- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Chemically Defined Media Market Size & Forecast | CAGR 11.9%

Global Chemically Defined Media Market Size, Share, Growth & Industry Analysis By Media Type (Liquid CDM, Powder CDM, Liquid Concentrate, Dry Powder Reconstituted), By End-Use Application (Biopharmaceutical Manufacturing, Cell & Gene Therapy, Vaccine Production, Academic Research, Industrial Biotechnology), By Cell Type (CHO Cells, T Cells, Stem Cells, Viral Vector Cell Lines, Microbial Systems) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

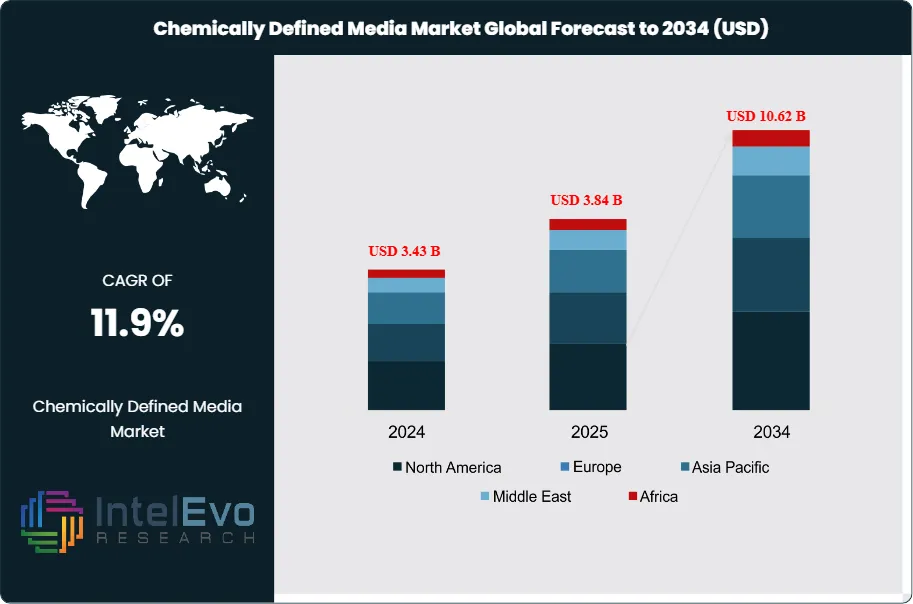

| USD 3.84 Billion | USD 10.62 Billion | 11.9% | North America, 40.6% |

The Chemically Defined Media Market was valued at approximately USD 3.43 Billion in 2024 and reached USD 3.84 Billion in 2025. The market is projected to grow to USD 10.62 Billion by 2034, expanding at a CAGR of 11.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 6.78 Billion over the analysis period, driven by accelerating adoption of animal-component-free manufacturing across biopharmaceuticals, cell and gene therapy, vaccine production, and the emerging cultivated food technology sector.

Get More Information about this report -

Request Free Sample ReportChemically defined media (CDM) are cell culture formulations in which every component is identified, characterized, and present at a known concentration. Unlike traditional serum-containing or protein-supplemented media, CDM provides full compositional transparency, enabling precise process control, superior lot-to-lot reproducibility, and regulatory documentation compliant with FDA and EMA requirements for biopharmaceutical manufacturing. The chemically defined media market has expanded well beyond its original pharmaceutical manufacturing application base and now encompasses a broad range of biological systems, including suspension CHO cell culture for monoclonal antibody production, T-cell expansion for CAR-T therapy, iPSC derivation and differentiation, viral vector biomanufacturing, and large-scale microbial fermentation for industrial enzymes and specialty biomolecules.

Several regulatory and commercial forces are structurally expanding the chemically defined media market. The FDA's ICH Q5A guideline on viral safety of biotechnology products effectively mandates elimination of animal-derived raw materials from biopharmaceutical manufacturing wherever technically feasible, as animal-derived components such as fetal bovine serum carry inherent adventitious agent risk that is difficult to fully mitigate. The EMA's guidelines on ATMPs under Regulation (EC) No 1394/2007 apply equivalent pressure across European cell and gene therapy developers. As of 2025, an estimated 82% of new monoclonal antibody BLA submissions in the United States incorporate chemically defined manufacturing processes, up from approximately 58% in 2020, reflecting a structural and accelerating regulatory ratchet.

