a notable shift toward plant-based and lab-grown alternatives as people seek healthier and more ethical food options.

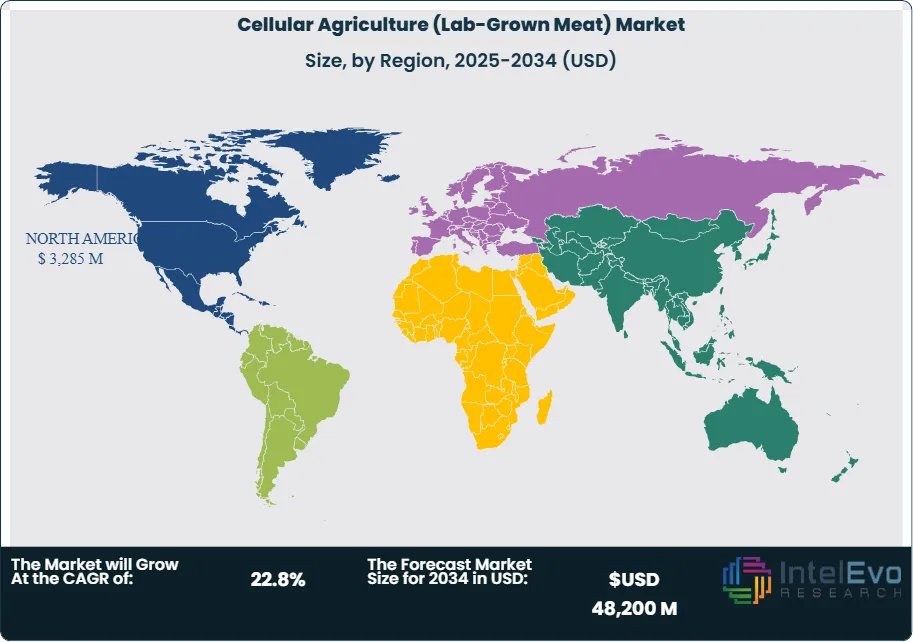

- Regional Analysis: North America is expected to lead the market, driven by innovation and consumer acceptance. The Asia-Pacific region is emerging as a significant player, particularly with regulatory support in countries like Singapore for lab-grown meat products.

Product Type

The product type segment of the cellular agriculture market is diversified, including beef, poultry, seafood, pork, and others. Beef is expected to dominate this segment due to its high consumption rates globally, coupled with increasing consumer demand for sustainable alternatives to conventional meat. Lab-grown poultry is also gaining traction, as it offers a familiar taste and is generally more accepted by consumers. Seafood products present a unique opportunity, given the environmental pressures on wild fish stocks. As consumers become more health-conscious and aware of the environmental impact of their food choices, the demand for lab-grown options across all product types is anticipated to grow significantly, reflecting a broader shift towards sustainable food sources.

Technology

The technology segment in the cellular agriculture market includes tissue engineering, cell culture technology, bio-printing, and others. Tissue engineering is the leading technology, involving the cultivation of animal cells in a nutrient-rich environment to produce muscle tissue that mimics traditional meat. This method is critical in developing lab-grown meat that meets consumer expectations for taste and texture. Cell culture technology, which allows for the scalable production of muscle cells, is also pivotal for market growth. Bio-printing, an emerging technology, involves 3D printing techniques to create complex tissue structures, thus holding significant potential for future innovations. As advancements in these technologies continue, the production processes will become more efficient and cost-effective, driving market acceptance and expansion.

Application

The application segment of the lab-grown meat market encompasses food products, nutritional supplements, and food service. The food products category is anticipated to hold the largest share, as consumers increasingly incorporate lab-grown meat into their diets. This segment includes ready-to-eat meals, burgers, and sausages, designed to appeal to various consumer preferences. Nutritional supplements that utilize lab-grown proteins are also emerging, particularly among health-conscious consumers looking for high-quality protein sources without the environmental impact of conventional meat production. The food service sector, including restaurants and catering services, is exploring lab-grown options to cater to evolving consumer demands. As more establishments embrace sustainable practices, the application segment is set to expand significantly.

End-User

The end-user segment in the cellular agriculture market is classified into retail, food and beverage industry, and restaurants. Retail is expected to capture a significant market share, driven by increasing consumer awareness of sustainable food practices and the availability of lab-grown meat products in grocery stores. The food and beverage industry is also a crucial player, with manufacturers looking to incorporate lab-grown ingredients into their offerings to meet consumer demand for healthier options. Restaurants are increasingly experimenting with lab-grown meat to attract a growing demographic of environmentally conscious diners. As acceptance of lab-grown products rises among consumers, all end-user segments will contribute to the overall growth of the market, shaping the future of meat consumption.

