- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Cloud FinOps Market Size, Share, Trends & Forecast 2034 | 14.9% CAGR

Global Cloud FinOps Market Size, Share, Analysis Report By Component (Services, Solutions), Service Type (SaaS, PaaS, IaaS), Deployment (Hybrid, Private, Public), Enterprise Size (SMEs, Large Enterprises), Industry Vertical (IT & Telecom, Healthcare, Government & Public Sector, BFSI, Retail & Consumer Goods, Manufacturing), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

Report Overview:

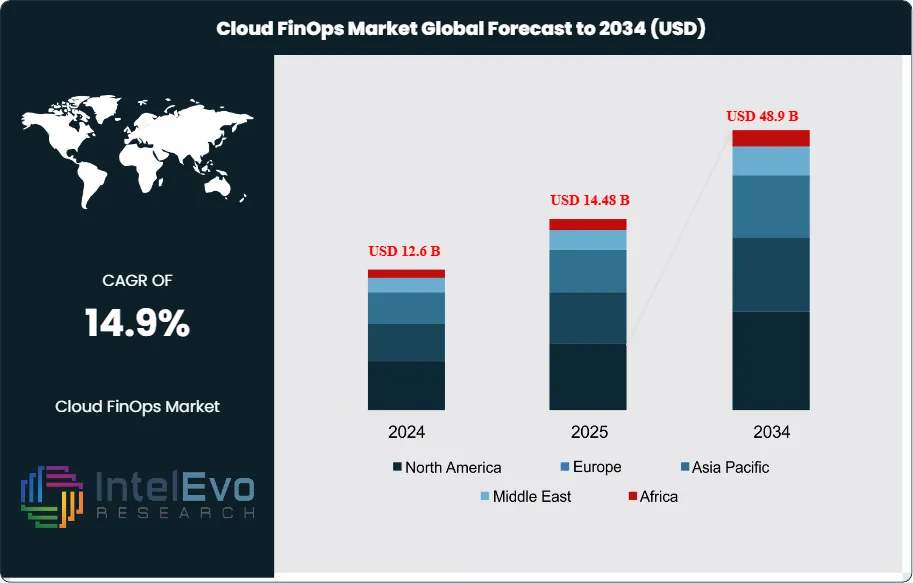

The Global Cloud FinOps Market size is projected to reach approximately USD 48.9 billion by 2034, up from USD 12.6 billion in 2024, growing at a CAGR of 14.9% during the forecast period from 2025 to 2034. As organizations continue to embrace multi-cloud and hybrid cloud infrastructures, the need for optimized financial management tools is surging. Cloud FinOps is emerging as a strategic enabler for enterprises to align cloud costs with business value, improving accountability, governance, and operational efficiency. With AI-powered cost optimization and automation becoming mainstream, the market is witnessing strong adoption across industries like BFSI, IT, and retail.

Get More Information about this report -

Request Free Sample ReportCloud FinOps, short for Cloud Financial Operations, is a practice that combines financial accountability with cloud operations to help organizations manage, optimize, and govern their cloud expenditures. It brings together finance, operations, and engineering teams to collaborate on managing cloud costs while ensuring the maximum value from cloud investments. The primary goal of Cloud FinOps is to provide transparency into cloud spending, optimize resource usage, and align financial decisions with business goals. This includes tasks like cost allocation, optimization of cloud resources, setting budgets, and forecasting future expenditures. By fostering collaboration among different teams and automating monitoring and reporting, Cloud FinOps helps organizations reduce waste, control costs, and ensure efficient resource allocation. It allows businesses to strike a balance between performance needs and cost efficiency, ultimately driving more sustainable and effective cloud usage.

