- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Circulating Tumor Cell Analysis Market Forecast | CAGR 13.7%

Global Circulating Tumor Cell Analysis Market Size, Share, Growth Analysis By Product (Instruments, Consumables, Software), By Technology (CTC Enrichment, Detection, Molecular Characterization), By Application (Diagnosis, Prognosis, Treatment Monitoring), By End-User (Hospitals, Diagnostic Labs, Research Institutes, Pharma & Biotech) Regional Outlook, Key Players – Dynamics, Liquid Biopsy Tech Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

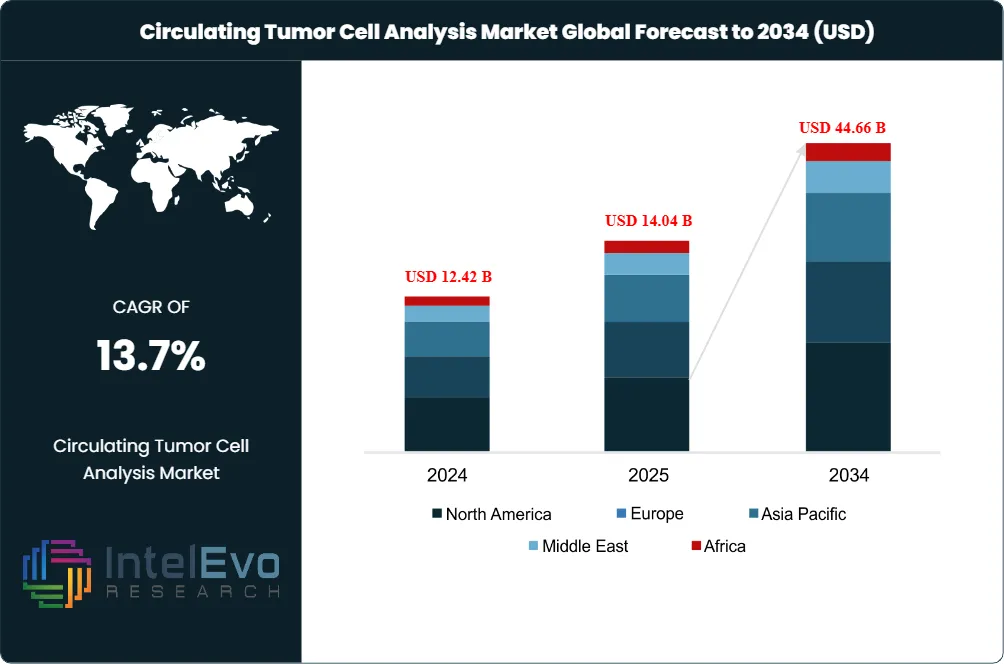

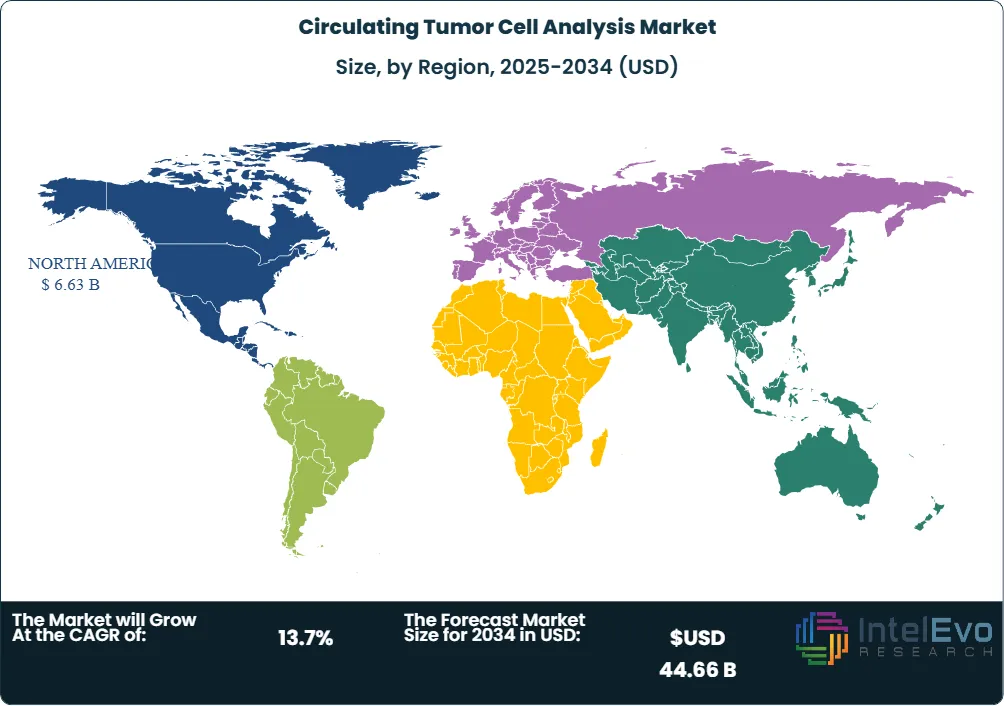

| USD 14.04 Billion | USD 44.66 Billion | 13.7% | North America, 47.2% |

The Circulating Tumor Cell Analysis Market was valued at USD 12.42 Billion in 2024 and is estimated to reach USD 14.04 Billion in 2025. The market is projected to reach USD 44.66 Billion by 2034, expanding at a CAGR of 13.7% during the forecast period (2026–2034). This represents an absolute dollar opportunity of USD 30.62 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportThe circulating tumor cell analysis market is moving from rare-cell research into clinical workflow support because oncology teams need live-cell information that circulating tumor DNA cannot provide. CellSearch from Menarini Silicon Biosystems remains the main FDA-cleared CTC enumeration system for metastatic breast, colorectal, and prostate cancer monitoring, while CelLBxHealth Parsortix adds antigen-independent capture for metastatic breast cancer cell enrichment.

Demand is anchored by global cancer burden. International cancer data show 20.0 million new cancer cases and 9.7 million cancer deaths in 2022, with incidence expected to exceed 35 million annual cases by 2050. This growth increases the need for blood-based monitoring, treatment response assessment, metastatic risk stratification, and research tools that work when tissue biopsy is unavailable or unsafe.

Regulation is shaping buyer behavior. FDA-cleared CTC platforms have created a narrower but more defensible commercial path than research-only rare-cell devices. The FDA also expanded its regulatory-science work on liquid biopsy in January 2026 through minimal residual disease projects, which strengthens institutional attention around blood-based oncology biomarkers even when ctDNA and CTC technologies serve different clinical questions.