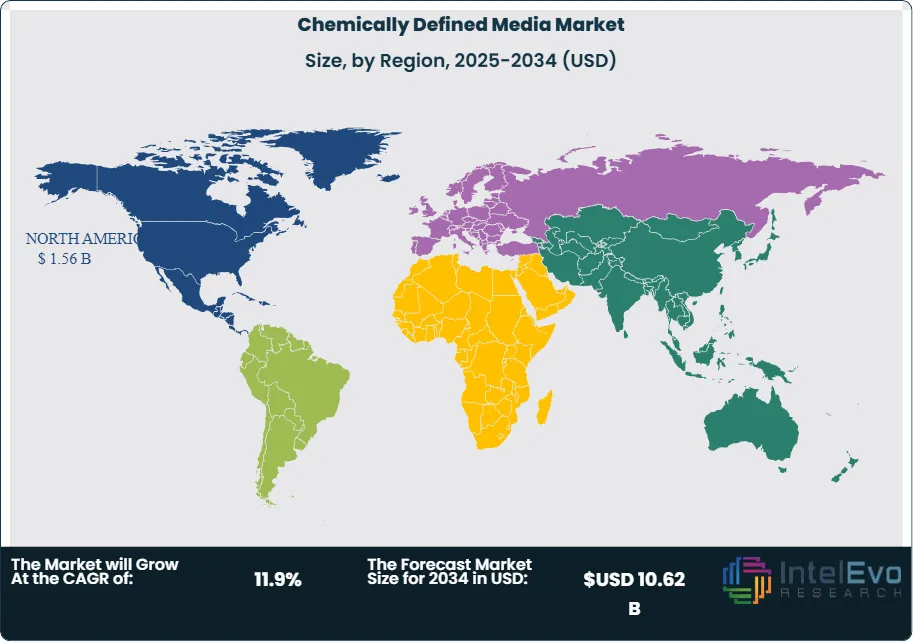

The cell and gene therapy sector provides the strongest near-term growth stimulus for the chemically defined media market. The global CGT pipeline exceeded 3,500 active clinical programs in 2025, according to ASGCT data, each requiring chemically defined, xeno-free media for clinical-grade cell expansion and viral vector production. Continuous biomanufacturing adoption by large pharmaceutical companies is also increasing CDM demand, as intensified perfusion processes require media formulations with precisely controlled nutrient delivery profiles that only chemically defined compositions can guarantee. North America dominated the chemically defined media market with a 40.6% share in 2025, equivalent to USD 1.56 Billion. Asia Pacific is the fastest-growing region, advancing at a projected CAGR of 14.2% through 2034, driven by biosimilar manufacturing expansion in South Korea and China and growing cell therapy programs in Japan and India.

, By End-Use Application (Biopharmaceutical Manufacturing, Cell & Gene Therapy, Vaccine Production, Academic Research, Industrial Biotechnology), By Cell Type (CHO Cells, T Cells, Stem Cells, Viral Vector Cell Lines, Microbial Systems) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global chemically defined media market was valued at USD 3.84 Billion in 2025 and is forecast to reach USD 10.62 Billion by 2034, registering a CAGR of 11.9% over the 2025-2034 forecast period.

- Segment Dominance: By media type, liquid chemically defined media held the largest share at 61.4% of the chemically defined media market in 2025, reflecting its dominance in large-scale suspension bioreactor operations for monoclonal antibody and viral vector manufacturing.

- Segment Dominance: By end-use application, biopharmaceutical manufacturing accounted for 48.6% of chemically defined media market revenues in 2025, driven by CHO cell-based monoclonal antibody production and the mandatory shift from serum-containing to chemically defined processes under ICH Q5A and FDA CBER guidance.

- Driver: The FDA and EMA's binding regulatory guidance on animal-component-free biopharmaceutical manufacturing is the primary structural driver, with new mAb BLA submissions incorporating chemically defined processes rising from 58% in 2020 to approximately 82% in 2025, compelling manufacturers to transition across their entire cell culture supply chains.

- Restraint: Premium pricing of pharmaceutical-grade chemically defined media, averaging 3-8 times the cost per liter of conventional serum-containing formulations, creates adoption barriers in cost-sensitive research and academic applications and constrains growth rates in Latin America, Middle East, and Africa.