The Cloud FinOps market is experiencing rapid growth, driven by the increasing adoption of cloud computing services across various industries. As more organizations migrate their operations to the cloud, managing and optimizing cloud spending has become more complex, creating a need for advanced financial operations frameworks. Cloud FinOps, which integrates finance, operations, and technology teams to improve financial accountability and optimize cloud costs, is gaining traction. Key drivers of this market growth include the need for enhanced cost visibility and control, the integration of artificial intelligence (AI) and machine learning (ML) for predictive analytics and cost optimization, and the rising demand for budgeting and forecasting tools to manage cloud expenditures more effectively. Additionally, industries like IT, BFSI (Banking, Financial Services, and Insurance), and SaaS are increasingly adopting FinOps practices to improve financial performance in the cloud. North America currently leads the market, with Asia-Pacific expected to experience significant growth due to emerging regulatory requirements and cloud infrastructure development. As the cloud landscape continues to expand, the Cloud FinOps market is set to play a critical role in helping organizations navigate the complexities of cloud financial management and achieve cost-effective operations.

North America stands as a key region in the Cloud FinOps market due to its strong inclination toward adopting cloud technologies across various industries. Businesses in the region are increasingly investing in cloud infrastructure to enhance operational efficiency, driving the demand for FinOps solutions that enable better management and optimization of cloud costs. The region’s robust economic environment, coupled with its advanced technological landscape, supports the rapid adoption of cloud financial management practices. Additionally, stringent regulatory standards around data security and privacy further incentivize companies to implement FinOps to ensure compliance while managing their cloud expenditures effectively. This combination of innovation, regulation, and economic strength makes North America a dominant force in shaping the growth of the Cloud FinOps market.

The COVID-19 pandemic had a significant impact on the Cloud FinOps market, accelerating the adoption of cloud technologies and, consequently, the need for better financial management of cloud resources. The shift to remote work and the rapid digitization of businesses pushed organizations to increasingly rely on cloud services, creating challenges around cloud cost management. This surge in cloud adoption led to greater demand for Cloud FinOps solutions to optimize spending, track usage, and manage resources efficiently.

, Service Type (SaaS, PaaS, IaaS), Deployment (Hybrid, Private, Public), Enterprise Size (SMEs, Large Enterprises), Industry Vertical (IT & Telecom, Healthcare, Government & Public Sector, BFSI, Retail & Consumer Goods, Manufacturing), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Key Takeaways:

- Market Growth: The Cloud FinOps market is expected to reach USD 48.9 billion, growing at a robust CAGR of 14.9%, indicating strong market expansion.

- Component Segment Dominance: The component segment is dominated by solutions, accounting for over 58% of the market share. Cloud FinOps solutions dominate the market due to their ability to optimize and manage cloud spending. IaaS (Infrastructure as a Service) plays a central role in cloud strategies by offering scalable and flexible computing resources, storage, and networking on-demand. Its dominance comes from its ability to support diverse applications and workloads, providing the digital agility and scalability necessary for businesses to succeed in a rapidly evolving landscape.

- Service Type Segment Insights: Infrastructure-as-a-Service (IaaS) is anticipated to hold the largest market share, favored for its lightweight and space-saving properties. The growing e-commerce sector further propels the demand for flexible, sustainable packaging solutions.

- Driver: A major driver of the Cloud FinOps market is the growing need for cost visibility and control in multi-cloud environments. As organizations scale their cloud usage, FinOps helps teams track spending, optimize resources, and align financial goals with cloud operations—making it essential for efficient cloud financial management.

- Restraint: A key restraint in the Cloud FinOps market is the lack of skilled professionals. Implementing effective FinOps practices requires a deep understanding of both finance and cloud operations, and the shortage of talent with this hybrid expertise can hinder adoption and successful execution.

- Opportunity: A major opportunity in the Cloud FinOps market lies in the rising adoption of multi-cloud and hybrid cloud environments. As businesses diversify their cloud infrastructure, the need for centralized cost management and optimization tools grows, opening new avenues for FinOps solutions to provide visibility, governance, and cost control across complex cloud setups.