Technology competition in the circulating tumor cell analysis market is shifting from simple enumeration toward cell recovery, single-cell imaging, molecular profiling, and combined CTC-DNA plus ctDNA workflows. RareCyte, Bio-Techne, Fluxion Biosciences, Miltenyi Biotec, ScreenCell, and Greiner Bio-One compete through imaging, depletion, microfluidics, filtration, immunomagnetic capture, and sample preparation systems used by academic cancer centers and pharmaceutical services groups.

North America led with 47.2% share in 2025 because the United States combines FDA precedent, cancer-center density, oncology trial activity, and liquid-biopsy reimbursement infrastructure. Europe held 25.1% share, supported by the United Kingdom, Germany, France, Italy, and Netherlands research networks. Asia Pacific will post the fastest growth through 2034 as China, Japan, South Korea, Singapore, and India expand precision-oncology testing and translational cancer research capacity.

Market Definition & Scope

The circulating tumor cell analysis market is defined as commercial activity around instruments, kits, reagents, software, and services used to isolate, enumerate, image, recover, and molecularly profile intact tumor cells shed into peripheral blood. The market encompasses CellSearch enumeration, Parsortix enrichment, microfluidic rare-cell capture, immunomagnetic separation, size-based filtration, label-free enrichment, single-cell retrieval, and downstream DNA, RNA, protein, and morphology analysis.

This analysis includes CTC instruments, consumables, antibody cocktails, enrichment cartridges, imaging platforms, data-analysis software, contract research services, pharma-services assays, and clinical testing services across solid-tumor oncology. It excludes pure circulating tumor DNA tests, exosome-only tests, tissue biopsy pathology, next-generation sequencing instruments sold without CTC workflow integration, and general flow cytometry platforms not configured for rare tumor cell analysis. The circulating tumor cell analysis market sits inside the broader liquid biopsy and precision oncology testing category.

, By Technology (CTC Enrichment, Detection, Molecular Characterization), By Application (Diagnosis, Prognosis, Treatment Monitoring), By End-User (Hospitals, Diagnostic Labs, Research Institutes, Pharma & Biotech) Regional Outlook, Key Players – Dynamics, Liquid Biopsy Tech Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The circulating tumor cell analysis market expanded from USD 14.04 Billion in 2025 toward a projected USD 44.66 Billion by 2034 at a 13.7% CAGR.

