- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Central Bank Digital Currency Market Size, Share | CAGR 37.7%

Global Central Bank Digital Currency Market Size, Share, Growth Analysis By Type (Retail CBDC, Wholesale CBDC), By Architecture (Two-Tier, Hybrid, Single-Tier), By Technology (Distributed Ledger Technology, Centralized Ledger), By Application (Domestic Payments, Cross-Border Payments, Financial Inclusion, Programmable Payments), By End-User, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

|---|---|---|---|

| USD 295 Million | USD 5.40 Billion | 37.7% | Asia Pacific, 44.2% |

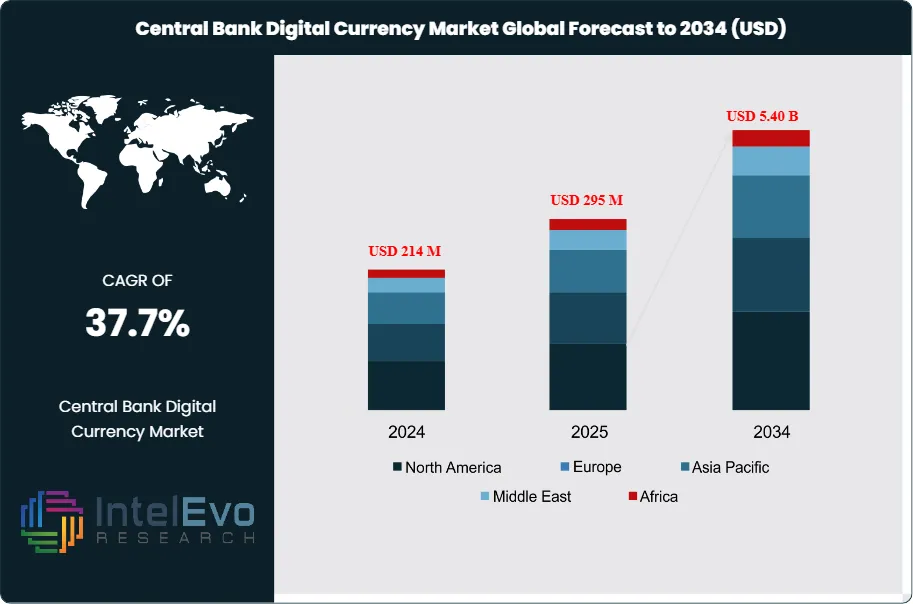

The Central Bank Digital Currency Market was valued at approximately USD 214 Million in 2024 and reached USD 295 Million in 2025. The market is projected to grow to USD 5.40 Billion by 2034, expanding at a CAGR of 37.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 5.10 Billion over the analysis period. The central bank digital currency market reflects a structural transition of sovereign money into programmable digital form, driven by monetary policy modernization, cross-border payment efficiency mandates, and responses to private stablecoins. Over 134 jurisdictions representing more than 98% of global GDP were in some phase of CBDC research, pilot, or launch by 2025, according to BIS surveys.

Get More Information about this report -

Request Free Sample ReportDemand momentum comes from three forces. First, central banks are seeking domestic payment infrastructure resilience, a priority reinforced after disruptions in legacy payment rails. Second, cross-border payments remain slow and expensive, with average correspondent banking costs at 6.2% of transaction value, pushing multilateral CBDC projects such as BIS Project Agorá, Project mBridge, and Project Cedar. Third, the rise of private stablecoins, with circulating supply surpassing USD 210 Billion in 2025, has accelerated sovereign responses. The European Central Bank moved the digital euro from investigation to preparation phase in late 2023 and continued toward implementation in 2025 and 2026. The People's Bank of China expanded e-CNY pilots to over 260 million wallets and 17 provinces by 2025. The Reserve Bank of India's eRupee surpassed 6.5 million retail users.

