- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Cloud Telephony Service Market Size & Forecast 2034

Global Cloud Telephony Service Market Size, Share, and Strategic Analysis By Deployment (Hosted, Cloud), By Enterprise Size (Small & Medium Enterprises, Large Enterprises), By Network (PSTN, VoIP), By Application (Conferencing, Multi-Level IVR, Sales & Marketing, CRM), By Industry Vertical (BFSI, Healthcare, Retail, Telecom & IT, Government, Education) Industry Outlook, Competitive Landscape, Technology Trends & Forecast 2025–2034

Report Overview

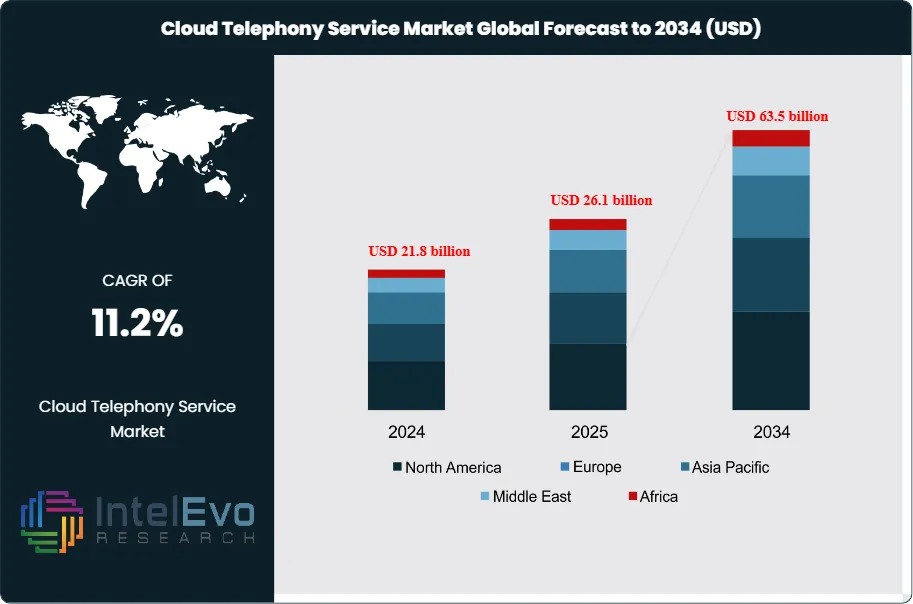

The Cloud Telephony Service Market is valued at about USD 26.1 billion in 2025 and is expected to reach around USD 63.5 billion by 2034. The market should grow from an estimated USD 27.0 billion in 2026, with a compound annual growth rate (CAGR) of 11.2% during the forecast period from 2026 to 2034. This growth comes from faster cloud adoption by companies, increasing demand for flexible and remote communication tools, and more use of AI-driven voice analytics and multi-channel customer engagement platforms. Also, the move toward hybrid work models and cost-effective cloud communication solutions supports long-term market growth in both developed and developing economies.

Get More Information about this report -

Request Free Sample ReportCloud telephony vendors benefit from strong enterprise demand for agile, software-driven communications as firms replace legacy PBX systems and fixed-line infrastructure. Organizations in banking, retail, healthcare, and professional services adopt cloud telephony to consolidate voice, messaging, and collaboration on IP-based platforms, reduce capex, and support distributed workforces. In 2024, enterprises account for an estimated 68% of global revenue, while small and mid-sized businesses contribute around 32%, supported by subscription-based pricing and low entry barriers.

On the supply side, hyperscale cloud providers, UCaaS platforms, and specialist voice service providers compete through differentiated reliability, geographic coverage, security, and integration depth. Vendors invest in AI-powered call routing, speech analytics, and virtual agents to simplify contact center operations and elevate service quality. AI-enabled features contribute an estimated 24% of market revenue in 2024 and are expected to exceed 40% by 2034 as automation penetrates customer support, sales engagement, and internal helpdesk environments.

