- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Clinical Trial Supply Chain Market Forecast 2034 | CAGR 10.5%

Global Clinical Trial Supply Chain Management Market Size, Share, Growth & Industry Analysis By Service Type (Logistics & Distribution, Packaging & Labeling, Storage & Inventory Management, Manufacturing & Comparator Sourcing), By Therapeutic Area (Oncology, CNS & Neurology, Infectious Diseases, Cardiovascular, Rare Diseases), By End User (Pharma & Biopharma Companies, CROs, Academic Institutes) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 5.8 Billion | USD 14.2 Billion | 10.5% | North America, 42.8% |

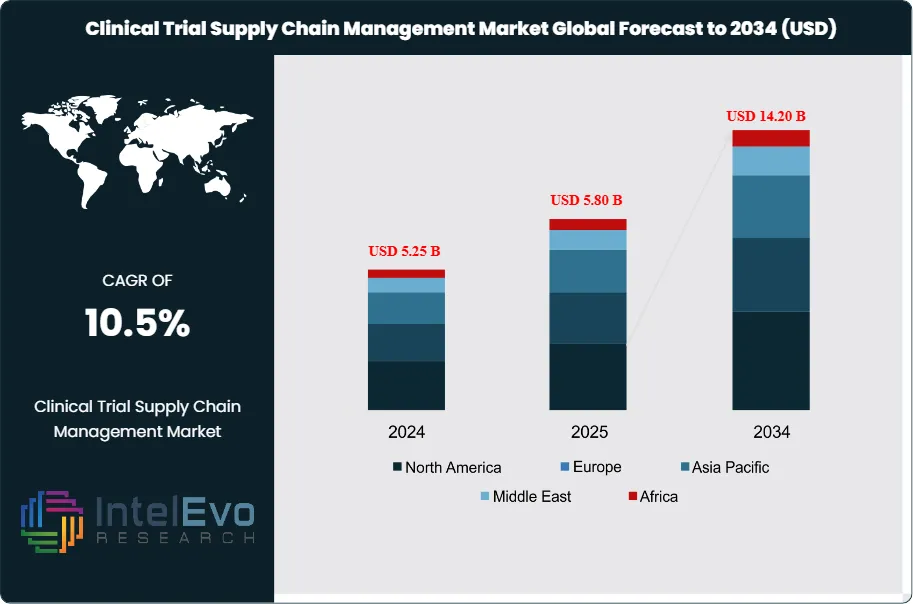

The Clinical Trial Supply Chain Management Market was valued at approximately USD 5.25 Billion in 2024 and reached USD 5.80 Billion in 2025. The market is projected to grow to USD 14.20 Billion by 2034, expanding at a CAGR of 10.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 8.4 Billion over the analysis period. Clinical trial supply chain management encompasses the planning, sourcing, manufacturing, packaging, labeling, storage, and distribution of investigational medicinal products and ancillary supplies required for pharmaceutical and biotechnology research studies. The market expansion reflects accelerating clinical trial complexity, globalization of research sites, and the rise of specialty therapies requiring temperature-controlled logistics.

Get More Information about this report -

Request Free Sample ReportSeveral structural factors are driving clinical trial supply chain management growth through 2034. The proliferation of decentralized and hybrid clinical trials following the COVID-19 pandemic has permanently altered distribution requirements. Direct-to-patient shipments increased from 8% of total clinical supply deliveries in 2020 to 24% in 2025, according to industry tracking data. Cell and gene therapy trials, which require cryogenic handling at temperatures below minus 150 degrees Celsius, now represent 18% of all Phase I through Phase III studies registered with regulatory authorities. These advanced therapy medicinal products demand specialized cold chain infrastructure that traditional pharmaceutical logistics networks cannot accommodate.

Regulatory pressure continues to shape clinical trial supply chain management investment priorities. The FDA Drug Supply Chain Security Act and EU Falsified Medicines Directive mandate serialization, track-and-trace capabilities, and temperature excursion documentation for all investigational products. Compliance costs have increased average supply chain spending per trial by 12% since 2022. Simultaneously, sponsors face pressure to reduce drug waste; current estimates indicate that 15-20% of manufactured clinical supplies expire before use due to forecasting inaccuracies. Advanced analytics platforms using machine learning algorithms have demonstrated 30% improvement in demand prediction accuracy, reducing both waste and stockout risk.

