- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Climate Risk Analytics Market Size, Share & Growth | CAGR 14.2%

Global Climate Risk Analytics Market Size, Share, Growth Analysis By Offering (Solutions, Services), By Deployment (Cloud-Based, On-Premise, Hybrid), By Application (Physical Risk Assessment, Transition Risk Analytics, Liability Risk Management, Climate Scenario Modeling), By End-User (BFSI, Energy & Utilities, Real Estate, Government), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

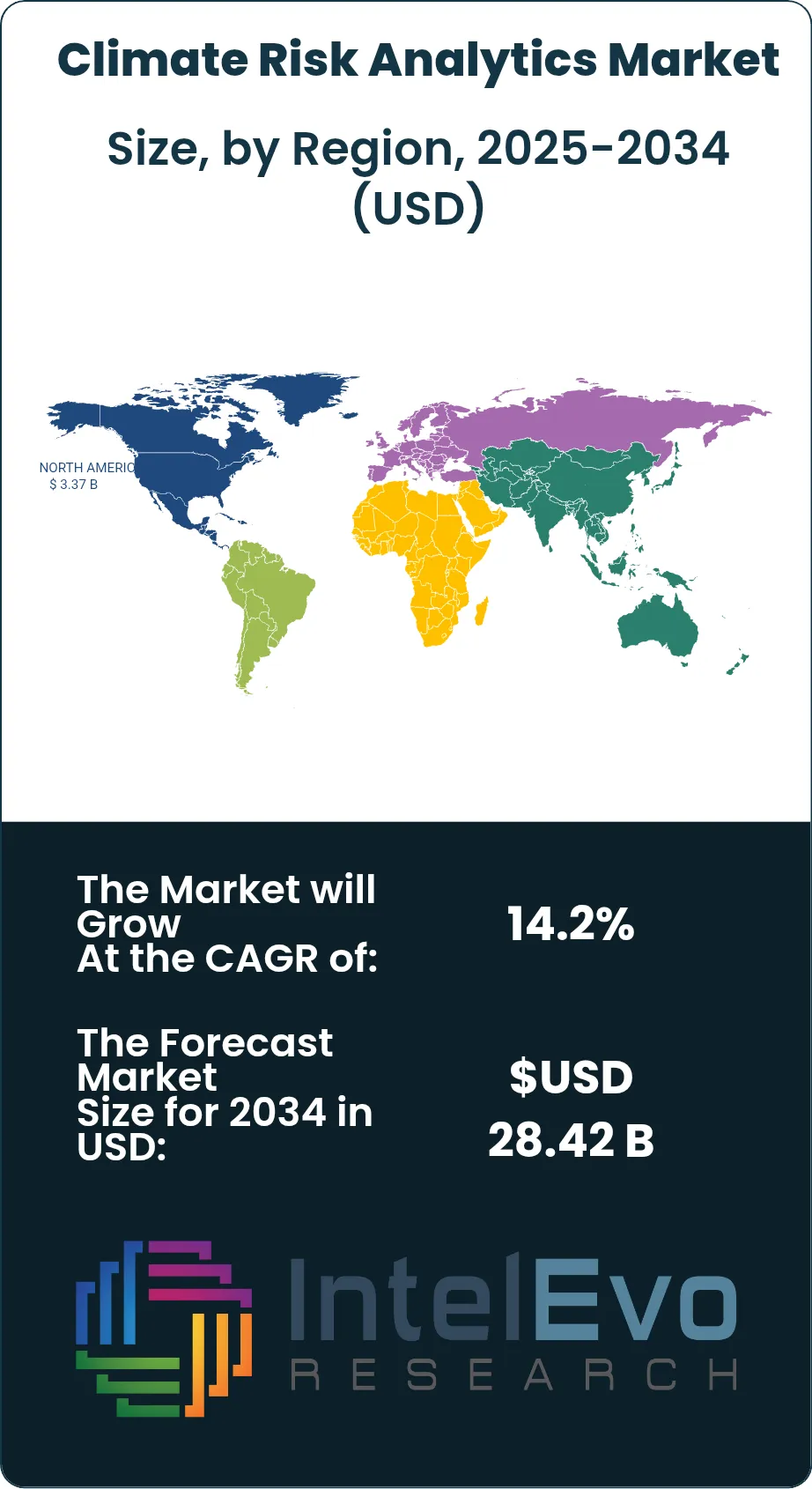

| USD 8.60 Billion | USD 28.42 Billion | 14.2% | North America, 39.2% |

The Climate Risk Analytics Market was valued at approximately USD 7.45 Billion in 2024 and reached USD 8.60 Billion in 2025. The market is projected to grow to USD 28.42 Billion by 2034, expanding at a CAGR of 14.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 19.82 Billion over the analysis period, driven by an accelerating intersection of mandatory climate disclosure regulation, institutional capital reallocation, and the maturation of geospatial artificial intelligence capable of translating atmospheric science into asset-level financial exposure.

Get More Information about this report -

Request Free Sample ReportThree distinct regulatory triggers explain the steepness of the current growth trajectory. First, the International Sustainability Standards Board's IFRS S2 Climate-related Disclosures standard, which took effect for fiscal years beginning January 2025 in jurisdictions covering approximately 73% of global equity market capitalization, created an immediate corporate procurement cycle for climate scenario modeling tools. Companies that previously treated climate risk as a reputational exercise now face mandatory quantitative disclosure obligations, compressing the sales cycle for climate risk analytics vendors from 18–24 months to as short as 60–90 days in high-compliance markets. Second, the European Banking Authority's Climate Risk Stress Testing framework under the Capital Requirements Directive VI (CRD VI) requires European banks with total assets above EUR 5 billion to submit supervisory-grade physical and transition risk scenarios annually beginning in 2025. The 187 in-scope institutions collectively manage loan books exceeding EUR 26 trillion, each requiring third-party climate risk data inputs. Third, the U.S. Securities and Exchange Commission's climate disclosure rules for large accelerated filers, partially reinstated following a federal appellate ruling in late 2024, reintroduced Scope 1 and Scope 2 physical risk disclosure requirements for approximately 1,300 domestic registrants.