- Opportunity: The global cell and gene therapy pipeline exceeded 3,500 active clinical programs in 2025, creating a rapidly expanding demand base for xeno-free, chemically defined expansion media for T cells, NK cells, and iPSC-derived products that is projected to generate an incremental CDM market opportunity of USD 2.1 Billion by 2034.

- Trend: Adoption of AI-assisted chemically defined media formulation optimization, which uses machine learning to predict optimal nutrient compositions for specific cell lines and bioreactor conditions, grew at approximately 21.6% annually in 2025, reducing CDM development timelines from months to weeks.

- Regional Analysis: North America led the chemically defined media market with a 40.6% share, equivalent to USD 1.56 Billion in 2025, sustained by the world's largest biopharmaceutical manufacturing base, active CGT clinical programs, and FDA regulatory frameworks that effectively mandate CDM adoption.

Competitive Landscape Overview

The chemically defined media market is moderately consolidated, with the top four suppliers — Thermo Fisher Scientific, Merck KGaA (MilliporeSigma), Sartorius AG, and Lonza Group AG — collectively accounting for approximately 54% of global market revenues in 2025. Competition centers on formulation depth and breadth, validated regulatory documentation packages, supply chain reliability at commercial scale, and speed of CDM customization for client-specific cell lines. M&A activity intensified in 2024-2025, with Sartorius expanding its CDM manufacturing footprint in Singapore and Cytiva (Danaher) launching a new perfusion-optimized CDM line to capture continuous biomanufacturing demand. Challengers including Nucleus Biologics and FUJIFILM Irvine Scientific are gaining share through AI-driven rapid formulation services and specialized xeno-free cell therapy CDM platforms.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Thermo Fisher Scientific | USA | Leader | CD OptiCHO & StemPro Chemically Defined Media | North America & Europe | Launched expanded CDM portfolio for viral vector and CAR-T manufacturing; Q1 2025. |

| Merck KGaA (MilliporeSigma) | Germany | Leader | EX-CELL Advanced CDM Series | Europe & North America | Introduced EX-CELL Advanced CHO high-titer fed-batch formulation validated at 8+ g/L; March 2025. |

| Sartorius AG | Germany | Leader | PM-CHO & Cell Culture CDM Solutions | Europe & Asia Pacific | Expanded chemically defined media manufacturing capacity in Singapore facility; Q2 2025. |

| Lonza Group AG | Switzerland | Leader | MOPS & LonzaBio CDM Platform | Europe & North America | Signed CDM supply agreement with top-5 biopharma company for commercial mAb manufacturing; Jan 2025. |

| Cytiva (Danaher) | USA | Challenger | HyClone CDM & ActiPro Chemically Defined | North America & Europe | Launched ActiPro chemically defined basal media for high-density perfusion CHO culture; Q3 2025. |

| FUJIFILM Irvine Scientific | USA | Challenger | IS CHO-CD & PRIME-XV Chemically Defined | North America & Asia Pacific | Expanded PRIME-XV xeno-free CDM platform to cover NK and gamma-delta T cell manufacturing; 2025. |

| Ajinomoto Co. | Japan | Challenger | CDM-HD & ASF104 Chemically Defined Media | Asia Pacific | Partnered with CDMO for CDM-HD supply in allogeneic cell therapy production; January 2026. |

| Corning Inc. | USA | Niche Player | BioCoat CDM & Synthecon Defined Media | North America | Launched chemically defined, ACF HEK293 suspension media for viral vector manufacturing; June 2025. |

| Nucleus Biologics | USA | Niche Player | Triton AI-Formulated CDM Platform | North America | Raised USD 55M Series C to scale AI-driven personalized chemically defined media; Feb 2025. |

| Pan-Biotech GmbH | Germany | Niche Player | Cell-Evo Chemically Defined Media | Europe | Released Cell-Evo CDM for iPSC and organoid research; expanded European distribution; 2025. |

By Media Type

The chemically defined media market by media type spans liquid CDM, powder CDM, liquid concentrate CDM, and dry powder reconstituted CDM formats. Liquid chemically defined media held the dominant share at 61.4% of the chemically defined media market in 2025, equivalent to approximately USD 2.36 Billion. Liquid CDM is preferred for large-scale suspension bioreactor operations because it eliminates the reconstitution step, reduces contamination risk during media preparation, and provides immediate use-ready formulations compatible with automated bioprocessing systems. Pharmaceutical manufacturers operating fed-batch and perfusion bioreactors at volumes of 2,000-20,000 liters routinely specify liquid CDM formats to ensure consistent nutrient concentrations at inoculation. Thermo Fisher Scientific's CD OptiCHO and Merck KGaA's EX-CELL Advanced series are the benchmark liquid CDM products for commercial-scale CHO monoclonal antibody manufacturing.