- Segment Dominance: Kits, reagents, and consumables led the product category with 46.8% share in 2025, equivalent to USD 6.57 Billion.

- Segment Dominance: Clinical monitoring and prognosis represented the largest application with 37.6% share in 2025, equivalent to USD 5.28 Billion.

- Driver: Cancer incidence growth is the primary demand driver, with 20.0 million new cancer cases reported globally in 2022 and more than 35 million projected by 2050.

- Restraint: Standardization remains the main constraint because CTC counts, enrichment yield, EpCAM dependence, and downstream interpretation vary across CellSearch, Parsortix, filtration, and microfluidic systems.

- Opportunity: Pharma-services and companion diagnostic development represent a USD 9.60 Billion opportunity by 2034 as drug developers use CTC-DNA, morphology, and protein expression to monitor therapy response.

- Trend: Integrated CTC-DNA plus ctDNA workflows are gaining attention because intact cells provide morphology and expression data while ctDNA captures broader mutation burden.

- Regional: North America led the circulating tumor cell analysis market with 47.2% share in 2025, equal to USD 6.63 Billion.

Key Insights Summary

- Global cancer surveillance recorded 20.0 million new cases and 9.7 million deaths in 2022, creating a structural need for repeatable blood-based oncology monitoring tools.

- CellSearch enumerates epithelial-origin CTCs from 7.5 mL of whole blood using CD45 exclusion, EpCAM enrichment, and cytokeratin 8, 18, or 19 identification.

- The CellSearch CTC result threshold of 5 or more cells per 7.5 mL has been associated with shorter progression-free survival and overall survival in metastatic breast cancer studies.

- Parsortix PC1 received FDA De Novo authorization for CTC enrichment in metastatic breast cancer in 2022, making it the first FDA-cleared system focused on intact CTC harvesting rather than only enumeration.

- CelLBxHealth reported more than 270 installed Parsortix systems and about 248,000 cumulative samples processed by 30 June 2025, indicating a growing research footprint despite modest company revenue.

- Akadeum Life Sciences closed more than USD 20 Million in financing in June 2025 for buoyancy-based cell separation, an adjacent rare-cell platform relevant to CTC enrichment workflows.

- RareCyte received a USD 495,177 Gates Foundation grant in 2025 to study circulating trophoblasts, showing investor and grant-maker interest in rare-cell isolation outside oncology.

Competitive Landscape Overview

The circulating tumor cell analysis market is moderately fragmented, with Menarini Silicon Biosystems, CelLBxHealth, RareCyte, and Bio-Techne accounting for an estimated 38% of 2025 commercial activity across systems, consumables, assays, and services. Competition is based on regulatory status, capture biology, downstream compatibility, sample throughput, and clinical evidence rather than price alone.

Menarini Silicon Biosystems holds the clearest clinical position through CellSearch, while CelLBxHealth competes through antigen-independent enrichment and pharma-services workflows. RareCyte differentiates through high-content rare-cell imaging and single-cell retrieval, and Bio-Techne participates through liquid biopsy reagents, sample-preparation assets, and diagnostic channels. Smaller vendors, including ScreenCell, Fluxion Biosciences, Greiner Bio-One, Miltenyi Biotec, and Ikonisys, compete through specialized capture formats and regional research relationships.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Menarini Silicon Biosystems | Italy / United States | Leader | CellSearch CTC Test and CellTracks systems | North America, Europe, Japan | Maintained FDA-cleared CTC monitoring position across breast, colorectal, and prostate cancer workflows |

| CelLBxHealth plc | United Kingdom | Leader | Parsortix PC1 System and CTC-DNA workflows | Europe, United States | Changed name from ANGLE plc in October 2025 to focus on CTC intelligence services |

| RareCyte, Inc. | United States | Challenger | CyteFinder, CytePicker, AccuCyte rare-cell systems | United States, Europe | Received a 2025 Gates Foundation grant supporting rare-cell molecular profiling research |

| Bio-Techne Corporation | United States | Challenger | Liquid biopsy reagents, Exosome Diagnostics legacy assets | North America, Europe | Divested Exosome Diagnostics to mdxhealth in August 2025 while retaining precision diagnostics emphasis |

| Guardant Health, Inc. | United States | Adjacent Leader | Guardant360, Reveal, Shield liquid biopsy portfolio | United States, Europe, Asia | Reported 39% Q4 2025 revenue growth driven by oncology and screening volumes |