- Trend: A prominent trend in the Cloud FinOps market is the integration of artificial intelligence (AI) and machine learning (ML) to enhance cost management and forecasting capabilities. Organizations are increasingly leveraging AI-driven analytics to predict cloud usage patterns, detect anomalies, and automate cost optimization processes, thereby improving financial efficiency.

- Regional Analysis: North America leads the Cloud FinOps market due to widespread cloud adoption, a strong focus on cost optimization, and strict regulatory compliance. With major cloud providers and tech-savvy enterprises, the region emphasizes financial accountability and real-time cloud cost management, driving rapid growth in FinOps adoption.

Component Analysis:

The component segment is divided into services and solutions. The solutions segment dominated the market, with a market share of around 58% accounting for 6.7 billion 2024. The dominance of solutions in the Cloud FinOps space is largely due to their ability to offer a comprehensive suite of tools designed to help businesses optimize and manage their cloud expenditures effectively. These solutions integrate critical functions such as cost monitoring, real-time data analysis, budgeting, and forecasting. By doing so, they provide organizations with the insights needed to optimize cloud spending, improve financial governance, and enhance operational efficiency. For businesses looking to leverage the economic advantages of cloud technology while maintaining control over costs, these tools are essential in ensuring both cost-effectiveness and financial transparency in cloud operations.

Service Type Analysis:

The service type segment is divided into Software-as-a-Service (SaaS), Platform-as-a-Service (PaaS), and Infrastructure-as-a-Service (IaaS). The Infrastructure-as-a-Service (IaaS) segment dominated the market, with a market share of around 40% accounting for 4.6 billion 2024. The reason IaaS is so dominant in cloud strategies is due to its adaptability. As businesses grow or face fluctuations in demand, they can quickly adjust their infrastructure without worrying about the limitations of physical hardware. This flexibility allows companies to deploy new applications, services, or systems more efficiently, saving on upfront costs, and providing the agility needed to stay competitive in a fast-paced digital environment. Additionally, IaaS supports a wide range of workloads, from basic computing needs to more complex processes like machine learning, big data analytics, and high-performance computing. This makes it a versatile option for businesses across industries, helping them manage and scale their IT resources based on specific requirements.

Deployment Analysis:

The deployment segment is divided into hybrid, private, and public. The public segment dominated the market, with a market share of around 42% accounting for 4.9 billion 2024. The public cloud has become dominant due to its ease of access and cost-effectiveness. It provides businesses with the ability to access cloud services without the need for extensive infrastructure investment. The pay-as-you-go model allows organizations to only pay for the resources they use, making it highly scalable and adaptable to real-time needs. This flexibility makes public clouds a natural fit for FinOps, as they enable companies to closely monitor and optimize cloud costs. By adjusting resources based on demand, organizations can better align their cloud spending with actual usage, leading to more efficient financial management and cost control.

Enterprise Size Analysis:

The enterprise size segment is divided into SMEs and large enterprises. The large enterprises segment dominated the market, with a market share of around 55% accounting for 6.4 billion 2024. Large enterprises typically operate across multiple departments and regions, leading to complex cloud usage and significant expenditures. FinOps solutions help these organizations gain visibility into their cloud costs, allocate resources more effectively, and implement cost-saving strategies. With robust tools for monitoring and optimization, large enterprises can ensure efficient cloud spending while maintaining performance and compliance across their global operations.

End User Analysis:

The industry vertical segment is divided into IT & telecom, healthcare, government & public sector, BFSI, retail & consumer goods, manufacturing, and others. The BFSI segment dominated the market, with a market share of around 21% accounting for 2.4 billion 2024. The BFSI sector leads the Cloud FinOps market due to its high demands for data security, regulatory compliance, and scalable IT infrastructure. Financial institutions are adopting cloud technologies to boost innovation, improve customer service, and manage costs effectively. FinOps practices help them monitor cloud usage, ensure compliance, and optimize spending. Additionally, the sector’s use of advanced tools like AI and analytics supports real-time insights and personalized services, further driving cloud adoption.