Powder chemically defined media held a 24.8% share of the CDM market in 2025, equivalent to approximately USD 952 Million. Powder CDM offers significant logistical advantages for high-volume manufacturing operations, as the dehydrated format reduces shipping weight and volume by approximately 90% compared to equivalent liquid volumes, lowers cold-chain requirements, and extends shelf life to 24-36 months versus 12-18 months for liquid formulations. Contract manufacturers operating at industrial scale in Asia Pacific and Latin America preferentially source powder CDM to manage supply chain costs. Liquid concentrate CDM, which requires dilution with water for injection before use, accounted for 9.6% of the chemically defined media market in 2025 and is gaining adoption in single-use bioprocessing environments where media preparation space is limited. Dry powder reconstituted CDM formulations held the remaining 4.2% share in 2025.

By End-Use Application

The chemically defined media market by end-use application reveals biopharmaceutical manufacturing as the dominant revenue segment, accounting for 48.6% of total CDM revenues in 2025, equivalent to approximately USD 1.87 Billion. Within this segment, CHO cell-based monoclonal antibody production is the largest sub-application. Monoclonal antibody manufacturing relies almost universally on chemically defined media in commercial-scale operations, as ICH Q5A viral safety requirements and FDA manufacturing change guidance make reversion to animal-derived media prohibitively complex from a regulatory standpoint. Bispecific antibodies, fusion proteins, and ADC drug substances produced in CHO cells represent additional growing applications within the biopharmaceutical CDM segment. Viral vector manufacturing for gene therapy, encompassing AAV and lentiviral vector production in HEK293 and Sf9 systems, is the fastest-growing biopharmaceutical sub-application, requiring specialized chemically defined suspension culture formulations validated to CBER standards.

Cell and gene therapy manufacturing represented 22.3% of the chemically defined media market in 2025. This application segment requires xeno-free, chemically defined media for T-cell expansion, NK cell expansion, iPSC derivation, and iPSC-to-cell-type differentiation, where any animal-derived component triggers regulatory review under FDA 21 CFR Part 1271 and EU ATMP regulation. Vaccine manufacturing accounted for 13.7% of CDM market revenues in 2025, with Vero cell-based and MDCK cell-based influenza vaccine platforms driving volume demand for chemically defined suspension culture media. Academic and research applications held 9.8% of the chemically defined media market in 2025, with growing NIH and Horizon Europe grant requirements specifying CDM use for reproducibility. Industrial biotechnology and other specialty applications collectively represented the remaining 5.6%.

By Cell Type

The chemically defined media market by cell type served encompasses CHO cells and other recombinant mammalian cell lines, human T cells and immune cells, iPSCs and pluripotent stem cells, viral vector production cell lines (HEK293, Sf9, Vero), and microbial systems. CHO cells and recombinant mammalian cell lines represented the dominant cell-type segment at 42.7% of the chemically defined media market in 2025, equivalent to USD 1.64 Billion. The Chinese Hamster Ovary cell platform has achieved the highest degree of CDM formulation optimization of any mammalian cell type, with multiple commercially validated fed-batch and perfusion CDM formulations achieving protein titers exceeding 8-12 grams per liter in clinical and commercial manufacturing bioreactors. This performance benchmark, achievable only with optimized chemically defined nutrients and feed strategies, has made CDM non-negotiable for CHO-based manufacturing operations competing on product cost of goods sold.