Beyond regulatory compliance, genuine investor demand for forward-looking climate exposure data is reshaping capital allocation. Pension funds managing combined assets under management exceeding USD 55 trillion globally have adopted climate risk integration policies, with physical risk screening becoming a standard step in infrastructure and real estate due diligence since 2023. This demand-side pull operates independently of regulatory mandates and provides a structurally durable revenue floor for analytics providers. The climate risk analytics market also benefits from a technology cost inflection: satellite observation costs fell approximately 67% between 2019 and 2024 as commercial Earth observation constellations scaled, making high-resolution physical risk data economically viable for mid-market financial institutions that previously lacked the data science infrastructure to process raw geophysical inputs.

A contrarian observation tempers the headline growth figures. While aggregate market revenue is expanding rapidly, a concentration dynamic is simultaneously narrowing competitive breadth. The top four vendors — Moody's, S&P Global, MSCI, and Verisk — collectively accounted for an estimated 54.3% of total climate risk analytics revenue in 2025, up from roughly 41% in 2022. This consolidation mirrors the trajectory of the credit ratings industry during the 1990s, when regulatory endorsement of a small set of nationally recognized statistical rating organizations entrenched incumbent advantages that smaller players have never fully eroded. If analogous regulatory recognition dynamics emerge in climate data — as the EU's forthcoming European Sustainability Reporting Standards assessment framework for data providers suggests — the current window for challenger brands to establish credible market share may be narrowing faster than headline CAGR figures imply.

Asia Pacific represents the most consequential emerging demand corridor, with China's Monetary Authority's green finance taxonomy revisions in 2025 and Australia's mandatory climate reporting legislation (effective July 2025 for ASX 300 companies) collectively adding an estimated USD 420 million in incremental addressable demand outside North America and Europe. This growth pattern parallels the trajectory of the environmental, social, and governance data market during 2016–2020, where initial European regulatory mandates preceded genuine commercial demand in other geographies by approximately 24 months before adoption accelerated sharply.