| Fluxion Biosciences | United States | Niche Player | IsoFlux CTC enrichment and analysis system | United States, academic centers | Continued supporting CTC enrichment studies in metastatic solid tumors |

| ScreenCell | France | Niche Player | ScreenCell filtration devices | Europe, Asia Pacific | Expanded filtration-based CTC research use in academic cancer studies |

| Greiner Bio-One | Austria | Challenger | Cell-free DNA and rare-cell blood collection products | Europe, North America | Supported liquid biopsy preanalytics adoption across clinical research sites |

| Miltenyi Biotec | Germany | Challenger | MACS rare-cell separation tools | Europe, North America, Asia | Expanded translational oncology cell-separation use through research channels |

| Ikonisys SA | France / United States | Niche Player | Ikoniscope rare-cell imaging systems | Europe, United States | Targeted automated rare-cell imaging for oncology and prenatal applications |

By Product

The circulating tumor cell analysis market by product is led by kits, reagents, cartridges, and other consumables, which held 46.8% share in 2025, equal to USD 6.57 Billion. Consumables dominate because each CellSearch, Parsortix, AccuCyte, ScreenCell, or microfluidic workflow requires single-use capture materials, antibody reagents, sample preservatives, and staining kits.

Instruments accounted for 31.6% share in 2025, equal to USD 4.44 Billion. Instrument revenue is concentrated in imaging, enrichment, and cell-recovery systems because capital purchases cluster around cancer-center core laboratories, translational medicine units, and pharma-services providers. Software and services held 21.6% share, equivalent to USD 3.03 Billion, and will grow faster than instruments as pharmaceutical sponsors outsource CTC-DNA, protein, and morphology analysis rather than building rare-cell laboratories internally.

By Technology

The circulating tumor cell analysis market by technology is led by CTC enrichment and detection systems, which represented 42.5% of revenue in 2025. CellSearch uses immunomagnetic EpCAM-based capture, while Parsortix uses size and deformability to enrich intact cells independent of epithelial marker expression. This distinction matters because mesenchymal and heterogeneous CTC phenotypes can escape EpCAM-dependent workflows.

Direct detection and imaging accounted for 28.1% share in 2025, supported by RareCyte, Ikonisys, fluorescence microscopy, and high-content imaging systems. Downstream CTC molecular analysis represented 19.4% share, with DNA, RNA, protein, and single-cell sequencing workflows used by pharmaceutical companies. Multimodal CTC plus ctDNA workflows held 10.0% share, but this sub-segment has the highest commercial upside because dual analyte testing reduces the blind spots of single-biomarker liquid biopsy.

By Application

Clinical monitoring and prognosis led the circulating tumor cell analysis market with 37.6% share in 2025, equivalent to USD 5.28 Billion. CTC enumeration is used to assess metastatic disease burden and therapy response in breast, colorectal, and prostate cancer, where clinicians value serial blood sampling over repeat tissue biopsy.

Early detection and diagnostic support accounted for 29.4% share in 2025, equal to USD 4.13 Billion. Research use is stronger than routine screening because CTC rarity, enrichment variability, and manual interpretation still limit high-throughput population testing. Drug development and companion diagnostic research represented 21.5% share, while recurrence surveillance, stemness analysis, and other oncology research applications accounted for 11.5%.

By End-User

Academic and cancer research institutes held 42.0% share of the circulating tumor cell analysis market in 2025, equal to USD 5.90 Billion. The segment leads because CTC analysis still requires technical expertise, optimized preanalytics, and advanced imaging or molecular workflows that fit translational research centers better than routine community laboratories.

Hospitals and diagnostic laboratories captured 31.0% share in 2025, led by CellSearch-supported metastatic monitoring and reference-lab testing models. Pharmaceutical companies and contract research organizations held 22.0% share because CTC-DNA, CTC clusters, and protein-expression profiling can reveal treatment resistance mechanisms during oncology trials. Other users, including forensic, veterinary, and prenatal rare-cell laboratories, represented 5.0%.

Regional Analysis

North America

North America led the circulating tumor cell analysis market with 47.2% share and USD 6.63 Billion in 2025. The United States dominates regional demand because FDA-cleared CTC technologies, NCI-designated cancer centers, liquid-biopsy reimbursement infrastructure, and oncology clinical trials concentrate in Boston, San Francisco, Houston, Research Triangle Park, and New York. Canada contributes through provincial cancer agencies and academic oncology networks, while Mexico remains a smaller research-led market. FDA regulatory-science work on liquid biopsy in January 2026 strengthened institutional attention around blood-based oncology biomarkers.