Human T cells and immune cells accounted for 19.4% of the chemically defined media market by cell type in 2025, driven by the rapid expansion of CAR-T, TCR-T, and NK cell therapy clinical programs requiring xeno-free, chemically defined T-cell activation and expansion media. iPSCs and pluripotent stem cells represented 14.8% of the cell-type segment in 2025, with application in both cell therapy manufacturing and pharmaceutical disease modeling. Viral vector production cell lines, primarily HEK293 for AAV and lentiviral vectors and Sf9 for baculovirus-expressed proteins, held 12.6% of the CDM market by cell type in 2025. Vero cells for vaccine manufacturing and microbial systems including E. coli and yeast for recombinant protein and enzyme production represented the remaining 10.5% of the chemically defined media market by cell type in 2025.

By End-User

The chemically defined media market by end-user segments into biopharmaceutical and biotechnology companies, contract development and manufacturing organizations (CDMOs), academic and government research institutions, cell and gene therapy developers, and vaccine manufacturers. Biopharmaceutical and biotechnology companies held the largest share at 45.8% of the CDM market in 2025, with large integrated pharmaceutical companies representing the highest-volume individual buyers of chemically defined media formulations. CDMOs accounted for 21.6% of the chemically defined media market in 2025, as CDMO clients increasingly mandate chemically defined manufacturing processes in their technology transfer and manufacturing service agreements, creating pass-through demand that CDMO operators satisfy through CDM procurement. Academic and government research institutions represented 16.4% of the end-user market in 2025. Cell and gene therapy developers held 11.3%, and vaccine manufacturers accounted for the remaining 4.9% of the chemically defined media market by end-user in 2025.

Regional Analysis

North America

North America chemically defined media market held a 40.6% share in 2025, generating approximately USD 1.56 Billion in revenue. The United States accounts for the vast majority of regional CDM demand, anchored by the world's largest concentration of commercial biopharmaceutical manufacturing facilities, an active cell and gene therapy clinical pipeline exceeding 1,800 US-based trials in 2025, and FDA regulatory frameworks that effectively mandate chemically defined manufacturing processes for new biologic drug submissions. Major US biopharmaceutical clusters in Massachusetts, New Jersey, California, and North Carolina host manufacturing operations for leading monoclonal antibody franchises that collectively consume hundreds of thousands of liters of CDM annually. The National Biotechnology and Biomanufacturing Initiative, extended by executive action in 2025, continues to direct federal resources toward domestic biomanufacturing infrastructure, with CDM supply chain resilience identified as a strategic priority following supply disruptions observed during the COVID-19 pandemic. BARDA's investments in advanced biomanufacturing preparedness also stimulate CDM adoption, as government-supported manufacturing facilities require chemically defined processes for rapid response drug substance manufacturing. Canada contributes through Montreal and Toronto-based biotech clusters, while Mexico represents an emerging growth market for CDM as its pharmaceutical manufacturing sector progressively aligns with ICH guidelines.

Europe

Europe chemically defined media market represented 27.9% of global revenues in 2025, equivalent to approximately USD 1.07 Billion. Germany is the largest national CDM market within Europe, housing major CDM producers including Merck KGaA and Pan-Biotech alongside a dense biopharmaceutical manufacturing base at companies including Bayer, Boehringer Ingelheim, and BioNTech. The EMA's GMP guidelines for ATMPs under Regulation (EC) No 1394/2007 have made chemically defined manufacturing conditions a de facto requirement for cell and gene therapy products across EU member states, creating sustained structural demand. Switzerland contributes significantly through the Lonza Group's CDM manufacturing and supply operations centered in Visp and Basel, where the company serves global pharmaceutical clients as both a CDM supplier and CDMO. The United Kingdom's MHRA has aligned its biopharmaceutical manufacturing guidance with EMA CDM requirements, supporting sustained demand from the UK's active CAR-T and gene therapy development sector. Denmark benefits from proximity to Novonesis's bioprocessing infrastructure and hosts growing cell therapy biotech activity that drives CDM adoption. The EU Horizon Europe program's continued funding of biomanufacturing research projects across member states sustains academic CDM demand and generates early-stage commercial application development.