, By Deployment (Cloud-Based, On-Premise, Hybrid), By Application (Physical Risk Assessment, Transition Risk Analytics, Liability Risk Management, Climate Scenario Modeling), By End-User (BFSI, Energy & Utilities, Real Estate, Government), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global climate risk analytics market reached USD 8.60 Billion in 2025 and is forecast to reach USD 28.42 Billion by 2034, at a CAGR of 14.2% over the 2026–2034 period, underpinned by mandatory disclosure regulations spanning four major economic blocs.

- Segment Dominance (By Offering): Solutions accounted for 58.3% of total revenue in 2025 because integrated platform deployments generate recurring SaaS subscription income at 3–5x the revenue multiple of one-time consulting engagements, incentivizing vendors to shift portfolio mix toward software licensing and API-based data delivery.

- Segment Dominance (By Application): Physical Risk Assessment led with 38.5% of application revenue in 2025, reflecting institutional lenders' prioritization of asset-level flood, wildfire, and hurricane exposure scoring driven by FDIC supervisory guidance issued in Q4 2024 requiring stress test documentation for climate-exposed mortgage portfolios.

- Driver: Mandatory climate disclosure frameworks spanning IFRS S2, CRD VI, and SEC physical risk rules created a procurement event affecting an estimated 14,000+ publicly listed and regulated entities globally, injecting approximately USD 2.3 Billion in new annual technology spending into the climate risk analytics market between 2024 and 2026.

- Restraint: Data standardization gaps between competing scenario frameworks — principally NGFS versus IPCC AR6 regional pathways — force buyers to license multiple incompatible datasets, increasing total cost of ownership by 25–40% and slowing enterprise-wide deployment, most acutely in Asia Pacific markets where regulatory alignment with international frameworks remains partial.

- Opportunity: The insurance and reinsurance underwriting segment remains underserved, with fewer than 12% of global primary insurers having deployed real-time dynamic climate peril models as of 2025. Full penetration of this vertical across North American, European, and Asia Pacific insurers represents an incremental addressable market of USD 4.8–6.2 Billion by 2030.

- Trend: Generative AI integration within climate risk platforms reached 31% adoption among North American enterprise users in 2025, against only 9% in Asia Pacific, as vendors embed large language models for regulatory report drafting and scenario narrative generation — a productivity differential that is attracting cross-border technology licensing deals valued at an estimated USD 780 million.

- Regional Analysis: North America held 39.2% of global climate risk analytics revenue at USD 3.37 Billion in 2025, supported by the SEC disclosure rule pipeline, deep venture capital backing for climate data startups, and a mortgage sector mandated by FHFA to incorporate physical risk into Fannie Mae and Freddie Mac underwriting guidelines.

Competitive Landscape Overview

The climate risk analytics market exhibits moderate-to-high consolidation. The top four players — Moody's Corporation, S&P Global, MSCI, and Verisk Analytics — collectively held an estimated 54.3% of total market revenue in 2025, with concentration intensifying as regulatory mandates effectively pre-qualify vendors already embedded in institutional financial workflows. Competition operates primarily on data depth, scenario methodology credibility, and regulatory alignment rather than on price. The vendor landscape bifurcates sharply between large financial data incumbents that added climate analytics through acquisition (Moody's acquiring Four Twenty Seven in 2019, S&P acquiring Trucost in 2016) and purpose-built climate risk specialists such as Jupiter Intelligence and XDI Systems that built bottom-up physical science models. In 2025–2026, three Chinese climate data firms — including state-backed entities affiliated with the National Climate Center in Beijing — have entered European procurement tenders, offering physical risk screening services at 18–25% lower price points than Western incumbents, triggering two defensive vertical integration transactions among European reinsurers valued at a combined USD 1.6 Billion.

Competitive Landscape Matrix

| Company | HQ Country | Market Position | Key Product / Solution | Geographic Strength | Recent Strategic Move (2024–2026) |

| Moody's Corporation | USA | Leader | Moody's RMS ClimateScore Global | North America | Acquired climatetech data firm Cape Analytics in Jan 2025, expanding property-level physical risk scoring to 95 million US parcels. |

| S&P Global | USA | Leader | S&P Global Sustainable1 Climate Analytics | North America / Europe | Launched EU Taxonomy-aligned climate transition risk tool in March 2025, targeting SFDR Article 9 fund managers across 18 EU jurisdictions. |