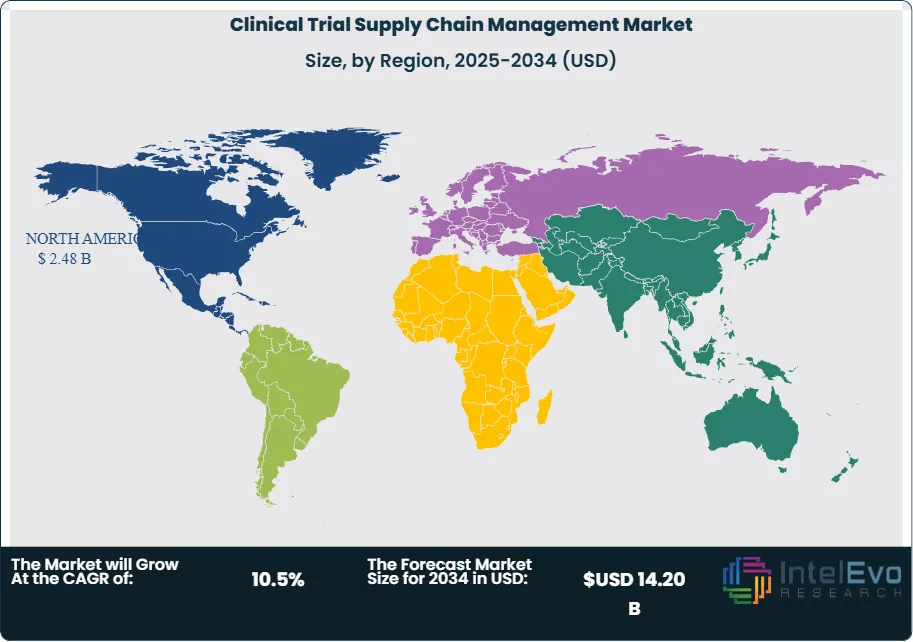

Regional dynamics reveal distinct growth patterns within clinical trial supply chain management. North America maintains leadership with 42.8% market share in 2025, anchored by the concentration of biopharmaceutical sponsors and contract research organizations. Asia Pacific represents the fastest-growing region at 12.8% CAGR through 2034 as sponsors increasingly locate trials in China, India, South Korea, and Australia to access patient populations and reduce costs. The expansion of Good Distribution Practice-compliant depot networks across emerging markets has reduced average delivery times to investigator sites from 14 days to 6 days over the past five years. Strategic partnerships between global logistics providers and regional cold chain specialists are addressing infrastructure gaps in Latin America, Middle East, and Africa.

, By Therapeutic Area (Oncology, CNS & Neurology, Infectious Diseases, Cardiovascular, Rare Diseases), By End User (Pharma & Biopharma Companies, CROs, Academic Institutes) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The clinical trial supply chain management market expands from USD 5.8 Billion in 2025 to USD 14.2 Billion by 2034, registering a CAGR of 10.5% across the nine-year forecast period.

- Segment Dominance: Logistics and distribution services command the largest share by service type at 38.2% in 2025, driven by specialized cold chain requirements and direct-to-patient delivery expansion.

- Segment Dominance: Oncology therapeutic area leads end-use segmentation with 32.4% market share in 2025, reflecting the high volume of cancer drug development programs requiring complex supply chain management.

- Driver: Expansion of cell and gene therapy clinical trials requiring cryogenic logistics has increased specialized cold chain service demand by 45% since 2022, creating sustained investment in infrastructure.

- Restraint: Temperature excursion events affect approximately 8% of clinical shipments annually, resulting in USD 350 Million in product loss and trial delays that constrain sponsor confidence.

- Opportunity: Artificial intelligence-powered demand forecasting and inventory optimization present a USD 1.8 Billion incremental revenue opportunity through 2034 by reducing clinical supply waste by 25-30%.

