- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Circular Saw Blade Market Size Growth & Forecast | CAGR of 6.1%

Global Circular Saw Blade Market Size, Share & Analysis By Type (Carbide Saw Blades, Diamond Saw Blades, Others), By Application (Stone Cutting, Metal Materials Cutting, Wood Cutting), Tool Performance Trends, Competitive Landscape & Forecast 2025–2034

Report Overview

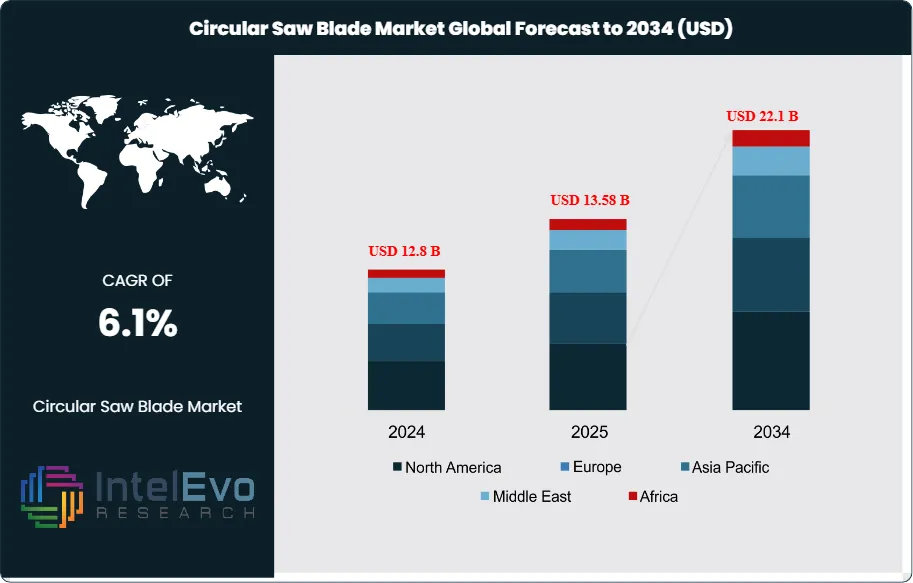

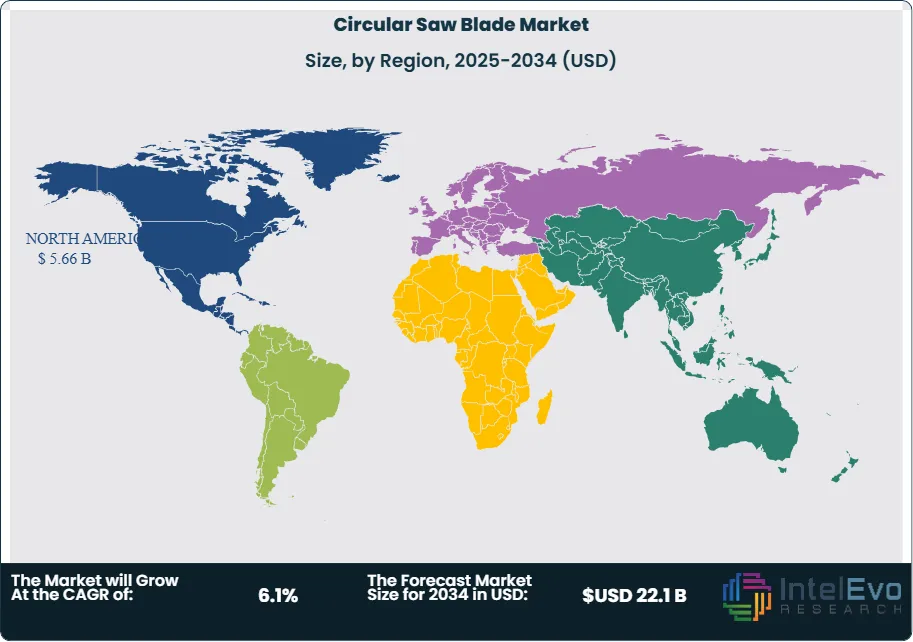

The Circular Saw Blade Market is valued at approximately USD 12.8 Billion in 2024 and is projected to reach nearly USD 22.1 Billion by 2034, expanding at a CAGR of about 6.1% during 2025–2034. Demand is accelerating as construction, woodworking, and metal fabrication industries adopt high-performance carbide, diamond-tipped, and precision-engineered blades for better accuracy and durability. Rising automation in manufacturing, along with rapid growth of home renovation and DIY activities, continues to strengthen global market momentum.

Get More Information about this report -

Request Free Sample ReportThis steady expansion reflects the growing role of saw blades as indispensable tools in woodworking, metalworking, and construction industries worldwide. Historically, market demand has been tied closely to infrastructure development, housing starts, and industrial manufacturing trends, and the current decade is expected to witness further acceleration as global construction activity rebounds and precision cutting solutions become integral to advanced manufacturing.