| MSCI Inc. | USA | Leader | MSCI Climate Value-at-Risk (CVaR) | Global Institutional | Integrated Nature-related Financial Disclosures (TNFD) metrics into MSCI ESG Manager in Q2 2025, covering 15,000+ equity and fixed income issuers. |

| Verisk Analytics | USA | Leader | Verisk Extreme Event Solutions (AIR Worldwide) | North America / APAC | Partnered with Japan's SOMPO Holdings in Nov 2024 to deploy AI-driven typhoon and flood risk models for the Asia Pacific reinsurance market. |

| IBM | USA | Challenger | IBM Environmental Intelligence Suite | Global Enterprise | Extended Watson-powered climate scenario modeling to cover ISSB S2-aligned disclosures in Feb 2026, targeting 2,500+ corporate clients. |

| Munich Re | Germany | Challenger | NATHAN Risk Suite | Europe / Global Re | Launched Climate Transition Risk Monitor for European banks in Sep 2025, fulfilling EBA Climate Risk Stress Testing mandates under CRD VI. |

| Swiss Re | Switzerland | Challenger | CatNet Climate Analytics | Europe / Global Re | Released updated 1.5°C and 2°C warming pathway models in CatNet in Q1 2026, aligned with IPCC AR6 regional downscaling data. |

| Jupiter Intelligence | USA | Niche Player | Jupiter ClimateScore for Infrastructure | North America / Europe | Secured USD 60 million Series C in Oct 2025 to expand 30-year asset-level physical risk projections to South and Southeast Asian markets. |

| CoreLogic | USA | Niche Player | CoreLogic Climate Risk Analytics | North America | Integrated FEMA Flood Risk Rating 2.0 data into its Climate Risk Analytics platform in May 2025, improving mortgage portfolio exposure models. |

| XDI Systems | Australia | Niche Player | XDI Physical Climate Risk Screening | Asia Pacific / Europe | Signed data partnership with the European Investment Bank in Aug 2025 to assess climate risk across USD 120 billion in infrastructure loan portfolios. |

By Offering

The solutions segment of the climate risk analytics market captured 58.3% of global revenue at USD 5.01 Billion in 2025, driven by a fundamental commercial logic: platform-based SaaS deployments generate annual contract values 3.2–5.1 times higher than equivalent one-time analytical consulting projects. When IFRS S2 and CRD VI mandates created recurring annual disclosure obligations, corporate and financial institution buyers shifted purchasing behavior toward multi-year platform licenses that automate scenario ingestion, data integration, and report generation. Vendors such as MSCI and S&P Global Sustainable1 designed their platforms as centralized data hubs capable of ingesting physical hazard layers, transition scenario outputs, and company-level emissions data simultaneously, creating switching costs that commoditize any single data input but entrench the platform itself. The competitive dynamic within solutions increasingly favors API-first architectures, as buy-side firms prefer to integrate climate risk outputs directly into proprietary risk management systems rather than operate standalone vendor portals.

Services maintained a 41.7% revenue share at USD 3.59 Billion in 2025, retaining structural relevance because the translation of raw climate science into regulatory-grade financial disclosures requires domain expertise that no fully automated platform yet replicates. The fastest-growing services sub-segment is regulatory compliance advisory, expanding at an estimated 18.6% annually through 2027 as the volume of jurisdiction-specific disclosure templates — SFDR, EU Taxonomy, TNFD, ISSB S2, SEC — multiplies faster than institutional compliance functions can hire internally. Accenture's green finance advisory practice and Deloitte's climate risk consulting group (referenced here as industry professional services providers, not research sources) report that ISSB S2 implementation engagements carried average project values of USD 1.4 million in 2025, double the level observed during comparable TCFD implementation cycles in 2020–2022.

By Deployment

Cloud-based deployment led with 64.2% of the climate risk analytics market at USD 5.52 Billion in 2025. Cloud dominance reflects three compounding factors: the sheer data volume of high-resolution physical hazard layers — a single global 90-meter resolution digital elevation model exceeds 400 gigabytes, making local storage economically impractical for most users; the computational intensity of running Monte Carlo simulations across 100,000+ asset portfolios under multiple warming scenarios; and the expectation among institutional buyers that data will refresh continuously as new satellite imagery and atmospheric reanalysis products become available. Microsoft Azure and Amazon Web Services host the majority of third-party climate risk analytics workloads, with Azure's Planetary Computer initiative — which provides curated access to petabytes of open geospatial climate data — becoming a de facto infrastructure layer for at least seven of the top twenty climate risk analytics vendors.