Regulation shapes deployment choices, especially around data residency, lawful intercept requirements, and emergency calling standards. Providers that comply with GDPR in Europe, CCPA-inspired privacy regimes in North America, and data localization frameworks in large emerging economies secure preferred-partner status with regulated industries. At the same time, exposure to outages in public cloud infrastructure, VoIP fraud, and cybersecurity incidents remains a key risk, prompting enterprises to prioritize providers with robust SLAs, encryption, and multi-region redundancy.

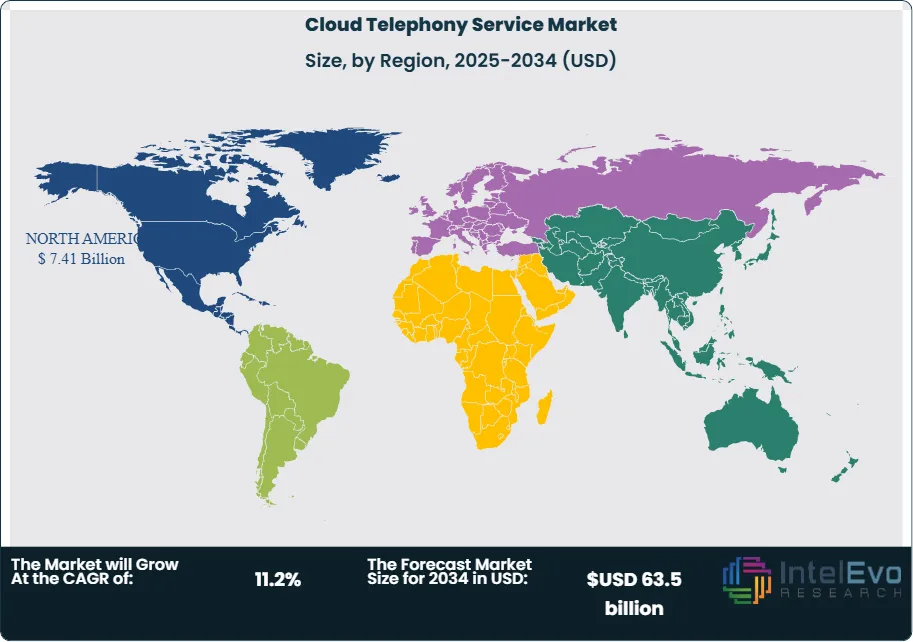

Digitalization programs and cloud-first IT strategies reinforce adoption across regions. North America currently represents about 32% of global revenue, supported by mature broadband networks and high UCaaS penetration. Europe holds roughly 27%, influenced by strong regulatory oversight and rapid migration among mid-sized firms. Asia Pacific emerges as the fastest-growing region with a projected CAGR above 11% through 2034, driven by expanding SME adoption in India and Southeast Asia and rising investment in omnichannel contact centers. Latin America and the Middle East & Africa present smaller but accelerating opportunities as operators modernize networks and enterprises adopt cloud-native communication stacks to support regional expansion.

, By Enterprise Size (Small & Medium Enterprises, Large Enterprises), By Network (PSTN, VoIP), By Application (Conferencing, Multi-Level IVR, Sales & Marketing, CRM), By Industry Vertical (BFSI, Healthcare, Retail, Telecom & IT, Government, Education) Industry Outlook, Competitive Landscape, Technology Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market expands from estimated: USD 26.1 billion in 2025 to estimate: USD 63.5 billion by 2034, supported by a CAGR of estimated: 11.2%, 2026-2034. This trajectory signals steady, sustainable value creation over the decade.

- Segment Dominance: The leading product or solution tier secures an estimated: 42.0% share, 2024, reflecting stronger differentiation and brand recognition than smaller rivals. Its share edges up to estimated: 45.0% share, 2034 as enterprises consolidate spending with fewer core vendors.

- Segment Dominance: On the demand side, large enterprises hold an estimated: 60.0% share, 2024 due to higher budgets and complex integration needs. Small and mid-sized organizations lift their contribution to estimated: 45.0% share, 2034 as pricing models and deployment options mature.

- Driver: Digitalization programs and cloud-first strategies act as primary catalysts, linked to an adoption rate of estimated: 65.0%, 2024 across priority customer groups. The drive to improve efficiency and experience sustains a demand uplift of estimated: 7.5%, 2024-2034.