On the supply side, technology vendors have built specialized CBDC platforms that replace general-purpose blockchain stacks. Offerings focus on privacy-preserving cryptography, offline transaction capability, tiered intermediation, and programmable payments. Regulatory design is converging on a two-tier model, where central banks issue the currency while regulated intermediaries handle distribution and user-facing services. Interoperability with instant payment systems such as FedNow, SEPA Instant, PIX, and UPI is now a baseline requirement. Privacy and AML/CFT balance, KYC frameworks aligned with FATF standards, and cyber resilience under frameworks such as NIST and ENISA shape platform architecture.

Regional activity is concentrated in Asia Pacific, which holds the largest share due to advanced retail CBDC deployments in China, India, and pilot activity in Japan, Korea, and Australia. Europe and Latin America follow, with Brazil's Drex platform entering phased rollout and the digital euro preparation phase advancing. Key investment hotspots include wholesale CBDC settlement systems for institutional markets, multi-CBDC bridges for cross-border payments, and offline retail CBDC modules for financial inclusion. The central bank digital currency market is shifting from research and pilot phases into active procurement cycles for production-grade issuance and distribution infrastructure.

, By Architecture (Two-Tier, Hybrid, Single-Tier), By Technology (Distributed Ledger Technology, Centralized Ledger), By Application (Domestic Payments, Cross-Border Payments, Financial Inclusion, Programmable Payments), By End-User, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global central bank digital currency market reached USD 295 Million in 2025 and is projected to hit USD 5.40 Billion by 2034, expanding at a CAGR of 37.7% during 2026–2034.

- Segment Dominance: By type, retail CBDC led the market with a 62.4% share in 2025, driven by advanced deployments in China, India, and the Eastern Caribbean.

- Segment Dominance: By application, domestic payments captured the largest share at 54.8% in 2025, supported by consumer-facing rollouts and merchant acceptance programs.

- Driver: Cross-border payment inefficiency, with correspondent banking costs averaging 6.2% of transaction value in 2025, is driving multilateral CBDC projects such as Agorá and mBridge.

- Restraint: Privacy, surveillance, and banking disintermediation concerns delay retail CBDC launches in major Western economies, with 68% of surveyed banks flagging deposit-flight risk in 2025.

- Opportunity: Wholesale CBDC for tokenized securities settlement represents an addressable market of USD 1.6 Billion by 2034, linked to over USD 28 Trillion in projected tokenized real-world assets.

- Trend: Multi-CBDC bridges and interoperability platforms saw central bank participation exceed 41% by 2025, with projects such as mBridge moving to minimum viable product status.

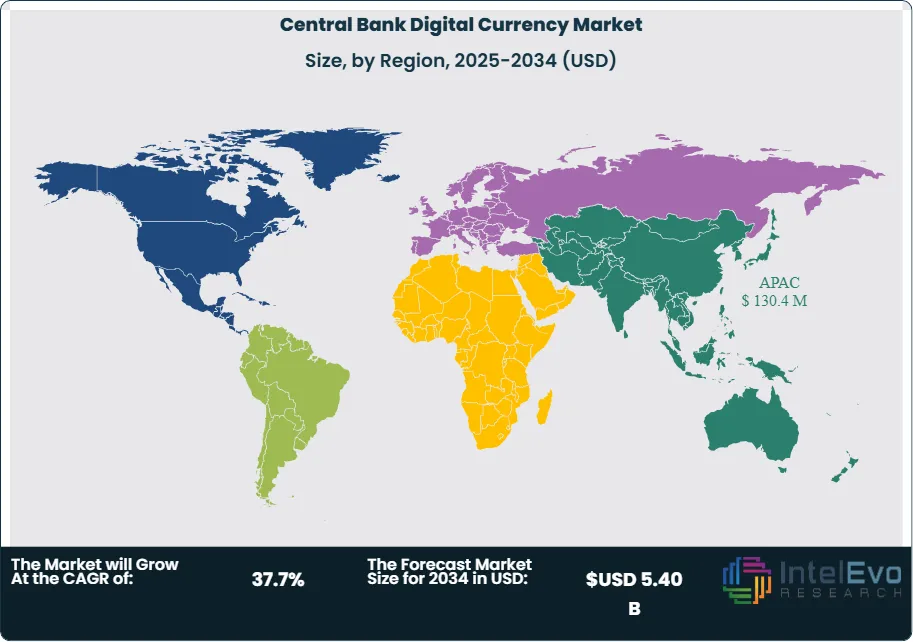

- Regional Analysis: Asia Pacific led the central bank digital currency market with a 44.2% share and USD 130.4 Million in revenue in 2025, supported by e-CNY scale and the eRupee rollout.