Europe

Europe held 25.1% share of the circulating tumor cell analysis market in 2025, equivalent to USD 3.52 Billion. The United Kingdom is anchored by CelLBxHealth, NHS cancer research networks, and pharma-services adoption, while Germany, France, Italy, and the Netherlands support translational oncology studies. The IVDR framework raises evidence requirements for clinical diagnostics, which favors companies with validated workflows and documented analytical performance. Europe differs from North America because reimbursement remains more fragmented, but research density and biobank infrastructure remain high.

Asia Pacific

Asia Pacific accounted for 20.3% share of the circulating tumor cell analysis market in 2025, equal to USD 2.85 Billion, and will grow fastest through 2034. China, Japan, South Korea, Singapore, India, and Australia are expanding precision oncology, cancer genomics, and hospital-based translational research programs. Japan benefits from established diagnostic manufacturers and oncology reimbursement infrastructure. China adds scale through cancer incidence, provincial research funding, and domestic microfluidics capabilities. India remains earlier-stage but gains from private oncology networks and lower-cost diagnostic outsourcing.

Latin America

Latin America held 4.7% share of the circulating tumor cell analysis market in 2025, equivalent to USD 0.66 Billion. Brazil, Mexico, Argentina, Chile, and Colombia account for most demand through academic oncology institutes and private reference laboratories. Adoption is restrained by capital-equipment budgets, reagent import costs, and limited reimbursement for advanced blood-based monitoring. The strongest near-term opportunities are pharma-sponsored trial services and centralized rare-cell testing rather than decentralized hospital deployment.

Middle East & Africa

Middle East and Africa represented 2.7% share of the circulating tumor cell analysis market in 2025, equal to USD 0.38 Billion. Saudi Arabia, the United Arab Emirates, Israel, South Africa, and Turkey lead adoption through cancer-center investment, precision-medicine programs, and private hospital groups. Gulf markets support premium oncology diagnostics, while South Africa anchors academic cancer research. Wider adoption is limited by laboratory workforce shortages, sample logistics, and reimbursement gaps across public health systems.

Country Analysis

United States

The United States circulating tumor cell analysis market reached USD 5.95 Billion in 2025 and is projected to grow at a 13.2% country CAGR through 2034. Demand is supported by FDA-cleared CellSearch and Parsortix regulatory pathways, NCI cancer-center density, Medicare-linked molecular testing infrastructure, and high oncology trial volume. FDA guidance on circulating tumor DNA in early-stage solid-tumor drug development and January 2026 regulatory-science work on MRD liquid biopsy reinforce broader blood-based biomarker acceptance.

United Kingdom

The United Kingdom circulating tumor cell analysis market reached USD 0.62 Billion in 2025 and is projected to grow at a 14.1% CAGR through 2034. CelLBxHealth anchors the country through Parsortix technology, pharma-services assays, and CTC-DNA workflows. The NHS, UK Biobank, Cancer Research UK, and academic centers in London, Cambridge, Manchester, and Oxford support translational oncology demand. The October 2025 CelLBxHealth rebrand sharpened commercial focus around CTC intelligence.

Germany

Germany recorded USD 0.74 Billion in circulating tumor cell analysis market revenue in 2025 and is projected to grow at a 12.6% CAGR through 2034. Demand is anchored by university hospitals, oncology research groups, and diagnostic suppliers including Miltenyi Biotec and Greiner Bio-One regional operations. IVDR requirements strengthen analytical validation, which benefits CTC platforms with clear preanalytical controls, documented recovery metrics, and compatible downstream molecular workflows.

China

China reached USD 1.05 Billion in circulating tumor cell analysis market revenue in 2025 and is projected to grow at a 15.8% CAGR through 2034. The country combines a large cancer population, hospital-based precision oncology investment, and domestic microfluidic device manufacturing. Adoption is strongest in tier-one cities, where cancer hospitals use CTC enrichment, imaging, and molecular profiling in translational studies. Local cost reduction will determine how quickly CTC workflows move beyond research laboratories.