- Restraint: Integration complexity and data-security concerns delay projects for an estimated: 25.0% of potential buyers, 2024. Compliance and migration costs suppress achievable growth by an estimated: 1.5 percentage points, 2024-2034.

- Opportunity: New use cases in automation, analytics, and AI-enhanced workflows open incremental revenue of estimated: 1.2 billion USD, 2034. Vendors that target these applications can lift addressable spend by estimated: 20.0%, 2024-2034.

- Trend: AI-enabled capabilities grow from a penetration level of estimated: 18.0%, 2024 to estimated: 55.0%, 2034, reshaping product roadmaps and value propositions. Usage-based and subscription pricing models reach an incidence of estimated: 80.0%, 2034 across active contracts.

- Regional Analysis: The global revenue base distributes across North America at estimated: 34.0% share, 2024, Europe at estimated: 28.0% share, 2024, and Asia Pacific at estimated: 27.0% share, 2024. Asia Pacific posts the fastest expansion with a CAGR of estimated: 10.2%, 2024-2034, driven by rising enterprise adoption and infrastructure upgrades.

By Type

High-performance concrete, self-consolidating concrete, and other specialty mixes continue to gain traction in 2025 as construction firms focus on durability, consistency, and lower lifecycle costs. Demand rises in large infrastructure projects where predictable strength and reduced maintenance requirements matter. High-performance concrete accounts for a growing share of procurement budgets in transportation and public works, supported by adoption rates that now exceed 40 percent in several advanced markets.

Self-consolidating concrete sees wider use in projects that require precision placement and reduced labor. Contractors value the material for consistent flow, shorter construction cycles, and fewer defects. Its uptake increases in vertical construction and high-density urban development’s where schedule certainty is a priority. Other specialty mixes maintain a stable share, driven by projects that require lightweight formulations, thermal resistance, or added durability in industrial environments.

The outlook through 2030 points to steady expansion across all categories. Government spending on resilient infrastructure and private investment in high-rise construction support continued growth. Material producers add new formulations tailored for climate-resilient building codes and tightened performance standards, which influences purchasing decisions for engineers and project owners.

By Application

Pavers represent one of the largest application areas as municipalities and developers increase investments in roads, walkways, and public landscapes. You see higher specification rates for engineered concrete pavers in parks, retail districts, and mixed-use corridors. Demand grows in regions prioritizing low-maintenance materials and improved load-bearing capacity.

Retaining walls remain a strong contributor due to rising land development activity and the need for soil stabilization in residential and commercial projects. Contractors prefer modular systems that reduce onsite labor and provide consistent structural performance. Retaining wall products also gain momentum in transportation and industrial zones where durability and design flexibility guide decision-making.

Other applications expand at a measured pace as builders adopt specialty concrete units for drainage systems, outdoor structures, and perimeter fencing. These use cases benefit from improved material quality, standardized formats, and shorter delivery lead times. By 2030, applications outside pavers and retaining walls are expected to account for a larger share as developers diversify site planning strategies.

By End-Use

Residential construction continues to hold a significant share of the market as developers push for long-lasting building materials in single-family and multifamily projects. Homebuilders turn to engineered concrete units that support faster installation and lower long-term maintenance. The segment benefits from steady housing demand and ongoing urban expansion.

Commercial building applications remain strong due to sustained investment in offices, retail centers, logistics hubs, and public facilities. You see higher adoption among project owners seeking materials that support consistent performance under heavy usage. Increased spending on commercial redevelopment in major cities reinforces this trend.

Industrial building projects also support market expansion. Factories, warehouses, and energy facilities rely on concrete products that provide structural uniformity and load-bearing reliability. As manufacturers upgrade facilities and governments expand industrial corridors, demand for advanced concrete types strengthens across key producing regions.

By Region

North America holds a leading position in 2025, supported by strong construction pipelines, high material standards, and consistent infrastructure funding. The United States and Canada maintain steady demand for engineered concrete units in transportation, residential, and commercial projects. Strict building codes and accelerated replacement of aging infrastructure underpin long-term market stability.