Competitive Landscape Overview

The central bank digital currency market is moderately concentrated at the technology-vendor tier and fragmented at the implementation services tier. The top four technology providers accounted for approximately 48.6% of vendor-attributed revenue in 2025. Competition is technology-driven, centered on privacy engineering, programmability, offline capability, and interoperability with instant payment systems. Strategic positioning has shifted since 2024, with pure-play blockchain firms specializing in central bank use cases and traditional payment-infrastructure vendors extending into token issuance. Joint ventures between technology firms and monetary authorities increasingly define the procurement model.

Competitive Landscape Matrix

| Company | HQ | Market Position | Key Product/Platform | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| R3 | USA/UK | Leader | Corda CBDC Platform | Europe, Asia Pacific | Selected for Project Agorá tokenized settlement, 2025 |

| Giesecke+Devrient | Germany | Leader | G+D Filia | Europe, MEA, LATAM | Selected by Central Bank of Thailand for retail pilot, 2025 |

| ConsenSys | USA | Leader | ConsenSys Codefi CBDC | North America, Europe | Expanded Hong Kong e-HKD phase 2 participation, 2025 |

| IBM | USA | Leader | IBM Digital Asset Platform | Global | Partnered on Monetary Authority of Singapore pilots, 2025 |

| Bitt | Barbados | Challenger | Bitt CBDC Solution | Latin America, Caribbean | Relaunched DCash under ECCB Phase II, 2025 |

| Ripple | USA | Challenger | Ripple CBDC Platform | Asia Pacific, MEA | Signed pilot agreements with Palau and Bhutan central banks, 2025 |

| Soramitsu | Japan | Niche Player | Sora / Bakong Platform | Asia Pacific | Expanded Cambodia Bakong cross-border integrations, 2025 |

| Thales Group | France | Niche Player | Gemalto Digital Currency | Europe, MEA | Launched offline CBDC wallet module, 2025 |

| Broadridge | USA | Niche Player | DLR Platform | North America, Europe | Extended tokenized repo processing to USD 1.6T, 2025 |

| eCurrency Mint | USA | Niche Player | DSC3 Platform | Africa, Caribbean | Partnered with Central Bank of Madagascar on pilot, 2026 |

By Type

Retail CBDC led the central bank digital currency market with a 62.4% share in 2025, translating to approximately USD 184.1 Million in revenue. This segment covers general-purpose digital cash for households and businesses, issued by central banks and distributed through commercial banks and licensed payment service providers. Deployment scale is led by the e-CNY in China, the eRupee in India, the Sand Dollar in the Bahamas, and the Nigerian eNaira. Retail CBDC design emphasizes offline functionality, privacy-preserving cryptography, and integration with national instant payment systems. Purchase cycles are long but contract values are substantial once production rollouts begin.

Wholesale CBDC accounted for the remaining 37.6%, representing USD 110.9 Million in 2025. This segment covers central bank money used for interbank settlement, securities delivery-versus-payment, and cross-border transactions among financial institutions. Wholesale projects include Project mBridge, Project Agorá, Project Cedar, Project Jura, and Project Helvetia. Wholesale CBDC revenue is growing faster than retail due to clearer regulatory pathways, institutional adoption of tokenized financial assets, and lower political sensitivity. Central banks have committed to at least 14 active wholesale pilots by 2025, with several advancing toward minimum viable products.