- Trend: Decentralized trial models now incorporate home delivery for 24% of clinical supplies in 2025, up from 8% in 2020, fundamentally reshaping last-mile distribution strategies.

- Regional Analysis: North America maintains market leadership with 42.8% share representing USD 2.48 Billion in 2025, supported by the concentration of pharmaceutical sponsors and advanced logistics infrastructure.

Competitive Landscape Overview

The clinical trial supply chain management market exhibits moderate consolidation with the top four providers controlling approximately 48% of global revenue in 2025. Competition centers on geographic network breadth, cold chain capabilities, technology platforms, and regulatory compliance expertise. Mergers and acquisitions have accelerated since 2023 as large pharmaceutical logistics companies seek cell and gene therapy handling capabilities. Thermo Fisher Scientific, Catalent, Almac Group, and Marken lead through integrated service portfolios spanning manufacturing, packaging, storage, and global distribution. Mid-tier challengers compete on specialized capabilities including direct-to-patient logistics, cryogenic transport, and regional expertise in emerging markets.

Competitive Landscape Matrix

| Company Name | HQ | Position | Key Solution | Geographic Strength | Recent Strategic Move (2024-2026) |

| Thermo Fisher Scientific | USA | Leader | Fisher Clinical Services | North America | Jan 2025: Expanded cold chain capacity in Singapore hub |

| Catalent Inc. | USA | Leader | Clinical Supply Services | North America, Europe | Mar 2025: Acquired gene therapy packaging specialist |

| Almac Group | UK | Leader | Clinical Services Division | Europe, North America | Dec 2024: Launched AI-driven demand forecasting platform |

| Marken Ltd. | USA | Leader | Direct-to-Patient Services | Global | Jun 2025: Partnered with decentralized trial tech provider |

| PCI Pharma Services | USA | Challenger | Clinical Trial Services | North America, Europe | Sep 2025: Opened new serialization facility in Ireland |

| Sharp Clinical Services | USA | Challenger | Packaging and Labeling | North America | Feb 2025: Integrated blockchain track-and-trace system |

| Parexel International | USA | Challenger | Supply Chain Solutions | Global | Nov 2024: Expanded Asia Pacific clinical depot network |

| World Courier | USA | Challenger | Specialty Logistics | Global | Apr 2025: Deployed autonomous temperature monitoring |

| Yourway Transport | USA | Niche Player | Home Healthcare Logistics | North America | Aug 2025: Launched patient-centric delivery app |

| Biocair | UK | Niche Player | Cell and Gene Therapy Logistics | Europe, North America | Oct 2025: Opened cryogenic hub in Boston |

By Service Type

Logistics and distribution services dominate the clinical trial supply chain management market with 38.2% share valued at USD 2.22 Billion in 2025. This segment encompasses temperature-controlled transportation, depot operations, customs clearance, and last-mile delivery to investigator sites or patient homes. Growth is propelled by the expansion of global trial networks requiring multi-country distribution capabilities and the shift toward decentralized trial models demanding direct-to-patient shipping infrastructure. Cold chain logistics for biologics and advanced therapies commands premium pricing, with cryogenic shipments costing three to five times more than ambient temperature deliveries. The segment is projected to grow at 11.2% CAGR through 2034 as specialty therapy trials multiply.

Packaging and labeling services account for 28.5% market share representing USD 1.65 Billion in 2025. Clinical trial packaging requires compliance with regulatory requirements across multiple jurisdictions, including country-specific labeling in local languages, blinding protocols for randomized studies, and serialization mandates. Just-in-time packaging strategies have gained adoption to reduce inventory holding costs and accommodate protocol amendments. Interactive response technology integration enables dynamic allocation of treatment kits based on real-time enrollment data. The segment benefits from increasing complexity of multi-arm adaptive trials requiring frequent re-packaging and re-labeling of investigational products.

Storage and inventory management services hold 22.8% share at USD 1.32 Billion in 2025. Clinical trial depots provide temperature-controlled storage ranging from ambient conditions to ultra-low temperatures for cell therapies. Strategic depot placement reduces transit times and temperature exposure risk. Inventory management platforms integrate demand forecasting, expiry date tracking, and automated replenishment triggers. The rise of precision medicine trials with biomarker-stratified enrollment has increased inventory complexity, requiring sophisticated allocation algorithms to prevent stockouts while minimizing waste.