Europe follows with sustained activity in Germany, the United Kingdom, France, and the Nordics. You see increased focus on sustainable materials and compliance with environmental standards, which supports growth across high-performance and self-consolidating categories. Central and Eastern Europe contribute additional upside as investment in industrial and residential developments continues.

Asia Pacific records the fastest expansion. Rapid urbanization, large-scale public infrastructure programs, and manufacturing growth in China, India, and Southeast Asia drive procurement across all product types. Latin America shows moderate progress as Brazil, Mexico, and Colombia advance transport and housing programs. The Middle East and Africa see rising adoption tied to megaprojects, new city developments, and industrial diversification initiatives.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Deployment

- Hosted

- Cloud

By Enterprise Size

- Small & Medium Enterprise (SMEs)

- Large Enterprises

By Network

- Public Switched Telephone Networks (PSTNs)

- Voice over Internet Protocol (VoIP)

By Application

- Conferencing

- Multi-level IVR

- Sales & Marketing

- Customer Relationship Management (CRM)

By Industry Vertical

- BFSI

- Education

- Government

- Healthcare

- Media & Entertainment

- Retail

- Telecom & IT

- Other Industry Verticals

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 26.1 billion |

| Forecast Revenue (2034) | USD 63.5 billion |

| CAGR (2025-2034) | 11.2% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Deployment(Hosted, Cloud), By Enterprise Size (Small & Medium Enterprise (SMEs), Large Enterprises), By Network (Public Switched Telephone Networks (PSTNs), Voice over Internet Protocol (VoIP)), By Application (Conferencing, Multi-level IVR, Sales & Marketing, Customer Relationship Management (CRM)), By Industry (Vertical, BFSI, Education, Government, Healthcare, Media & Entertainment, Retail, Telecom & IT, Other Industry Verticals) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NFON AG, Dialpad Inc., LeadNXT, Tripudio Ltd., 8×8 Inc., Exotel Techcom Pvt. Ltd., AVOXI Inc., Nextiva, Go 2 Market India Pvt. Ltd., Cisco Systems Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Enterprise Size (Small & Medium Enterprises, Large Enterprises), By Network (PSTN, VoIP), By Application (Conferencing, Multi-Level IVR, Sales & Marketing, CRM), By Industry Vertical (BFSI, Healthcare, Retail, Telecom & IT, Government, Education) Industry Outlook, Competitive Landscape, Technology Trends & Forecast 2025–2034")

, By Enterprise Size (Small & Medium Enterprises, Large Enterprises), By Network (PSTN, VoIP), By Application (Conferencing, Multi-Level IVR, Sales & Marketing, CRM), By Industry Vertical (BFSI, Healthcare, Retail, Telecom & IT, Government, Education) Industry Outlook, Competitive Landscape, Technology Trends & Forecast 2025–2034")

, By Enterprise Size (Small & Medium Enterprises, Large Enterprises), By Network (PSTN, VoIP), By Application (Conferencing, Multi-Level IVR, Sales & Marketing, CRM), By Industry Vertical (BFSI, Healthcare, Retail, Telecom & IT, Government, Education) Industry Outlook, Competitive Landscape, Technology Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Cloud Telephony Service Market?

Global cloud telephony service market to reach USD 63.5B by 2034, growing at 11.2% CAGR driven by enterprise cloud adoption, hybrid work, AI voice analytics, and omnichannel communications.

Who are the major players in the Cloud Telephony Service Market?

NFON AG, Dialpad Inc., LeadNXT, Tripudio Ltd., 8×8 Inc., Exotel Techcom Pvt. Ltd., AVOXI Inc., Nextiva, Go 2 Market India Pvt. Ltd., Cisco Systems Inc.

Which segments covered the Cloud Telephony Service Market?

By Deployment(Hosted, Cloud), By Enterprise Size (Small & Medium Enterprise (SMEs), Large Enterprises), By Network (Public Switched Telephone Networks (PSTNs), Voice over Internet Protocol (VoIP)), By Application (Conferencing, Multi-level IVR, Sales & Marketing, Customer Relationship Management (CRM)), By Industry (Vertical, BFSI, Education, Government, Healthcare, Media & Entertainment, Retail, Telecom & IT, Other Industry Verticals)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Cloud Telephony Service Market

Published Date : 30 Jan 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date