Asia Pacific

Asia Pacific held approximately 22.4% of the global chemically defined media market in 2025, generating USD 860 Million, and represents the fastest-growing regional market at a projected CAGR of 14.2% through 2034. South Korea is the most technically sophisticated CDM consumer in the region, driven by Samsung Biologics, Celltrion, and other biosimilar manufacturers that have substantially completed FBS phaseout across their commercial CHO manufacturing operations and now source large volumes of chemically defined media for 10,000-liter-scale bioreactors. China is the largest Asia Pacific CDM market by revenue, where rapid biosimilar and monoclonal antibody manufacturing capacity expansion at WuXi Biologics, Zymeworks Biologics, and other CDMOs is generating growing chemically defined media procurement volumes. China's NMPA has progressively strengthened its cGMP requirements to align with ICH Q5A, directly incentivizing domestic manufacturers to transition to CDM-based processes for international market access. Japan's cell therapy sector, regulated under the Act on the Safety of Regenerative Medicine and supported by PMDA guidance, requires chemically defined conditions for clinical-grade cell manufacturing, sustaining demand for specialized xeno-free CDM from Ajinomoto Co. and other suppliers. India is the fastest-growing individual national CDM market within Asia Pacific, as its large generic pharmaceutical manufacturing sector begins adopting biologic and biosimilar production platforms requiring chemically defined media.

Latin America

Latin America held approximately 5.8% of the chemically defined media market in 2025, generating approximately USD 223 Million. Brazil is the dominant regional CDM market, where ANVISA's biopharmaceutical GMP regulations are progressively aligning with ICH guidelines, compelling manufacturers producing biologics for domestic consumption or export to document and justify any animal-derived component use in their manufacturing dossiers. Public health institutions including FIOCRUZ have implemented CDM use requirements for government-funded vaccine and biologic manufacturing programs, creating institutional demand for pharmaceutical-grade chemically defined media at scale. Argentina represents the second-largest Latin American CDM market, where domestic pharmaceutical companies targeting export markets to Europe and North America are proactively adopting CDM to satisfy international regulatory requirements. Mexico contributes through pharmaceutical contract manufacturing operations linked to global biopharmaceutical companies that mandate CDM as a condition of technology transfer agreements. Regional growth is constrained by the premium cost of pharmaceutical-grade CDM relative to local purchasing power, limited domestic CDM manufacturing capability, and cold-chain logistics challenges for liquid formulations in tropical climates.

Middle East & Africa

The Middle East and Africa region held approximately 3.3% of the global chemically defined media market in 2025, generating approximately USD 127 Million. Saudi Arabia and the UAE are the primary demand centers within the region, where government biotechnology investment programs under Saudi Vision 2030 and the UAE National Innovation Strategy are funding construction of biopharmaceutical manufacturing facilities that reference FDA and EMA manufacturing standards. The King Abdulaziz City for Science and Technology in Saudi Arabia has supported domestic biopharmaceutical research programs that require chemically defined cell culture conditions. South Africa leads the African CDM market through vaccine manufacturing programs at the Biovac Institute and Aspen Pharmacare, both of which are transitioning manufacturing processes toward animal-component-free conditions to satisfy WHO prequalification requirements for vaccine supply programs. Israel, while geographically small, contributes disproportionately to the regional CDM market through a concentrated biotech sector with multiple cell therapy and biologics companies conducting early-phase clinical programs requiring xeno-free CDM. The region's overall CDM market remains heavily dependent on imported formulations from North American and European suppliers, creating supply chain vulnerability that government industrial policy in Saudi Arabia and the UAE is beginning to address through domestic biomanufacturing incentive programs.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Media Type

- Liquid Chemically Defined Media

- Powder Chemically Defined Media

- Liquid Concentrate CDM

- Dry Powder Reconstituted CDM

By End-Use Application

- Biopharmaceutical Manufacturing

- Cell & Gene Therapy Manufacturing

- Vaccine Manufacturing

- Academic & Research Applications

- Industrial Biotechnology & Others

By Cell Type

- CHO Cells & Recombinant Mammalian Cell Lines

- Human T Cells & Immune Cell Types

- iPSCs & Pluripotent Stem Cells

- Viral Vector Production Cell Lines (HEK293, Sf9, Vero)

- Microbial Systems

By End-User

- Biopharmaceutical & Biotechnology Companies

- Contract Development & Manufacturing Organizations (CDMOs)