Manufacturing and comparator sourcing services represent 10.5% market share valued at USD 609 Million in 2025. This segment includes clinical batch manufacturing, formulation development, analytical testing, and procurement of comparator drugs and ancillary supplies. Contract manufacturing organizations provide scalable capacity for Phase I through Phase III production. Comparator sourcing addresses the challenge of obtaining commercial products for active-controlled trials, including management of global supply networks and regulatory documentation.

By Therapeutic Area

Oncology therapeutic area commands the largest share of clinical trial supply chain management demand at 32.4% representing USD 1.88 Billion in 2025. The concentration reflects the pipeline dominance of cancer drugs, which constitute over 35% of all clinical trials registered globally. Oncology trials present unique supply chain challenges including cytotoxic handling requirements, patient-specific dosing for personalized therapies, and rapid enrollment fluctuations. Immuno-oncology agents and antibody-drug conjugates require cold chain logistics, while cell therapies like CAR-T demand cryogenic transport with vein-to-vein tracking.

Central nervous system and neurology trials account for 18.6% share at USD 1.08 Billion in 2025. This segment includes trials for Alzheimer's disease, Parkinson's disease, multiple sclerosis, and psychiatric conditions. Supply chain complexity arises from specialized storage requirements for biologics targeting neurological conditions, controlled substance handling for certain therapeutics, and distribution to diverse clinical sites including academic medical centers and community neurology practices.

Infectious disease and vaccines represent 15.8% market share valued at USD 916 Million in 2025. The segment experienced permanent expansion following COVID-19 vaccine development, with continued investment in pandemic preparedness programs. Vaccine trials require strict cold chain maintenance, often at minus 20 or minus 70 degrees Celsius for mRNA products. Global distribution for infectious disease trials spans endemic regions in Africa, Asia, and Latin America where logistics infrastructure may be limited.

Cardiovascular and metabolic disorders hold 14.2% share at USD 824 Million in 2025. Large-scale outcomes trials for cardiovascular therapies involve thousands of patients across multiple countries, requiring extensive depot networks and inventory management systems. GLP-1 receptor agonist trials for obesity and diabetes have surged, adding demand for cold chain logistics for these injectable biologics.

Rare diseases and orphan drugs account for 11.5% market share at USD 667 Million in 2025. Orphan drug trials present distinct supply chain challenges due to small patient populations dispersed globally, requiring flexible depot strategies and often patient-centric delivery models. Gene therapies targeting rare genetic conditions require specialized cryogenic logistics and site-specific delivery coordination.

Other therapeutic areas including immunology, dermatology, respiratory, and ophthalmology comprise the remaining 7.5% share valued at USD 435 Million in 2025. These segments collectively benefit from expanding pipelines and increasing clinical trial activity across diverse indications.

By End User

Pharmaceutical and biopharmaceutical companies constitute the primary end user segment at 62.5% market share representing USD 3.63 Billion in 2025. Large pharmaceutical sponsors increasingly outsource clinical supply chain functions to specialized providers, retaining strategic oversight while leveraging external expertise and infrastructure. The trend toward integrated supply chain partnerships has accelerated, with sponsors seeking end-to-end service providers capable of managing complexity across global trial portfolios.

Contract research organizations hold 24.3% share at USD 1.41 Billion in 2025. CROs have expanded clinical supply chain capabilities through acquisitions and organic investment to offer sponsors comprehensive trial execution services. Full-service CRO models integrate supply chain management with site management, patient recruitment, and data collection to reduce coordination complexity for sponsors.

Academic and research institutions account for 13.2% market share valued at USD 766 Million in 2025. Investigator-initiated trials and federally funded research programs require specialized supply chain support adapted to academic procurement processes and institutional compliance requirements. Growth in this segment reflects increasing collaboration between academia and industry for early-stage clinical development.