Region Analysis:

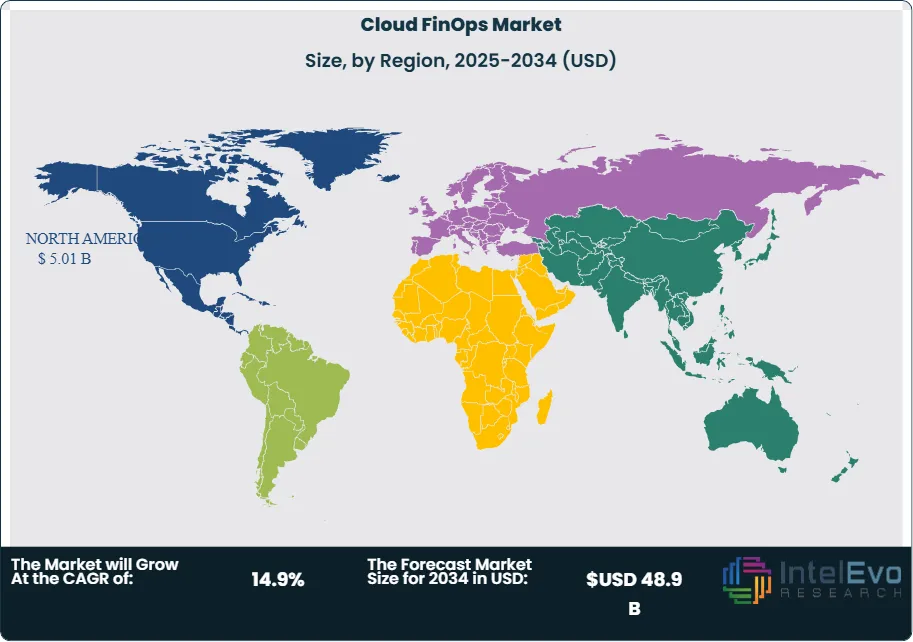

North America Leads With 39.8% Market Share in the Cloud FinOps Market: Cloud FinOps is gaining significant traction in North America due to the region's rapid adoption of cloud technologies and its strong emphasis on cost efficiency and compliance. As businesses increasingly migrate their operations to the cloud, there is a growing need to manage and optimize cloud spending effectively. This has led to widespread adoption of Cloud FinOps—an operational framework that combines financial accountability with cloud engineering and operations to drive cost optimization. North America, particularly the United States and Canada, has a highly developed cloud ecosystem supported by major players like AWS, Microsoft Azure, and Google Cloud. Enterprises in this region prioritize cloud cost visibility, budgeting, and forecasting to align their cloud investments with business goals. Moreover, strict regulatory requirements related to data privacy and security further push organizations to implement structured FinOps practices. The region’s culture of innovation, large enterprise presence, and advanced IT infrastructure are key enablers for the Cloud FinOps market. As organizations continue to expand their cloud footprint, the demand for real-time financial insights and governance tools will continue to grow, solidifying North America’s position as a leader in the global Cloud FinOps space.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Component

- Services

- Solutions

By Service Type

- Software-as-a-Service (SaaS)

- Platform-as-a-Service (PaaS)

- Infrastructure-as-a-Service (IaaS)

By Deployment Mode

- Public Cloud

- Private Cloud

- Hybrid Cloud

- Multi-Cloud

By Enterprise Size

- Large Enterprises

- Small & Medium-Sized Enterprises (SMEs)

By Application

- Cost Optimization & Budget Management

- Resource Allocation & Utilization

- Cloud Governance & Compliance

- Cloud Financial Visibility & Forecasting

- Workflow Automation & Policy Enforcement

By End User

- Banking, Financial Services & Insurance (BFSI)

- Information Technology (IT) & Telecom

- Retail & E-commerce

- Healthcare & Life Sciences

- Manufacturing

- Government & Public Sector

- Others (Media, Education, Energy, etc.)