A key growth driver is the rapid pace of innovation in material science and production processes. Carbide, diamond-tipped, and specialty alloy blades are increasingly adopted due to their superior durability, precision, and cost efficiency. Investments in robotics, automation, and data-driven manufacturing are also reshaping the competitive landscape. For instance, industry surveys indicate that more than 60% of manufacturers are integrating automation and analytics into blade production, significantly enhancing productivity and reducing operational downtime. These advances enable the creation of specialized blades for diverse applications, from high-speed industrial cutting to precision woodworking, thereby expanding addressable market segments.

On the demand side, the global push toward urbanization and industrialization, particularly in Asia-Pacific and parts of Latin America, continues to underpin market growth. The Asia-Pacific region accounts for the largest revenue share, supported by China and India’s large-scale construction pipelines and rising investments in smart manufacturing. Meanwhile, North America and Europe remain critical due to strong demand for advanced tooling in high-value manufacturing and stringent safety and quality standards. Emerging economies in Southeast Asia and the Middle East present new investment hotspots, driven by infrastructure development and increased adoption of modern woodworking and metal fabrication technologies.

Nonetheless, the market faces challenges, including raw material price volatility, supply chain disruptions, and the need for continuous adaptation to new environmental and regulatory requirements. Energy efficiency, recyclability of blade materials, and workplace safety standards are shaping purchasing decisions, compelling manufacturers to adopt sustainable production practices. Overall, the market’s forward trajectory will be defined by its ability to balance technological innovation with cost competitiveness, while capturing growth opportunities in high-potential emerging markets.

, By Application (Stone Cutting, Metal Materials Cutting, Wood Cutting), Tool Performance Trends, Competitive Landscape & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global Circular Saw Blade market was valued at USD 12.8 Billion in 2024 and is projected to reach USD 22.1 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 6.1%. This growth is primarily fueled by increasing demand from the construction, woodworking, and metal fabrication industries, alongside rapid technological advancements in blade manufacturing.

- Product Type: Carbide saw blades lead the market with a substantial 55.2% revenue share in 2024. Their superior durability, precision cutting capability, and longer operational lifespan make them the preferred choice across industrial and professional-grade applications.

- Application: Stone cutting applications account for the largest share at 41.2% in 2024, driven by high-volume demand from the construction and infrastructure sectors, particularly in emerging economies with large-scale urban development projects.

- Driver: Technological investments are a major growth catalyst; for instance, 62% of woodworking machinery manufacturers are adopting robotics, 60% are leveraging data analytics, and 39% are integrating IoT solutions. These advancements significantly improve blade performance, reduce downtime, and enable production of specialized, high-precision tools.

- Restraint: Price volatility in raw materials—especially tungsten carbide and steel—poses a challenge for manufacturers, impacting production costs and profit margins. Fluctuations in global metal supply chains further exacerbate this issue, particularly for export-dependent producers.

- Opportunity: The Asia-Pacific region, led by China and India, presents robust growth potential with double-digit increases in construction expenditure and industrial manufacturing output. This region is expected to outpace global averages, making it a critical focus for market expansion and localized production investment.

- Trend: The rising adoption of automated and smart manufacturing processes, including CNC-enabled blade sharpening systems and predictive maintenance tools, is reshaping competitive dynamics. Companies like Freud and Leitz are investing in digital production lines to meet evolving industry standards and customer demands.

- Regional Analysis: North America dominates the global market with a 41.7% share in 2023, supported by high-end manufacturing infrastructure and early adoption of advanced technologies. Meanwhile, Asia-Pacific is the fastest-growing region, projected to register a CAGR above the global average, driven by rapid industrialization and infrastructure development.

Type Analysis

Carbide saw blades continue to hold a dominant position in the global circular saw blade market, accounting for approximately 55.2% of total revenue share as of 2025. Their extensive use across multiple end-use industries stems from their superior edge retention, high-temperature tolerance, and ability to cut through dense materials with minimal wear. These blades are particularly favored in the construction, woodworking, and metal fabrication sectors, where precision, efficiency, and durability are critical. The demand is further bolstered by increased automation in manufacturing, where carbide blades are compatible with CNC machines and robotic cutting systems.

Diamond saw blades represent the second most significant product segment, particularly for applications involving abrasive and mineral-based materials such as concrete, asphalt, ceramics, and stone. Their popularity is driven by their extended lifespan and cutting efficiency, especially in infrastructure projects and heavy-duty industrial settings. As infrastructure investments surge across Asia, the Middle East, and Latin America, the segment is expected to expand at a healthy pace, supported by rising demand in civil engineering and urban development.

The "Others" category—including high-speed steel (HSS) and abrasive blades—occupies a smaller but specialized share of the market. These blade types serve niche applications such as fine metal cutting, non-ferrous materials, and general-purpose industrial uses. Despite their lower market penetration, innovations in blade coating and design have enhanced their cutting performance and cost efficiency, ensuring continued relevance in specific industrial niches.