On-premise deployments held 24.8% of the market at USD 2.13 Billion in 2025, sustained by sovereign financial institutions, central banks, and defense-adjacent government agencies with data residency requirements that prohibit third-party cloud processing of portfolio or infrastructure exposure data. The European Central Bank, for instance, requires national central bank climate stress test computations to occur on sovereign infrastructure, sustaining demand for on-premise licensed climate risk models from vendors such as Munich Re and Swiss Re that maintain air-gapped model delivery capabilities. Hybrid deployments, at 11.0% and USD 0.95 Billion, are growing at the highest rate within the deployment segmentation as organizations with partial cloud migration maturity adopt edge-compute architectures that process sensitive asset data locally while leveraging cloud APIs for public hazard dataset enrichment.

By Application

Physical risk assessment commanded 38.5% of application-level revenue at USD 3.31 Billion in 2025 for a reason that is commercially precise rather than conceptually broad: property-secured lenders face a concrete impairment event if a mortgaged asset becomes uninsurable or its flood zone designation changes, whereas transition risks play out over decades and lack equivalent near-term balance sheet triggers. The FDIC's November 2024 supervisory guidance letter, which requested that U.S. commercial banks document physical climate risk exposure for loan portfolios with combined real estate collateral above USD 100 million, created a defined procurement deadline for approximately 320 mid-size regional banks that previously lacked vendor relationships in this space. CoreLogic's integration of FEMA Flood Risk Rating 2.0 granular parcel data into its mortgage analytics suite in May 2025 captured a disproportionate share of this demand wave, onboarding 48 community and regional bank clients within six months of release.

Transition risk analytics held 29.4% of application revenue at USD 2.53 Billion in 2025, reflecting the analytical demands of financial institutions managing Scope 3 financed emissions inventories and loan book carbon intensity assessments. The fastest-growing sub-application within transition risk is sectoral stranded asset modeling, growing at approximately 19.8% annually as European pension funds model the present-value impact of accelerated decarbonization policies on fossil fuel and carbon-intensive industrial assets in their equity and credit portfolios. Moody's Investors Service's 2025 carbon transition credit factor integration into its corporate rating methodology — the first major rating agency to embed climate transition probability into standard credit assessments — directly elevated demand for the underlying analytics that feed transition risk models. Liability risk management at 16.8% and climate scenario modeling at 15.3% complete the application landscape, with scenario modeling growing fastest among central banks and prudential regulators building systemic financial stability assessments.

By End-User

Financial services firms — banks, asset managers, insurers, and pension funds — collectively represented 42.1% of end-user demand at USD 3.62 Billion in 2025. This dominance stems not from voluntary environmental commitment but from regulatory arithmetic: a European bank failing a CRD VI climate stress test faces a mandatory capital add-on under Pillar 2 guidance, creating a quantifiable cost-of-non-compliance that makes climate analytics spending directly return-on-investment-positive for chief risk officers. The energy and utilities sector at 22.3% is the second-largest end-user category because power generation and transmission asset operators face the most direct intersection of physical hazard exposure (power lines, substations, and hydroelectric capacity impaired by changed precipitation patterns) and transition risk (stranded thermal generation assets under accelerating renewable mandates). Real estate at 14.6%, government and regulatory bodies at 12.4%, and other industries at 8.6% complete the distribution.

Regional Analysis

North America

Backed by three intersecting regulatory mandates — the SEC physical risk disclosure rules, FHFA mortgage underwriting guidance incorporating flood risk, and the Federal Reserve's 2025 climate scenario analysis exercise for the eight largest U.S. bank holding companies — North America's climate risk analytics market captured 39.2% of global revenue at USD 3.37 Billion in 2025. The United States accounts for approximately 82% of regional revenue, with California-domiciled property insurers emerging as unexpectedly significant buyers following the January 2025 Los Angeles County wildfire events that generated insured losses exceeding USD 28 billion and triggered mandatory actuarial reviews of catastrophe model assumptions at all admitted carriers. Canada contributed the remaining share, led by the Office of the Superintendent of Financial Institutions' B-15 Guideline on Climate Risk Management requiring federally regulated financial institutions to conduct forward-looking climate risk assessments. New York City's climate risk data requirements for pension funds managing municipal assets above USD 500 million added a sub-national procurement dimension that Moody's and S&P specifically targeted with dedicated product configuration offerings for public-sector retirement systems.