Japan

Japan reached USD 0.54 Billion in circulating tumor cell analysis market revenue in 2025 and is forecast to grow at an 11.9% CAGR through 2034. Demand is supported by oncology screening culture, advanced hospital laboratories, and diagnostic manufacturing expertise. Menarini Silicon Biosystems, Sysmex, Takara Bio, and university hospital networks support the local rare-cell research base. Japan remains more conservative than China on adoption speed because reimbursement and clinical-guideline recognition drive purchasing decisions.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Product

- Instruments

- Consumables & Reagents

- Software & Services

By Technology

- CTC Enrichment

- CTC Detection & Analysis

- Molecular Characterization

By Application

- Cancer Diagnosis

- Prognostic Assessment

- Treatment Monitoring

- Research

By End-User

- Hospitals & Clinics

- Diagnostic Laboratories

- Academic & Research Institutes

- Pharmaceutical & Biotechnology Companies

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 14.04 B |

| Forecast Revenue (2034) | USD 44.66 B |

| CAGR (2025-2034) | 13.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product, (Instruments, Consumables & Reagents, Software & Services), By Technology, (CTC Enrichment, CTC Detection & Analysis, Molecular Characterization), By Application, (Cancer Diagnosis, Prognostic Assessment, Treatment Monitoring, Research), By End-User, (Hospitals & Clinics, Diagnostic Laboratories, Academic & Research Institutes, Pharmaceutical & Biotechnology Companies), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MENARINI SILICON BIOSYSTEMS, CELLBXHEALTH PLC, RARECYTE, INC., BIO-TECHNE CORPORATION, GUARDANT HEALTH, INC., FLUXION BIOSCIENCES, SCREENCELL, GREINER BIO-ONE INTERNATIONAL GMBH, MILTENYI BIOTEC B.V. & CO. KG, IKONISYS SA, QIAGEN N.V., SYSMEX CORPORATION, TAKARA BIO INC., EPIC SCIENCES, INC., AKADEUM LIFE SCIENCES, CLEARBRIDGE BIOMEDICS, BIOCEPT, INC., OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (CTC Enrichment, Detection, Molecular Characterization), By Application (Diagnosis, Prognosis, Treatment Monitoring), By End-User (Hospitals, Diagnostic Labs, Research Institutes, Pharma & Biotech) Regional Outlook, Key Players – Dynamics, Liquid Biopsy Tech Trends & Forecast 2026-2034")

, By Technology (CTC Enrichment, Detection, Molecular Characterization), By Application (Diagnosis, Prognosis, Treatment Monitoring), By End-User (Hospitals, Diagnostic Labs, Research Institutes, Pharma & Biotech) Regional Outlook, Key Players – Dynamics, Liquid Biopsy Tech Trends & Forecast 2026-2034")

, By Technology (CTC Enrichment, Detection, Molecular Characterization), By Application (Diagnosis, Prognosis, Treatment Monitoring), By End-User (Hospitals, Diagnostic Labs, Research Institutes, Pharma & Biotech) Regional Outlook, Key Players – Dynamics, Liquid Biopsy Tech Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Circulating Tumor Cell Analysis Market?

Global Circulating Tumor Cell Analysis Market was valued at USD 12.42 billion in 2024 and is projected to reach USD 44.66 billion by 2034, at a CAGR of 13.7% (2026–2034).

Who are the major players in the Circulating Tumor Cell Analysis Market?

MENARINI SILICON BIOSYSTEMS, CELLBXHEALTH PLC, RARECYTE, INC., BIO-TECHNE CORPORATION, GUARDANT HEALTH, INC., FLUXION BIOSCIENCES, SCREENCELL, GREINER BIO-ONE INTERNATIONAL GMBH, MILTENYI BIOTEC B.V. & CO. KG, IKONISYS SA, QIAGEN N.V., SYSMEX CORPORATION, TAKARA BIO INC., EPIC SCIENCES, INC., AKADEUM LIFE SCIENCES, CLEARBRIDGE BIOMEDICS, BIOCEPT, INC., OTHERS

Which segments covered the Circulating Tumor Cell Analysis Market?

By Product, (Instruments, Consumables & Reagents, Software & Services), By Technology, (CTC Enrichment, CTC Detection & Analysis, Molecular Characterization), By Application, (Cancer Diagnosis, Prognostic Assessment, Treatment Monitoring, Research), By End-User, (Hospitals & Clinics, Diagnostic Laboratories, Academic & Research Institutes, Pharmaceutical & Biotechnology Companies),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Circulating Tumor Cell Analysis Market

Published Date : 08 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date