Application Analysis

Stone cutting applications continue to dominate the circular saw blade market, capturing approximately 41.2% of the application-based revenue share in 2025. This leadership reflects sustained global investment in commercial and residential construction, particularly in large-scale infrastructure projects that require cutting of granite, concrete, and other dense materials. The growth of prefabricated construction and increased architectural demand for stone finishes are further strengthening this segment.

Metal cutting is another major application area, driven by heightened demand in manufacturing-intensive sectors such as automotive, aerospace, and heavy machinery. With global industrial production showing signs of post-pandemic recovery and governments promoting localized manufacturing, the demand for metal-cutting blades is expected to grow steadily. Advancements in metallurgy and coating technologies are also enhancing the cutting speed and longevity of blades used for metals.

While wood cutting holds a comparatively smaller share, it remains an essential application within furniture production, residential carpentry, and panel fabrication. The increasing popularity of modular construction and DIY woodworking—especially in North America and Europe—continues to support demand in this segment. Additionally, the push toward sustainable building materials has prompted the use of engineered woods, which require specialized saw blades for precision cutting, contributing to segment resilience.

End-Use Analysis

In 2025, residential construction emerges as the leading end-use sector for circular saw blades, underpinned by ongoing housing demand, urban redevelopment, and increased home renovation activities. The segment benefits from the widespread use of circular saws in roofing, flooring, framing, and cabinetry. Particularly in North America and Asia Pacific, strong consumer spending on home improvement and government-backed affordable housing initiatives are key growth drivers.

The commercial building segment is also expanding, supported by sustained investment in offices, retail spaces, educational facilities, and healthcare infrastructure. As global economies prioritize modernization of public infrastructure and smart city development, circular saw blades are increasingly utilized for structural framing, HVAC installation, and interior fittings. Moreover, the rise in green building certifications is encouraging the use of precision-cut materials, increasing reliance on high-performance saw blades.

Industrial construction, including factories, warehouses, and utility structures, contributes steadily to market demand. The rise of automation, expansion of logistics hubs, and energy infrastructure projects—especially in Asia and the Middle East—are boosting blade usage in industrial fabrication and assembly operations. Circular saw blades used in this sector typically demand high endurance and compatibility with automated systems, driving innovation in blade design and materials.

Regional Analysis

North America remains the largest regional market for circular saw blades, commanding an estimated 41.7% share of global revenue in 2025. This is primarily due to mature construction and manufacturing industries in the U.S. and Canada, where there is consistent demand across wood, metal, and stone-cutting applications. Technological integration in production, including IoT-enabled equipment and advanced automation, further enhances product usage across end-use sectors.

Europe exhibits stable growth, with key markets such as Germany, France, and the UK investing in both industrial modernization and sustainable building initiatives. The region’s stringent safety and quality regulations favor high-grade circular saw blades, encouraging manufacturers to develop precision-engineered products. Demand from the furniture manufacturing sector, particularly in Italy and Poland, continues to sustain wood-cutting blade sales.

Asia Pacific represents the most dynamic and fastest-growing region, fueled by rapid industrialization, expanding urban infrastructure, and growing manufacturing output in countries like China, India, Japan, and South Korea. The region is expected to witness the highest CAGR over the forecast period, supported by government infrastructure projects, private sector construction investments, and a growing middle class driving residential construction and renovations.

Latin America and the Middle East & Africa are emerging markets showing steady potential. Infrastructure development plans such as Brazil’s public works programs and the UAE’s smart city initiatives are driving blade demand. However, economic uncertainties, import dependencies, and currency fluctuations pose near-term challenges. Despite these constraints, localized manufacturing and rising construction activity offer long-term growth opportunities in these regions.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Carbide Saw Blades

- Diamond Saw Blades

- Others

By Application

- Stone Cutting

- Metal Materials Cutting

- Wood Cutting

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 12.8 B |

| Forecast Revenue (2034) | USD 22.1 B |

| CAGR (2024-2034) | 6.1% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Carbide Saw Blades, Diamond Saw Blades, Others), By Application (Stone Cutting, Metal Materials Cutting, Wood Cutting) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Robert Bosch GmbH, HUANGHE WHIRLWIND, Stanley Black and Decker, BOSUN, Freud SpA, General Saw, Hilti Corporation, STARK SpA, Lenox, Tenryu Saw Mfg. Co. Ltd., Tangshan Metallurgical Saw Blade, DEWALT |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Stone Cutting, Metal Materials Cutting, Wood Cutting), Tool Performance Trends, Competitive Landscape & Forecast 2025–2034")

, By Application (Stone Cutting, Metal Materials Cutting, Wood Cutting), Tool Performance Trends, Competitive Landscape & Forecast 2025–2034")

, By Application (Stone Cutting, Metal Materials Cutting, Wood Cutting), Tool Performance Trends, Competitive Landscape & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date