Europe

Regulatory architecture under the EU Sustainable Finance Disclosure Regulation, the EU Taxonomy Regulation, and the Corporate Sustainability Reporting Directive collectively reshaped procurement patterns across the European climate risk analytics market, which held 28.6% share worth USD 2.46 Billion in 2025. Germany dominated regional demand through its concentration of insurance headquarters (Munich Re and Allianz SE in Munich, Hannover Re in Hannover) and automotive OEM exposure assessment requirements, with Frankfurt-based banks navigating ECB supervisory expectations under the Guide on Climate-Related and Environmental Risks. France's Loi Energie Climat provisions and the Autorité de Contrôle Prudentiel et de Résolution's 2025 climate scenario publication created a compliance-driven demand wave among the six major French banking groups. The Netherlands, home to ING Groep and APG Asset Management — the latter managing EUR 600 billion in pension assets — represents the fourth-highest demand concentration within Europe, with Amsterdam-based asset managers leading TNFD beta reporting adoption across the continental investor community.

Asia Pacific

Manufacturing capacity additions in climate data processing infrastructure across Guangdong and Zhejiang provinces in China, combined with Australia's Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Act 2024 mandating climate-related financial disclosures for ASX 300 companies effective July 2025, propelled Asia Pacific's climate risk analytics market to 19.8% global share at USD 1.70 Billion in 2025. China's Monetary Authority's revised green finance taxonomy, published in February 2025, created a classification framework that domestic banks must apply to loan portfolios above CNY 50 billion, generating immediate demand for transition risk assessment tools aligned with Chinese-specific sector definitions. Japan's Financial Services Agency guidance on climate-related risk disclosure for listed companies produced approximately USD 230 million in incremental software procurement across Japanese megabanks and life insurance groups in 2025. Australia, despite representing a smaller absolute market, shows the highest per-institution climate analytics spending in the region, as ASX-listed mining companies face particularly complex physical risk exposures across Pilbara iron ore operations and Queensland coal assets simultaneously subject to cyclone intensification and chronic heat stress.

Latin America

Currency volatility across Brazil and Argentina constrained capital equipment imports and slowed technology license adoption in enterprise segments, yet Latin America's climate risk analytics market still reached USD 0.61 Billion (7.1% global share) in 2025, driven by agricultural finance and sovereign debt management applications unique to the region's economic profile. Brazil dominates regional demand, where BNDES — the national development bank managing a BRL 1.1 trillion loan portfolio concentrated in agribusiness, infrastructure, and energy — completed a USD 12 million climate risk analytics platform implementation in 2025 to assess flood and drought exposure across sugarcane, soybean, and beef production value chains. São Paulo-based Itaú Unibanco and Bradesco adopted physical risk screening tools sourced from XDI Systems for their real estate collateral portfolios, representing the first significant market penetration by a purpose-built climate analytics specialist in the Brazilian private banking sector. Colombia's financial regulator, the Superintendencia Financiera, published climate risk guidance for the domestic banking sector in late 2024, creating a nascent but formalizing procurement environment for regional vendors.

Middle East & Africa

Saudi Arabia's Vision 2030 industrial diversification program and the UAE's Net Zero by 2050 Strategic Initiative — which mandates that Abu Dhabi Global Market-registered financial institutions conduct annual climate risk assessments — opened new demand corridors, pushing the MEA climate risk analytics market to USD 0.46 Billion (5.3% share) in 2025. The UAE's position as the host of COP28 in late 2023 elevated climate risk analytics to a policy priority level, with the Dubai Financial Services Authority releasing climate risk guidance for DIFC-licensed banks and insurers in Q1 2025. Saudi Aramco's sustainability disclosure commitments under the Saudi Exchange's ESG reporting requirements created demand for enterprise physical risk tools covering its Abqaiq oil processing facility and Ras Tanura export terminal — assets whose combined throughput represents approximately 5.6% of global crude oil supply and whose physical resilience to Gulf heat index escalation and Red Sea storm surge events is of systemic interest to sovereign risk managers. South Africa represents the third-priority demand center, where the Prudential Authority's Guidance Note 4 of 2025 introduced climate risk governance expectations for licensed banks managing combined loan books exceeding ZAR 8 trillion.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Solutions