- Academic & Government Research Institutions

- Cell & Gene Therapy Developers

- Vaccine Manufacturers

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.84 B |

| Forecast Revenue (2034) | USD 10.62 B |

| CAGR (2025-2034) | 11.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Media Type, (Liquid Chemically Defined Media, Powder Chemically Defined Media, Liquid Concentrate CDM, Dry Powder Reconstituted CDM), By End-Use Application, (Biopharmaceutical Manufacturing, Cell & Gene Therapy Manufacturing, Vaccine Manufacturing, Academic & Research Applications, Industrial Biotechnology & Others), By Cell Type, (CHO Cells & Recombinant Mammalian Cell Lines, Human T Cells & Immune Cell Types, iPSCs & Pluripotent Stem Cells, Viral Vector Production Cell Lines (HEK293, Sf9, Vero), Microbial Systems), By End-User, (Biopharmaceutical & Biotechnology Companies, Contract Development & Manufacturing Organizations (CDMOs), Academic & Government Research Institutions, Cell & Gene Therapy Developers, Vaccine Manufacturers) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | THERMO FISHER SCIENTIFIC, MERCK KGAA (MILLIPORESIGMA), SARTORIUS AG, LONZA GROUP AG, CYTIVA (DANAHER), FUJIFILM IRVINE SCIENTIFIC, AJINOMOTO CO., CORNING INC., NUCLEUS BIOLOGICS, PAN-BIOTECH GMBH, PROMOCELL GMBH, HIMEDIA LABORATORIES, BIOLOGICAL INDUSTRIES (SARTORIUS), BIOWEST SAS, CELLERO (NOVATEK INTERNATIONAL), ADVANCED INSTRUMENTS (AI BIOSCIENCES), OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-Use Application (Biopharmaceutical Manufacturing, Cell & Gene Therapy, Vaccine Production, Academic Research, Industrial Biotechnology), By Cell Type (CHO Cells, T Cells, Stem Cells, Viral Vector Cell Lines, Microbial Systems) Industry Trends & Forecast 2026–2034")

, By End-Use Application (Biopharmaceutical Manufacturing, Cell & Gene Therapy, Vaccine Production, Academic Research, Industrial Biotechnology), By Cell Type (CHO Cells, T Cells, Stem Cells, Viral Vector Cell Lines, Microbial Systems) Industry Trends & Forecast 2026–2034")

, By End-Use Application (Biopharmaceutical Manufacturing, Cell & Gene Therapy, Vaccine Production, Academic Research, Industrial Biotechnology), By Cell Type (CHO Cells, T Cells, Stem Cells, Viral Vector Cell Lines, Microbial Systems) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Chemically Defined Media Market?

Global Chemically defined media market valued at USD 3.43B in 2024, reaching USD 10.62B by 2034, growing at a CAGR of 11.9% during 2026–2034.

Who are the major players in the Chemically Defined Media Market?

THERMO FISHER SCIENTIFIC, MERCK KGAA (MILLIPORESIGMA), SARTORIUS AG, LONZA GROUP AG, CYTIVA (DANAHER), FUJIFILM IRVINE SCIENTIFIC, AJINOMOTO CO., CORNING INC., NUCLEUS BIOLOGICS, PAN-BIOTECH GMBH, PROMOCELL GMBH, HIMEDIA LABORATORIES, BIOLOGICAL INDUSTRIES (SARTORIUS), BIOWEST SAS, CELLERO (NOVATEK INTERNATIONAL), ADVANCED INSTRUMENTS (AI BIOSCIENCES), OTHERS

Which segments covered the Chemically Defined Media Market?

By Media Type, (Liquid Chemically Defined Media, Powder Chemically Defined Media, Liquid Concentrate CDM, Dry Powder Reconstituted CDM), By End-Use Application, (Biopharmaceutical Manufacturing, Cell & Gene Therapy Manufacturing, Vaccine Manufacturing, Academic & Research Applications, Industrial Biotechnology & Others), By Cell Type, (CHO Cells & Recombinant Mammalian Cell Lines, Human T Cells & Immune Cell Types, iPSCs & Pluripotent Stem Cells, Viral Vector Production Cell Lines (HEK293, Sf9, Vero), Microbial Systems), By End-User, (Biopharmaceutical & Biotechnology Companies, Contract Development & Manufacturing Organizations (CDMOs), Academic & Government Research Institutions, Cell & Gene Therapy Developers, Vaccine Manufacturers)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Chemically Defined Media Market

Published Date : 18 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date