Region Analysis:

North America Leads with 45% Market Share in the Cellular Agriculture Market: North America holds a commanding share of approximately 45% in the cellular agriculture market, primarily driven by significant investments in research and development and a strong consumer inclination towards sustainable food options. The United States, in particular, is home to numerous startups and established firms pioneering lab-grown meat technologies, facilitating rapid innovation and product development. The region's robust infrastructure for food safety regulations further enhances the feasibility and acceptance of lab-grown products. Additionally, growing concerns about animal welfare and environmental sustainability resonate well with consumers, resulting in increased demand for lab-grown alternatives. Major companies in the U.S. are focusing on marketing strategies that emphasize the health benefits and ethical aspects of lab-grown meat, reinforcing the region's dominance in the global market.

The Asia-Pacific region is identified as the fastest-growing segment in the cellular agriculture market, driven by a rapidly urbanizing population and shifting dietary preferences towards protein-rich foods. Countries like Singapore are leading the charge, having established favorable regulatory frameworks that allow for the sale and distribution of lab-grown meat. This regulatory support, combined with rising disposable incomes and health-conscious consumers, is propelling growth in the region. Furthermore, the increasing focus on food security and sustainable practices in nations like China and India contributes to the region's expansion. While North America currently leads in market share, Asia-Pacific is projected to experience the highest CAGR, as more countries recognize the potential of lab-grown meat to meet their nutritional needs while addressing environmental challenges. Europe, Latin America, and the Middle East and Africa also show promise, with growing interest in sustainable food sources, albeit at a slower pace compared to Asia-Pacific.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Meat Type:

- Beef

- Poultry

- Pork

- Seafood

- Others

By Cell Type:

- Stem Cells

- Non-Stem Cells

By Production Technology

- Cell Culture Media

- Bioreactors & Scaffolding Systems

- 3D Printing & Tissue Engineering

- Others

By End-User:

- Food & Beverage Industry

- Retail & Supermarkets

- Foodservice / Restaurants

- Institutional Buyers

- Others

By Application:

- Food Products

- Nutritional Supplements

- Food Service

By Region:

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8,964.40 M |

| Forecast Revenue (2034) | USD 48,200 M |

| CAGR (2025-2034) | 22.8% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Meat Type:(Beef, Poultry, Pork, Seafood, Others), By Cell Type:(Stem Cells, Non-Stem Cells, By Production Technology, Cell Culture Media, Bioreactors & Scaffolding Systems, 3D Printing & Tissue Engineering, Others), By End-User:(Food & Beverage Industry, Retail & Supermarkets, Foodservice / Restaurants, Institutional Buyers, Others), By Application:(Food Products, Nutritional Supplements, Food Service) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Memphis Meats, Mosa Meat, Just Inc., Future Meat Technologies, Aleph Farms, Eat Just Inc., Upside Foods, SuperMeat, Cellular Agriculture Society, Geltor, Wild Type, Finless Foods, New Age Meats, Shiru, Believer Meats, The Better Meat Co., Primeval Foods, ProVeg International, Redefine Meat, STEM (Science Technology Engineering Medicine) |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Technology (Tissue Engineering, Cell Culture Technology, Bio-printing, Others), Application (Food Products, Nutritional Supplements, Food Service), End-User (Retail, Food and Beverage Industry, Restaurants), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Technology (Tissue Engineering, Cell Culture Technology, Bio-printing, Others), Application (Food Products, Nutritional Supplements, Food Service), End-User (Retail, Food and Beverage Industry, Restaurants), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Technology (Tissue Engineering, Cell Culture Technology, Bio-printing, Others), Application (Food Products, Nutritional Supplements, Food Service), End-User (Retail, Food and Beverage Industry, Restaurants), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Frequently Asked Questions

How big is the Cellular Agriculture (Lab-Grown Meat) Market?

Explore the Cellular Agriculture (Lab-Grown Meat) Market, projected to hit $48.2 billion by 2034 at a CAGR of 22.8%. Rising demand for sustainable proteins, ethical food choices, and carbon-neutral innovations drive this fast-growing market.

Who are the major players in the Cellular Agriculture (Lab-Grown Meat) Market?

Memphis Meats, Mosa Meat, Just Inc., Future Meat Technologies, Aleph Farms, Eat Just Inc., Upside Foods, SuperMeat, Cellular Agriculture Society, Geltor, Wild Type, Finless Foods, New Age Meats, Shiru, Believer Meats, The Better Meat Co., Primeval Foods, ProVeg International, Redefine Meat, STEM (Science Technology Engineering Medicine)

Which segments covered the Cellular Agriculture (Lab-Grown Meat) Market?

By Meat Type:(Beef, Poultry, Pork, Seafood, Others), By Cell Type:(Stem Cells, Non-Stem Cells, By Production Technology, Cell Culture Media, Bioreactors & Scaffolding Systems, 3D Printing & Tissue Engineering, Others), By End-User:(Food & Beverage Industry, Retail & Supermarkets, Foodservice / Restaurants, Institutional Buyers, Others), By Application:(Food Products, Nutritional Supplements, Food Service)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date