- Services

By Deployment

- Cloud-Based

- On-Premise

- Hybrid

By Application

- Physical Risk Assessment

- Transition Risk Analytics

- Liability Risk Management

- Climate Scenario Modeling

By End-User

- Financial Services (BFSI)

- Energy & Utilities

- Real Estate

- Government & Regulatory Bodies

- Other Industries

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.60 B |

| Forecast Revenue (2034) | USD 28.42 B |

| CAGR (2025-2034) | 14.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Solutions, Services), By Deployment, (Cloud-Based, On-Premise, Hybrid), By Application, (Physical Risk Assessment, Transition Risk Analytics, Liability Risk Management, Climate Scenario Modeling), By End-User, (Financial Services (BFSI), Energy & Utilities, Real Estate, Government & Regulatory Bodies, Other Industries) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MOODY'S CORPORATION, S&P GLOBAL, MSCI INC., VERISK ANALYTICS, IBM CORPORATION, MUNICH RE, SWISS RE, JUPITER INTELLIGENCE, CORELOGIC, XDI SYSTEMS, FOUR TWENTY SEVEN (MOODY'S), CLIMATEAI, SUST GLOBAL (FORMERLY CERVEST), RISILIENCE, ICEYE, CLIMATE X, FIRST STREET FOUNDATION, THE PHYSICAL RISK COMPANY, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment (Cloud-Based, On-Premise, Hybrid), By Application (Physical Risk Assessment, Transition Risk Analytics, Liability Risk Management, Climate Scenario Modeling), By End-User (BFSI, Energy & Utilities, Real Estate, Government), Industry Trends & Forecast 2026-2034")

, By Deployment (Cloud-Based, On-Premise, Hybrid), By Application (Physical Risk Assessment, Transition Risk Analytics, Liability Risk Management, Climate Scenario Modeling), By End-User (BFSI, Energy & Utilities, Real Estate, Government), Industry Trends & Forecast 2026-2034")

, By Deployment (Cloud-Based, On-Premise, Hybrid), By Application (Physical Risk Assessment, Transition Risk Analytics, Liability Risk Management, Climate Scenario Modeling), By End-User (BFSI, Energy & Utilities, Real Estate, Government), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Climate Risk Analytics Market?

The Global Climate Risk Analytics Market was valued at USD 7.45 Billion in 2024 and is projected to reach USD 28.42 Billion by 2034, growing at a CAGR of 14.2% from 2026 to 2034, driven by rising demand for ESG risk assessment, climate scenario modeling, AI-powered climate intelligence platforms, geospatial analytics, and increasing regulatory focus on climate-related financial disclosures across global industries and financial institutions.

Who are the major players in the Climate Risk Analytics Market?

MOODY'S CORPORATION, S&P GLOBAL, MSCI INC., VERISK ANALYTICS, IBM CORPORATION, MUNICH RE, SWISS RE, JUPITER INTELLIGENCE, CORELOGIC, XDI SYSTEMS, FOUR TWENTY SEVEN (MOODY'S), CLIMATEAI, SUST GLOBAL (FORMERLY CERVEST), RISILIENCE, ICEYE, CLIMATE X, FIRST STREET FOUNDATION, THE PHYSICAL RISK COMPANY, Others

Which segments covered the Climate Risk Analytics Market?

By Offering, (Solutions, Services), By Deployment, (Cloud-Based, On-Premise, Hybrid), By Application, (Physical Risk Assessment, Transition Risk Analytics, Liability Risk Management, Climate Scenario Modeling), By End-User, (Financial Services (BFSI), Energy & Utilities, Real Estate, Government & Regulatory Bodies, Other Industries)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Climate Risk Analytics Market

Published Date : 27 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date