By Architecture

The two-tier intermediated architecture dominated with a 71.5% share in 2025, worth approximately USD 210.9 Million. In this design, the central bank issues the digital currency while commercial banks and payment service providers handle onboarding, KYC, wallet distribution, and customer service. This architecture preserves existing banking relationships, mitigates disintermediation risk, and is the preferred model in jurisdictions including the eurozone, the United Kingdom, Brazil, and Japan. Two-tier designs also simplify compliance with AML and sanctions frameworks.

Hybrid architectures held 19.4% share, valued at USD 57.2 Million, combining direct central bank claims on users with intermediated distribution. The Bahamas Sand Dollar and the eNaira deploy hybrid designs. Single-tier direct models captured the residual 9.1%, worth USD 26.8 Million, used in limited pilot contexts where the central bank operates the wallet and transaction layer directly. Direct models face scalability and operational burden concerns and are rarely adopted for large economies.

By Technology

Distributed ledger technology-based platforms led with 58.2% share in 2025, valued at USD 171.7 Million. Permissioned DLT frameworks, including Corda, Hyperledger Fabric, Besu, and bespoke national chains, dominate central bank procurement because they allow fine-grained access control, auditability, and programmability while avoiding the energy and governance issues of public chains. Centralized ledger designs captured 41.8%, worth USD 123.3 Million, and remain relevant in jurisdictions prioritizing throughput and regulatory simplicity, such as the e-CNY, which uses a centralized architecture with DLT-like features.

By Application

Domestic payments captured the largest application share at 54.8% in 2025, representing USD 161.7 Million. This category covers person-to-person transfers, merchant payments, government disbursements, and utility settlements. Growth is anchored by public-sector payment programs and merchant acceptance incentives in active retail CBDC jurisdictions. Cross-border payments held 26.4%, roughly USD 77.9 Million, supported by multilateral wholesale projects targeting reductions in settlement time from T+2 to near-instant and cost reductions of up to 50% compared with correspondent banking. Financial inclusion applications accounted for 12.6% at USD 37.2 Million, with initiatives targeting unbanked populations in Africa, the Caribbean, and South Asia. Monetary policy transmission and programmable payments covered the residual 6.2%, equivalent to USD 18.3 Million, covering conditional subsidy disbursement and targeted fiscal transfer use cases.

By End-User

Central banks represented the largest end-user category with a 48.6% share in 2025, valued at USD 143.4 Million. Procurement covers core issuance platforms, governance tooling, and oversight systems. Commercial banks accounted for 28.4%, equivalent to USD 83.8 Million, covering distribution node infrastructure, wallet middleware, and integration with core banking. Payment service providers and fintechs took 14.8% at USD 43.7 Million, driven by front-end wallet applications and merchant acquiring services. Retailers, merchants, and other businesses captured the residual 8.2%, roughly USD 24.2 Million, reflecting point-of-sale acceptance technology and treasury management integration.

Regional Analysis

The central bank digital currency market shows pronounced regional variation based on monetary authority ambition, domestic payment maturity, and stance toward digital assets.

Asia Pacific

Asia Pacific led the central bank digital currency market with a 44.2% share and USD 130.4 Million in revenue in 2025. China dominated with approximately USD 72.1 Million, driven by the e-CNY rollout that reached over 260 million wallets, 17 provinces, and cumulative transaction volume exceeding 7.3 trillion yuan. India contributed USD 21.5 Million, supported by the Reserve Bank of India's eRupee pilot, which expanded to 6.5 million retail users and over 400,000 merchants. Japan added USD 12.8 Million, with the Bank of Japan's Central Bank Digital Currency Forum progressing through pilot stages. Australia contributed USD 9.6 Million through the Reserve Bank of Australia's Project Acacia on wholesale CBDC. South Korea added USD 7.4 Million via Bank of Korea tokenized deposit trials. The region benefits from strong digital payment adoption, government-backed digitization agendas, and regulatory clarity for permissioned DLT. Project mBridge, led by the BIS Innovation Hub Hong Kong Centre with PBoC, HKMA, Bank of Thailand, UAE central bank, and Saudi Central Bank participation, remains the anchor multilateral initiative.