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 14.48 B |

| Forecast Revenue (2034) | USD 48.9 B |

| CAGR (2025-2034) | 14.9% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component (Services, Solutions), By Service Type (Software-as-a-Service (SaaS), Platform-as-a-Service (PaaS), Infrastructure-as-a-Service (IaaS)), By Deployment Mode (Public Cloud, Private Cloud, Hybrid Cloud, Multi-Cloud), By Enterprise Size (Large Enterprises, Small & Medium-Sized Enterprises (SMEs)), By Application (Cost Optimization & Budget Management, Resource Allocation & Utilization, Cloud Governance & Compliance, Cloud Financial Visibility & Forecasting, Workflow Automation & Policy Enforcement), By End User (Banking, Financial Services & Insurance (BFSI), Information Technology (IT) & Telecom, Retail & E-commerce, Healthcare & Life Sciences, Manufacturing, Government & Public Sector, Others (Media, Education, Energy, etc.) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Amdocs, Apptio Inc., HCL, KubeCost, AWS, IBM, Oracle, SoftwareOne, Nagarro, Flexera, Nordcloud Oy, Microsoft, Google, Amazon, Atlassian, Broadcom, Dynatrace, HashiCorp, NetApp, SAP, Splunk, ServiceNow, Virtana, Anodot, CloudBolt Software, Nutanix |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Service Type (SaaS, PaaS, IaaS), Deployment (Hybrid, Private, Public), Enterprise Size (SMEs, Large Enterprises), Industry Vertical (IT & Telecom, Healthcare, Government & Public Sector, BFSI, Retail & Consumer Goods, Manufacturing), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Service Type (SaaS, PaaS, IaaS), Deployment (Hybrid, Private, Public), Enterprise Size (SMEs, Large Enterprises), Industry Vertical (IT & Telecom, Healthcare, Government & Public Sector, BFSI, Retail & Consumer Goods, Manufacturing), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Service Type (SaaS, PaaS, IaaS), Deployment (Hybrid, Private, Public), Enterprise Size (SMEs, Large Enterprises), Industry Vertical (IT & Telecom, Healthcare, Government & Public Sector, BFSI, Retail & Consumer Goods, Manufacturing), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Frequently Asked Questions

How big is the Cloud FinOps Market?

Explore the Global Cloud FinOps Market growth, size, and forecast to 2034. Discover key trends, AI-driven cost optimization tools, and leading players shaping cloud finance.

Who are the major players in the Cloud FinOps Market?

Amdocs, Apptio Inc., HCL, KubeCost, AWS, IBM, Oracle, SoftwareOne, Nagarro, Flexera, Nordcloud Oy, Microsoft, Google, Amazon, Atlassian, Broadcom, Dynatrace, HashiCorp, NetApp, SAP, Splunk, ServiceNow, Virtana, Anodot, CloudBolt Software, Nutanix

Which segments covered the Cloud FinOps Market?

By Component (Services, Solutions), By Service Type (Software-as-a-Service (SaaS), Platform-as-a-Service (PaaS), Infrastructure-as-a-Service (IaaS)), By Deployment Mode (Public Cloud, Private Cloud, Hybrid Cloud, Multi-Cloud), By Enterprise Size (Large Enterprises, Small & Medium-Sized Enterprises (SMEs)), By Application (Cost Optimization & Budget Management, Resource Allocation & Utilization, Cloud Governance & Compliance, Cloud Financial Visibility & Forecasting, Workflow Automation & Policy Enforcement), By End User (Banking, Financial Services & Insurance (BFSI), Information Technology (IT) & Telecom, Retail & E-commerce, Healthcare & Life Sciences, Manufacturing, Government & Public Sector, Others (Media, Education, Energy, etc.)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date