Regional Analysis

North America Clinical Trial Supply Chain Management Market

North America dominates the clinical trial supply chain management market with 42.8% share valued at USD 2.48 Billion in 2025. The region benefits from the highest concentration of pharmaceutical and biotechnology sponsors globally, with the United States alone representing approximately 38% of worldwide clinical trial activity. The United States pharmaceutical supply chain infrastructure includes over 150 Good Distribution Practice-certified clinical trial depots providing nationwide coverage. Canada contributes USD 187 Million to regional revenue, supported by favorable regulatory pathways and clinical research tax incentives. Mexico has emerged as a cost-effective location for clinical trials serving Latin American patient populations, generating USD 94 Million in supply chain services. FDA regulatory requirements for serialization, temperature monitoring, and chain of custody documentation drive continuous investment in compliance capabilities. The region leads adoption of decentralized trial logistics, with direct-to-patient shipments accounting for 28% of clinical supply deliveries in 2025 compared to 18% in Europe and 12% in Asia Pacific.

Europe Clinical Trial Supply Chain Management Market

Europe holds 28.4% market share representing USD 1.65 Billion in 2025 within clinical trial supply chain management. Germany leads regional demand at USD 412 Million, anchored by major pharmaceutical company headquarters and extensive clinical research activity. The United Kingdom maintains a strong position at USD 298 Million despite post-Brexit regulatory adjustments, benefiting from favorable clinical trial governance and life sciences investment incentives. France generates USD 264 Million through its extensive hospital network participating in clinical research. The EU Clinical Trial Regulation implemented in 2022 harmonized requirements across member states, facilitating multi-country trial logistics. European Medicines Agency oversight ensures consistent Good Distribution Practice compliance. The region demonstrates particular strength in rare disease trials supported by European Reference Networks coordinating specialized care across borders. Cold chain infrastructure is well-developed with depot networks providing 24-hour delivery capability to most investigator sites.

Asia Pacific Clinical Trial Supply Chain Management Market

Asia Pacific represents the fastest-growing region at 12.8% CAGR, holding 19.5% market share valued at USD 1.13 Billion in 2025 for clinical trial supply chain management. China dominates regional activity at USD 425 Million, driven by regulatory reforms accelerating drug development timelines and government investment in clinical research infrastructure. Japan contributes USD 312 Million through established pharmaceutical industry presence and sophisticated logistics capabilities. India generates USD 186 Million as a preferred destination for large cardiovascular and diabetes outcomes trials due to treatment-naive patient populations and cost advantages. South Korea and Australia round out key markets with USD 124 Million and USD 86 Million respectively. The region faces infrastructure challenges in emerging markets including cold chain gaps and customs clearance delays, prompting investment in regional depot expansion. Chinese clinical trial supply chain services have grown 35% annually since 2021 following National Medical Products Administration reforms enabling accelerated drug approvals.

Latin America Clinical Trial Supply Chain Management Market

Latin America accounts for 5.8% market share valued at USD 336 Million in 2025 within clinical trial supply chain management. Brazil leads regional demand at USD 156 Million through extensive public hospital networks participating in clinical research. Mexico contributes through its cross-border logistics connections with North American sponsors. Argentina maintains clinical research activity despite economic volatility, generating USD 62 Million in supply chain services. Chile and Colombia emerge as alternative trial locations offering regulatory efficiency and patient access. Regional challenges include customs import delays averaging 5-7 days, temperature excursion risks due to infrastructure limitations, and currency fluctuation impacts on pricing. International logistics providers have established regional hubs in Sao Paulo and Mexico City to address coverage gaps. The region grows at 9.2% CAGR through 2034 as sponsors seek geographic diversification.