Europe

Europe captured a 24.8% share of the central bank digital currency market in 2025, valued at USD 73.2 Million. The eurozone contributed the bulk with the digital euro preparation phase, led by the European Central Bank. The ECB progressed through scheme rulebook drafting, procurement of technical service providers, and legislative processes in Brussels. The United Kingdom added meaningful revenue through the Bank of England and HM Treasury joint design phase on a digital pound. Switzerland contributed via Project Helvetia and Project Jura wholesale pilots operated by the Swiss National Bank. Sweden's Riksbank continued the e-krona proof of concept. Regulatory drivers include the Markets in Crypto-Assets Regulation, which creates clear boundaries between private crypto-assets and sovereign money, and the EU's payment services regulation modernization. European procurement favors consortia of incumbent payment infrastructure providers paired with DLT specialists, reflecting a preference for proven operational resilience.

North America

North America held a 13.6% share of the central bank digital currency market in 2025, valued at USD 40.1 Million. The United States contributed approximately USD 29.4 Million, driven by Federal Reserve research, the Federal Reserve Bank of New York Innovation Center's Project Cedar and Project Agorá participation, and Treasury-led policy work. US CBDC progress remained cautious due to congressional scrutiny, executive orders limiting retail CBDC issuance, and the parallel rise of regulated private stablecoins under the proposed payment stablecoin framework. Canada contributed USD 8.9 Million through the Bank of Canada's contingency planning and wholesale DLT trials. Mexico added USD 1.8 Million under Banxico's DiMo digital payments and exploratory CBDC work. Regional activity is concentrated in wholesale CBDC, tokenized securities settlement, and cross-border pilot participation. Political sensitivity around retail CBDC issuance has slowed consumer-facing work, but institutional and wholesale use cases continue to advance.

Latin America

Latin America accounted for 10.4% of the central bank digital currency market in 2025, valued at USD 30.7 Million, supported by some of the most advanced live CBDC implementations globally. Brazil led with USD 17.2 Million, driven by the Banco Central do Brasil's Drex platform, which entered phased production in 2025 with over 16 authorized financial institutions participating. Drex combines programmable money features with the established PIX instant payment system. The Eastern Caribbean Currency Union's DCash and the Central Bank of Jamaica's JAM-DEX continued live retail operations, with ECCB relaunching DCash Phase II in 2025 after platform upgrades. Mexico, Colombia, and Chile each maintained research and design-phase programs. The region benefits from a history of high inflation, large remittance corridors, and advanced domestic instant payment rails that favor CBDC experimentation. Political continuity of digital asset regulation remains a variable.

Middle East and Africa

Middle East and Africa captured the remaining 7.0% of the central bank digital currency market in 2025, valued at USD 20.7 Million. The United Arab Emirates led at USD 7.2 Million through the Central Bank of the UAE's Digital Dirham program under the Financial Infrastructure Transformation strategy, and participation in Project Aber with the Saudi Central Bank and in mBridge. Saudi Arabia contributed USD 5.1 Million through wholesale CBDC work and Project Aber. Nigeria added USD 3.4 Million, although the eNaira, launched in 2021, recorded modest retail uptake despite being one of the earliest live retail CBDCs. South Africa contributed USD 2.3 Million through the South African Reserve Bank's Project Khokha wholesale pilots. Israel, Ghana, Kenya, and Morocco each maintained active pilots or design-phase programs. The region balances financial inclusion ambitions in Africa with sovereign wealth-backed wholesale experimentation in the Gulf, producing a heterogeneous opportunity set for technology vendors.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Retail CBDC

- Wholesale CBDC

By Architecture

- Two-Tier (Intermediated)

- Hybrid

- Single-Tier (Direct)

By Technology

- Distributed Ledger Technology (DLT)

- Centralized Ledger

By Application

- Domestic Payments

- Cross-Border Payments

- Financial Inclusion

- Monetary Policy Transmission and Programmable Payments

By End-User

- Central Banks

- Commercial Banks

- Payment Service Providers and Fintechs

- Retailers, Merchants, and Businesses

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 295 M |

| Forecast Revenue (2034) | USD 5.40 B |

| CAGR (2025-2034) | 37.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type, (Retail CBDC, Wholesale CBDC), By Architecture, (Two-Tier (Intermediated), Hybrid, Single-Tier (Direct)), By Technology, (Distributed Ledger Technology (DLT), Centralized Ledger), By Application, (Domestic Payments, Cross-Border Payments, Financial Inclusion, Monetary Policy Transmission and Programmable Payments), By End-User, (Central Banks, Commercial Banks, Payment Service Providers and Fintechs, Retailers, Merchants, and Businesses) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | R3, GIESECKE+DEVRIENT (G+D), CONSENSYS, IBM CORPORATION, BITT INC., RIPPLE LABS, INC., SORAMITSU CO., LTD., THALES GROUP, BROADRIDGE FINANCIAL SOLUTIONS, ECURRENCY MINT LIMITED, NCHAIN GROUP, QUANT NETWORK, POLYGON LABS, ALGORAND FOUNDATION, STELLAR DEVELOPMENT FOUNDATION, NEXI GROUP (SIA), FIS GLOBAL, FINASTRA, HITACHI, LTD., FUJITSU LIMITED, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Architecture (Two-Tier, Hybrid, Single-Tier), By Technology (Distributed Ledger Technology, Centralized Ledger), By Application (Domestic Payments, Cross-Border Payments, Financial Inclusion, Programmable Payments), By End-User, Industry Trends & Forecast 2026-2034")

, By Architecture (Two-Tier, Hybrid, Single-Tier), By Technology (Distributed Ledger Technology, Centralized Ledger), By Application (Domestic Payments, Cross-Border Payments, Financial Inclusion, Programmable Payments), By End-User, Industry Trends & Forecast 2026-2034")

, By Architecture (Two-Tier, Hybrid, Single-Tier), By Technology (Distributed Ledger Technology, Centralized Ledger), By Application (Domestic Payments, Cross-Border Payments, Financial Inclusion, Programmable Payments), By End-User, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Central Bank Digital Currency Market?

The Global Central Bank Digital Currency Market was valued at USD 214 Million in 2024 and is projected to reach USD 5.40 Billion by 2034, growing at a CAGR of 37.7% from 2026 to 2034, driven by rising government initiatives for digital financial infrastructure, increasing adoption of blockchain and distributed ledger technologies, growing demand for secure cross-border payment systems, and expanding central bank CBDC pilot programs worldwide.

Who are the major players in the Central Bank Digital Currency Market?

R3, GIESECKE+DEVRIENT (G+D), CONSENSYS, IBM CORPORATION, BITT INC., RIPPLE LABS, INC., SORAMITSU CO., LTD., THALES GROUP, BROADRIDGE FINANCIAL SOLUTIONS, ECURRENCY MINT LIMITED, NCHAIN GROUP, QUANT NETWORK, POLYGON LABS, ALGORAND FOUNDATION, STELLAR DEVELOPMENT FOUNDATION, NEXI GROUP (SIA), FIS GLOBAL, FINASTRA, HITACHI, LTD., FUJITSU LIMITED, Others

Which segments covered the Central Bank Digital Currency Market?

By Type, (Retail CBDC, Wholesale CBDC), By Architecture, (Two-Tier (Intermediated), Hybrid, Single-Tier (Direct)), By Technology, (Distributed Ledger Technology (DLT), Centralized Ledger), By Application, (Domestic Payments, Cross-Border Payments, Financial Inclusion, Monetary Policy Transmission and Programmable Payments), By End-User, (Central Banks, Commercial Banks, Payment Service Providers and Fintechs, Retailers, Merchants, and Businesses)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Central Bank Digital Currency Market

Published Date : 21 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date