Middle East and Africa Clinical Trial Supply Chain Management Market

Middle East and Africa represent 3.5% market share valued at USD 203 Million in 2025 for clinical trial supply chain management. The United Arab Emirates serves as regional logistics hub at USD 58 Million, leveraging Dubai's position as global air cargo transit point with cold chain capabilities. Saudi Arabia generates USD 47 Million through Vision 2030 initiatives promoting clinical research and healthcare infrastructure investment. South Africa anchors Sub-Saharan African activity at USD 52 Million, providing access to diverse patient populations for infectious disease and vaccine trials. Israel contributes through its advanced biotechnology sector and clinical research capabilities. Regional clinical trial activity focuses on infectious diseases endemic to Africa, oncology, and rare genetic conditions prevalent in Middle Eastern populations. Infrastructure development remains ongoing, with investment in temperature-controlled storage and regional depot networks expanding access to previously underserved trial sites.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Service Type

- Logistics and Distribution Services

- Packaging and Labeling Services

- Storage and Inventory Management Services

- Manufacturing and Comparator Sourcing Services

By Therapeutic Area

- Oncology

- Central Nervous System and Neurology

- Infectious Disease and Vaccines

- Cardiovascular and Metabolic Disorders

- Rare Diseases and Orphan Drugs

- Other Therapeutic Areas

By End User

- Pharmaceutical and Biopharmaceutical Companies

- Contract Research Organizations

- Academic and Research Institutions

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.80 B |

| Forecast Revenue (2034) | USD 14.20 B |

| CAGR (2025-2034) | 10.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service Type, (Logistics and Distribution Services, Packaging and Labeling Services, Storage and Inventory Management Services, Manufacturing and Comparator Sourcing Services), By Therapeutic Area, (Oncology, Central Nervous System and Neurology, Infectious Disease and Vaccines, Cardiovascular and Metabolic Disorders, Rare Diseases and Orphan Drugs, Other Therapeutic Areas), By End User, (Pharmaceutical and Biopharmaceutical Companies, Contract Research Organizations, Academic and Research Institutions) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | THERMO FISHER SCIENTIFIC, CATALENT INC., ALMAC GROUP, MARKEN LTD., PCI PHARMA SERVICES, SHARP CLINICAL SERVICES, PAREXEL INTERNATIONAL, WORLD COURIER, YOURWAY TRANSPORT, BIOCAIR, MOVIANTO, CRYOPORT INC., QUICK INTERNATIONAL COURIER, RUBICON LIFE SCIENCES, PATHEON (THERMO FISHER), OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Therapeutic Area (Oncology, CNS & Neurology, Infectious Diseases, Cardiovascular, Rare Diseases), By End User (Pharma & Biopharma Companies, CROs, Academic Institutes) Industry Trends & Forecast 2026–2034")

, By Therapeutic Area (Oncology, CNS & Neurology, Infectious Diseases, Cardiovascular, Rare Diseases), By End User (Pharma & Biopharma Companies, CROs, Academic Institutes) Industry Trends & Forecast 2026–2034")

, By Therapeutic Area (Oncology, CNS & Neurology, Infectious Diseases, Cardiovascular, Rare Diseases), By End User (Pharma & Biopharma Companies, CROs, Academic Institutes) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Clinical Trial Supply Chain Management Market?

Global Clinical trial supply chain market valued at USD 5.25B in 2024, reaching USD 14.2B by 2034, growing at a CAGR of 10.5% from 2026–2034.

Who are the major players in the Clinical Trial Supply Chain Management Market?

THERMO FISHER SCIENTIFIC, CATALENT INC., ALMAC GROUP, MARKEN LTD., PCI PHARMA SERVICES, SHARP CLINICAL SERVICES, PAREXEL INTERNATIONAL, WORLD COURIER, YOURWAY TRANSPORT, BIOCAIR, MOVIANTO, CRYOPORT INC., QUICK INTERNATIONAL COURIER, RUBICON LIFE SCIENCES, PATHEON (THERMO FISHER), OTHERS

Which segments covered the Clinical Trial Supply Chain Management Market?

By Service Type, (Logistics and Distribution Services, Packaging and Labeling Services, Storage and Inventory Management Services, Manufacturing and Comparator Sourcing Services), By Therapeutic Area, (Oncology, Central Nervous System and Neurology, Infectious Disease and Vaccines, Cardiovascular and Metabolic Disorders, Rare Diseases and Orphan Drugs, Other Therapeutic Areas), By End User, (Pharmaceutical and Biopharmaceutical Companies, Contract Research Organizations, Academic and Research Institutions)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Clinical Trial Supply Chain Management Market

Published Date : 15 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date